I’ve been following the European P2P lending space for years, and Maclear has been on my radar for a while as one of the more interesting newer platforms in the SME lending category. Swiss-registered, collateral-backed, focused on small and medium businesses in Eastern and Southern Europe, with returns in the 14–16% range. It stood out enough that I wanted to take a proper look.

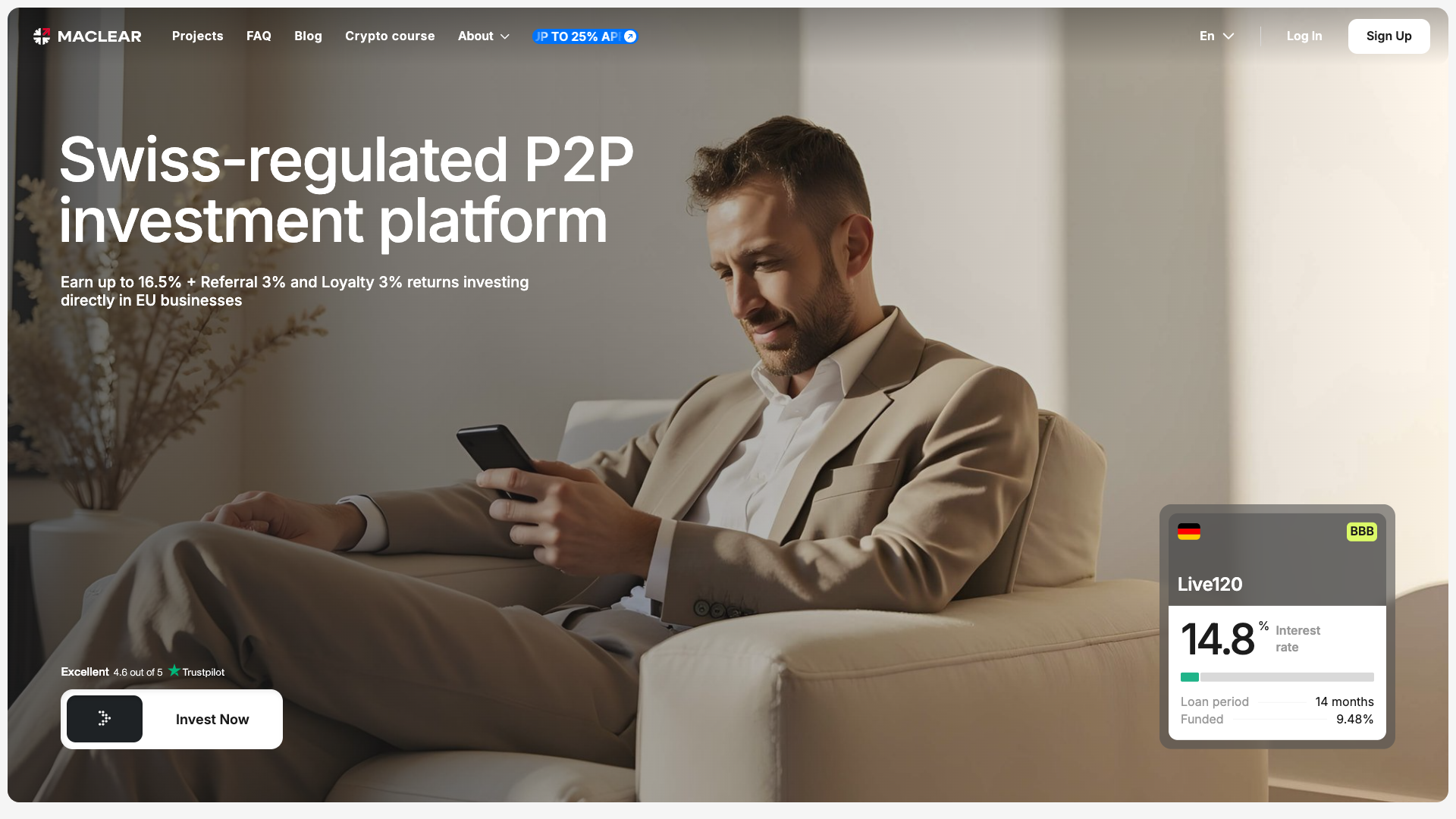

On the surface it’s a compelling proposition: Swiss-registered, collateral-backed SME lending, one default to date repaid in full, and a structural approach to investor protection that goes beyond what most P2P platforms in the space offer. The platform has grown from nothing in 2023 to over €89M funded and 32,300+ investors across 1,367 projects as of March 2026. The team responds to questions professionally. The product is clean and functional.

