If you’ve been exploring opportunities in the consumer loan space and are curious about the Esketit platform, then you’re in the right place.

Esketit is a fintech company that has carved out a position in the European consumer loan market. Their focus is on providing transparent and accessible financing solutions to borrowers, while also offering investors like us the opportunity to participate in this space. As someone who’s always keen on exploring investment opportunities, I’ve been following the platform since its early days.

Esketit was founded in December 2020 by Davis Barons and Matiss Ansviesulis, and the company is registered in Ireland. Davis and Matiss also established the Latvia-based AvaFin Group (formerly known as Creamfinance), an international non-bank lender in the consumer loans sector. However, in a significant development in 2025, AvaFin withdrew from P2P lending operations, and Esketit now operates independently. This is a notable shift from the platform’s earlier setup, where the backing of the parent company was a key selling point.

Affiliated loan originators issue the loans on Esketit, ensuring transparency and easy oversight throughout the entire process. Davis and Matiss have historically adopted a ‘skin in the game’ strategy, though the dynamics of this have shifted with AvaFin’s departure from P2P.

Investing in personal loans through the Esketit Platform is straightforward. The platform continues to operate across multiple markets and has been adding new loan originators to diversify its offerings. In February 2026, Jet Finance launched on the platform, offering vehicle-backed loans from Central Asia — a sign that Esketit is actively working to replace departed originators and expand its geographic reach.

Esketit at a Glance

| Founded | 2020 |

| Country | Ireland (registered) |

| Regulation | ECSP licensed |

| Average Returns | 10-14% annually |

| Buyback Guarantee | Yes (60 days) |

| Secondary Market | Yes |

| Auto-Invest | Yes |

| Min. Investment | EUR 10 |

| Loan Types | Consumer loans, auto loans, vehicle-backed loans |

| Parent Company | Independent (formerly backed by AvaFin/Creamfinance) |

The Investment Process

The Esketit platform streamlines the process of investing in consumer loans. To start, you’ll need to create an account and complete the necessary verification steps. Once you’re all set, you can browse the available loans on the platform, assess the risk levels and potential returns, and decide which loans to invest in.

What I appreciate about Esketit is the detailed information they provide about each loan, such as the borrower’s credit score, loan purpose, and repayment history. This transparency allows investors like us to make informed decisions and effectively manage the risk-reward balance.

Both individuals and corporate entities can invest in Esketit, and both will need to pass a straightforward KYC process, as is customary with all P2P lending platforms that are regulated.

Founders’ Skin in the Game

The founders of Esketit, Davis Barons and Matiss Ansviesulis, follow a “skin in the game” approach. This means that they invest their own money alongside the investors on the platform. By co-investing, the founders demonstrate their confidence in the platform’s performance and align their interests with those of other investors. This approach adds a layer of assurance for investors using the Esketit platform, as the founders have a personal stake in ensuring the platform’s success and the quality of the investment opportunities offered.

Team Competencies

As noted, Davis and Matiss bring significant experience to Esketit from their years building AvaFin.

In July 2025, Ieva Grigalune took over as CEO of the Esketit platform, replacing Vitalijs Zalovs who had served in the role since April 2021. Vitalijs was a recognized figure in the sector, having previously dedicated six years to the Latvian P2P marketplace Mintos as Head of Investor Relations. I had the pleasure of speaking with him many times in his role at Esketit.

The leadership transition came during a period of significant change for the platform, coinciding with AvaFin’s withdrawal from P2P operations. Ieva faces the challenge of steering Esketit through its new phase of independence.

Diversification Opportunities

One key aspect of successful investing is diversification, and Esketit doesn’t disappoint in this regard. The platform offers a wide variety of consumer loans, including personal loans, auto loans, and home improvement loans, among others. This variety allows investors to build a diversified portfolio and spread their risk across different loan types and borrowers.

Auto-Invest Feature

Esketit’s auto-invest feature is something I find particularly appealing. This tool allows you to set specific investment criteria and automatically allocate funds to loans that match your preferences. It’s a real time-saver for busy investors like me who want to maintain a diversified portfolio without having to constantly monitor and manually invest in individual loans.

