Real estate investing needs little introduction. This asset class has been a top choice for investors since time immemorial. It’s an asset you can see, use, or rent out, and it requires no technical knowledge to understand. That’s why real estate remains one of the primary places people park their money.

I’ve been investing through various platforms over the years, which has given me a solid idea of what works and what doesn’t. Here’s a quick list of the property-based crowdfunding platforms I currently recommend, all of which I’ve reviewed on this site.

- Raizers — French and European real estate, AMF-regulated since 2014

- LANDE — agricultural lending backed by farmland mortgages, ECSP licensed

- InRento — buy-to-let properties across Europe, ECSP licensed

- Letsinvest — Lithuanian platform, ECSP licensed, first-rank mortgages

- Crowdpear — Lithuanian platform, ECSP licensed, up to 14% returns

- Fintown — Prague short-term rental properties, developer skin-in-the-game

For a broader overview you can also visit my dedicated page on European property investments.

REITs vs Real Estate Crowdfunding vs Private Investing

When talking about the real estate market, there are currently three main ways of investing:

- Property Crowdfunding

- Real Estate Investment Trusts (REITs)

- Private Investing

Each has its own pros and cons. I’ll describe all three so you can decide which suits your situation and goals.

Property Crowdfunding

Real estate crowdfunding platforms are part of the fintech wave of the past decade and have become popular across the EU, UK, and beyond. A property crowdfunding platform gives you the ability to view individual projects in an offering phase — you can read about the location, the developer’s plans and financials, and the type of financing involved (leveraged vs. non-leveraged).

Typically your money is tied up for a 12-36 month term, and some platforms offer a secondary market where you can sell your position to other investors early (usually with a fee or at a discount).

I’ve personally invested in several property crowdfunding platforms, including Raizers, LANDE, and InRento. So far I’m happy with the results, and I’m convinced we’ll continue to see more first-time property investors starting through crowdfunding platforms rather than direct ownership or REITs.

Since November 2023, European crowdfunding platforms that want to operate across EU member states are required to hold a license under the European Crowdfunding Service Provider (ECSP) regulation. This is a meaningful shift that I’ll cover in detail below.

Real Estate Investment Trusts (REITs)

One of the better ways to diversify a property portfolio is through real estate investment trusts. REITs started in the USA but are now available in many countries. A pure REIT represents shares in an individual real estate company, while a REIT ETF passively tracks a broader index of the real estate market.

REITs own many types of commercial real estate: office buildings, apartment complexes, warehouses, hospitals, shopping centers, hotels, and more. Some REITs also engage in financing real estate.

The iShares Europe Developed Real Estate ETF is an example of a European real estate ETF you might want to check out. The ETF seeks to track the investment results of an index composed of real estate equities in developed European markets. You can expect to pay around 0.5% in fees.

The Vanguard REIT ETF (VNQ) is the largest US REIT in the sector and has been trading since 2004. It invests in stocks issued by REITs and seeks to track the MSCI U.S. REIT index.

One key advantage of publicly traded REITs is liquidity. You can sell your investment at any point if you need the cash or want to exit. The trade-off is that you’re highly detached from the underlying properties, and your investment moves with the broader stock market rather than reflecting real estate fundamentals directly.

Private Investing

Private investment is the oldest and most well-known form of property investing. An investor purchases one or more properties and rents them out for monthly income. For higher returns, the investor might also flip properties — buying an older property, refurbishing it, and selling within 8-12 months in an appreciating market.

Private investing gives you maximum control. You can manage tenant relationships, refurbish the property how you see fit, and negotiate directly. If you’re an expert in the local market with the right contacts, this can be a serious income generator.

The main drawbacks are time and concentration risk. Unless you have significant capital across multiple cities or countries, your entire property portfolio depends on the fortunes of one local economy. Vacant periods hit hard too — even one or two empty months can meaningfully affect your cash flow.

Personally, private investing doesn’t fit my situation. I have no interest in the day-to-day management of properties, I’m not a local market expert, and I don’t want to take on the leverage required to buy multiple properties. That’s not a criticism of private investing — it can work very well for people who are passionate about real estate and treat it as a part-time or full-time job.

Why I Prefer Real Estate Crowdfunding

With property crowdfunding, I can stay free from the operational headaches of managing properties while still having full visibility into the financials, business plans, and individual performance of each investment. I’ve invested in Spanish real estate, UK real estate, and Baltic platforms. The Baltic platforms — specifically those focused on first-rank mortgage loans — have performed best for me.

