Scramble is a European P2P investment platform with an unusual pitch: instead of funding consumer loans, mortgages, or small business debt, it provides working capital to early-stage consumer goods brands — think food startups, beauty labels, pet care companies, and fashion brands, mostly based in the UK and Europe. I’ve been keeping an eye on it for a while, and this review covers everything you need to know before putting money in, including the parts the platform doesn’t lead with.

Scramble at a Glance

| Founded | 2021 |

| Headquarters | Tallinn, Estonia |

| Legal entity | Scramble OU (registry code 14991448) |

| Regulated | No — no ECSP license |

| Investment type | Working capital loans to consumer brands |

| Loan terms | 6 months, extendable to 24 months |

| Returns (Group A) | Up to 12.4% annualized |

| Returns (Group B) | Up to 25% annualized |

| Platform average | 16.54% annualized (claimed) |

| Minimum investment | EUR 10 |

| Secondary market | None |

| Auto-invest | None |

| Buyback guarantee | None |

| On-time repayment | 84% |

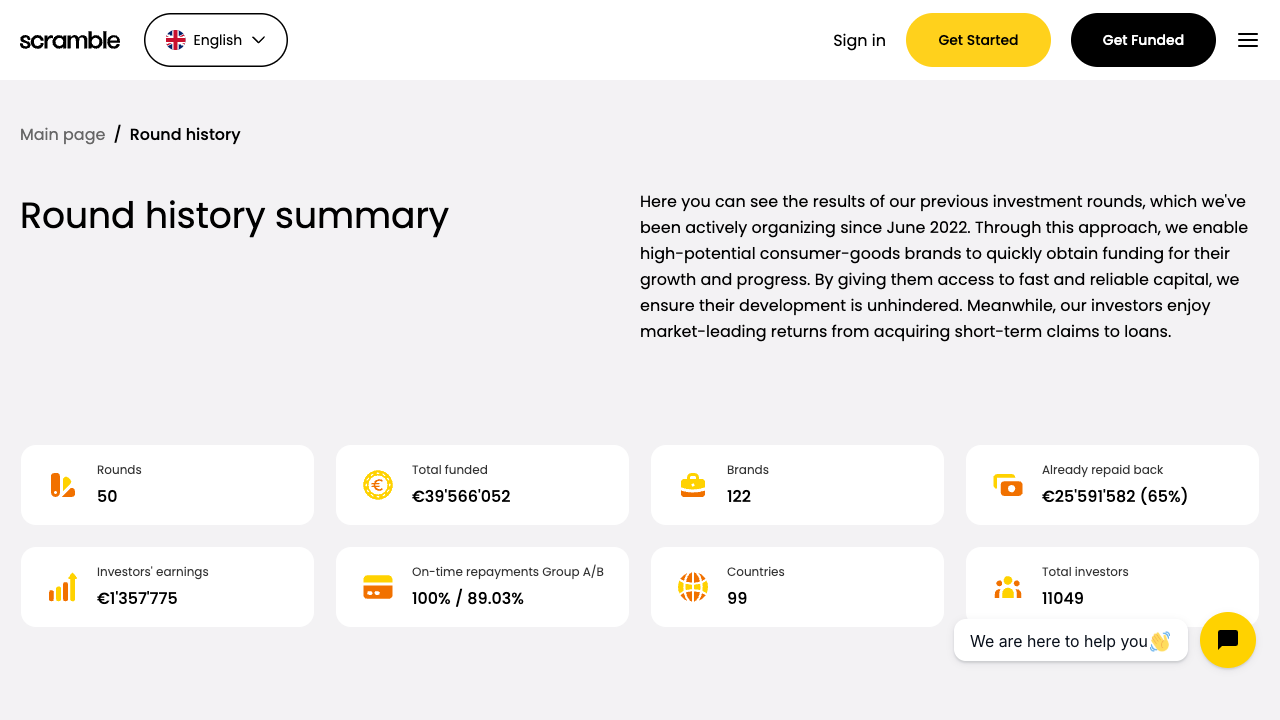

| Total funded | ~EUR 36 million |

| Investors | 33,200+ from 85+ countries |

| Trustpilot | 4.7/5 (1,130+ reviews) |

| Investor fees | Zero |

| Funds segregated | Yes, at LHV Bank |

How Scramble Works

Scramble uses a claims assignment model, meaning you’re not directly lending money — you’re purchasing a claim on a debt that Scramble has already extended to a borrower. The platform then services repayments and passes them on to investors. It’s a structural detail worth understanding because it affects how your rights are defined if something goes wrong.

Borrowers are consumer brands that need short-term working capital — typically to fund inventory ahead of a sales season. Loan terms are 6 months, extendable up to 24 months, and the platform funds UK and European brands in categories like food, beauty, fashion, pet care, and lifestyle.