Returns and Risk Management

Esketit offers competitive returns compared to traditional investment options, with annualized yields typically ranging from 5% to 15%, depending on the risk profile of the loans you choose to invest in. Of course, higher returns come with higher risks, so it’s essential to be diligent in your loan selection process and employ proper risk management techniques.

To help mitigate risk, Esketit employs strict underwriting standards and performs thorough due diligence on all borrowers. Additionally, the platform offers a secondary market where you can sell your investments before the loan term ends, providing liquidity in case you need to exit your investment early.

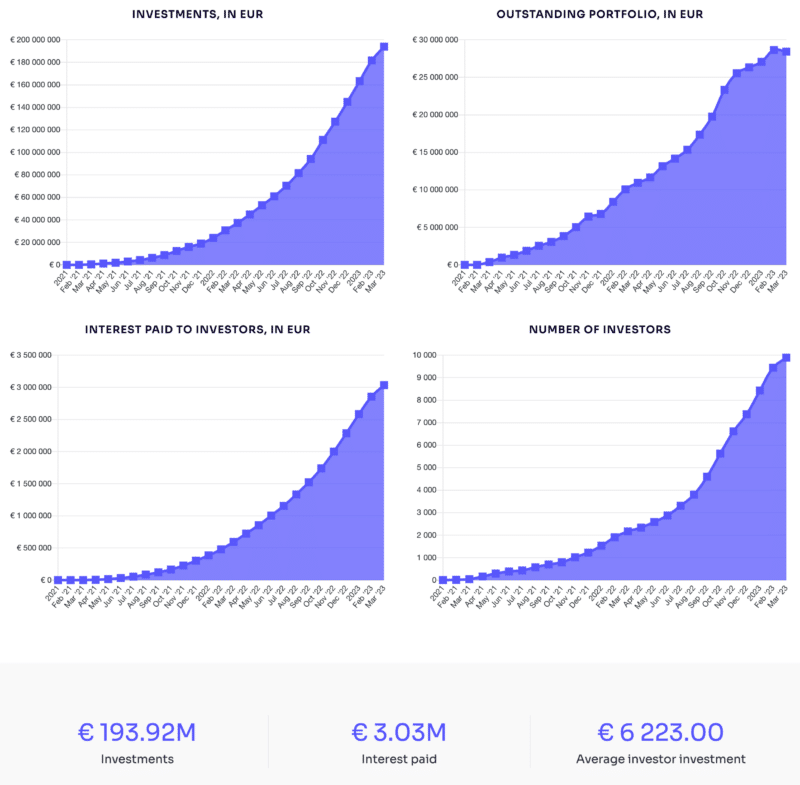

Esketit are completely transparent about their numbers and publish them monthly on their statistics page.

Customer Support

From my experience, Esketit’s customer support has been responsive and helpful. They offer multiple channels for communication, including email, phone, and live chat. This level of support is comforting, as it ensures that any questions or concerns you may have as an investor are addressed promptly.

Some Drawbacks to Consider

No investment platform is perfect, and Esketit has its drawbacks as well. One thing to keep in mind is that investing in consumer loans involves a certain level of risk, and there’s always the possibility of borrowers defaulting on their loans. It’s essential to be aware of these risks and manage your investment strategy accordingly.

More significantly, 2025 brought some structural changes that investors should be aware of. AvaFin (the former Creamfinance) withdrew from P2P operations, meaning Esketit no longer benefits from the direct backing of a large, profitable parent company. The MFF loan originator also ceased P2P operations, reducing the platform’s loan supply. As a result, the total portfolio experienced its first annual decline, going from EUR 48 million to EUR 45 million.

While Esketit is working to replace departed originators — Jet Finance launched in February 2026 with vehicle-backed loans from Central Asia — investors should understand that the platform is in a transitional period. The “startup backed by a profitable lending group” narrative no longer applies in the same way. With over five years of operations behind it, Esketit has proven it can operate, but the question now is whether it can sustain and grow as an independent platform.

How Does Esketit Compare?

See how Esketit stacks up against other popular platforms:

- Mintos vs Esketit — Which Is Better in 2026?

- PeerBerry vs Esketit — Which Is Better in 2026?

- Esketit vs ViaInvest — Which Is Better in 2026?

- Esketit vs Lonvest — Which Is Better in 2026?

