- Mintos is Europe’s largest P2P lending marketplace, regulated under MiFID II in Latvia

- After 9 years and EUR 150,000+ invested, my net annual return averages ~9%

- 60+ loan originators across 33 countries with a buyback obligation on most loans

- Best for experienced investors comfortable with originator risk — not suitable as emergency savings

- Pursuing a full banking license in 2026

Mintos is a multi-asset investment platform in Europe. Like many other FinTech companies of this type, it is based in the Baltic region; in Latvia specifically.

Currently, Mintos has four offices employing more than 160 people in Riga, Vilnius, Berlin and Warsaw.

Mintos started operating in 2015 but has experienced rapid growth due to getting many things right and becoming popular with financial bloggers due to its ease of use and transparency.

The average interest rate is around 12%, with more than 700,000 investors registered worldwide and over 800 million euros currently under management.

Another important statistic to look at is the loan book growth, and here again, Mintos is doing very well as can be seen in the following screenshot.

The total money invested so far is more than 12 billion euros, which is a staggering number and a testament to the platform’s growth. There is no doubt that Mintos is the biggest player in P2P lending in Europe at the moment, with the largest share of the European P2P lending market by a wide margin. There are some good competitors, but none of them provide the security and track record that Mintos does.

The management team of Mintos is clearly displayed on the website with links to the Linkedin profiles of each person on the team. Mintos is currently the biggest employer in the P2P lending space.

Being able to view the team and also check out various YouTube videos with their CEO Martins Sulte enhances the feeling of transparency and peace of mind. I am one of those who take a look at these pages on a website and use them when judging whether I should invest on a platform or not. Everything counts.

I have personally interviewed Martins on my podcast Mastermind.fm, so be sure to check out that episode if you like podcasts.

Mintos obtained its investment firm license in 2021 and now operates under the MiFID II framework across Europe. This is the same regulatory standard that governs banks and brokerages, and it comes with an additional layer of security via the EUR 20,000 investor protection scheme. Investment products on the platform are structured as Notes, which are regulated financial instruments under EU securities law. The platform ranked 3rd among 30 P2P platforms in 2025, confirming its position as one of the top choices for European investors.

Finally and very importantly, Mintos as a company is profitable, so they are not only running on investor money but are actually turning a profit, which means that they have a much higher chance of standing the test of time compared to some other competitors that are still in startup mode. In February 2026, Mintos announced it is pursuing a full banking license in Latvia, which would be a transformative step for the platform — allowing it to offer deposit accounts and potentially other banking services alongside its investment products.

The biggest number of investors come from Germany, Spain and the Czech Republic respectively, but this is mostly a reflection of those countries’ familiarity with this type of investing. There are more than 700,000 investors that have used Mintos and they come from 90+ countries.

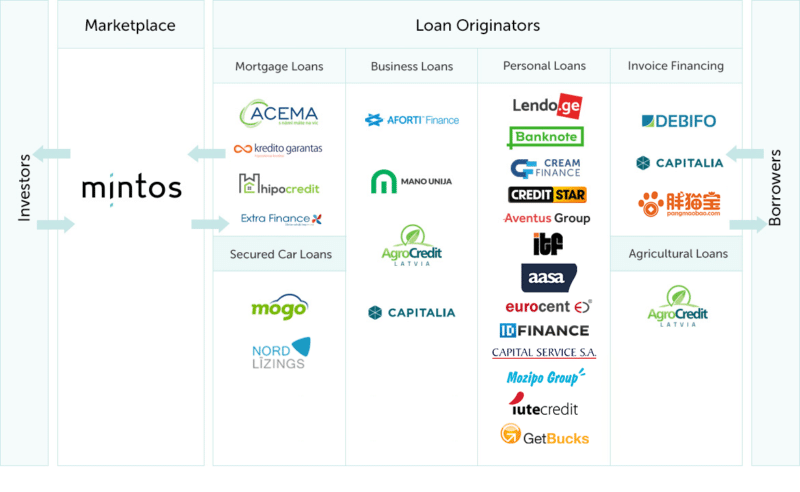

More than 60 lending companies offer their loans on the Mintos platform, with over 25,000 people working at these companies and spread over 33 countries, so you can have a global reach when investing on Mintos.

The company supports 10 languages via its multilingual support team, while the website is available in 6 languages and there are loans available in multiple currencies.

How Does Mintos Work?

Mintos is a loan aggregator, which means that it partners with loan originators worldwide to bring in their loans onto the platform. These loans would be pre-funded, which means that the originators themselves have supplied the loan to the end customer, and are now reselling part of that loan to us investors via Mintos.

