Letsinvest is a Lithuanian real estate crowdfunding platform that lets retail investors participate in mortgage-secured property loans across Lithuania, Latvia, Spain, Portugal, and Norway — with returns advertised at up to 12.5% and a minimum investment of EUR 500.

Letsinvest at a Glance

| Founded | 2014 (company); platform launched late 2020 |

| Legal entity | 8 Stars UAB, Vilnius, Lithuania |

| Regulation | ECSP license (LB002206), Bank of Lithuania, issued July 2023 |

| Investment types | Bridge loans, development loans, bonds, equity stakes |

| Advertised returns | Up to 12.5% (historical average ~10–10.5%) |

| Minimum investment | EUR 500 |

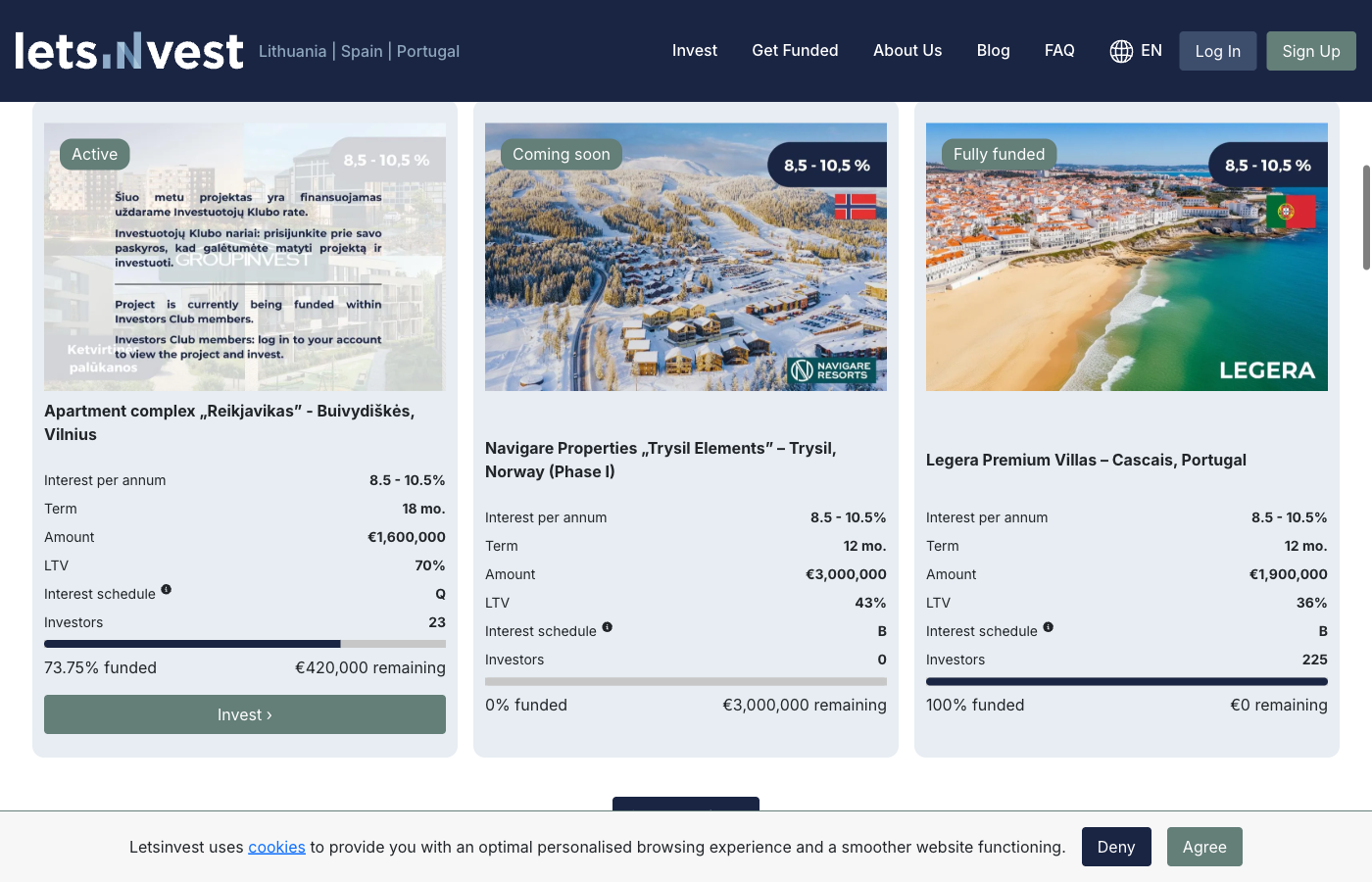

| Project size | EUR 1M–5M per project |

