Crowdpear is a Lithuanian real estate crowdfunding platform that launched in January 2023 and has quietly built one of the more credible track records among newer European platforms — EUR 42.5 million funded, zero confirmed capital losses, and a full ECSP license from the Bank of Lithuania. It’s a PeerBerry spin-off, which cuts both ways depending on how you look at it.

Crowdpear at a Glance

| Founded | Registered July 2021, operational January 2023 |

| Headquarters | Vilnius, Lithuania |

| Asset class | Real estate-backed business loans |

| Advertised returns | Up to 14% p.a. (realistic: 10–11%) |

| Loan terms | 12–18 months (bullet structure) |

| Interest payments | Quarterly |

| Minimum investment | EUR 100–500 (varies by project) |

| Secondary market | Yes (2% fee, 14-day listing limit) |

| Auto-invest | No |

| Buyback guarantee | No (prohibited under ECSP regulation) |

| Regulation | ECSP license, Bank of Lithuania (granted July 25, 2023) |

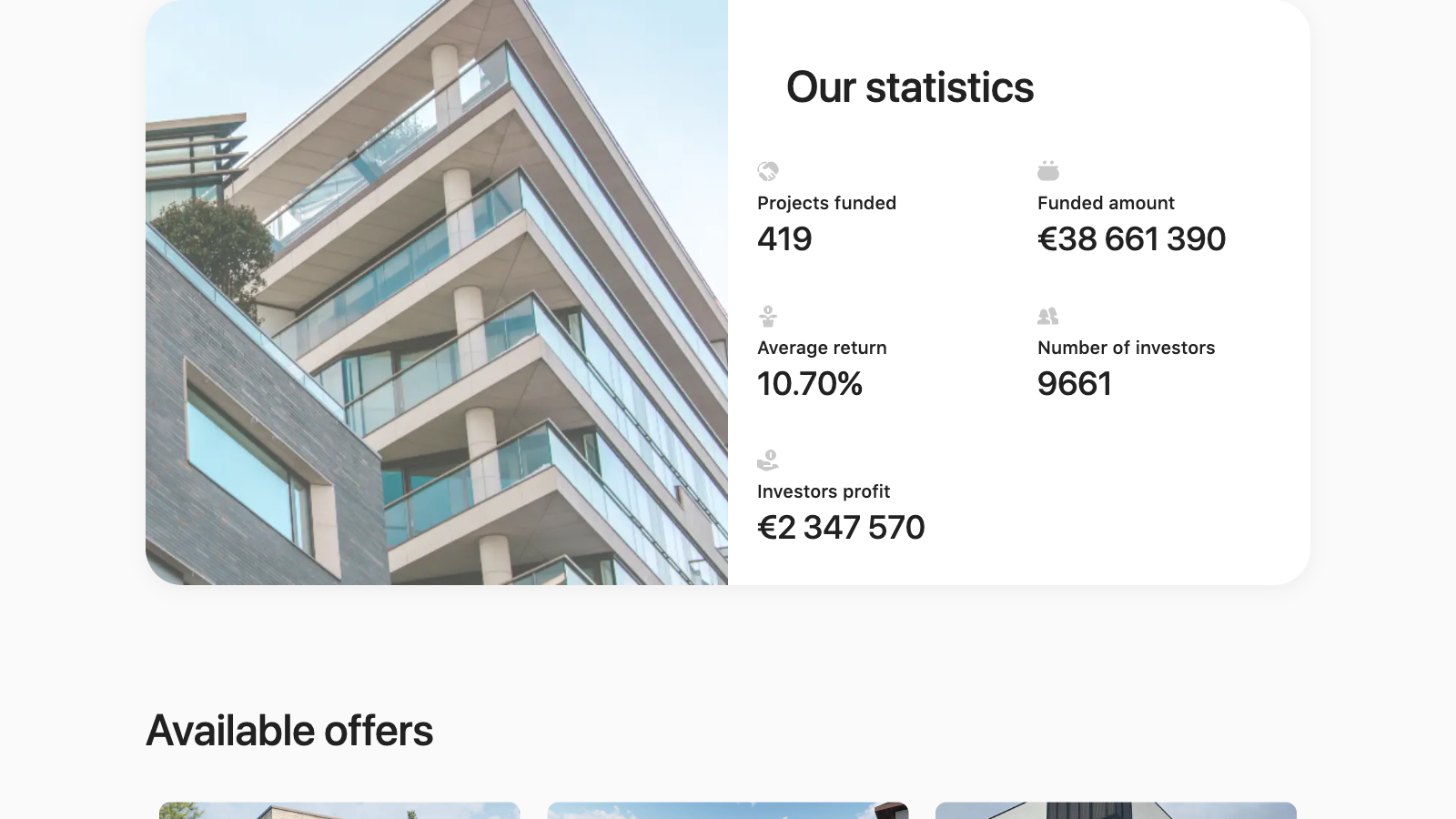

| Cumulative funded | EUR 42.53 million (as of February 2026) |

| Loans repaid | 249 of 436+ funded |

| Late loans (90+ days) | 9.26% of historical volume |

| Capital losses | Zero to date |

| Investors | ~9,929 verified |

| Trustpilot | 4.3/5 (31 reviews) |

How Crowdpear Works

Crowdpear funds real estate-backed business loans in Lithuania, with early-stage expansion into Romania and Portugal. Borrowers are typically property developers seeking short-term financing — bridge loans, construction finance, and similar instruments. Investors provide capital in exchange for a fixed interest rate, with the loan secured by a mortgage on the underlying property.

The loan structure is a bullet loan: you receive interest quarterly, but the principal comes back in a lump sum at maturity. That means your money is tied up for the full 12–18 month term unless you use the secondary market. This is a meaningful difference from amortizing loans where principal trickles back over time.

Crowdpear uses a claims assignment model. When you invest, you’re buying a fractional claim to the loan rather than directly lending to the borrower. This is standard practice in European crowdfunding and has some legal nuance worth understanding — your recourse runs through Crowdpear as intermediary, not directly to the borrower. If Crowdpear were to fail as a company, there are provisions under the ECSP framework for orderly wind-down, but this is a risk to be aware of.