The people at Mintos conduct their research on each loan originator periodically and assign them a score based on various factors. They also provide information pages on each of these originators so that as an investor you can easily learn more about them. No other platform in Europe currently has anywhere close to the number of loan originators that Mintos has. This contributes to the huge loan pool that Mintos currently has and improves liquidity.

Every loan originator is required to have skin in the game, and many of them also provide a buyback obligation.

The buyback obligation means that if a borrower defaults, the loan originator will automatically buy back the defaulted loan from the investors and also pay them interest for the period during which the loan was in default.

Some people have thus asked me where is the risk in investing in Mintos when loans come with a buyback obligation. We will have a look at the risks later but to answer that question, the risk is that the loan originator itself goes out of business. This has happened multiple times over the years, with several loan originators defaulting on their buyback obligations. The platform currently carries around EUR 130 million in unresolved defaults from past originator failures. Mintos has a claims management process in place, but recovery rates have been mixed. I personally treat any funds tied to defaulted originators as bad debts and assume they won’t be recovered.

Some people have thus asked me where is the risk in investing in Mintos when loans come with a buyback obligation. We will have a look at the risks later but to answer that question, the risk is that the loan originator itself goes out of business. This has happened multiple times over the years, with several loan originators defaulting on their buyback obligations. The platform currently carries around EUR 130 million in unresolved defaults from past originator failures. Mintos has a claims management process in place, but recovery rates have been mixed. I personally treat any funds tied to defaulted originators as bad debts and assume they won’t be recovered.

Mintos has historically been fee-free for investors, but that has started to change. Since May 2025, there is a new annual fee of 0.29% on Custom Loan Portfolios. Additionally, the High-Yield Bonds Portfolio (launched November 2025) carries a 0.39% annual management fee starting in 2026. These fees are still reasonable compared to traditional investment products, but they’re worth factoring into your expected returns. Taxes are to be declared and paid in your country of residence and Mintos does not withhold any taxes. Rest assured though that this won’t be a hassle as it’s pretty straightforward to declare your income from P2P platforms in your tax return. I suggest you consult an accountant the first time you do it, and for the subsequent years, you can do it yourself.

Mintos is therefore just the go-between bringing together loan originators and investors. This allows investors to use one website to diversify their investments across several countries, loan types and even different currencies.

You can deposit either Euros or USD into your Mintos account, and there is a 1% charge for currency conversions. I have actually used Mintos to “save money” on currency conversions, feel free to take a look at my separate post on how to save money with currency conversions.

Beyond loans, Mintos now also offers fractional bonds and ETFs, making it a broader investment platform. The minimum investment is EUR 10 per loan.

In simple terms, here’s how loan investing on Mintos works:

- Lenders place loans on Mintos to finance their operations

- You invest in loans, thus providing financing to lenders

- Borrowers pay back loans in monthly installments

- You get the earnings and invest again or withdraw

Who is Investing on Mintos?

You might think that investing is something exclusive that only very knowledgeable people can partake in, but this is not true. Anyone with a basic knowledge of money and an interest to learn more about it is a good candidate for investing in P2P lending.

I spoke with Mintos and asked them about the typical profiles for their lenders, and they told me that they come from all walks of life and the amounts invested range from a few hundred euros to millions of euros. In the end, it doesn’t matter how much you invest, everyone can get the same returns on their investment in terms of percentage ROI.

You might also be under the false impression that only residents of certain countries are allowed to invest. This is far from the truth, as you can invest from all over the world, with only a few restrictions based on EU regulations. If you’re an EU resident, you can definitely invest.

To give you an idea, the top countries I’m seeing new investors join from after reading my articles or contacting me are the following: UK, USA, Germany, Netherlands, France, Spain, Belgium and Malta.

I’ve also seen strong activity from Asian countries such as India and China. I think Mintos is proving to be an excellent way for non-European investors to gain access and exposure to the European market and earn Euros, which is also a way for them to hedge against currency risks.

Mintos is open to both private and corporate investors. So if you want to invest via your company, you can easily do so.

What Can You Invest in?

At Mintos, investors can invest in different types of loans originated by many different loan originators.

Loans can be of the following types, and you can, of course, limit your investment to specific types when setting up your automated strategy.

- Mortgage Loans

- Car Loans

- Invoice Financing

- Business Loans

- Short-term Loans

- Personal Loans

- Agricultural Loans

In November 2025, Mintos launched a High-Yield Bonds Portfolio, giving investors access to a curated selection of high-yield corporate bonds. This carries a 0.39% annual management fee from 2026, but offers another way to diversify beyond P2P loans.