With REITs, the detachment from the underlying properties is my main objection. Crowdfunding platforms strike a better balance: institutional-grade deal flow, real collateral, visible loan terms, and no need to manage anything yourself.

Apart from the return potential, crowdfunding is a solid educational experience. Understanding LTV ratios, collateral structures, and developer track records builds a base of knowledge that transfers well to private investing or buying your own property down the line.

ECSP Regulation: What It Means for European Investors

The EU’s European Crowdfunding Service Provider (ECSP) regulation — formally Regulation (EU) 2020/1503 — came into force in November 2021 and became mandatory for all platforms operating across EU borders from November 2023. This is the most significant regulatory development in European crowdfunding in years, and it matters directly for investors.

Before ECSP, each EU country had its own patchwork of rules. A platform licensed in Lithuania could not legally offer investments to retail investors in Spain or Germany without navigating separate regulatory frameworks in each country. ECSP changed that: a single license from any EU national regulator is now valid across all EU member states.

What ECSP requires of licensed platforms:

- Registration with and oversight from a national financial regulator

- Clear Key Investment Information Sheets (KIIS) for every project — standardized disclosure documents that allow investors to compare projects across platforms

- Client onboarding requirements, including a “knowledge test” for first-time or inexperienced investors

- A 4-day reflection period for retail investors, during which they can withdraw their investment without penalty

- Segregation of client funds and clear contingency arrangements if the platform ceases to operate

- Investment limits for non-sophisticated retail investors (€1,000 per project or 10% of net worth, whichever is higher)

What ECSP does not do: It does not guarantee returns, protect against borrower defaults, or provide deposit insurance. An ECSP license is a governance and transparency standard, not a backstop for your capital.

That said, ECSP-licensed platforms are meaningfully more trustworthy than unlicensed ones. When I evaluate a new European crowdfunding platform today, an ECSP license is one of the first things I look for. The platforms I recommend above — LANDE, InRento, Letsinvest, and Crowdpear — all hold ECSP licenses.

Why do Borrowers Obtain Finance from Real Estate Crowdfunding Platforms?

A common question from new investors: if borrowing rates are so low at banks, why would a developer pay 10-12% per year on a crowdfunding loan?

The answer involves several advantages that crowdfunding platforms offer over traditional bank financing.

Speed

Bank financing for a real estate project can take 4-6 months from application to receiving funds. Crowdfunding platforms can provide an indicative offer within 24 hours and funds within 2 weeks. This speed advantage makes crowdfunding attractive as bridge financing — a developer can start work on a project while the bank is still evaluating the application.

Flexible Loan Terms

Banks typically require monthly interest and principal payments. Crowdfunding platforms often allow bullet repayment structures — where the borrower pays everything at the end of the term — which frees up cash flow during the construction or refurbishment period. Early repayment without penalty is also common, so a developer who sells units earlier than expected can repay the loan and reduce their interest costs.

No Monthly Servicing Requirements

With flexible repayment schedules, developers can fully focus on the project rather than managing monthly liabilities. For a developer doing a 12-month renovation, not having to service debt every month is a meaningful operational advantage.

Marketing Exposure

A platform with thousands of registered investors from multiple countries is also a sales channel. A development project published on a crowdfunding platform with 50,000 registered investors is getting free exposure to people who are already interested in real estate. The financial details visible to investors are typically limited to verified platform users, not the general public.

How Property Crowdfunding is Taxed

Property crowdfunding is a form of indirect property investment. You are investing in loans to, or shares in, a company that owns and manages property. The tax treatment varies depending on the structure.

In a loan-based crowdfunding model (the most common in Europe), you are earning interest income. Most EU countries tax interest income at standard income tax rates or at a specific savings rate. For example, Lithuania withholds 15% tax at source on interest paid to foreign investors (reducible by tax treaty in many cases).

In an equity-based crowdfunding model, you hold shares in a special purpose vehicle (SPV) that owns a property. Income arrives as dividends (taxed as dividend income in most jurisdictions) and capital gains on the eventual sale of the property or your shares.

In most countries you’ll be taxed on both:

- Interest or dividend income — received periodically or at loan maturity

- Capital gains — realized when a property is sold and principal is returned at a premium, or when you sell shares

The specific rates depend entirely on your country of residence. Spain, for example, taxes savings income on a progressive scale starting at 19%. Malta, Germany, and Portugal all have different treatments.

For a more detailed breakdown specific to Spain, see how crowdlending is taxed in Spain. For a broader European view, see how P2P lending is taxed in Europe.