| Operating countries | Lithuania, Latvia, Spain, Portugal, Norway |

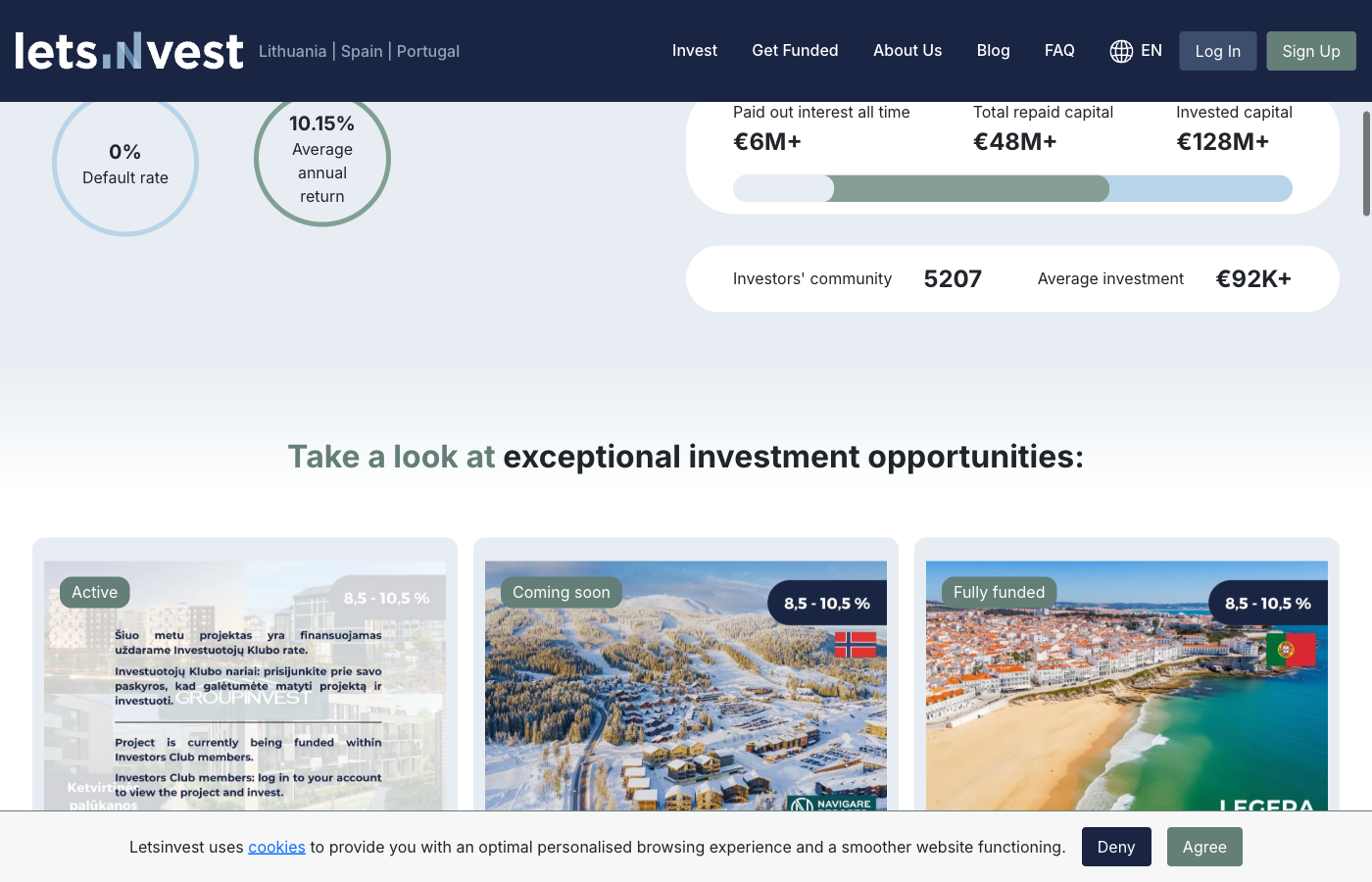

| Total funded | EUR 100M+ lifetime |

| Registered investors | ~4,500–4,800 |

| Defaults | Zero to date |

| Fees for investors | None |

| Auto-invest | No |

| Secondary market | No |

| Buyback guarantee | No |

How Letsinvest Works

Letsinvest operates as a real estate crowdfunding platform under the European Crowdfunding Service Providers (ECSP) regulation. Rather than buying property directly, investors lend money to real estate developers — either as bridge loans (6–12 months) to cover short-term financing gaps, or as longer development loans (12–24 months) tied to construction or renovation projects. The platform has also expanded into bonds and equity stakes.