Mintos also offers Buy Now Pay Later (BNPL) loans. These are the microloans you see at checkout when shopping online — buy the product now, pay by installments over several months. BNPL has grown rapidly across Europe and represents another loan category available for investment on the platform.

Where Can You Invest via Mintos?

Another question is which countries you can invest in via Mintos. To make sure we are well diversified, it’s important that we spread our investments across different countries to reduce our reliance on any one country’s economic performance. We can further add another layer of diversification by investing in loans denominated in several different currencies.

With Mintos, you have the option of investing across dozens of countries and multiple currencies. This makes it the most well-diversified platform that I know about. Over the years, Mintos has expanded the investment opportunities on the marketplace beyond Europe by offering loans in Africa, Latin America, and Southeast Asia.

How I’m Investing in Mintos

I am currently using several custom automated strategies that I tweak every few months as necessary. If you don’t feel confident setting up all the parameters yourself, you can use Core Loans, the premade automated portfolio offered by Mintos, and I’ll cover that later in this article.

Over nine years of investing on Mintos, my average net annual return has been around 9%. That accounts for the good years (11-12% in the early days), the rough patches (COVID in 2020 and the Russian originator defaults in 2022), and the recovery since. It’s a realistic number for a diversified investor who stuck with the platform through its ups and downs.

I have invested over €150,000 into the platform over the years. The originator defaults that hit me directly were relatively minor — around €600 total across affected originators — a small amount relative to overall profits. That is largely because I keep my portfolio widely diversified across originators and geographies and use the buyback obligation consistently.

The general support via email, phone, and online chat is solid.

Core Loans: The Premade Portfolio

If you don’t want to set up your own custom strategy, Mintos offers Core Loans, a premade automated portfolio that handles everything for you. Core Loans diversifies your investment across loans from multiple lending companies, automatically adjusting the portfolio mix based on market conditions.

To get started, you just select the amount you want to invest. The algorithm handles loan selection, diversification across originators and geographies, and reinvestment of returned principal. It’s the simplest way to start investing on Mintos if you don’t have much experience or just want a hands-off approach.

Core Loans comes with a cashout option that lets you access your money faster (subject to market demand), providing additional liquidity compared to building a fully custom portfolio.

Using Custom Strategies

Obviously manually selecting thousands of loans to comprise your portfolio is a very inefficient way of doing things, although it might be a good way to test the waters if it’s the first time you are dealing with a peer to peer loan platform. It is perfectly OK to invest a set amount and then just wait a month or two to judge the results of your investment and learn how the platform works. Once you’re confident about the platform, you can then set up an automated strategy and be well on your way to passive income.

You have to be careful when setting the automated strategy parameters on Mintos, because the biggest risk you face is that of a loan originator going bankrupt, and that has happened in the past. Mintos assigns a Risk Score to every loan originator on the marketplace, which you can review to help decide which originators to include in your custom strategy.

Here’s how I go about building a custom strategy.

By setting up automated strategy with a custom strategy, we are looking to combine the benefits of compounding interest with the safety of the buyback obligation.

The first step when creating a custom strategy is that of choosing the loan originators you want to invest in. Keep in mind that there are several loan originators that are not profitable and are relying on their seed investment runway until they do achieve profitability. I prefer to use those that have already proven that they know what they are doing and are turning healthy yearly profits.

We have to keep in mind that peer to peer loan investing is in itself a risky proposition, so there is no sense in increasing that risk by going for unprofitable loan originators. Once you consider all loan originators, you might end up with 15-20 of them that you are comfortable investing in.

Beyond that, you can set up a bunch of other parameters like the loan duration, rate of return, countries, loan types, whether they have buyback or not etc.

A lot of these parameters will depend on your goals, so there is little sense in telling you my exact parameters, because even then, I go in and change them every now and then depending on what I want to achieve during a particular period.

Real Estate Investment Opportunities with Mintos

Mintos has expanded into real estate, allowing you to invest in rental residential properties starting from just EUR 50. You earn a share of the rental income from tenants and may also benefit from capital appreciation over time. I haven’t personally used this feature extensively, as I prefer to keep my Mintos portfolio focused on loans, but it’s a useful diversification option if you want real estate exposure without buying property directly.

The real estate investments are also available on the secondary market, so you’re not fully locked in if you need to exit before the investment term ends.