I am not an accountant or financial advisor. The above reflects my personal research and may contain inaccuracies or become outdated as tax law changes. Before submitting any tax returns, consult a qualified tax advisor in your country of residence.

How to Evaluate Real Estate Crowdfunding Investments

With dozens of real estate crowdfunding platforms now operating across Europe, investors can fund projects in multiple countries from a laptop. Not all platforms and projects are equally good, so it’s worth developing a basic framework before you hit the invest button.

Loan-To-Value

If the deal involves giving a loan to a property developer, loan-to-value (LTV) is the most important metric to examine. It compares the loan amount to the value of the property used as collateral.

The lower the LTV, the more cushion you have if things go wrong. If a developer defaults and the platform must sell the property, a low LTV gives room for the sale price to come in below the original valuation and still cover investor capital.

Watch out for how platforms calculate “value.” Some use the projected future value of a completed development rather than the current as-is value of the property. A project with a loan of €250,000 against a current property value of €500,000 is a 50% LTV — healthy. If the platform instead quotes that same loan against a projected completed value of €1,000,000, you get a quoted LTV of 25%, which looks conservative but is essentially fictional until the project is finished and sold. Stick to current as-is valuations.

This kind of optimistic accounting contributed to the collapse of the UK platform Lendy, which went bust after borrowers failed to complete projects that had been valued on aspirational rather than current figures.

First or Second Rank Mortgage

A mortgage rank indicates who gets paid first if a borrower defaults and the collateral is sold.

First-rank mortgage holders get paid before anyone else. Second-rank holders get whatever is left over after the first-rank holder is made whole — which may be nothing if the property sells at a discount.

You should prefer first-rank mortgages wherever possible. Platforms like LANDE and Letsinvest only do first-rank mortgages as a policy. Second-rank mortgages appear more often on German and British platforms, and they carry meaningfully higher risk.

There are nuances. If a property is already built, fully tenanted, and generating strong rental income, a second-rank position may be acceptable if the yield coverage and LTV ratios are conservative. But as a default rule, first-rank is safer.

Apply Financial Ratios and Rules

Whether you’re evaluating a direct property purchase or a loan on a crowdfunding platform, the following ratios are useful quick-filters.

Price/Rent Ratio

Compare the median property price to the median annual rent for the same area. Lower ratios indicate better rental yield potential.

The 50% Rule

A shortcut for estimating net operating income (NOI): assume 50% of gross rent will be consumed by vacancy, management fees, taxes, insurance, and maintenance. The remaining 50% is your NOI estimate. This excludes mortgage costs.

Capitalization Rate

The cap rate lets you compare the performance of one property to another on a like-for-like basis. Take your NOI and divide it by the property value. In some markets a 6% cap rate is excellent; in lower-priced markets you might need 10-12% to make the numbers work.

The 1% Rule

Gross monthly rent should equal at least 1% of total investment (purchase price plus refurbishment costs). On a €100,000 total investment, you’d want at least €1,000 per month in gross rent.

The 2% Rule

The same calculation but targeting 2% monthly gross rent. Applicable in lower-priced markets where higher yields are achievable.

When to Apply Each Rule

Which rule you use depends entirely on local market conditions. In prime urban markets (Barcelona, London, Amsterdam), even hitting 1% is exceptional. In smaller cities or emerging markets, 2% may be achievable. Know the yields typical for the area you’re analyzing before applying any rule.

Rule Limitations

These ratios are filters, not decisions. They don’t account for:

- Taxes and condominium fees

- Insurance

- Maintenance (an older building may pass the 1% Rule but have far higher maintenance costs than a new one)

- Vacancy and tenant turnover

- Management fees

Use these rules to quickly eliminate weak candidates from a list. Once you’ve narrowed it down, dig into the full numbers before committing capital.

Consider the Platform’s History

Before investing with any platform, look at how long it has been operating and what its track record looks like across different market conditions. Any platform can perform well when the market is rising. The real test is how a platform behaves during a correction.

Look specifically for:

- Default and late payment rates over time

- Recovery outcomes on defaulted loans

- How the platform communicates when projects run into trouble

- Whether audited financial accounts are publicly available

Platforms that have lived through the 2020 COVID shock and the 2022-2023 rate environment and come out with their investors made whole are worth more confidence than newer platforms with unblemished but short track records.

Read Reviews

Online reviews are inherently biased to some degree — platforms pay affiliates, which colors recommendations. That said, independent reviews from experienced investors can surface risks that are not obvious from the platform’s own marketing. Pay attention to recurring complaints about late withdrawals, lack of communication, or poor recovery on defaults. Those patterns don’t tend to be invented.