This review walks through what Maclear actually does, how the safety structure works, the returns and bonuses on offer, how it compares to alternatives, and who I think it’s a good fit for.

Maclear at a Glance

| Founded | Platform launched August 2023 (company acquired 2020) |

| Headquarters | Wallisellen, Zürich, Switzerland |

| Legal Framework | PolyReg SRO member (PolyReg #67438); Swiss Code of Obligations Art. 401 |

| Loan Type | SME business loans (primarily Baltic/Eastern Europe) |

| Advertised Returns | 13.5–16.5% annually; platform average 14.6% |

| Minimum Investment | €50 |

| Provision Fund | Yes (2% of each funded project, plus secondary market commissions) |

| Collateral | Yes, on all loans (collateral agent structure) |

| Secondary Market | Yes (2.5% seller fee, buyers pay nothing) |

| Auto-Invest | Yes (introduced July 2025) |

| Fees for Investors | 0% (no deposit, investment, or withdrawal fees) |

| Total Funded | €89M+ (as of March 2026) |

| Active Investors | 32,300+ |

| Projects Financed | 1,367 total (886 in 2025 alone) |

| Loan Duration | 9–16 months typical |

| Defaults | One (Vibroedil, fully recovered via collateral, July 2025) |

| Languages | English, French, German, Spanish |

The Platform: What Maclear Actually Does

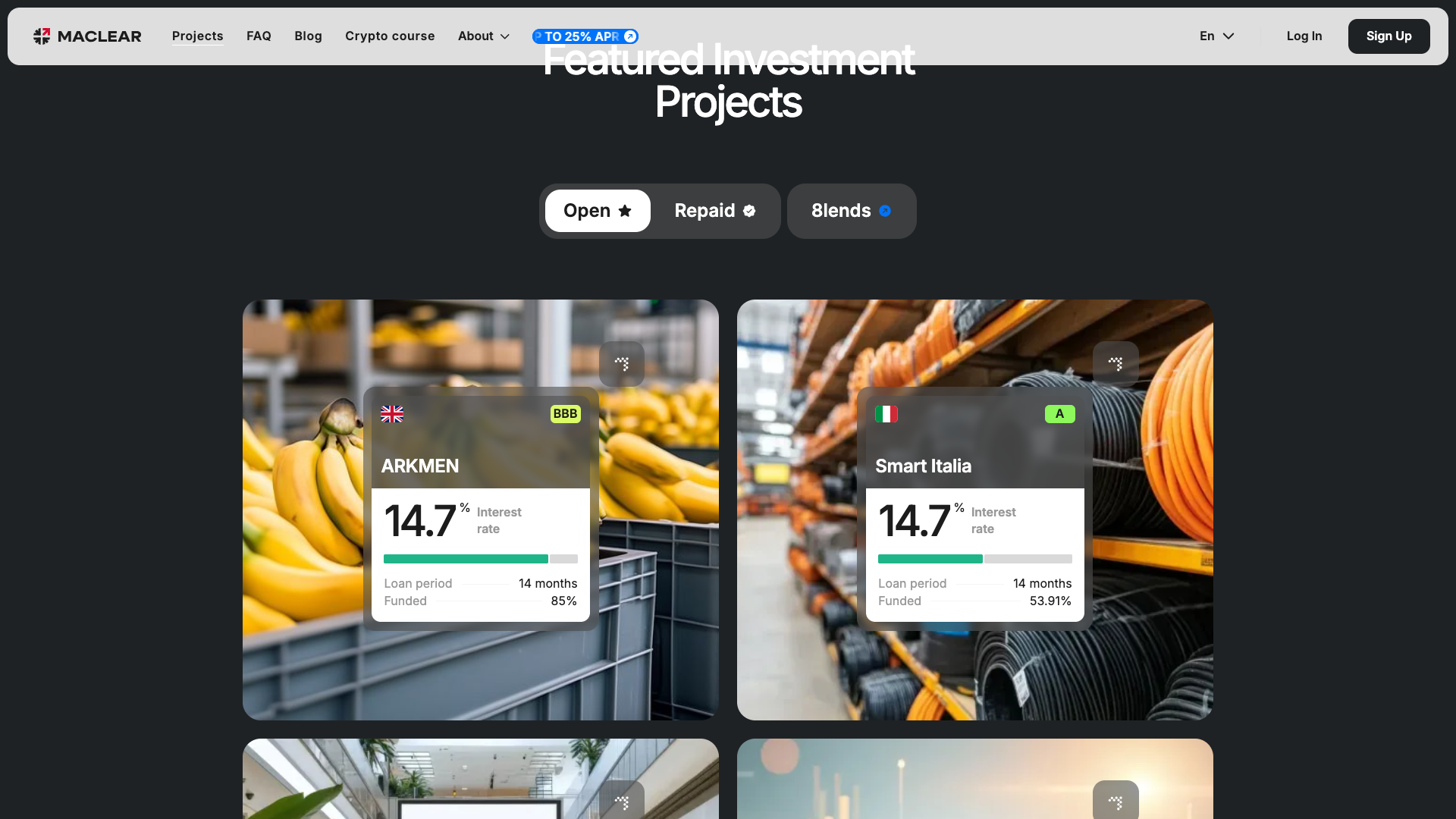

Maclear is a peer-to-business (P2B) lending platform, which means you’re lending to businesses, not consumers. Specifically, they focus on SMEs in real sectors: manufacturing, trade, logistics, construction, services. The borrowers span the Baltic states, Eastern and Southern Europe, Italy, and more recently the UAE, with an investor base now active across 72 countries.

Loan amounts typically sit in the €100,000–€500,000 range for 9–16 months. Each loan is secured by collateral (equipment, property, receivables) managed through a formal collateral agent structure, meaning a third party holds and administers the collateral on behalf of investors. Every funded project also contributes to a provision fund that acts as a buffer if a borrower runs into difficulty.

Monthly repayments of both interest and principal are standard. You’re not waiting until month 16 for a bullet repayment. You’re getting cash flow from month one, which compresses the effective duration of your exposure.