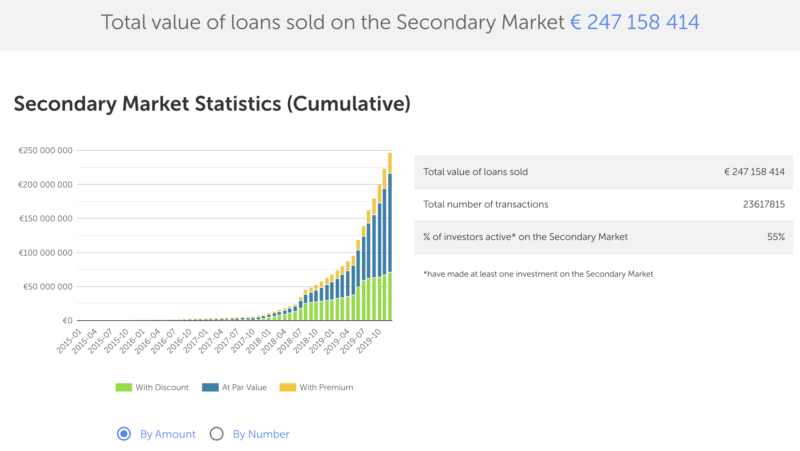

The Mintos Secondary Market

I think the secondary market deserves its own section as it has become such an important part of the platform. The secondary market is what gives Mintos the capability to have such high liquidity for its investors. I know investors who have sold over 1 million euros from their portfolio in just a few days’ time. The way to offload loans if you need cash is to sell them on the secondary market.

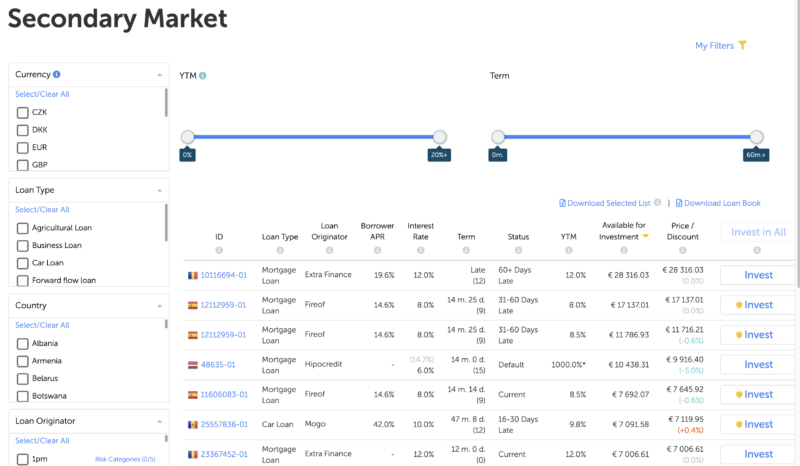

Buying and selling loans on the secondary market is very easy. If you want to buy, you can set up an automated strategy to pick up loans specifically from the secondary market, with the same criteria as you are able to set up for the primary market.

You can also manually buy loans from the secondary market from the dedicated page on the Mintos website (shown above). You can of course filter according to your wishes and then click the Invest button to buy those loans. Many investors try to pick up good loans at a discount and thus improve their rate of return even further.

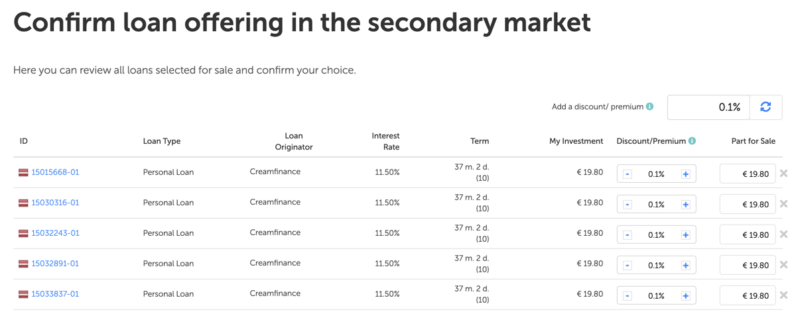

If you are looking for very quick liquidity, you can select the loans you possess, and then hit the Sell All button to sell them off on the secondary market. Before you do that, it would be a good idea to set a small discount on those loans, as that will make them much more likely to be picked up by other investors looking for bargains and extra profits.

The secondary market is huge on Mintos. The secondary market typically has more loans available than the primary market.

There is a small 0.85% fee for selling loans on the Secondary Market. I think it’s a fair and transparent fee that will help Mintos stay profitable, and it’s on par with or below other leading platforms in Europe and the UK. Mintos reports that a significant proportion of active investors use the Secondary Market regularly. This 0.85% fee will apply to investors selling their investment on the Secondary Market, and will be applied after the sale.