Every project on the platform is secured by a first-rank mortgage, which means investors hold a priority claim on the underlying property if a borrower defaults. The platform caps loan-to-value ratios at 70–75%, which provides a meaningful buffer before investor capital is at risk. Management co-invests in each project alongside retail investors — a sign of alignment that’s worth noting.

Projects are larger than what you typically see on peer-to-peer platforms. The EUR 1M–5M range per deal means Letsinvest is targeting institutional-grade transactions rather than small-ticket residential loans. You won’t find dozens of new listings per week, but the ones that do appear tend to be more substantial.

There is no auto-invest feature, so you have to manually select and commit to each project. There is also no secondary market, which means once you invest, your capital is locked in until maturity. This is a meaningful constraint for investors who might need liquidity before a 12- or 24-month term ends.

Returns and Track Record

The advertised rate of “up to 12.5%” is technically accurate but worth reading carefully. The actual historical average sits closer to 10–10.5% across the portfolio — still competitive relative to comparable ECSP platforms, but the headline figure shouldn’t be taken as typical. Returns vary by project type and duration, with development loans generally offering higher rates than shorter-term bridge deals.

Since launching in late 2020, Letsinvest has funded over EUR 100 million in projects and reported approximately 90% year-on-year growth in 2025. The platform has posted a profit every year since launch, with 2024 revenue of EUR 1.12 million and net profit of EUR 251,000. Those are modest but consistent numbers for a platform of this size.

The standout data point is zero defaults to date. That sounds impressive, and it is — but it needs context. The platform launched in late 2020 and has operated almost entirely during a period of rising or stable real estate values. It has not been tested by a sustained downturn in any of its operating markets. The zero-default record reflects genuine underwriting discipline, but it also reflects favorable market conditions. Investors should not treat it as a permanent guarantee.

The bullet repayment structure is another factor to understand. Unlike platforms where you receive monthly principal repayments, Letsinvest returns 100% of principal at maturity. That means your capital is fully at risk throughout the entire loan term, and there is no gradual de-risking as repayments come in. You receive interest periodically, but the principal only returns at the end.

Regulation and Investor Protection

Letsinvest holds an ECSP license (LB002206) from the Bank of Lithuania, valid since July 25, 2023. This is a meaningful credential. The ECSP framework is an EU-wide regulation specifically designed for real estate and business crowdfunding platforms, requiring platforms to meet capital, governance, and transparency standards before they can operate cross-border.

The platform has cross-border registrations with Spain’s CNMV, Portugal’s CMVM, and Estonia’s FSA, allowing it to legally accept investors from those jurisdictions. In April 2025, its license was expanded to include securities placement and SPV (special purpose vehicle) operations — a sign of regulatory maturity and ambition.

What ECSP regulation does not provide is a deposit guarantee or access to a compensation scheme. If Letsinvest were to fail as a business, there is no state-backed fund that would make investors whole. The Bank of Lithuania supervises the platform and can intervene, but investor capital is tied to the underlying loans — not held on a protected balance sheet. This is standard for real estate crowdfunding across Europe, but it’s important to be clear about what regulatory oversight actually covers versus what it does not.

The Small Team Question

Letsinvest operates with approximately four employees. That is not a typo. For a platform that has funded over EUR 100 million in real estate projects and manages an active investor base of nearly 5,000 people, the headcount raises questions that deserve honest scrutiny.

CEO Vytenis Kinduris brings 25+ years of business development and real estate experience, and management co-investing in deals is a strong alignment signal. But four people managing deal sourcing, due diligence, investor relations, compliance, and operations creates genuine key-person risk. If one or two critical people leave, the platform’s operational capacity could be materially affected overnight.

The capitalization picture compounds this. Letsinvest’s share capital stands at EUR 50,000 — thin by any standard for a regulated financial services business. The company is profitable, which helps, but the balance sheet offers limited cushion in an adverse scenario. Contrast that with larger ECSP platforms that hold millions in equity capital as a buffer.

The absence of any Trustpilot reviews — with an unclaimed profile — is a separate flag. It does not mean investors are dissatisfied, but it does suggest the platform has not invested in building a public reputation layer. For a business that relies on investor trust, that’s a gap worth noting.

Who Letsinvest Is For — and Who Should Avoid It

Letsinvest suits investors who already have exposure to larger, more established real estate crowdfunding platforms and are looking to diversify into a smaller, mortgage-secured portfolio with a regulated framework. The EUR 500 minimum is accessible, the fee structure is clean, and the ECSP license provides a meaningful baseline of oversight.

The EUR 50,000 VIP tier with a personal advisor is genuinely useful for larger investors who want more access to deal information and direct communication with the team. At that level, the relationship dynamic changes and the key-person concern becomes a feature rather than a bug — you actually know who you’re dealing with.