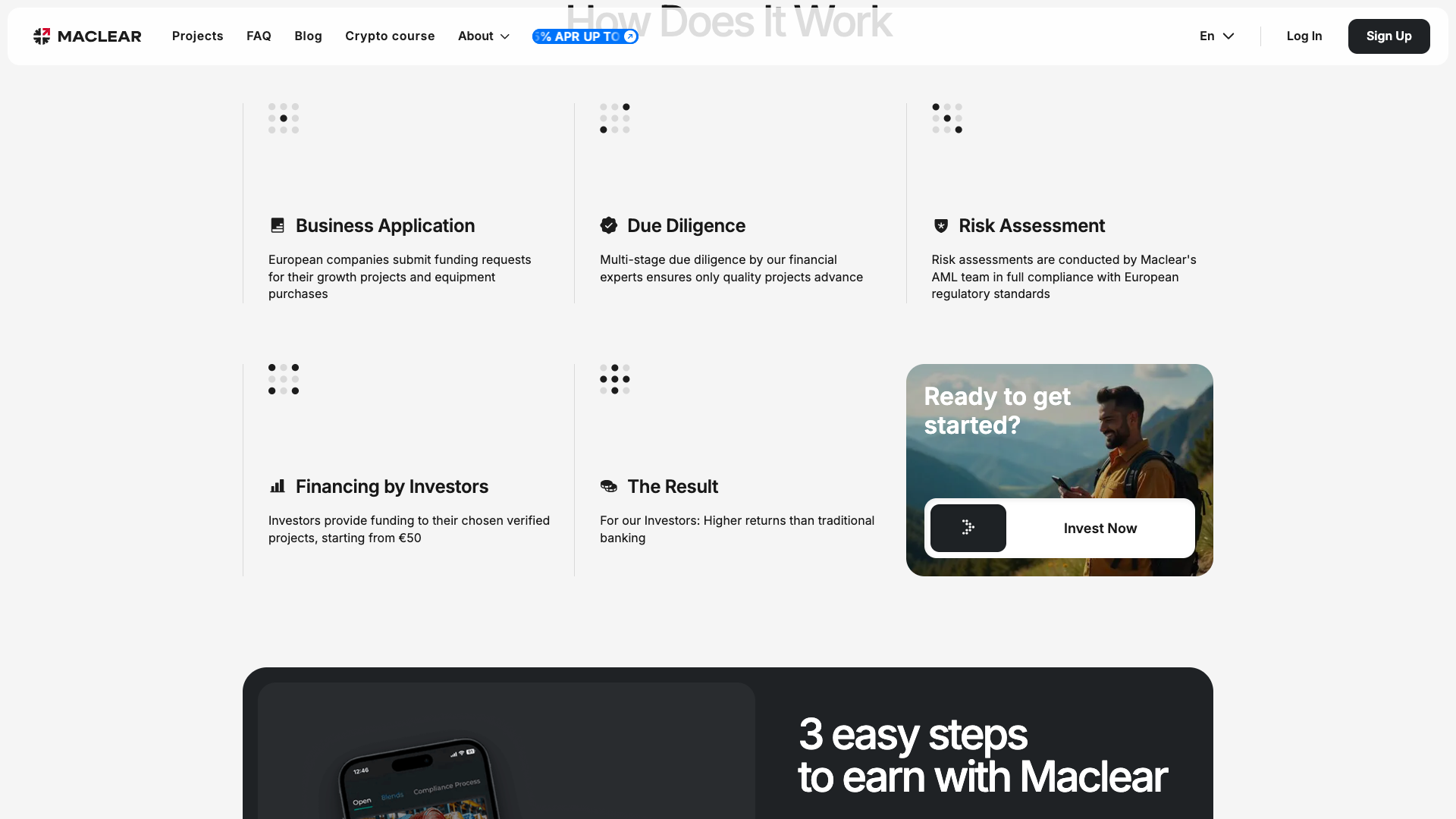

The platform uses a staged financing model. Rather than disbursing the full loan amount upfront, capital is released to borrowers in stages as operational milestones are verified. Each stage represents a separate loan fragment with its own terms. A borrower that fails to hit milestones doesn’t automatically receive the next tranche. Investors can also enter projects at different stages, which offers some flexibility in timing and exposure.

The platform is genuinely functional. Auto-invest launched in July 2025 and lets you set filters (country, return rate, loan term) and have capital deployed automatically. The secondary market allows you to list positions for sale (2.5% seller fee, buyers pay nothing), with a 30-day holding period before reselling any purchase. The interface is clean and well-designed. Registration and KYC typically takes under 15 minutes via Veriff.

The Team

Understanding who runs a P2P platform is one of the most important things you can do as an investor. In this space, the team is the single biggest variable between a platform that navigates difficulty well and one that implodes.

Denis Ustjev (CEO & Co-founder) has a background in business consulting, capital investment, and business loan management, with senior roles across Estonia, Azerbaijan, and the United States. He and Aleksandr Lang acquired Maclear AG in 2020, converting a dormant Swiss shell company from GRC software into a crowdlending platform, and launched the first campaign in August 2023.

Aleksandr Lang (CFO & Co-founder) leads financial strategy and project selection. His background is in foreign trade and industrial projects, with a professional network concentrated in Estonia, which explains the platform’s early focus on Baltic borrowers.