There is no auto-invest function. You browse available projects manually, review the loan documentation, and commit capital project by project. For active investors, this is fine. For anyone expecting a hands-off experience, it’s a limitation — especially when new loans fill up quickly.

Returns: What’s Advertised vs. What Investors Actually Earn

Crowdpear advertises returns “up to 14%,” which is technically accurate for the highest-risk tier of projects. The realistic range for a typical portfolio is 10–11% gross. That’s still competitive for a regulated, real-estate-backed instrument in Europe.

Where things get more complicated is taxes. Lithuania applies a 15% withholding tax on interest income paid to foreign investors by default. You can reduce this to 10% by submitting a DAS-1 form (a double-taxation relief certificate from your home country). After the lower 10% rate, a 10% gross return becomes roughly 9% net. After the default 15% rate, you’re looking at closer to 8.5% net. These aren’t catastrophic haircuts, but the gap between the headline and the after-tax reality is worth factoring into your expectations from the start.

For investors who are late payments, Crowdpear charges borrowers an additional 5% per annum penalty interest and passes this through to investors for the duration of the delay. It doesn’t make late loans desirable, but it does mean delays aren’t entirely unrewarded.

Larger portfolio holders qualify for loyalty bonuses up to 1% on top of base rates, which partially offsets the withholding tax drag for committed investors.

Regulation and Investor Protection

This is where Crowdpear has a genuine edge over many smaller platforms. It received its ECSP (European Crowdfunding Service Provider) license from the Bank of Lithuania on July 25, 2023 — a license that requires compliance with EU Regulation 2020/1503, which sets out specific rules on disclosure, investor classification, and operational safeguards. This is a meaningful hurdle, not a rubber stamp.

In December 2025, Crowdpear also became the first Lithuanian crowdfunding platform to achieve ISO/IEC 27001:2022 certification for information security management. It’s a third-party-audited credential, which matters more than self-reported security claims.

