I’ve been investing in European P2P lending for years, through the good times and the platform collapses. This guide is everything I wish I’d known when I started: how it actually works, what returns are realistic, where the real risks hide, and how to build a portfolio that survives when one platform inevitably disappoints you.

If you’re after specific recommendations rather than the full picture, jump straight to the best European P2P lending platforms for 2026. Otherwise, read on.

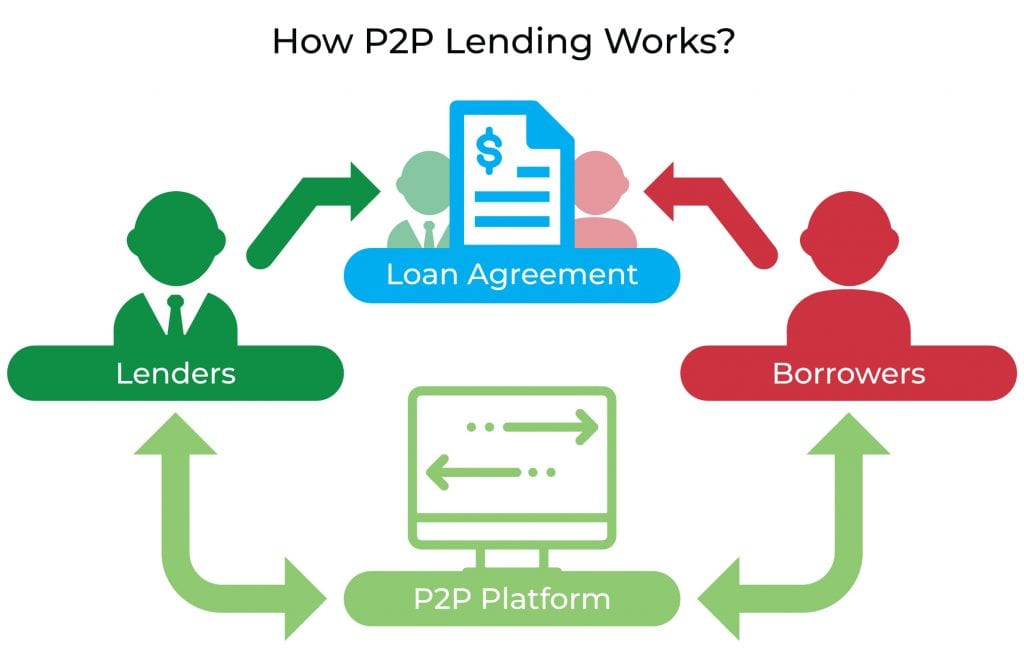

What Is P2P Lending?

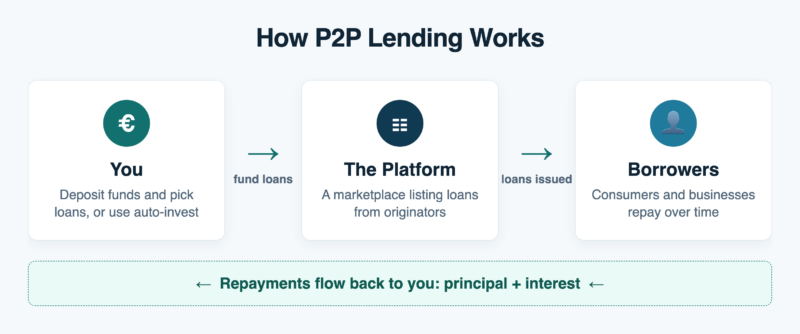

Peer-to-peer lending connects people who want to lend money with people who want to borrow it, cutting out the bank in the middle. You, the investor, fund small slices of loans. Borrowers repay the principal plus interest over time, and that interest is your return.

In Europe, most platforms don’t originate the loans themselves. They act as a marketplace: loan originators (consumer lenders, car-finance firms, agricultural lenders) issue the loans, then list them on a platform like Mintos or Nectaro for investors to fund. You’re effectively buying exposure to a pool of loans, often with a buyback guarantee from the originator if a borrower defaults.

The mechanics are simple from your side: you deposit money, choose loans manually or let an auto-invest tool spread it for you, and interest accrues as borrowers repay. Most platforms let you start with as little as €10 to €50.