Alexej Martin (Director, AMLA Office) is a lawyer specialising in banking and financial markets law, and holds a concurrent role as Relationship Manager at MBaer Merchant Bank AG in Zürich. That dual role at a legitimate Swiss private bank suggests genuine Swiss market embeddedness rather than just a registration address.

Simon Brauchli (Chief Accountant) rounds out the public-facing team listed on Maclear’s site.

The team’s Estonian and Baltic operational roots explain the platform’s early focus on Baltic borrowers, with the Swiss legal framework providing the regulatory backbone for cross-border asset-backed lending across multiple jurisdictions.

Returns and the Loyalty Program

The headline return range is 13.5–16.5% annually. The platform average sits at 14.6%. Individual projects currently listed show rates between 14.7% and 15.9%, which is within that range and consistent with what you’d find on comparable SME lending platforms.

On top of base returns, there is a tiered loyalty bonus program offering up to 3% additional annual return for longer-term, higher-volume investors. The tiers are based on total amount invested over time, so the bonus compounds as your portfolio grows.

For new investors, the onboarding bonuses are aggressive: a €15 welcome bonus on your first investment, plus 3% cashback on all primary market investments during your first 90 days. There is also a running “500/30” promotion: for every €500 you invest in a single project on the primary market, the platform credits €30. That promotion can be used up to 10 times, capping out at €300. Stack the cashback and the 500/30 bonus on a €1,000 first-month investment and you are looking at an additional €90 on top of the base interest rate.

A referral program gives both parties 3% on investments made within 90 days of referral.

At the top end of the loyalty scale plus base returns, you’re theoretically looking at returns above 18%. In practice, the realistic expectation for most investors sits in the 14–16% range, depending on the projects you select and whether you qualify for any loyalty tier.