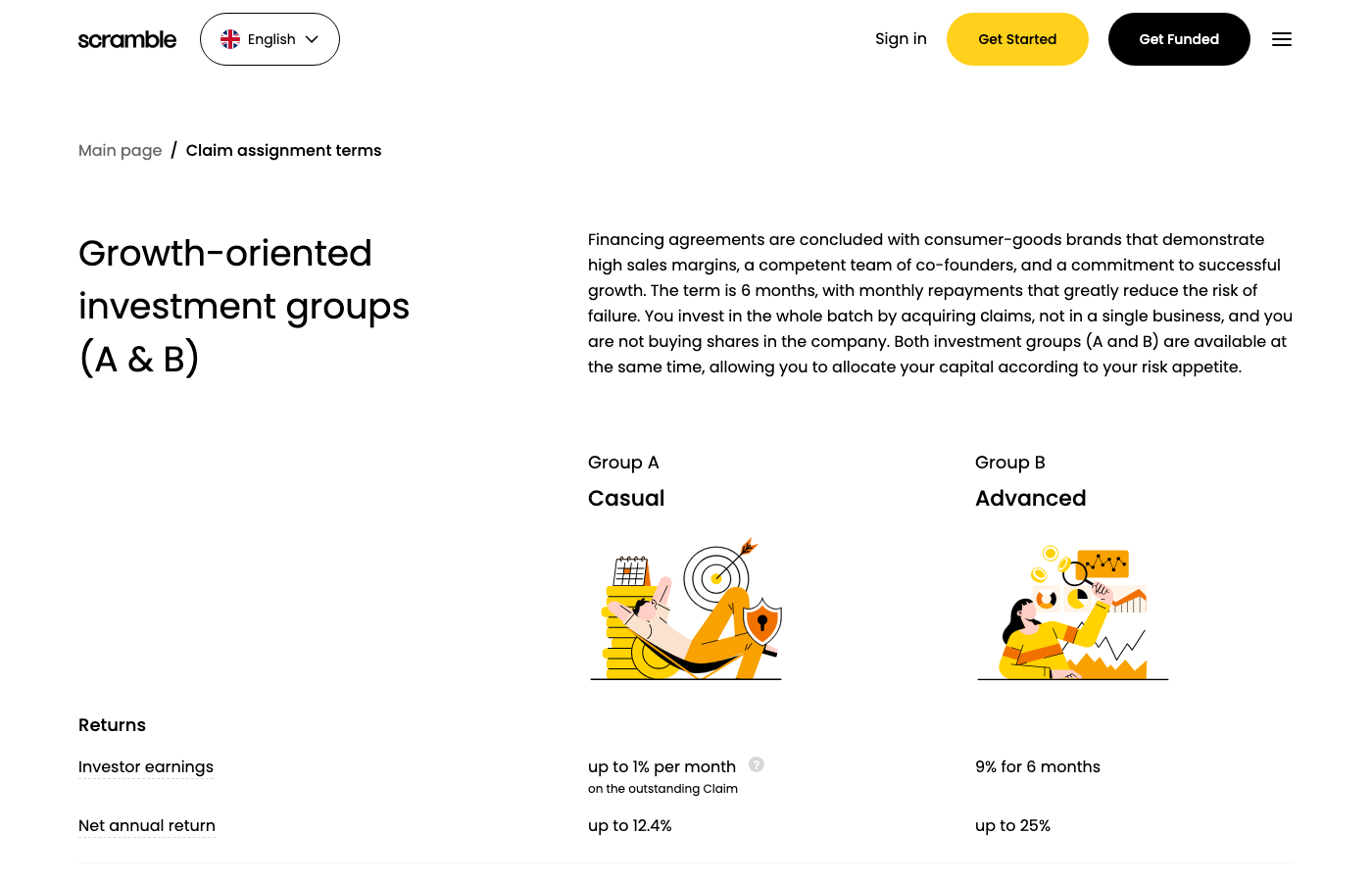

Group A vs. Group B

Scramble splits each deal into two investor tiers with very different risk-return profiles.

Group A (senior): You earn up to 12.4% annualized and receive monthly interest payments. Group A investments have a 15% first-loss buffer funded by Group B investors — meaning Group B absorbs the first 15% of any losses before Group A is touched. Group A is also described as “triple-secured,” with upfront borrower fees, monthly repayments, and co-founder personal guarantees.

Group B (junior): You earn up to 25% annualized but receive no payments until the loan matures — it’s a bullet structure, meaning you wait 6 months for both principal and interest. Group B is repaid only after Group A, making it genuinely subordinate. The higher yield reflects that real extra risk, not just marketing copy.

Fees are zero for investors. Borrowers pay 5% per 6-month term for Group A funding and 9% for Group B.

Returns and Risk

The platform claims a 16.54% annualized average across all deals. That’s an attractive number, but “up to” language matters here. Not every deal offers the maximum rate, and the mix of Group A and Group B in your portfolio will heavily influence your actual return.

The on-time repayment rate is 84%, which means 16% of loans have been delayed at some point. Scramble is transparent about this figure, which I appreciate — but delayed is not the same as defaulted, and the platform doesn’t yet publish granular data on how many delayed loans ultimately resolved versus resulted in a loss to investors. That gap in reporting is something to factor into your expectations.

There is no secondary market, so once you’re in a deal, your money is locked until repayment. If a borrower extends to 24 months, you wait 24 months. There’s no auto-invest feature either, so you need to log in and pick deals manually.

The Regulation Question

This is the most important section of this review, and I want to be direct about it.