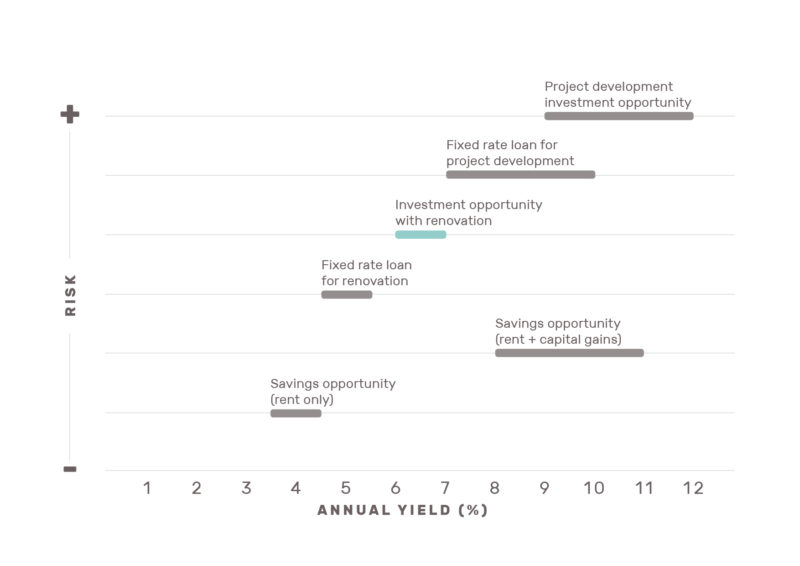

Yield vs Risk in Real Estate Investing

Like any financial product, higher expected yields come with higher risk. In the crowdfunding world, the yield-risk relationship generally looks like this:

- Lower risk, lower yield (6-9%): First-rank mortgage loans on completed, tenanted properties with conservative LTVs. ECSP-licensed platforms in well-regulated jurisdictions. Examples: LANDE, InRento.

- Mid-range risk and yield (9-12%): First-rank mortgage loans on development projects in progress, ECSP-licensed platforms. Examples: Letsinvest, Crowdpear, Raizers.

- Higher risk, higher yield (12%+): Second-rank mortgages, development projects in newer or less liquid markets, shorter operating history. These require deeper due diligence.

Renovation projects tend to sit in the mid-range — they’re not pure development plays, but there’s more execution risk than a stabilized rental property. They’re popular on many platforms for exactly that reason: the risk-return profile is balanced and the 8-18 month timelines keep capital moving.

I run a mixed portfolio: some lower-risk first-rank loan investments for predictable returns, some development-stage projects for higher upside. The key is sizing each position so no single default is catastrophic.

Platforms That Failed: What to Learn From Them

European real estate crowdfunding has had its share of casualties. Understanding what went wrong is as important as knowing what to look for.

Lendy (UK, collapsed 2019): Inflated property valuations using projected future values, not current as-is figures. When borrowers couldn’t complete developments, the collateral was worth far less than the platform had represented.

Housers (Spain): Long delays, poor communication, and a business model that prioritized marketing spend over investor returns. Still technically operating but with a badly damaged reputation and numerous unresolved delayed loans.

Property Partner / London House Exchange (UK): Originally launched in 2014 as a promising equity crowdfunding platform for UK residential property. Rebranded as London House Exchange after years of underperformance. If you invested early and held, you likely lost money — the platform struggled to generate the returns its marketing implied. I have a detailed review of London House Exchange covering why I no longer recommend it.

The consistent lesson across failed platforms is the same: be skeptical of headline yields, verify valuation methodology, and favor platforms with first-rank collateral and conservative LTV ratios.

Frequently Asked Questions

Is real estate crowdfunding safe?

No investment is safe in the sense of being risk-free. Real estate crowdfunding carries the risk of borrower default, platform insolvency, and liquidity constraints (you typically cannot exit early). That said, platforms offering first-rank mortgage loans at conservative LTVs have historically provided good capital protection. Diversifying across multiple platforms and projects reduces concentration risk. See my guide on whether P2P lending is safe for a fuller discussion of risks.

How much should I invest in real estate crowdfunding?

As a general rule, no single asset class should represent more than 20-30% of a diversified portfolio, and crowdfunding specifically should be treated as an alternative investment within that. Within crowdfunding, spreading across 5-10 platforms limits your exposure to any single platform’s problems. ECSP regulation imposes a €1,000 per project or 10% of net worth limit for non-sophisticated retail investors, which is a reasonable guardrail.

What is an ECSP license and why does it matter?