There are no fees of any kind charged to investors: no deposits, no withdrawal fees, no investment charges. Not unusual in the P2P space, where platforms earn from borrower fees and the spread between the interest rate charged to borrowers and the rate passed to investors.

Safety Structure: How Your Money Is Protected

This is where Maclear’s structure is most worth understanding in detail, because there are multiple layers, and they operate differently.

Account Segregation Under Swiss Law

Investor funds are segregated from Maclear’s operational finances under several provisions of Swiss law: Article 401 of the Swiss Code of Obligations, the Banking Act (Article 37D), the Federal Act on Intermediated Securities (FISA, Article 11A), and the Financial Market Infrastructure Act (FMIA, Article 73). In practice, this means your uninvested cash sits in a dedicated account that cannot be used for salaries, technology costs, or marketing. If Maclear became insolvent, segregated holdings would be excluded from the bankruptcy estate. You would not be an unsecured creditor of the platform. Your underlying loan receivables would remain valid claims against borrowers, recoverable independently.

This is a genuine legal protection, not a marketing claim. It’s one of the more concrete structural advantages of the Swiss domicile.

Provision Fund

2% of every funded project is transferred into a provision fund, which also receives commissions from secondary market transactions. The fund’s purpose is to cover temporary borrower difficulties, ideally stepping in before collateral enforcement becomes necessary. In the one confirmed default case to date (Vibroedil), the provision fund wasn’t actually needed because collateral recovery fully covered investor capital. The fund remains available as a first line of defence against short-term payment disruptions.

Collateral

All loans carry collateral (equipment, machinery, property, or receivables) managed through a dedicated collateral agent structure. Maclear uses independent third-party appraisers to value collateral and commissions secondary appraisals to verify the valuations. Collateral is valued at current market value rather than historical book value, which better reflects actual recovery potential in a default scenario. Importantly, in the one case where collateral enforcement was needed, it worked exactly as intended: investors were made whole.

Borrower Credit Scoring

Maclear uses a 10-tier scoring system from AAA to D, modelled on major agency frameworks. The score aggregates three components: financial risk (leverage ratios, debt/equity), qualitative risk (business quality, management quality, industry quality), and coverage and liquidity risk (debt service coverage ratio, interest coverage, current ratio). Scores update quarterly, or immediately on material changes. Loans are also put through multi-stage due diligence including legal review, AML/KYC checks, on-site visits, and financial modelling.

Regulation: PolyReg and Swiss Oversight

Maclear is a member of PolyReg Services GmbH, a Swiss self-regulatory organisation with over 25 years of experience that operates under FINMA (Swiss Financial Market Supervisory Authority) supervision. PolyReg conducts mandatory annual audits of all members, plus unannounced extraordinary inspections triggered by risk indicators.

What the audit covers in practice: fund segregation verification, borrower onboarding procedures, transaction monitoring, internal compliance structures, documentation standards, and loan metrics (LTV ratios, debt-to-equity, credit scores). This is meaningful oversight of operational quality, not a paperwork exercise. Combined with the Swiss legal framework around segregated client accounts, it forms a regulatory backbone that compares favourably to the lighter-touch oversight in some other crowdlending jurisdictions.

The Swiss structure is a deliberate choice. Maclear operates cross-border asset-backed lending across multiple jurisdictions, and Swiss law provides the operational flexibility to do that within a respected financial framework. The combination of PolyReg supervision, FINMA oversight, and Article 401 of the Swiss Code of Obligations gives investors a layered set of protections that doesn’t exist on every European P2P platform.

How to Start Investing

The process is straightforward:

- Register at maclear.ch. Basic personal details, takes about 5 minutes

- Complete KYC via Veriff. Upload an ID document and take a selfie; usually approved within 15 minutes

- Fund your account via bank transfer. SEPA transfers typically clear within 1–2 business days

- Browse available projects manually, or set up auto-invest with your preferred filters

- Receive monthly interest and principal repayments as the loan progresses

The €50 minimum per project means even modest initial deposits can be spread across several loans. There’s no withholding tax on returns at the platform level, a practical advantage over some EU-based platforms that deduct tax at source.

The Secondary Market

A secondary market has been available since the early days of the platform and is a meaningful feature. Many competing SME lending platforms don’t offer one. You can list any active investment for sale at original price or at a discount of up to 50%.

