“Is P2P lending safe?” is the right question to ask, and the honest answer is: it depends entirely on how you do it. I’ve invested in European P2P lending for years, through both the boom and the platform collapses, and I’ve seen people earn steady double-digit returns while others lost money on platforms that should never have been trusted with it. The difference was rarely luck. It was risk management.

This is the realistic picture: where the risks actually are, how big each one is, and exactly how I reduce them. If you want the broader primer first, start with my complete guide to P2P lending.

The Honest Answer

P2P lending sits in the middle of the risk ladder: above savings accounts and government bonds, below stocks and crypto. You’re lending real money to real borrowers through a platform, and any link in that chain can break. There is no government deposit insurance backing your investment. If a platform fails, you can lose part or all of what’s on it.

That sounds alarming, but every investment that pays more than a savings account carries risk. The point isn’t to avoid risk, it’s to understand it and get paid fairly for taking it. So let’s break down exactly what you’re exposed to.

The Real Risks of P2P Lending

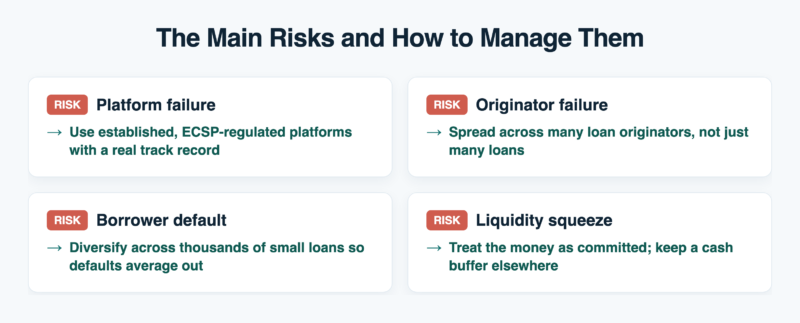

Platform and Operational Risk (the big one)

This is the risk that wipes people out. The platform itself goes bankrupt, is mismanaged, or fraudulent. When a platform collapses, recovering your money becomes slow, partial, or impossible. Almost every serious P2P loss story traces back here, not to individual borrowers. The defence is simple to state and essential to follow: only use established platforms with a real multi-year track record and proper regulation.

Loan Originator Risk

On marketplace platforms like Mintos, the loans are issued by separate companies (loan originators) and then listed for you to fund. The buyback guarantee that protects you against defaults is provided by that originator. If the originator fails, the guarantee is worthless. A buyback guarantee is only as strong as the company behind it, so spreading across multiple originators matters as much as spreading across loans.

Credit and Default Risk

The most visible risk, and usually the most manageable. Some borrowers won’t repay. On its own this would be a problem, but because you fund tiny slices of thousands of loans, defaults average out. Where a buyback guarantee applies, the originator covers the defaulted loan (assuming it’s still solvent). This is the risk diversification handles best.

Liquidity Risk

Your money is tied up in loans with set terms. Many platforms have a secondary market where you can sell loans to exit early, but in a crisis those markets dry up exactly when everyone wants out. Treat P2P money as committed, not as an emergency fund.

Currency Risk

If you invest in loans denominated in a currency other than your own, exchange-rate moves can eat into your returns. Sticking to euro-denominated loans removes this for euro-based investors.

Concentration Risk

Putting too much into one platform, one originator, one country, or one loan type concentrates your exposure. The whole safety strategy is built on spreading out, which is the opposite of concentration.

Market and Macro Risk

A recession raises defaults across the board and can strain originators and platforms simultaneously. P2P lending has yet to be tested through a truly severe, prolonged downturn, so size your allocation with that uncertainty in mind.

Ethical Considerations

Some consumer lending, particularly high-interest short-term loans, raises ethical questions about the borrowers being funded. Worth being aware of what your money is actually financing, and choosing platforms whose lending you’re comfortable with.

