Mintos and PeerBerry are the two largest peer-to-peer lending platforms in Europe, and if you’re getting started with P2P investing, you’ve probably narrowed it down to one of these two. I’ve been investing on both for years — over EUR 150,000 on Mintos since 2017 and a smaller but meaningful allocation on PeerBerry.

They’re both solid platforms, but they take fundamentally different approaches. Mintos is the feature-rich marketplace with 60+ loan originators, a secondary market, and now even bonds and ETFs. PeerBerry is the lean, focused alternative with fewer originators, higher concentration, and a loyalty program that rewards bigger investors.

The short version: Mintos wins on diversification, regulation, and features. PeerBerry wins on simplicity, zero fees, and its loyalty program. Most experienced investors use both — and that’s probably the right call.

Quick Comparison: Mintos vs PeerBerry

| Feature | Mintos | PeerBerry |

|---|---|---|

| Founded | 2015 | 2017 |

| Country | Latvia | Latvia |

| Regulation | MiFID II licensed (pursuing banking license) | Not regulated (Lithuanian licensing) |

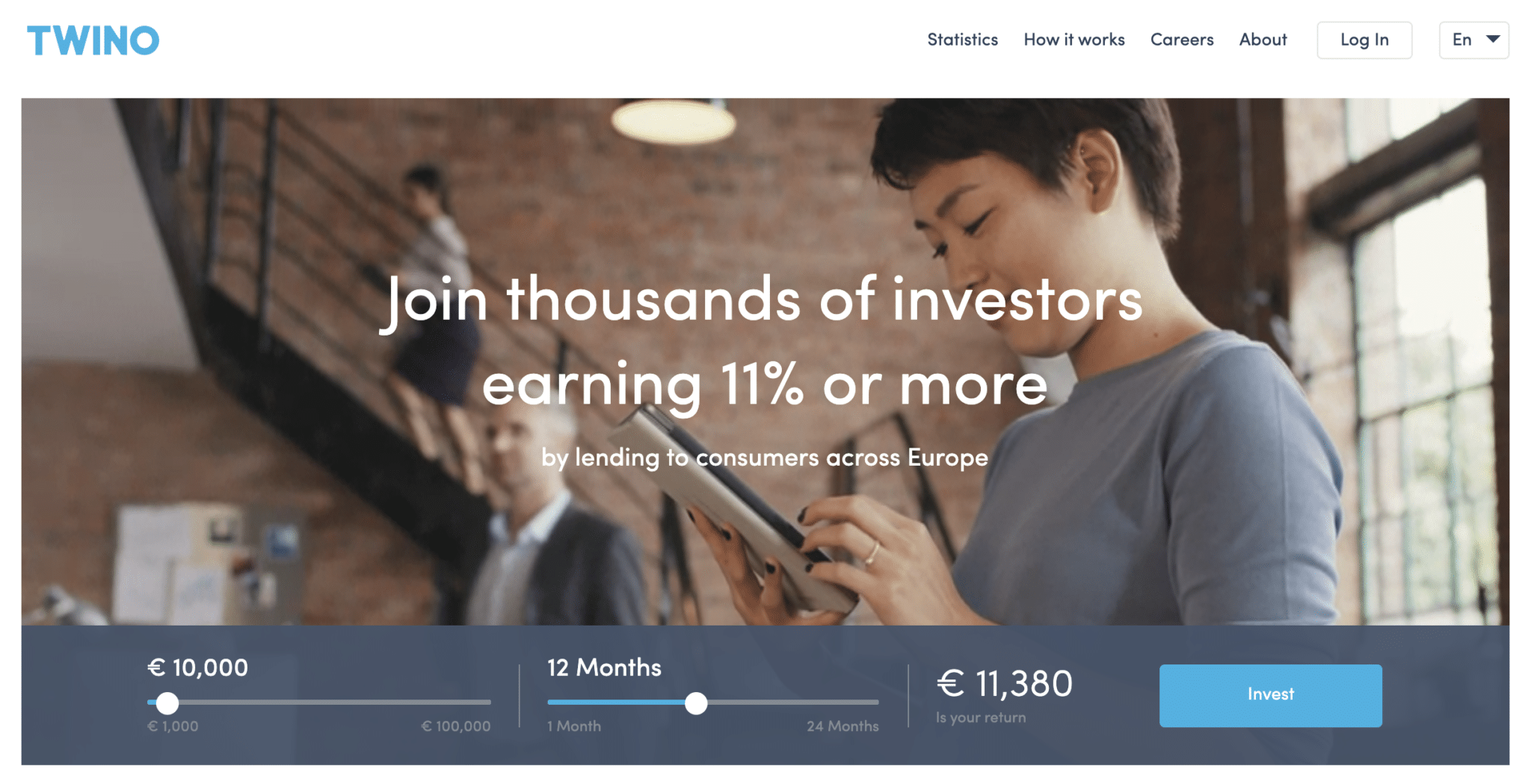