The mechanics: sellers pay a 2.5% fee on successful transactions. Buyers pay nothing. There’s a 30-day holding period after purchasing a secondary market position before you can resell it. The market is still relatively small given the platform’s size, and liquidity isn’t guaranteed. If you need to exit urgently, you may need to discount meaningfully to find a buyer.

Why Maclear Stands Out

Across the European P2P lending space, Maclear’s combination of structural protections is unusual.

The collateral structure is meaningful. Every loan has physical assets behind it, valued by independent appraisers. Most consumer P2P platforms rely on buyback guarantees backed by the loan originator’s own balance sheet, which is only as good as the originator’s solvency. Maclear’s physical collateral is a structurally different protection mechanism.

The fund segregation under Swiss law is a genuine protection. If Maclear as a company were to fail, your invested capital would not be part of the bankruptcy estate. You would still hold valid claims against borrowers, recoverable independently. That’s meaningfully better than unsecured creditor status.

The monthly repayment structure compresses duration risk. A 14-month loan returns capital from month one, which reduces your average exposure period considerably compared to bullet-repayment structures common elsewhere in P2P.

The returns are competitive for the asset class. 14–16% on collateral-backed SME lending is in line with what you’d expect from this type of exposure, and the combination with Swiss fund segregation and physical collateral is what makes the package distinctive.

Maclear publishes monthly investor updates on a reliable cadence with full deposit, investment and repayment figures. A dedicated statistics page provides sector and geographic breakdowns in real time. Regular borrower interviews add qualitative colour to the portfolio. The voluntary transparency cadence is more than many platforms at this stage of development bother with.

Pros and Cons Summary

Pros

- Collateral on every loan (physical assets, not just promises)

- Fund segregation under Swiss law (structural insolvency protection)

- Provision fund buffer (2% per project)

- Monthly interest and principal repayments (ongoing cash flow)

- Competitive 14–16% base returns

- Tiered loyalty bonus up to 3% additional per year

- Secondary market with buyer-fee-free entry

- Auto-invest tool (since July 2025)

- No fees for investors

- No withholding tax at platform level

- €50 minimum enables diversification across projects

- PolyReg AML/fund segregation compliance verified annually

- One default to date, fully recovered without provision fund use

- Multi-language platform (English, French, German, Spanish)

- Monthly investor update reports with full deposit, investment and repayment figures

- Dedicated statistics page with sector and geographic breakdowns

- Regular borrower interviews published on the blog

- Deposits processed exclusively through Narvi Bank for added security

- Investor base active across 72 countries

Cons

- Secondary market liquidity not guaranteed for urgent exits

- No mobile app yet

- Swiss registration is regulatory — founders, borrowers, and operations are Baltic

- Young platform (first campaign August 2023) with only one default tested to date