ECSP stands for European Crowdfunding Service Provider. It’s an EU-wide license that crowdfunding platforms must hold to legally offer investments to retail investors across EU member states. Platforms with ECSP licenses are regulated by a national financial authority (such as the Bank of Lithuania), must provide standardized project disclosure documents, and must segregate client funds. It doesn’t guarantee returns, but it means the platform is accountable to a regulator.

What’s the difference between loan-based and equity-based crowdfunding?

In loan-based crowdfunding, you lend money to a developer at a fixed interest rate, secured against a property. Your return is the interest payments. In equity-based crowdfunding, you buy shares in a company that owns the property. Your return is rental dividends plus any appreciation in the property’s value when it’s eventually sold. Loan-based is more common in Europe and simpler to understand; equity-based gives more upside if the property appreciates significantly.

Are there real estate crowdfunding platforms for US investors?

Most European platforms are not available to US investors due to securities regulations. For US-based investors, Fundrise is a well-known US-focused alternative — I’ve reviewed Fundrise here.

Related

Hola Jean, felicitaciones por la publicación y muchas gracias por su utilidad para quienes, como Yo, apenas estamos conociendo de estos instrumentos de Inversión como el Crowfunding. Por otra parte, me gustaría saber si has invertido y administrado propiedades como para tener una opinión cercana sobre este tipo de opción.

Agradecido.

Great information! While trying to decide which one to choose amongst REITs and Real Estate Crowdfunding, there really isn’t any right or wrong option. It depends on each individual investor’s risk capacity, budget, understanding of the tax implications on dividends earned, and tenure of the investment. For investors who are risk-averse REITs may be a better option that would allow them faster liquidity as compared to real estate crowdfunding. On the other hand, investors with a greater entrepreneurial mindset who are willing to take on certain risks and long-term financial goals could opt for real estate crowdfunding.

Totally agreed.

All good information thanks. Reits are also attractive because national regulations usually force them to issue a huge part of their profits so their dividends are usually very healthy. Yes they are more liquid than owning an actual property but one should invest in a Reit only with a 3 to 5 year plan since the stock price might lose value from time to time and not always rise. You don’t want to sell at a lower stock price. But when you want to get rid of it at a profit it can be done on a day if it’s traded publicly. I agree that buying a Reit is accepting quite a distance from the properties themselves. So far less control than other options. Buying a single property wont always mean high risk because of non diversification..not if you buy in a sought after rental city. But yes its hard work and it can become a part time occupation if not more.

The only thing that worries me about crowdfunding is how to trust the people running it. I have developed a very low trust for humans in the financial industry. But otherwise it seems like the path of least resistance. Just sad that you cannot enough the property you invested in…because you don’t own it fully. Then again a property investment isn’t a financial investment if it becomes your home. Your home should not be considered as part of your investment portfolio.

Agreed, I will soon be experimenting with a kind of hybrid between impersonal web-based crowdfunding and private investment. There are groups of experienced private real estate investors and developers and they invest in properties together, with a maximum number of investors typically in the 5-10 region. This brings you much closer to actually owning the place and giving you a much bigger say in the directions taken, while also allowing you to personally know the other investors and decide how trustworthy they are. It also gives you some of the advantages of crowdfunding since the sum invested is lower, you have a team rather than being alone, and you can diversify.

We have a model that is aimed at ensuring you feel invested enough.property markets in east africa have been on the rise with foreigners taking keen interest to holiday homes,office and large storage blocks and with that the portfolio is diverse. For able investors we do locally offer custodian services and encourage them to have power of attorney over properties we oversee and manage. every thing is transparent and any changes are communicated well in advance. We believe this model is the best approach to bringing fruitful investment and with as little as $200,000 one is able to own a home with a ROI of 5-6%

Great article, clear and syntactic, congrats. I have one question, how do you gather all your investments information from the different platforms you have money in?

It seems like individually go to these platforms can be a pain point.

Hi Lio, that is indeed one of the pain points, but it’s the same with owning several businesses or owning several properties. It seems to me that it is one of those problems in life that there isn’t ever a solution for apart from hiring someone to do the data collection and possibly analysis (based on your parameters) for you.

Great and easy to understand article Jean. By the way did you try to trade your investment share in Spanish and German real estate crowdfunding sites and whats your take on this functionality?

Thanks, so far I have not done any trading but it’s a handy feature to have if you need quick liquidity.

Thank you for the informative article, Jean. I appreciate your taking the time to explain the difference between private investment, REITs, and property crowdfunding. Great work! Peace and best wishes!

You’re welcome Reg.