Bondora is one of the oldest peer-to-peer lending platforms, and I joined early on in my P2P lending journey, around 2016.

While this platform has been criticized by investors in the past, my portfolio has been chugging along quite well over the years, and my only complaint would be about the graphics and UI of the platform, which I find really ugly.

In this Bondora review, I’ll be sharing my results on this Estonian platform, since many of you have been asking me if you should invest in this platform and if so, how to do it.

You probably know this platform by the very distinctive cartoon characters they employ on the website. I find them a bit old-fashioned, but there’s no question that it gives Bondora a very distinctive and memorable branding.

Bondora at a Glance

| Founded | 2009 |

| Country | Estonia |

| Regulation | Licensed by Estonian Financial Supervision Authority (EFSA) |

| Main Product | Go & Grow (6% annual return) |

| Buyback Guarantee | No |

| Secondary Market | Yes (limited liquidity) |

| Auto-Invest | Yes (via Go & Grow) |

| Min. Investment | EUR 1 |

| Loan Types | Consumer loans (Estonia, Finland, Netherlands, Denmark, Latvia) |

| Profitability | 8 consecutive profitable years |

Let’s look at what makes Bondora stand out from other P2P platforms.

Bondora’s slogan is “it just takes a minute to beat your bank”, and I would say that’s true. I sometimes forget I even have an account on Bondora as it was super easy to set up since I used their Go and Grow system all along.

Other investors have had tough times with defaults and delays when using other strategies, and that seems to be the source of most of the bad comments about Bondora.

Bondora assigns a rating to its loans going all the way from AA to HR. HR stands for high risk. Those who invested in the riskier loans chasing high returns got burnt.

On the other hand, everyone seems to agree that Go and Grow has always worked just fine.

I would, therefore, recommend that you use Go and Grow if you want to add Bondora to your diversified set of peer-to-peer lending investments.

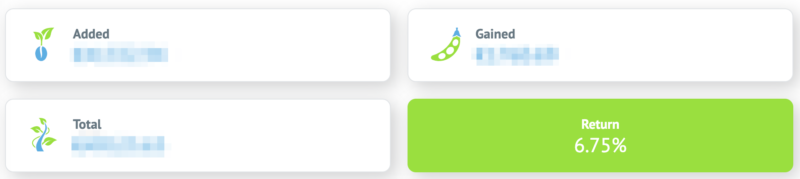

Through this method, I have been able to obtain a steady return over the years, which I’m quite happy with considering the total lack of work involved from my end. In 2025 Bondora moved Go & Grow to a flat 6% annual return with no monthly limits or earning tiers, and it remains 6% in 2026.

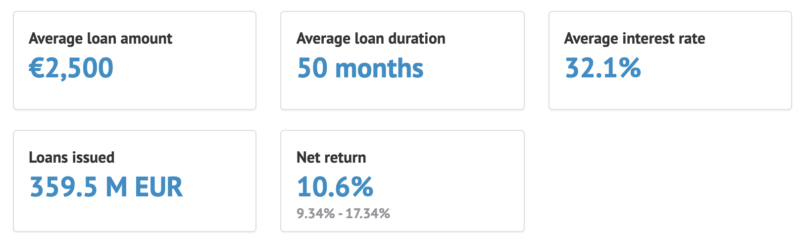

If we take a look at the latest statistics on Bondora (the platform is very transparent about all the major stats, and that’s a very positive thing), we can see that the net average return is 10.6%, but that takes into consideration investors using other ways of investing on Bondora apart from Go & Grow, so it’s expected that the average return is higher than what I managed to achieve.

Bondora is a loan originator itself, so it’s different from other platforms like Mintos, which act as aggregators of loans (and loan originators).

The secondary market is reported to be quite illiquid, although I haven’t tried it myself as I’m happy to let my money grow slowly in the Go & Grow portfolio.

Another thing to keep in mind is that there are no buyback guarantees on loans, so if a loan gets delayed, you might have to wait a long time until it is eventually recovered.