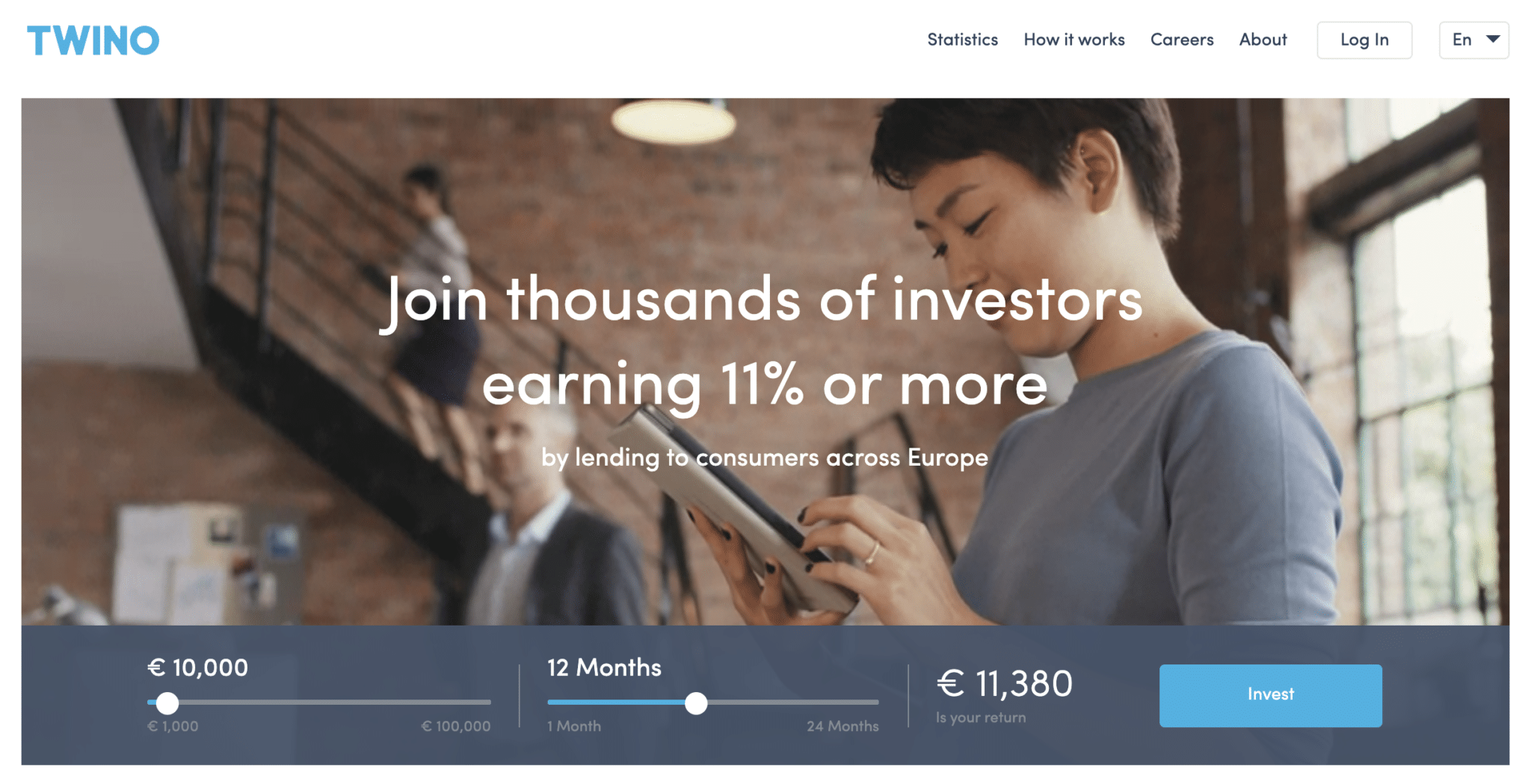

How Maclear Compares to Alternatives

If you’re looking at P2P lending as an asset class, this table puts Maclear next to two of the better-known European platforms so you can see where it sits.

| Feature | Maclear | Mintos | EstateGuru |

|---|---|---|---|

| Loan type | SME / P2B | Consumer + business via originators | Real estate (P2B) |

| Returns | 14–16% | 9–12% | 8–11% |

| Collateral model | Physical assets on every loan | Originator buyback guarantee | Real estate |

| Jurisdiction | Switzerland (PolyReg, Art. 401) | Latvia (ECSP) | Estonia (ECSP) |

| Fund segregation | Yes, under Swiss law | Yes, under EU rules | Yes, under EU rules |

| Provision fund | Yes (2% per project) | No | No |

| Minimum investment | €50 | €10 | €50 |

| Investor fees | 0% | 0% | 0% |

| Secondary market | Yes (no buyer fee, 2.5% seller fee) | Yes (0.85% buyer fee) | Yes (2% seller fee) |

| Auto-invest | Yes | Yes | Yes |

| Welcome bonus | €15 + 3% cashback (90 days) + 500/30 promo | None | 0.5% cashback |

| Repayment structure | Monthly interest + principal | Mostly monthly | Bullet at maturity |

| Borrower geography | Baltic, E. Europe, S. Europe, Italy, UAE | Global (40+ countries) | Baltic, Finland, Germany |

Maclear’s differentiator is the combination: Swiss legal protections, physical collateral on every loan rather than originator buyback guarantees, monthly cash flow, and returns at the higher end of the range. For investors who want collateral-backed SME lending specifically, that combination is hard to find elsewhere in the European P2P space.

Portfolio Diversification

Whatever your view on any single platform, no one P2P platform should dominate a portfolio. The standard rules apply: keep no more than 20–30% of your P2P allocation in any one platform, no more than 10–15% in any single loan originator or borrower, and mix loan terms so capital is freed up regularly rather than locked in for years at a time.

Maclear’s €50 minimum makes diversification easy. You can spread an initial €500–1,000 across ten projects without much friction, and the monthly repayment structure means cash starts flowing back from month one. That’s useful for compounding into new positions or reallocating across other platforms in your stack. A simple ladder strategy across loan terms (mixing 9-month and 16-month projects) gives you regular liquidity without sacrificing the higher returns that come with the longer-duration loans.