| Avg. Returns | ~12% | ~11% (up to 12% with loyalty bonus) |

| Buyback Guarantee | Yes (60 days) | Yes (60 days) |

| Secondary Market | Yes (0.85% fee) | No |

| Auto-Invest | Yes (Custom + Core Loans) | Yes |

| Min. Investment | EUR 10 | EUR 10 |

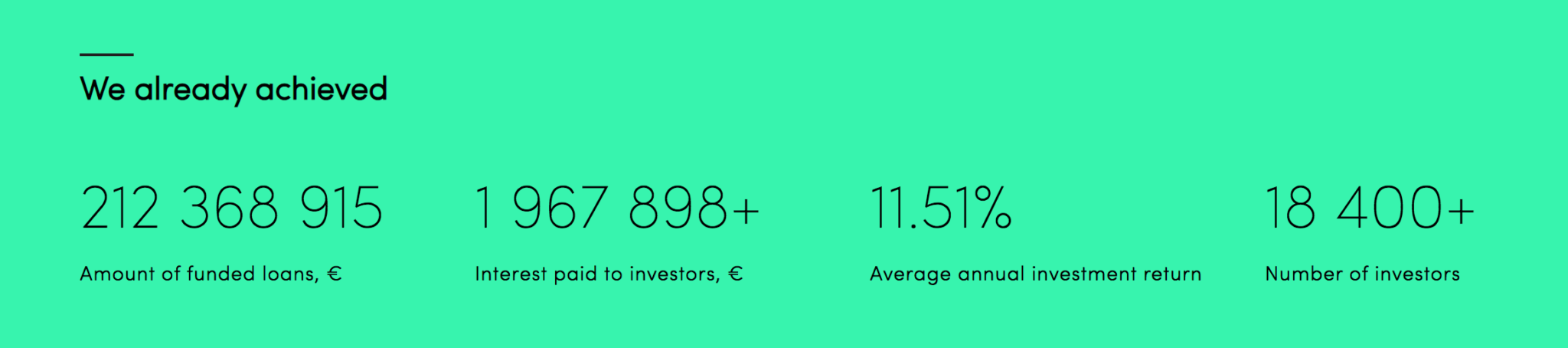

| Total Funded | EUR 12 billion+ | EUR 3.24 billion+ |

| Registered Investors | 700,000+ | 110,000+ |

| Loan Originators | 60+ | 12 |

| Countries | 33+ | 8 |

| Fees | 0.29% annual (Custom Portfolios), 0.85% secondary market | None |

| Loyalty Program | No | Yes (+0.5% to +1% based on portfolio size) |

| Additional Assets | Bonds, ETFs, Real Estate | Loans only |

Returns and Performance

On paper, Mintos advertises higher average returns at ~12% compared to PeerBerry’s ~11%. In practice, the gap is narrower than it looks.

My personal experience on Mintos over 9 years has averaged around 9% net annually. That accounts for the good years (11-12% in the early days), the rough patches during COVID and the Russian originator defaults in 2022, and the recovery since. It’s a realistic number for a diversified long-term investor.