What Returns Do You Get for This Risk?

In 2026, net returns on the major European platforms typically run from around 9% to 13%, depending on the platform and loan type. That premium over savings and bonds is the compensation for the risks above. The key test before funding anything: does the return make sense for the risk? A rate far above the market average isn’t a bargain, it’s a warning sign, often the signature of exactly the platforms that later collapse.

How to Minimize the Risks

1. Stick to Regulated, Established Platforms

The European Crowdfunding Service Providers (ECSP) regulation brought much of the sector under a single EU licensing framework, with capital requirements, disclosure rules, and supervision. It’s not a guarantee against loss, but “is this platform ECSP-licensed or otherwise properly regulated?” is the first question I ask. Combine that with a real track record: years in operation, ideally through a downturn. My current top pick on both counts is Nectaro, which is ECSP-licensed.

2. Diversify Across Platforms, Not Just Loans

This is the single most important rule. Because platform failure is the biggest risk, spreading across several platforms matters more than holding many loans on one. If any single platform vanished tomorrow, the damage should be annoying, not ruinous. Spread across originators and countries too. The strongest options to combine are in my ranked list of the best European P2P lending platforms, with Nectaro and Afranga among my favourites.

3. Do Your Due Diligence

Before funding a platform, check who’s behind it, whether it publishes real financials and loan data, how long it’s operated, and what independent investors say about getting their money out. Transparency is a feature; vagueness is a red flag.

4. Size Your Position Sensibly

P2P should be one slice of a diversified portfolio, not the whole thing. Only invest money you can afford to lock up and, in the worst case, lose. That single rule prevents a platform failure from becoming a personal disaster.

5. Review Periodically

Check your platforms a few times a year. Watch for slowing repayments, rising defaults, withdrawal delays, or worsening transparency, the early warning signs that it’s time to stop reinvesting and start withdrawing.

So, Is It Safe?

P2P lending is safe enough to be a sensible part of an income portfolio, provided you respect the risks rather than chase the highest advertised rate. The sector has matured: regulation is tighter, the strongest platforms have genuine track records, and the failures of the past taught hard lessons. The investors who do well are the disciplined ones, diversified across solid, regulated platforms, holding some liquidity, and treating P2P as one tool among several.

If you’re comfortable with that, the next step is choosing where to invest. Start with the best European P2P lending platforms for 2026, and read why I invest in P2P lending for the case in favour. Don’t forget that interest is taxable; see how P2P lending income is taxed.

Frequently Asked Questions

Is P2P lending safe?

It carries real risk and has no deposit insurance, so it’s not as safe as a bank account. But it can be a sensible, reasonably safe part of a portfolio if you use established, regulated platforms, diversify across several of them, and only invest money you can afford to lock up. The biggest danger is platform failure, not individual borrower defaults.

What is the biggest risk in P2P lending?

Platform and loan-originator failure, by a wide margin. Individual borrower defaults are smoothed out by diversifying across many loans, but if the platform itself or the originator behind a buyback guarantee collapses, recovering your money can be slow, partial, or impossible. That’s why sticking to regulated, established platforms is the most important safety step.

Can you lose money in P2P lending?

Yes. There’s no deposit insurance, and if a platform or loan originator fails you can lose part or all of what’s invested there. You reduce this risk by diversifying across platforms, choosing regulated providers, and never investing money you can’t afford to lose.

How do I reduce the risk of P2P lending?

Use ECSP-licensed or otherwise regulated platforms with a real track record, diversify across several platforms (not just many loans on one), spread across loan originators and countries, keep P2P to a sensible slice of your overall portfolio, and review your platforms a few times a year for early warning signs.

Is P2P lending covered by deposit protection?

No. Unlike bank deposits, P2P investments are not covered by government deposit-guarantee schemes. Your capital is at risk. This is the key difference to understand before investing, and the reason diversification and platform selection matter so much.

Related

Leave a Reply