Scramble is unregulated. It does not hold a European Crowdfunding Service Provider (ECSP) license under EU Regulation 2020/1503. That regulation governs investment-based crowdfunding platforms operating in the EU, and ECSP authorization carries meaningful investor protections — including mandatory disclosures, risk warnings, and conduct requirements supervised by a national regulator.

Scramble has not obtained this license. The platform operates under a legal structure (claims assignment) that it argues places it outside the scope of ECSP regulation. That may be legally defensible — it’s not an uncommon approach among early-stage fintech platforms — but it means you have no regulatory backstop. If Scramble fails, mismanages funds, or acts improperly, you have no regulator to complain to and no compensation scheme to fall back on.

This doesn’t automatically make Scramble a bad platform. Regulation is not a quality guarantee. But the absence of it is a material risk that needs to be in your decision-making, not buried in the fine print.

Company Financial Health

Scramble’s 2024 financials are public, and they paint a picture of an early-stage company that is still far from profitable.

- Revenue: EUR 186,293 (up sharply from EUR 8,288 the prior year, but still very small)

- Net loss: EUR -366,411

- Cash: EUR 440,854 (down from EUR 1.03M the year before)

- Total equity: EUR -1.63M (negative)

- Only 2 FTE employees registered in Estonia

- Primarily funded by convertible loans from related parties at 10-15% interest

Negative equity means liabilities exceed assets. It’s not unusual for an early-stage startup, particularly one funded through convertible instruments, but it does mean the company itself is not financially self-sustaining. Scramble is burning cash, growing slowly on the revenue side, and relying on its backers — who include the founder of Wise, a former chairman of Skype, and a former CTO of Pipedrive — to keep the lights on.