PeerBerry’s returns have been more consistent, partly because the platform weathered the same crises with fewer originator failures. Add in PeerBerry’s loyalty program — which gives you up to an extra 1% if you invest EUR 40,000+ — and the effective returns can match or even exceed Mintos for larger investors.

The key difference is volatility. Mintos gives you higher upside but also more variance. PeerBerry is steadier. If you’re optimizing for peace of mind, PeerBerry has the edge. If you’re comfortable with some turbulence for higher potential returns and broader diversification, Mintos is the better bet.

Regulation and Safety

This is where Mintos pulls clearly ahead. Mintos obtained its investment firm license in 2021 and now operates under the MiFID II framework — the same regulatory standard that governs banks and brokerages in Europe. This comes with an EUR 20,000 investor protection scheme and means investment products on the platform are structured as regulated Notes under EU securities law.

In February 2026, Mintos announced it’s pursuing a full banking license in Latvia, which would be a transformative step — allowing deposit accounts and potentially other banking services alongside investments.

PeerBerry, by contrast, is not regulated under MiFID II or ECSP. It operates under Lithuanian licensing, which provides some oversight but significantly less investor protection than Mintos’s regulatory framework. There’s no investor compensation scheme if something goes wrong at the platform level.

Both platforms have buyback guarantees (60-day default triggers), but regulation matters for the “what if the platform itself has problems” scenario. Mintos is meaningfully safer on this dimension.

That said, PeerBerry’s main loan originators — Aventus Group (80% of loans) and Gofingo (15%) — are both profitable, audited companies. The platform has operated without major incidents since 2017. No regulation doesn’t mean unsafe — it means less protection if things go wrong.

Diversification

Mintos is in a completely different league when it comes to diversification. Over 60 loan originators across 33+ countries, spanning mortgage loans, car loans, business loans, short-term consumer loans, agricultural loans, and even BNPL products. No other European P2P platform comes close to this breadth.

PeerBerry has 12 loan originators across 8 countries, with Aventus Group accounting for 80% of all loans. This concentration is PeerBerry’s biggest structural risk — if Aventus runs into trouble, the platform’s entire loan supply is affected.

For investors who want to spread their risk as widely as possible, Mintos is the clear choice. For investors who are comfortable with a more concentrated bet on a proven lending group, PeerBerry’s simplicity can be appealing.

Beyond loans, Mintos now also offers fractional bonds, ETFs, and real estate investments, making it increasingly a multi-asset platform rather than just a P2P marketplace. PeerBerry remains a pure P2P lending platform.

Ease of Use and Features

PeerBerry’s biggest advantage is its simplicity. The platform is clean, fast, and easy to navigate. Set up auto-invest, deposit money, and you’re done. There’s no secondary market to manage, no complex settings to optimize, and the loan types are straightforward. For a hands-off investor, PeerBerry requires almost zero maintenance.

Mintos is more powerful but also more complex. The Custom Strategy builder has many parameters to configure, and optimizing your portfolio across 60+ loan originators requires some research. However, Mintos also offers Core Loans — a fully managed auto-invest option that handles everything for you, similar to PeerBerry’s simplicity.

The secondary market is a major feature advantage for Mintos. If you need to exit early, you can sell your loans (for a 0.85% fee). On PeerBerry, you’re locked in until maturity. Given that PeerBerry’s loans are mostly short-term (30-day maturities), the lack of a secondary market is less of an issue than it would be on a platform with longer loan terms — but it’s still a meaningful difference for larger portfolios.

Both platforms offer auto-invest, and both work well. Mintos provides more granular control; PeerBerry keeps it simple.

Fees

PeerBerry wins this category cleanly. The platform charges zero fees — no investment fees, no withdrawal fees, no management fees. Combined with the loyalty program (which adds 0.5-1% to your returns), PeerBerry is one of the most cost-effective P2P platforms in Europe.