Alternatives to Esketit

Esketit faces competition from several other prominent platforms in the European P2P lending and investment industry.

- Mintos, a well-established player in the market, offers a wide range of investment opportunities in loans issued by various loan originators.

- Bondora, another competitor, has been operating since 2009, providing access to consumer loans from multiple European countries.

- PeerBerry, a relatively newer platform, focuses on short-term consumer loans with a buyback guarantee, catering to investors seeking lower-risk investment options. Each of these platforms has its unique selling points, such as the range of loan types, geographical diversification, and risk management features. Investors should carefully consider their specific needs and preferences when choosing a platform to diversify their portfolios in the growing P2P lending space.

Frequently Asked Questions

Is Esketit safe to invest in?

Esketit holds an ECSP license, which provides a level of regulatory oversight. The platform has been operating since 2020 and has a track record of honoring buyback guarantees. However, AvaFin’s withdrawal from P2P operations in 2025 means Esketit now operates independently, which changes its risk profile. As with all P2P platforms, your capital is at risk.

What happened with AvaFin and Esketit?

AvaFin (formerly Creamfinance), the lending group that founded Esketit, withdrew from P2P lending operations in 2025. This means Esketit no longer benefits from the direct backing of its former parent company and now operates independently with new loan originators.

What returns can I earn on Esketit?

Returns on Esketit typically range from 10% to 14% annually, depending on the loan type and risk level you select. New investors can get a 0.5% cashback bonus for the first 90 days after registration.

Does Esketit have a buyback guarantee?

Yes, Esketit offers a buyback guarantee. If a borrower is more than 60 days late on repayment, the loan originator repurchases the loan, covering both principal and accrued interest.

How does Esketit compare to PeerBerry?

Both platforms offer similar returns (10-14%) and buyback guarantees. PeerBerry is larger (EUR 3.24B funded vs Esketit’s smaller portfolio) and has a longer track record. Esketit offers a secondary market while PeerBerry does not. Esketit is ECSP licensed, which PeerBerry is not.

Final Thoughts

Overall, Esketit remains an interesting platform in the consumer loan space. The platform offers a streamlined process, detailed loan information, and attractive diversification opportunities. The auto-invest feature and competitive returns make it an appealing option for investors seeking exposure to this market.

I like the platform’s design and ease-of-use — that’s definitely something that is important for such a platform, especially if an investor is new to P2P lending and is trying to learn the ropes.

Withdrawing money is fast and reliable, as are deposits, so you can put your money to work with no hassle. The buyback guarantee is an extra measure of safety, although this is not unique to Esketit.

That said, 2025 was a pivotal year. The departure of AvaFin from P2P, the loss of MFF as a loan originator, the CEO change, and the first portfolio decline all represent meaningful shifts. These aren’t reasons to panic, but they do warrant attention. The platform is clearly in a transitional period as it establishes its independence.

The addition of Jet Finance in February 2026 is encouraging and shows that the team is actively working to diversify and grow the loan supply. But investors should monitor how this transition unfolds and adjust their exposure accordingly.

If you’re an investor looking for an alternative investment opportunity in the consumer loan market, Esketit is still worth considering — but with a clearer understanding that the platform’s risk profile has evolved since its earlier days. As always, do your own research and make sure your investments align with your overall financial goals and risk tolerance.

If you consider investing on Esketit, a sign up through this link will enable you to get an unlimited cashback bonus of 0,5% in the first 90 days after registration.

Summary

AvaFin withdrew from P2P, portfolio declining, lost secondary market after Croatia relocation. New CEO from Mintos but platform rated D grade and named major loser of 2025. Only for those already invested. Do not add new funds until trajectory improves.

Pros

- Transparency in loan origination and investment process

- Founders co-invest, aligning their interests with investors

- Diversification across multiple markets

- User-friendly platform for both novice and experienced investors

- Access to a growing industry (P2P lending)

Cons

- Relatively new platform with limited track record

- Investment is restricted to consumer loans, lacking other asset classes

- May not be suitable for investors seeking a hands-on approach or direct control over individual investments

- Platform's success depends on the performance of affiliated loan originators

- Potential regulatory risks associated with P2P lending industry

Related

Leave a Reply