On the other hand, this is one of the oldest platforms, and the chances of it going bankrupt seem pretty slim to me, and that’s a very positive thing. You will also see that the platform has an extremely high rating on Trustpilot, which wouldn’t be the case if it were a bad platform, especially since it has been in business for so many years and had plenty of time to prove its’ worth.

How Bondora Works

Unlike most P2P platforms that act as marketplaces connecting investors with third-party loan originators, Bondora originates all its own loans. This means Bondora is both the platform and the lender: it issues consumer loans directly to borrowers in Estonia, Finland, the Netherlands, Denmark, and Latvia, and then offers portions of those loans to investors.

This single-originator model has both advantages and disadvantages. On the positive side, Bondora has complete control over its underwriting standards and loan quality. On the negative side, there is no diversification across multiple loan originators like you would get on platforms such as Mintos or PeerBerry.

Go & Grow: The Main Product

Go & Grow is Bondora’s flagship product and, in my opinion, the only way most investors should use the platform. It is essentially a managed account where Bondora handles all the loan selection and portfolio management for you.

In 2025 Bondora moved Go & Grow to a flat 6% annual return with no monthly limits or earning tiers, and it remains 6% in 2026. Your returns accrue daily, and withdrawals usually reach your bank within one to three days for a EUR 1 fee. New investors who sign up through the link below also get a €5 bonus to start. One honest caveat: Bondora keeps the contractual right to slow withdrawals if too many investors try to exit at once, which it used briefly in early 2020 and has not needed since.

The 6% rate is lower than what you can earn on most P2P lending platforms, but the trade-off is simplicity and reliability. You do not need to configure auto-invest settings, evaluate loan originators, or worry about buyback guarantees. You deposit money and it earns 6%.

The key question is whether 6% is competitive enough in the current interest rate environment. With some savings accounts and money market funds offering 2-4%, and other P2P platforms offering 10-14%, Go & Grow sits in a middle ground, better than a savings account but below what active P2P investing can yield.

Open a Go & Grow account and get a €5 bonus

Registration and Getting Started

Setting up a Bondora account takes a few minutes. You need to be at least 18, hold an EU bank account, and complete identity verification. The minimum investment is just EUR 1, making it one of the most accessible platforms for beginners.

Deposits are made via SEPA bank transfer. Once your funds arrive, you can allocate them to Go & Grow with a single click.

Regulation and Safety

Bondora is regulated by the Estonian Financial Supervision Authority (EFSA) and has been operating since 2009, making it one of the longest-running P2P platforms in Europe. The company has been profitable for 8 consecutive years, a track record that very few P2P platforms can match.

Investor funds are held in segregated accounts, meaning they are separate from Bondora’s operational funds. The company publishes regular financial reports and is transparent about its statistics.

That said, there is no buyback guarantee on loans. If borrowers default, the recovery process can take months or years. This risk is largely abstracted away by Go & Grow (you still earn 6% regardless), but it is worth understanding the underlying mechanics.

Pros

- One of the oldest P2P platforms in Europe (since 2009)

- 8 consecutive years of profitability

- Extremely simple with Go & Grow, no configuration needed

- Regulated by Estonian Financial Supervision Authority

- High Trustpilot rating with years of track record

- Low minimum investment (EUR 1)

- Daily liquidity through withdrawals

Cons

- 6% return is below what other P2P platforms offer (10-14%)

- No buyback guarantee on underlying loans

- Single loan originator, no diversification across lenders

- Secondary market has limited liquidity

- EUR 1 withdrawal fee on Go & Grow

- Portfolio Pro and other manual strategies have higher default risk

Frequently Asked Questions

Is Bondora safe?

Bondora is one of the more established P2P platforms, operating since 2009 with 8 consecutive profitable years. It is regulated by the Estonian Financial Supervision Authority. However, like all P2P investments, your capital is at risk and there is no deposit guarantee scheme.

What returns does Bondora Go & Grow offer?

As of 2025, Bondora Go & Grow offers a flat 6% annual return. It replaced the older tiered system. Returns accrue daily and you can withdraw at any time (EUR 1 fee applies).

Is Bondora better than a savings account?

At 6%, Go & Grow currently offers better returns than most European savings accounts (typically 1-3%). However, unlike a bank account, your capital is not protected by a deposit guarantee scheme, so you are taking on more risk for the higher return.