Mintos has introduced fees over the past two years. Since May 2025, there’s a 0.29% annual fee on Custom Loan Portfolios. The High-Yield Bonds Portfolio carries a 0.39% annual management fee. And the secondary market charges 0.85% per transaction.

These fees are reasonable compared to traditional investment products, but they eat into your returns. On a EUR 50,000 portfolio at 12% returns, the 0.29% annual fee costs you EUR 145/year. Over time, this adds up — especially when PeerBerry charges nothing.

Who Should Choose Which?

Choose Mintos if you:

- Want maximum diversification across countries, loan types, and originators

- Value regulation and investor protection (MiFID II, EUR 20,000 scheme)

- Need liquidity (secondary market)

- Want to invest in more than just loans (bonds, ETFs, real estate)

- Are building a large P2P portfolio (EUR 50,000+) and want to spread risk widely

Choose PeerBerry if you:

- Prefer simplicity and a hands-off approach

- Want zero fees and a loyalty program that rewards larger investments

- Are comfortable with higher concentration (Aventus Group)

- Primarily invest in short-term loans (30-day maturities)

- Are starting out with P2P lending and want an easy entry point

Use both if: You have a P2P allocation of EUR 20,000+ and want to diversify across platforms. This is what I do, and I’d recommend it to most experienced P2P investors. The two platforms complement each other well — Mintos for broad diversification and PeerBerry for steady, fee-free returns on short-term loans.

Verdict

If I had to pick just one platform, I’d choose Mintos. The MiFID II regulation, secondary market, unmatched diversification, and multi-asset capabilities give it a clear structural advantage. It’s the most complete P2P investment platform in Europe and the one I trust most for larger sums.

But PeerBerry earns its place in a diversified P2P portfolio. Zero fees, consistent returns, the loyalty program, and the simplicity of the platform make it an excellent complement to Mintos. The Aventus Group concentration is a real risk, but the group’s profitability and track record are reassuring.

For a deeper look at each platform, read my full Mintos Review and PeerBerry Review.

Frequently Asked Questions

Is Mintos safer than PeerBerry?

From a regulatory perspective, yes. Mintos is MiFID II licensed with an EUR 20,000 investor protection scheme, while PeerBerry operates without equivalent regulation. However, PeerBerry’s main loan originators (Aventus Group and Gofingo) are profitable, audited companies with a clean track record since 2017. Both platforms offer buyback guarantees on loans.

Which platform has better returns — Mintos or PeerBerry?

Mintos advertises ~12% average returns, while PeerBerry offers ~11%. However, PeerBerry’s loyalty program adds up to 1% for larger investors (EUR 40,000+), closing the gap. My personal net returns on Mintos over 9 years have averaged around 9% after accounting for originator defaults. PeerBerry’s returns have been more consistent with fewer incidents.

Can I use both Mintos and PeerBerry?

Yes, and many experienced P2P investors do exactly that. The platforms complement each other well — Mintos for diversification and liquidity, PeerBerry for simplicity and fee-free returns. Using both also provides platform-level diversification, which is important in P2P investing.

Do Mintos and PeerBerry charge fees?

PeerBerry charges zero fees. Mintos charges 0.29% annually on Custom Loan Portfolios and 0.85% on secondary market transactions. The High-Yield Bonds Portfolio has a 0.39% annual management fee. While Mintos’s fees are reasonable for the features provided, PeerBerry has a clear cost advantage.

Which platform is better for beginners?

PeerBerry is the easier entry point due to its simpler interface and lack of complex settings. However, Mintos’s Core Loans product offers a similarly hands-off experience with better diversification. Either platform works well for beginners investing EUR 1,000-5,000 to learn the ropes.

Does PeerBerry have a secondary market?

No. PeerBerry does not offer a secondary market, which means you cannot sell your loans before maturity. Since most PeerBerry loans have 30-day maturities, this is less of an issue than on platforms with longer loan terms. If liquidity is a priority, Mintos’s secondary market is a significant advantage.

Open a Mintos account Open a PeerBerry account

Related

Leave a Reply