The Secondary Market thus offers considerably liquidity to those investors who want to exit an investment early and is a very important component in this platform. If Mintos did not have such a good secondary market, I would not have invested such a big amount of money here.

Depositing and Withdrawing Money

Deposits and withdrawals on Mintos are free and processed without delays. If your bank charges fees for SEPA transfers, consider using a digital bank like N26, Revolut, or Wise to avoid unnecessary costs. You can check out my guide to depositing and withdrawing money from P2P platforms for more detail.

Mintos Risk Score

When you set up an automated strategy, you will notice that all loan originators have been assigned a Mintos Risk Score. The Risk Score is Mintos’s proprietary assessment framework for evaluating each loan originator’s financial and operational stability. It replaced the earlier rating system and provides a more comprehensive view of counterparty risk.

The Mintos Risk Score measures the risk of loss resulting from a loan originator’s failure to service loans, transfer payments from borrowers to investors, or meet other contractual obligations including the buyback obligation. It captures both the operational risk and default risk of each company acting as a loan originator and servicer on the platform.

The Risk Score is driven by five core factors characterizing each loan originator: operating environment (10% factor weight), company profile (15%), management and strategy (15%), risk appetite (20%) and financial profile (40%). Additionally, a support factor is incorporated for loan originators who receive guarantees from the group or a related company.

The Mintos Risk Score is based on information obtained during the initial due diligence process and data from ongoing monitoring. This includes the primary information from loan originators such as management interviews, site visits, audited and interim financial statements, corporate presentation, credit policy and risk control documents. The score is updated annually, except in certain instances where a loan originator’s score requires an immediate change. This could be due to a cash injection, positive or negative regulation being implemented in the country of the loan originator and so on.

I would recommend doing your own research on loan originators if you are investing big sums of money. For smaller amounts, the Mintos Risk Score is a reasonable guide for selecting originators.

Potential Downsides of Investing with Mintos

Let’s have a look at the main risks of investing in P2P lending and Mintos in particular.

Loan Originator Risk

As we have already mentioned, P2P lending is a moderate-risk investment, and you must be aware that loans can default. With Mintos, you get a buyback obligation as we discussed earlier. Thus the biggest potential downside of investing with Mintos is that a loan originator goes bankrupt, as described earlier in this review.

The only way to mitigate this risk is to keep an eye on the profitability of the loan originator. Most of them release their financial reports to the public every year, so you can see how they are doing. This is not as easy as it sounds, however.

Only 38% provide audited financial statements. Unaudited financial statements are not as trustworthy when compared to audited ones. You’re basically relying on what the business is saying about itself rather than what a trusted 3rd party (audit firm) is saying.

Almost 45% of loan originators are not profitable. It’s quite normal for new businesses in this space to be unprofitable for the first few years, but you also have to factor in the increased risk of them spending all the investor money before they turn profitable, which leads to complications including bankruptcy.

Around 80% of the loan originators are less than 10 years old, which means that they were founded after the last great world recession and we don’t know how they will perform if another one hits in the coming years. During a world recession, credit companies are some of the hardest hit as borrowers default on their loans due to having lost their jobs or having experienced severe pay cuts.

Interest Rate Risk

One other risk is that interest rates rise in the future, making it harder for you to sell your existing loans with lower interest returns on the secondary market, if you wished to do that. Of course, you could also just let the loans run their course and continue receiving payments until maturity.

When investing on P2P platforms, it’s best to invest money that you can afford to use without running into severe financial troubles. That way, you minimise the chances of having to sell loans prematurely, potentially at a time that is not advantageous.

Cash Drag Risk

Cash drag varies among different P2P lending sites, and thankfully this hasn’t been a problem with Mintos. Mintos is extremely liquid meaning that you can throw thousands of Euros at the platform and see them invested within minutes, and conversely, you can also sell your loans on the secondary market within a day or two.

Although it is not currently a problem, it could become so at any point in time, even though it might only be for a short time. If there is a surge in popularity for P2P lending platforms, we will have a situation where lots of lenders are competing to lend while there are not enough borrowers, which will result in a higher cash drag, because you have to wait your turn.

To put this into practice, let’s say that the interest rates you earn when lending are 10%, but, on average during the year, half your money is sitting as cash in your lending account with no borrowers available. With just half your money being lent and the other half in cash, it means you’re actually earning just 5%.

That’s an extreme example. Cash drag is not usually anything like that much. In fact, it typically reduces a 10% rate down to between 9.4% and 9.8%.