What the ECSP license does not provide is deposit protection or a government backstop for investor losses. There is no buyback guarantee — the regulation actually prohibits platforms from offering them, on the grounds that guarantees create false security and moral hazard. If a borrower defaults and the collateral recovery falls short of the loan value, investors bear that loss. The mortgage security is only as good as the property market and the speed of recovery proceedings.

On that front: three projects totaling EUR 496,646 are currently in recovery as of early 2026. No capital losses have been confirmed. That’s a healthy position for a three-year-old platform, though the sample size is still small relative to a full real estate cycle.

The PeerBerry Connection

Crowdpear is not a standalone operation. Two of its three shareholders — CEO Vytautas Olsauskas (25% stake) and Ivan Butov (25% stake) — are also shareholders in PeerBerry, one of Europe’s larger P2P lending platforms. The third shareholder, Vytautas Straznickas (50% stake), is part of Aventus Group management, the same group that sits behind PeerBerry’s loan originators. Crowdpear’s Deputy CEO, Arunas Lekavicius, simultaneously serves as CEO of PeerBerry.

This overlap is worth understanding clearly. It means Crowdpear is effectively a PeerBerry-affiliated venture, not an independent startup. The management team brings genuine experience — Olsauskas founded Mano Bankas, a bank licensed by the European Central Bank, and has over 15 years in financial services. That’s a more credible founding pedigree than most crowdfunding platforms can claim.

The risk is concentration: if something were to go wrong at the Aventus Group level, there is a plausible path for contagion to affect Crowdpear. PeerBerry navigated the Aventus exposure to Russian-Ukrainian loan originators in 2022 and ultimately repaid investors, but it was a stress test that revealed how interconnected these structures can be. Crowdpear operates in a different asset class (real estate, not consumer loans), but the ownership links are a factor for anyone building a concentrated position.

For investors who already hold PeerBerry, adding Crowdpear meaningfully increases exposure to the same ownership group — worth keeping in mind when thinking about portfolio diversification.

Who Crowdpear Is For — and Who Should Avoid It

Crowdpear suits investors who want real-estate-backed exposure in a properly regulated European platform, are comfortable with illiquid bullet loans (12–18 months), and don’t need auto-invest to manage their portfolio. The 10–11% gross return range is realistic and competitive. The zero capital loss record, while still early-stage, is encouraging.

It’s also well-suited for investors who are already familiar with P2P or real estate crowdfunding and understand that “ECSP licensed” means regulated but not guaranteed. The documentation on each project is detailed, and the quarterly interest payments provide a regular income signal on portfolio health.

Crowdpear is a poor fit if you need liquidity on short notice. The secondary market exists, but with a 2% fee and a 14-day listing limit, it’s not a reliable exit route if you need cash in a hurry. The platform’s loan supply is also limited — cash drag (idle cash earning nothing while you wait for suitable projects) is a documented frustration among investors on forums and review sites.

It’s also not suitable as a standalone investment. With ~9,929 investors and EUR 42.5 million funded across three years of operation, Crowdpear is still a relatively small platform. Anyone allocating more than a modest slice of their investment portfolio here is taking on concentration risk that the platform’s track record doesn’t yet fully justify.

Frequently Asked Questions

Is Crowdpear safe?

No investment platform is “safe” in the absolute sense. Crowdpear holds a valid ECSP license from the Bank of Lithuania, is audited to ISO/IEC 27001 information security standards, and has recorded zero capital losses to date. That’s a better regulatory and operational foundation than most comparably sized platforms. But loans are backed by Lithuanian real estate, and if property values fall sharply or recovery proceedings are slow, investors can lose money. Treat it as a medium-risk instrument, not a cash equivalent.

What is the minimum investment?

The minimum was EUR 100 at launch. Some newer projects appear to have a EUR 500 floor — the threshold varies by project. Check the individual listing when investing.

Are there any late or defaulted loans?

9.26% of historical loan volume has experienced 90+ day late payments. Three projects totaling EUR 496,646 were in active recovery as of early 2026. No confirmed capital losses have occurred. The late loan rate is not low, but the collateral recovery process has so far prevented losses from materializing.

Does Crowdpear have a buyback guarantee?