On the other hand, investors looking for liquidity, an auto-invest tool, or a secondary market should look elsewhere. If you need to be able to exit before maturity, this platform is not designed for you. Similarly, investors who want a platform with a long operational track record through multiple market cycles should factor in that Letsinvest has only existed in broadly benign conditions.

New investors who have no prior experience with crowdfunding or illiquid assets should start with lower minimums and more established platforms before committing EUR 500 to a single project here.

Frequently Asked Questions

Is Letsinvest regulated?

Yes. Letsinvest holds an ECSP license (LB002206) from the Bank of Lithuania, issued in July 2023. It is also cross-border registered with regulators in Spain, Portugal, and Estonia. Regulation does not eliminate investment risk, but it does impose meaningful governance and transparency obligations on the platform.

What is the minimum investment?

EUR 500 per project. This is higher than the EUR 100 minimum the platform operated with previously. The higher floor makes sense given the institutional scale of the projects, but it does mean you need a reasonably sized portfolio to achieve meaningful diversification across multiple deals.

Are there any fees?

No fees for investors. Letsinvest earns its revenue from borrowers, not from the investors participating in the loans.

Is there a secondary market?

No. Once committed to a project, your capital is locked in until maturity. There is no mechanism to sell your position early. Factor this illiquidity into any allocation decision.

What happens if a borrower defaults?

To date, no borrower has defaulted on the platform. In the event of a default, the first-rank mortgage security would be enforced — meaning the platform would pursue sale of the underlying property to recover investor principal. The 70–75% LTV cap provides a buffer, but recovery timelines and outcomes depend on real estate market conditions at the time. There is no buyback guarantee.

Can non-EU residents invest?

Letsinvest’s cross-border registrations cover EU member states including Spain, Portugal, and Estonia. Non-EU residents should check the platform’s current terms, as ECSP regulation is an EU framework and access may be restricted outside that geography.

My Opinion

Letsinvest is a platform I find genuinely interesting — and genuinely uncertain about. The regulatory credentials are real, the mortgage-first security structure is sound, and the management co-investment policy is one of the stronger alignment mechanisms I’ve seen on a platform this size. The zero-default record and consistent profitability since launch are not nothing.

But the concerns are also real. A team of four people managing a EUR 100M+ portfolio is an operational concentration risk that goes beyond what’s typical even for smaller ECSP platforms. The EUR 50,000 share capital is thin. The lack of a secondary market means your capital is genuinely locked up, and the bullet repayment structure keeps 100% of principal at risk until the very end of the loan term.

The zero-default record deserves the most honest treatment here. It reflects disciplined underwriting and favorable market conditions in roughly equal measure. Letsinvest has never had to enforce a mortgage, which means the process is untested. That will remain true until the first default happens — and on any real estate lending platform, that day will eventually come.

I would approach Letsinvest as a satellite allocation rather than a core holding. For investors already diversified across more established platforms, adding a small position here to access a regulated, mortgage-secured portfolio with genuine Baltic and Southern European deal flow makes sense. I would not make it a significant percentage of a crowdfunding portfolio until the team scales and the platform builds a longer track record through less favorable market conditions.

The potential upside — 10%+ returns, first-rank mortgage security, ECSP oversight, and a management team that puts its own money in — is real. So is the downside of a small team, thin capital, and an illiquid structure. Price it accordingly.

Disclosure: This article contains affiliate links. If you sign up through my link, I may earn a commission at no extra cost to you. I only recommend platforms I have personally researched or used. This is not financial advice.

Summary

Letsinvest is an ECSP-licensed Lithuanian real estate crowdfunding platform offering mortgage-secured property loans with returns averaging 10-10.5%. Zero defaults to date, but small team and thin capitalization are notable risks.

Pros

- ECSP licensed with Bank of Lithuania oversight

- Zero defaults to date

- First-rank mortgage security on all projects

- Management co-invests alongside retail investors

- No fees for investors

- Multi-country real estate exposure

Cons

- Very small team of approximately 4 employees

- Thin share capital of EUR 50,000

- No secondary market or auto-invest

- Bullet repayment structure locks capital until maturity

- No Trustpilot presence

Summary

Letsinvest is an ECSP-licensed Lithuanian real estate crowdfunding platform offering mortgage-secured property loans with returns averaging 10-10.5%. Zero defaults to date, but small team and thin capitalization are notable risks.

Pros

- ECSP licensed with Bank of Lithuania oversight

- Zero defaults to date

- First-rank mortgage security on all projects

- Management co-invests alongside retail investors

- No fees for investors

- Multi-country real estate exposure

Cons

- Very small team of approximately 4 employees

- Thin share capital of EUR 50,000

- No secondary market or auto-invest

- Bullet repayment structure locks capital until maturity

- No Trustpilot presence

Related

Leave a Reply