Considering these potential downsides, I think that investing in P2P lending platforms and Mintos, in particular, is a very good deal for investors, because there aren’t any other readily available investment opportunities with such a favorable risk-return profile.

Moreover, Mintos is currently the biggest platform in Europe and has proved itself to be competent by providing great communication with its investors as well as a very liquid primary and secondary market for loans for several years now.

Foreign Exchange Risk (or Opportunity)

You can invest in loans denominated in currencies other than EUR, including USD and GBP. This means that when you convert back to Euro, you might lose money depending on how the rates have moved in the meantime. This could, however, also be an opportunity to make extra returns. I’ve seen investors using currency arbitrage to raise their overall returns to 15-20% which is really impressive.

I like to keep things simple myself so I only invest in Euro. I also use Mintos to minimise the cost of currency conversions.

If you want to invest in other currencies, I would recommend using a platform like Wise; in that way, you’ll avoid the Mintos commission on exchanges.

Frequently Asked Questions about Mintos

I’ve spoken to many people about Mintos and I get to hear many questions that investors seem to have in common, so I’ll try to address them in this section. If you have any other questions you’d like me to address, just leave a comment below the post.

How can I reduce the number of late loans? e.g. 1-15, 15-30, 30-60 etc

I don’t think you can really avoid that unless perhaps you study your portfolio’s performance and identify if there are any specific factors that result in loans being regularly late, for example, loans from a particular country or a particular type. This is not something that I’m too concerned about, plus I don’t really get into hyper optimization with my portfolios as I don’t feel it justifies the time investment given the yearly returns. Therefore I haven’t done such a study myself. However, if any of you reading this post do conduct such a study, I’d definitely be interested to know what you find out.

What are pending payments?

In your dashboard, you will sometimes see some money that is marked as pending payment. This means that Mintos is gathering the money and preparing it for distribution.

If this happens, you will be compensated for the delays in settling pending payments.

The interest on pending payments is 1.2x the interest of the loan in question. You can expect to receive the interest weekly, once it’s paid by the respective lending company.

The interest will be calculated for both the principal and interest and the calculation will begin after the settlement period (7 days) has ended.

How are loan returns taxed?

Mintos sends you the returns gross of tax; they don’t withhold any taxes. You will, therefore, have to declare the income in your country of residence, as explained in further detail in my post about P2P lending platform taxation. I’ve also written a post about how crowdlending is taxed in Spain specifically.

Do you recommend just investing in Mintos or do you recommend spreading your money across different platforms?

Mintos is my preferred platform and its where I invest most of my P2P portfolio, but I would always recommend spreading your capital across different platforms.

What returns can I expect?

The headline interest rates on Mintos range from 10% to 14%, but your actual net return will be lower once you account for originator defaults, cash drag, and the occasional rough year (like 2020 and 2022). Over nine years, my own average has been around 9% net. That’s a realistic benchmark for a diversified, long-term investor.

I don’t have as much capital as you to invest, what is the minimum to invest at Mintos or P2P sites in general?

I would say that you can start with as little as €1,000 to see how things work on any of my recommended platforms, but to make any meaningful income you need to invest at least €10,000. Anything less than that is not worth the time and hassle in my opinion. If you have more than that amount to invest, then it’s even better.

Does Mintos allow investments in cryptocurrencies?

No, this is not something that Mintos provides at the moment, but I wouldn’t be surprised if they branch into this area in the future. For now, you could have a look at my article on the best P2P crypto loan platforms.

I am a bit worried about having a significant number of loans that are late. Is it normal?

Yes, it’s normal to have a portion of your loans being late with their principal and interest payments. On a diversified portfolio, it is common to see around 20-30% of loans in some stage of lateness. Here’s roughly what to expect:

- Grace Period: a small percentage

- 1-15 Days Late: the largest group

- 16-30 Days Late: moderate

- 31-60 Days Late: smaller percentage

The exact percentages fluctuate over time, but having a significant portion of loans in various stages of lateness is normal for this asset class. What matters is that your loans are covered by a buyback obligation.

There should be no loans beyond 60+ Days Late if you’re using buyback obligation, as that would mean the loan originator is having problems buying back the loans. Any loans I have that are 60+ Days Late belong to originators that defaulted on their obligations and are now in recovery.

How long would it take for me to sell all my loan portfolio should I need quick liquidity?

From my experience in tests I’ve conducted and also those done by other investors I’ve spoken to, it takes between 24 to 72 hours to sell a complete portfolio. Size doesn’t seem to be a problem, as I know people who have sold 7 figure portfolios on the secondary market in this short timeframe.