No, and it cannot have one. The ECSP regulation prohibits platforms from offering buyback guarantees. Loans are secured by real estate mortgages, which is a different form of protection — asset-backed rather than platform-backed.

How is interest taxed?

Lithuania withholds 15% from interest payments to foreign investors by default. This can be reduced to 10% with a DAS-1 form submitted through your home country’s tax authority. You also need to declare interest income in your country of residence according to local rules.

Is there an auto-invest feature?

No. All investments are made manually. Given the limited loan supply, this is less of a burden than it would be on a high-volume platform, but it does mean you need to check in regularly to deploy capital when new projects open.

Can I exit early?

There is a secondary market where you can list your loan positions for sale. The seller pays a 2% fee, and listings expire after 14 days. Liquidity on the secondary market depends on buyer demand and is not guaranteed.

My Opinion

Crowdpear has done the hard things right. Getting an ECSP license in year one of operations, achieving ISO 27001 certification, and maintaining zero capital losses across three years of real estate lending is a track record that many older platforms in this space cannot match. The founding team’s banking background gives the credit process more credibility than a startup assembled by tech entrepreneurs with no prior lending experience.

The PeerBerry ownership overlap is the most significant caveat. I don’t think it disqualifies the platform, but it does mean that investors who hold PeerBerry are not diversifying as much as they might think by adding Crowdpear. The two platforms share management, shareholders, and — through Aventus Group — some of the same institutional relationships. If you’re constructing a multi-platform portfolio specifically to spread risk across independent operators, this connection is worth weighting.

The advertised “up to 14%” is a marketing number. The realistic net return after Lithuanian withholding tax sits in the 8.9–9.5% range for most investors. That’s a reasonable outcome for a regulated, real-estate-backed instrument, but it requires the DAS-1 form and some administrative effort. Going in with an expectation of 14% and ending up with 8.5% net after the default tax rate would be a frustrating surprise.

The limited loan supply and lack of auto-invest mean Crowdpear works best as a deliberate allocation within a broader portfolio, not a platform you set up and forget. The 2025 growth rate (60% YoY, EUR 21.2 million) suggests loan volume is improving, but cash drag remains a real constraint for investors trying to deploy larger sums efficiently.

Overall: a well-regulated, competently run platform at an early stage of its growth. Worth a position for investors who understand what they’re getting — real estate-backed loans in a single market, managed by a PeerBerry-connected team, with solid regulatory foundations and a still-developing track record. Start small, verify the DAS-1 process for your country, and don’t treat the headline return as the one you’ll actually receive.

Disclosure: This article contains affiliate links. If you sign up through my link, I may earn a commission at no extra cost to you. I only recommend platforms I have personally researched or used. This is not financial advice.

Summary

Crowdpear is a PeerBerry-affiliated Lithuanian real estate crowdfunding platform with ECSP regulation and zero capital losses across EUR 42.5M funded. Solid for experienced investors, but PeerBerry ownership overlap creates concentration risk.

Pros

- ECSP licensed by Bank of Lithuania

- Zero confirmed capital losses to date

- ISO/IEC 27001 certified for information security

- Secondary market available

- Experienced management team

- Loyalty bonuses for larger portfolios

Cons

- PeerBerry ownership overlap creates concentration risk

- No auto-invest feature

- 15% Lithuanian withholding tax on interest

- Bullet loan structure locks capital for 12-18 months

- Cash drag reported by investors waiting for new projects

Summary

Crowdpear is a PeerBerry-affiliated Lithuanian real estate crowdfunding platform with ECSP regulation and zero capital losses across EUR 42.5M funded. Solid for experienced investors, but PeerBerry ownership overlap creates concentration risk.

Pros

- ECSP licensed by Bank of Lithuania

- Zero confirmed capital losses to date

- ISO/IEC 27001 certified for information security

- Secondary market available

- Experienced management team

- Loyalty bonuses for larger portfolios

Cons

- PeerBerry ownership overlap creates concentration risk

- No auto-invest feature

- 15% Lithuanian withholding tax on interest

- Bullet loan structure locks capital for 12-18 months

- Cash drag reported by investors waiting for new projects

Related

Leave a Reply