How P2P Platforms Make Money

Platforms earn from the spread and from fees charged to loan originators or borrowers, not usually from you. Many European platforms are free for investors, with no deposit, account, or investment fees. A few charge a small fee to sell loans early on a secondary market. Always read the fee page, but the headline rate you see is generally what you earn.

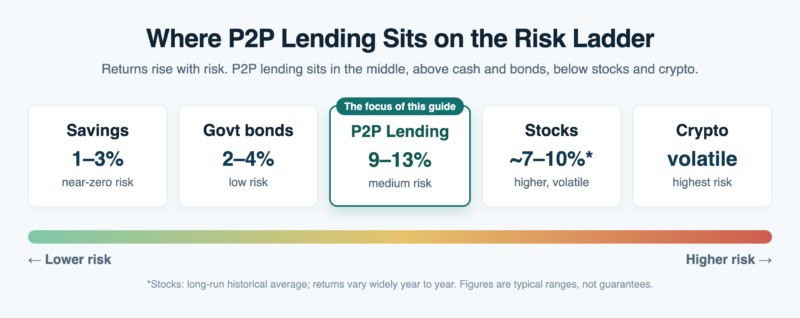

What Returns Can You Expect?

European consumer P2P lending has settled into a fairly consistent band. In 2026, advertised net returns on the major platforms run roughly:

- 9% to 11% on large, diversified consumer-loan platforms

- 11% to 13% on higher-yield platforms and shorter-term loans

- Occasionally higher on niche or business/property loans, with correspondingly higher risk

These are not guaranteed. The advertised rate assumes borrowers repay and, where offered, that buyback guarantees are honoured. Treat the headline number as a best case and expect your realised return to be a little lower once you account for cash drag (idle money waiting to be invested) and the occasional loss.

Is P2P Lending Safe? The Real Risks

P2P lending is not a savings account. Your capital is at risk, there’s no deposit insurance, and the failures I’ve watched over the years were almost never about individual borrowers defaulting. They were about the platform or the loan originator. The risks worth understanding:

- Platform risk: the platform itself goes bust or is fraudulent. This is the one that wipes people out. Stick to established, regulated platforms with a real track record.

- Loan originator risk: on marketplace platforms, the company that issued the loan (and stands behind the buyback guarantee) can fail. A buyback guarantee is only as good as the originator backing it.

- Borrower default: the most visible risk but usually the most manageable, because diversification across thousands of small loans smooths it out.

- Liquidity risk: your money is tied up in loans. Secondary markets help, but in a crisis they dry up exactly when you want out.

I go deeper on this in my dedicated piece on whether P2P lending is safe. The short version: respect the risk, size your allocation accordingly, and never put in money you can’t afford to lock up or lose.

ECSP Regulation: What It Means for You

The European Crowdfunding Service Providers (ECSP) regulation brought much of the sector under a single EU licensing framework. For investors, that’s a meaningful upgrade: licensed platforms face capital requirements, disclosure rules, and supervision, and a licence passports across the EU.

It isn’t a guarantee against loss, and not every platform or loan type falls under it. But “is it ECSP-licensed (or otherwise properly regulated)?” is now one of the first questions I ask before funding a platform. Regulation doesn’t make a platform safe; it raises the floor.

Who Can Invest in P2P Lending?

Most European platforms accept investors who are at least 18, hold an EU/EEA (and often UK or Swiss) bank account, and can pass standard identity checks. You don’t need to be wealthy or accredited. The practical barrier is lower than almost any other asset class: a working SEPA bank account and a passport are usually enough.

How to Choose a Platform

After years of doing this, my checklist is short:

- Track record: years in operation, ideally through a downturn. New and shiny is a red flag, not a feature.

- Regulation: an ECSP licence or equivalent oversight.

- Transparency: clear loan data, real financials, named people behind it.

- Returns that make sense: a rate far above the market average is a warning, not a bargain.

On that basis, the platforms I rate most highly in 2026 are Nectaro (my current top pick, ECSP-licensed), Afranga (among the highest reliable returns), and Mintos (the largest and most diversified, though its recovery backlog and fees are worth understanding first). I rank and explain all of them in the best European P2P lending platforms guide.