Whether you can sell your loans at par or whether you’d need to apply a discount depends on what kind of rates loan originators are offering at the moment you decide to sell versus what rates they were offering when you bought. For example, if you invested in Mogo loans at 11% 6 months ago and the average for Mogo loans is now 12%, nobody is going to buy your loans unless you offer them at a discount.

In the end, you might have to give up an equivalent of a week or two of interest income to sell your loan portfolio, which I think is a good tradeoff.

I see capital gains in my account, how is that calculated?

Mintos calculates the positive gain on a loan-level for investments on the Secondary market. For example, if an investor invested into a loan this year and it will be fully repaid only the next year then in the capital gain of this year the gain will not be calculated as the income from the loan is lower than the invested amount. Unfortunately, it is not easy to calculate as Mintos looks at all the previous years as well.

Here is an example: say you invested 90 EUR in a loan and received 100 EUR back from the borrower when the loan finished. The capital gain is 10 EUR.

If however only half of the principal was repaid in the first year, the capital gain for that year is 0 EUR. If the loan is repaid in full the following year and the total funds received reach 100 EUR, then the capital gain for that year will be 10 EUR.

The data can be found under Account Statement, but then you have to look at all the previous years in which you have earned with Discount / Premium on Secondary market transactions and which loans were fully repaid in a given year.

Mintos Mobile App

The Mintos mobile app provides a significant differentiator for Mintos when compared to other competitors in the space. It’s extremely well-made from a technical and usability point of view. My background is in creating software so I know a well-made product when I see one. I’ve also used and cursed at a ton of banking apps that had the most horrifying UI and nonsensical errors thrown at their users.

There are no such mishaps with the Mintos app. It has a light and dark mode (white or black background) and it shows you all the most important stats about your investments. You can withdraw or deposit money, and operate in both the primary and secondary markets directly from the app — so you may never need to log into the website at all. Given that most people operate exclusively from their phones these days, it’s an obvious step for platforms such as Mintos as they strive to reach a wider audience and make things easier for their existing investors.

I especially like the stats section as I can quickly check the vital stats on my money, including the countries I’m invested in, the lending companies, the average interest rate, average remaining term and amount of late loans. These are all stats that are also available on the site, but they are not as easily and readily available. Let’s not forget that there is much more friction in sitting down at your desk, opening a website, logging in and navigating to the pages you need, when compared to opening a mobile app that’s always logged in and shows pretty and easy-to-read stats immediately.

What Improvements Would I Like to See from Mintos?

Better Statistics

We can see the cumulative number of investors on the Mintos statistics page, however, there is no clear indication of how many users joined every month and more importantly how many of them are even active. Many users can sign up but then never invest, and that is not reflected in the stats.

The same goes for the investment volumes section of the statistics. We can see the cumulative investment growing month by month, but we don’t have information on how many new loans were issued each month. This would give a clearer picture of volumes month by month.

With regards to loans, Mintos gives us a breakdown of Current vs Delayed loans, but in reality, the term “Current” is not 100% accurate. It is a catch-all for recently issued loans that have not reached their first repayment date, as well as those loans that have been paying back principal and interest successfully. There is obviously more uncertainty and risk with loans that have not started their repayments, so they should not be bundled together with the others that are being repaid already.

Ownership & Related Parties Transparency

There are some long-standing doubts about the ownership of Mintos and its relation to some of the loan originators on the platform. The ultimate beneficiary owner of Mintos is Aigars Kesenfelds. He is currently the true beneficiary of numerous Latvian companies. At the same time, he owns no shares in any company.

This businessman is the true beneficiary in several real estate companies, as well as a firm that offers self-service carwash – SIA Wash and Drive, AS Skanstes Biroju Centres, SIA Mintos Finance and others. Kesenfelds’ interests in those companies are represented by AS ALPS Investments, as well as Malta-based Dyonne Trading & Investments Limited and other companies of this kind.

More Details on Loan Originators and Their Loans

I’d like to see more details such as audited statements for each loan originator, as well as a breakdown of loans issued by country, default rates and recovery rates.

Previous Concerns that Have Been Addressed

I have previously criticized Mintos over its lack of profitability and lack of transparency in the ownership structure. However, both issues are now solved, as Mintos is profitable and has a healthy cash balance in the bank, and the shareholders and original founders are clearly mentioned on the site now.

As for regulation, Mintos is now operating under EU securities law with its transition to Notes, and as mentioned earlier, is pursuing a full banking license in Latvia.