The VC backing is genuinely notable and lends credibility to the founders’ vision. But VC support is discretionary, not contractual. If the platform hits a bad patch, there’s no legal obligation for shareholders to continue funding it.

Investor Protection: What’s There and What Isn’t

Here’s an honest accounting of what protections exist.

What you have:

- Investor funds are segregated in accounts at LHV Bank, a well-regarded Estonian bank. Your uninvested cash isn’t mixed with Scramble’s operating funds.

- Group A investments have a 15% first-loss buffer provided by Group B investors in the same deal.

- Co-founder personal guarantees on loans — up to 40% per founder (80-100% with multiple co-founders) using lifetime income over 5 years.

- A voluntary safety fund, funded by VC shareholders, has covered all defaults since early 2022.

What you don’t have:

- No buyback guarantee

- No secondary market to exit early

- No regulatory compensation scheme

- No contractual obligation from shareholders to keep the safety fund funded

- No auto-invest — you manage everything manually

The safety fund is worth noting in both columns. It’s real, and the platform has a track record of honoring it. But “voluntary” means it can be withdrawn. Don’t underwrite your risk tolerance based on its continued existence.

Who Scramble Is For

Scramble makes sense as a small allocation within a diversified P2P portfolio for investors who:

- Can tolerate illiquidity — no secondary market means capital is locked for the loan term

- Understand and accept unregulated platform risk

- Want exposure to an asset class (consumer brand working capital) that most platforms don’t offer

- Are comfortable with the company’s early-stage financial position

- Are investing an amount they can afford to lose entirely

Scramble is not suitable for you if:

- You need liquidity or may need to access your funds before the loan matures

- You’re looking for a regulated, licensed investment platform

- You’re allocating a significant portion of your investable capital

- You’re new to P2P investing and don’t yet have a baseline feel for platform risk

Frequently Asked Questions

Is Scramble safe?

No P2P platform is “safe” in the conventional sense, and Scramble is riskier than most because it’s unregulated, early-stage, and operates in a niche market. Investor funds are segregated at LHV Bank, and a voluntary safety fund exists for defaults — but neither of these removes the fundamental risks of lending to early-stage brands or of the platform itself encountering financial difficulties.

What happens if Scramble goes bankrupt?

Investor funds are held separately at LHV Bank, so they’re not part of Scramble’s estate in an insolvency. However, recovering your money from active loan positions would depend on whether an administrator could service those loans — which is uncertain and potentially slow. The absence of regulatory oversight makes this scenario harder to navigate than it would be on a licensed platform.

Can I withdraw my money early?

No. There is no secondary market and no early exit mechanism. Once you invest in a deal, your funds are locked until the borrower repays. Loans run 6 months with a possible extension to 24 months.

My Opinion on Scramble

Scramble has a genuinely interesting angle. Consumer brand working capital is an underserved niche in the P2P space, the founding team has real credentials, and the platform’s transparency on stats like its 84% on-time rate is better than average for a platform this size.

But I can’t look past the combination of negative equity, no ECSP license, no secondary market, and a voluntary (not contractual) safety fund. Each of these is manageable on its own. Together, they paint a picture of meaningful platform risk — not just borrower default risk — that you need to price in before investing.

My view: if you’re an experienced P2P investor who has already covered the regulated, liquid options in your portfolio, Scramble could be a small, high-risk satellite position worth exploring. If you’re newer to this space, or if capital preservation is a priority, look elsewhere first.

Disclosure: This article contains affiliate links. If you sign up through my link, I may earn a commission at no extra cost to you. I only recommend platforms I have personally researched or used. This is not financial advice.

Related

Leave a Reply