How to Diversify Across Platforms

The single most important rule in P2P lending: never trust one platform with all your money. The whole game is surviving the failure of any single platform without it hurting too much. That means spreading across several, not just across many loans on one.

A sensible structure for, say, a €10,000 P2P allocation might look like:

- 40% across one or two large, established platforms (your core)

- 40% across two or three higher-yield platforms with solid track records

- 20% held back as cash or in your most liquid platform, ready to redeploy

The exact split matters less than the principle: if any one platform vanished tomorrow, you’d be annoyed, not ruined. For concrete head-to-head picks, I’ve compared the main options directly, for example Nectaro vs Mintos, and listed the strongest Nectaro alternatives.

P2P Lending and Taxes

Interest from P2P lending is taxable income in most countries, and it’s your responsibility to declare it; the platforms generally don’t withhold tax for you. How it’s taxed depends on where you live. I’ve written separately on how P2P lending income is taxed, and for Spanish residents, foreign-held P2P accounts can also trigger the Modelo 720 reporting obligation. Keep clean records of your interest earned per platform; most platforms provide an annual tax statement.

Alternatives to P2P Lending

P2P lending is one tool, not a whole portfolio. If you like the idea of income-generating alternatives but want to spread beyond consumer loans, the natural neighbours are real estate crowdfunding (property-backed loans, often with collateral) and dividend stocks or bond funds for the more liquid, regulated end. Each has a different risk profile; the point is that P2P should be a slice of your income allocation, not the entire thing.

Conclusion

P2P lending has matured a lot. Regulation is tighter, the strongest platforms have real track records, and double-digit returns are still achievable for investors who respect the risks. The investors who do well aren’t the ones chasing the highest advertised rate; they’re the ones who diversify across solid platforms, keep some liquidity, and treat it as one part of a broader plan.

If you’re ready to start, the fastest way in is my ranked, regularly updated list of the best European P2P lending platforms for 2026. And if you’re still deciding whether it’s for you, read why I invest in P2P lending and whether it’s safe.

Frequently Asked Questions

What returns can you realistically earn from P2P lending?

In Europe in 2026, net returns typically run from around 9% to 13%, depending on the platform and loan type. These are not guaranteed; your realised return is usually a little lower than the advertised rate once you account for idle cash and occasional losses.

Is P2P lending safe?

It carries real risk and there’s no deposit insurance. The main danger is platform or loan-originator failure rather than individual borrowers defaulting. You manage it by sticking to established, regulated platforms and diversifying across several of them. Never invest money you can’t afford to lock up or lose.

How much money do I need to start P2P lending?

Very little. Most European platforms let you start with €10 to €50. The practical requirements are being 18 or older, having an EU/EEA (often also UK or Swiss) bank account, and passing a standard identity check.

How many P2P platforms should I use?

More than one, always. The biggest risk is a single platform failing, so spreading across three to five solid platforms is more important than holding many loans on just one. See the best European P2P lending platforms for options worth combining.

Do I have to pay tax on P2P lending income?

Yes, in most countries interest from P2P lending is taxable and you must declare it yourself. The exact treatment depends on your country of residence. See my guide on how P2P lending is taxed, and note that foreign-held accounts may trigger reporting duties such as Spain’s Modelo 720.

Related

Hi Sir,

I have red somewhere that Mintos is not free for a French man.

In other words I cannot invest in Mintos because I am French.

Can you say the same,

Smiling Paul

PS: excuse my bad English!

thax

Why do you recomend Bulkestate? For the level of transparency?

I also like Viainvest for the track record and transparency.

And what´s your opinion for Crowdestor?

I should have probably made a separate category for real estate crowdfunding websites, in which I would also include Reinvest24 and Property Partner.

I’ll update the post.

Thanks for your post. What makes you recommend those 3/4 platforms over the others?

Several factors, I would say these are some of them that are important for me:

Happy to answer other questions you may have and discuss further.

Thanks for your replay Jean. Do you no longer recommend Twino?

Did you try any factoring P2P sites yet? Investly seems interesting and has a low default rate. I’m not sure I understand how it works yet though.

All thes best

Thanks! Happy first advent.