How Does Mintos Compare?

See how Mintos stacks up against other popular platforms:

- Mintos vs PeerBerry — Which Is Better in 2026?

- Mintos vs Bondora — Which Is Better in 2026?

- Mintos vs Robocash — Which Is Better in 2026?

- Mintos vs ViaInvest — Which Is Better in 2026?

Mintos Alternatives

Many people are skeptical about P2P lending platforms and prefer to diversify their investments across multiple platforms in case things go south on one of them. While I think Mintos is currently the best platform in Europe, there are others that are right up there vying for that number one position with Mintos. They would be worth looking into and possibly used to diversify your portfolio along with your Mintos investment.

Here are my favorites:

You can see my full list of recommended European P2P lending platforms for more options.

Final Thoughts on Mintos

I’ve been investing on Mintos for over nine years now, and I’ve seen the platform grow from strength to strength. The transition to Notes, the pursuit of a banking license, and the launch of new products like the High-Yield Bonds Portfolio all signal that Mintos is evolving beyond a simple P2P lending marketplace.

I think one should be realistic and understand that this is an area of investment with a certain degree of general risk. The introduction of fees (0.29% on Custom Loan Portfolios, 0.39% on the High-Yield Bonds Portfolio) is something to factor in, though these are still modest by industry standards. When I balance the risks versus the return, I feel that investing in such platforms, and Mintos in particular, is justified.

I keep a certain part of my net worth constantly invested in P2P lending platforms to take advantage of their fantastic returns, and Mintos by far holds the biggest portion of this investment. The platform’s 3rd place finish in the re:think P2P community vote for 2025 confirms it remains one of the top choices in Europe. I have no plans of changing my approach, as I have been very happy with the performance over the years.

Therefore, we can wrap this up by saying that Mintos comes highly recommended from me. Please leave any questions you have about the platform below and I’ll be happy to answer them.

Frequently Asked Questions

Is Mintos safe to invest in?

Mintos is licensed under MiFID II by Latvijas Banka, which means investor funds are protected up to EUR 20,000 under the investor compensation scheme. Over 700,000 investors have used the platform since launch. That said, past loan originator defaults left around EUR 130 million in unresolved claims, so the risk of individual originators failing is real and should be factored into your strategy.

What returns does Mintos offer?

Headline interest rates on Mintos range from 10% to 14%, but your actual net return will be lower after accounting for originator defaults and cash drag. Over nine years of investing, my own average has been around 9% net, though many investors target the 11-12% range before any losses.

What is the minimum investment on Mintos?

The minimum investment per loan on Mintos is EUR 10 for most products. Some investment options, like the real estate investments, require a minimum of EUR 50. You can start with a relatively small amount and scale up as you get comfortable with the platform.

Is Mintos regulated?

Yes, Mintos is regulated under MiFID II and licensed by Latvijas Banka, the Latvian financial regulator. The platform transitioned from traditional P2P loans to Notes, which are financial instruments under EU securities law. Mintos is also pursuing a full banking license in Latvia.

Does Mintos have a buyback guarantee?

Yes, most loans on Mintos come with a buyback obligation from the loan originator. If a borrower is more than 60 days late on repayment, the originator is obligated to repurchase the loan at par plus accrued interest. The key risk here is that the buyback is only as strong as the originator behind it.

Summary

Mintos is the largest P2P platform in Europe by volume and the one I have invested the most on u2014 over EUR 150,000 across 9 years. Now fully regulated and transitioning to Notes as financial instruments, it is pursuing a banking license. The 0.29% annual fee introduced in 2025 is worth noting but the platform remains the benchmark in European P2P lending.

Pros

- Great liquidity

- Straightforward to start investing

- Well established platform

- Buyback guarantees

- Mobile app

Cons

- Risk of loan originators defaulting

Related

Os 9% líquidos ao ano como média de nove anos é o número mais honesto que já vi publicado sobre a Mintos. Inclui os anos bons e os anos com defaults de originadores russos e ucranianos. É esse o benchmark realista, não os 12-14% do título.

O que me faz manter posição aqui é a regulação MiFID II e o mercado secundário. Para crédito com garantia real por operação, uso a Maclear onde a plataforma atua como Collateral Agent em cada empréstimo P2B. Para diversificação entre originadores independentes a preços menores, PeerBerry complementa bem. E para crédito empresarial regulado com ABS, o Debitum fecha o conjunto.

Os 130 milhões em defaults por resolver continuam a ser o número que mais importa vigiar. A licença bancária em 2026 pode mudar bastante a equação se se concretizar.