Who This Platform Is For

Maclear is a strong fit for investors who want collateral-backed SME lending in the 14–16% range and value the Swiss legal framework. Specifically, it’s worth considering if:

- You’re building a diversified P2P portfolio and want SME lending exposure with physical collateral, not originator buyback guarantees

- You prefer monthly cash flow from interest and principal payments over bullet-repayment structures

- You like the idea of fund segregation under Swiss law as a structural protection layer

- You want a platform with active auto-invest and a functioning secondary market

- You’re happy to start small (the €50 minimum makes initial diversification easy)

It may be less of a fit if you need guaranteed instant liquidity, or if you only invest through fully ECSP-licensed EU platforms.

Caveats Worth Knowing

No review is complete without an honest look at what could go wrong, and with a platform this young there are two things worth flagging before you commit capital.

Swiss domicile, Baltic operations. Maclear is Swiss-registered and the legal protections that flow from that are genuine. But the operational reality is Baltic: the founders are Estonian, the borrower pipeline is concentrated in the Baltics and Eastern Europe, and there are no Swiss borrowers or Swiss shareholders. Maclear’s own explanation is that Switzerland provides a superior legal framework for cross-border asset-backed lending while the Baltics provide the deal flow, which is a reasonable argument. But it’s fair to note the “Swiss” label here is a regulatory choice, not an operational centre of gravity. If you were picturing a Zurich-based lender with Swiss SME borrowers, that is not what this is.

Young platform, limited track record. The first campaign launched in August 2023, which makes the platform roughly two and a half years old. Over that period it has scaled to €89M+ funded with exactly one default, which was recovered in full through collateral enforcement. That is a good outcome, but one recovered default is not a tested track record. The real pressure test for any SME lending platform is a recession, a wave of borrower defaults, or a sector-wide shock where multiple collateral enforcements have to happen in parallel. Maclear has not seen that yet, and neither has its credit scoring model. The structural protections look well-designed on paper, but “well-designed on paper” and “battle-tested” are different things.

Neither of these is a reason to avoid the platform. They are reasons to size your position accordingly.

The Bottom Line

Maclear is one of the more structurally interesting P2P platforms to emerge in the European market in the last few years. The Swiss fund segregation, the physical collateral on every loan, the provision fund buffer, the monthly repayment cadence, and the active secondary market are all real and well-constructed. The one default case to date (Vibroedil) ended with full investor recovery through collateral enforcement, which is exactly what the structure is designed to do.

The platform is growing fast: €89M+ funded, 32,300+ investors, 1,367 projects, and a consistent monthly reporting cadence that’s better than many competitors at this stage of development. The combination of returns at 14–16%, structural protections, and aggressive new-investor bonuses (€15 welcome + 3% cashback in the first 90 days + the 500/30 promotion) makes the first-year returns notably attractive.

If you’re looking to add asset-backed SME lending to a diversified P2P portfolio, Maclear is worth a closer look. You can visit Maclear directly to sign up, complete the quick KYC, and start exploring current projects.

This article is not individual investment advice. All investments carry risk of capital loss, and P2P/P2B lending is no exception. Make your own decisions based on your own research and risk tolerance.

Summary

Maclear is a Swiss-registered P2B lending platform offering 13.5u201316.5% returns on asset-backed SME loans, primarily to Baltic and Eastern European borrowers. The legal structure, segregated accounts, and annual audits are real safeguards, but the platform is young, the 2024 audit is delayed, and the Swiss label is regulatory rather than operational. A reasonable small allocation for experienced P2P investors, not a starter platform.

Pros

- Swiss-registered with segregated client accounts under Swiss law

- Independent annual audit (2022 and 2023 published)

- Base returns of 13.5-16.5% plus up to 3% loyalty bonus

- Asset-backed loans with collateral (mortgages, pledges, guarantees)

- Zero investor fees - no deposit, withdrawal, or investment charges

- Stackable new-investor bonuses (welcome + cashback + 500/30 promo)

- Multi-language platform with investors across 72 countries

Cons

- 2024 audit not yet published (delayed; committed for Q1 2026)

- Swiss registration is regulatory - founders, borrowers, and operations are Baltic

- Young platform - first campaign launched in August 2023

- Borrower concentration in Baltic and Eastern European SMEs

Related

Leave a Reply