Can I lose money on Bondora?

Yes. While Go & Grow has historically paid its stated return, P2P lending carries inherent risks. If Bondora were to face severe financial difficulties, investors could potentially lose capital. The company’s 8-year profitability streak is reassuring but does not guarantee future performance.

How does Bondora compare to Mintos?

Bondora and Mintos serve different investor profiles. Bondora’s Go & Grow is simpler and more hands-off (6% return, no configuration), while Mintos offers higher potential returns (10-12%) with more control over loan selection and multiple loan originators. Mintos is better for active P2P investors; Bondora suits those wanting simplicity.

Does Bondora have a buyback guarantee?

No. Bondora does not offer a buyback guarantee on its loans. If borrowers default, Bondora pursues recovery, but there is no guaranteed timeline for getting your money back. This risk is largely abstracted by Go & Grow, where you still earn the stated return.

How Does Bondora Compare?

See how Bondora stacks up against other popular platforms:

Conclusion

Bondora’s Go & Grow is one of the simplest ways to get started with P2P lending in Europe. The 6% annual return will not set records, but the platform’s longevity, profitability track record, and ease of use make it a solid option for investors who value simplicity over maximizing returns.

I have had my money in Go & Grow for years and it has performed exactly as advertised. For investors willing to accept slightly lower returns in exchange for a completely hands-off experience, Bondora remains a reasonable choice in the P2P landscape.

Join Bondora Go & Grow and get a €5 bonus

Summary

Bondora is one of the oldest P2P platforms in Europe and Go & Grow remains its signature product u2014 simple, liquid, and now offering a flat 6% annual return. While no longer as competitive as it once was, it is a solid low-effort option for conservative P2P investors who value simplicity over maximum yield.

Pros

- Reputable platform

- Secondary market

- Various strategies can be used

Cons

- Ugly graphics

- Hard to navigate the UI in my opinion

Related

Hi do you white label your solution for p2p lending as i need to us it for start-up financing.

br

Zulfiqar

I would not recommend Bondora after being there with a total investment amount of EUR 65,000. In the beginning it looks all fine with net returns up to let’s say 15 to 20%. But over time you most likely see that you go down to around 3% (I’m at 2.79% now after 4 years). I have to be honest, in the beginning I selected manually my own loans (with very low risk) and those have been very profitable. But once you invest more and rely on re-investment of Bondora in their D, E, F, G categories, returns go down month by month. My best case scenario today is that I will get my initial investment back (EUR 29,000 to go) and seems totally unlikely for the moment. Just put your money in a bank account with zero interest, at least you don’t need to worry. Hope this helps some of you.

Hi,

Such a nice review ! I am heavily considering signing up with Bondora. Thanks for writing I had a question regarding buyback guarantees…. If there is no buyback guarantee does the company have to do anything to recover it for us ?? Or can they just let the loan be defaulted and move on

I was lured to your post by the title as I am considering investing in Bondora myself. I missed the “bad things people are saying” in the post itself. Can you elaborate?

You’re right I should have expanded on that. Will updated as soon as I have time, but the main criticisms are a high degree of loan defaults and low interest rates. But the issue with defaults is if you invest via auto invest, I haven’t had any problems with Go & Grow, although I had to settle for lower interest rates since they are safer investments. At this point I would only recommend that people invest with a Go&Grow strategy.

While I have you ‘on the line’, due to the current crisis situation, what would be your advise regarding loans on Mintos ?

1- would you put the auto-invest temporarily in pause ? Or

2- begin to withdraw some money from the platform ?

Thank you in advance 🙂

A separate post on the current situation will be published soon, hopefully I’ll have time to tidy it up and publish later today.

Yes, a communication would be great; because it is unclear to me what to do with my Mintos auto-invest 🙂 Regards,Alain

Thank you Jean ‘

About “there are no buyback guarantees on loans, so if a loan gets delayed, you might have to wait a long time until it is eventually recovered.”

Which means that if the loan is never recovered, your money is lot ?

Correct ?

That is correct.

Caramba… Very risk indeed.