Peer-to-peer lending creates a marketplace that offers both parties what they seek. Borrowers can sidestep the hassle of traditional banks and often secure more competitive interest rates. Investors, in turn, get access to yields that leave savings accounts and fixed-rate bonds in the dust.

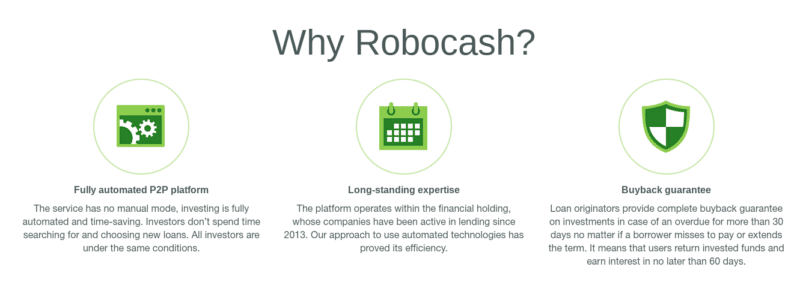

Robocash is one such provider that caught my eye. Launched in 2017, it offers a fully automated platform that follows the core principles of the peer-to-portfolio model. Investors fund loans facilitated by the UnaFinancial Group — the holding company behind Robocash.

In this review, I explore how Robocash works, what loans you are investing in, how much you should expect to make, and what risks to weigh carefully.

Robocash at a Glance

| Founded | 2017 |

| Country | Croatia |

| Regulation | Not ECSP regulated |

| Average Returns | 8-13% annually |

| Buyback Guarantee | Yes (30 days) |

| Secondary Market | Yes (no fees) |

| Auto-Invest | Yes (fully automated) |

| Min. Investment | EUR 10 |

| Loan Types | Consumer loans (short-term and long-term) |

| Parent Company | UnaFinancial Group |

| Total Funded | EUR 1.3 billion+ |

| Registered Investors | 42,000+ |

What is Robocash?

Robocash is the P2P investing arm of UnaFinancial Group, a fintech holding company that operates consumer lending subsidiaries across several Asian and European markets. The platform focuses on providing automated investment solutions and making cross-border lending accessible to retail investors.

The peer-to-peer lending process sits at the core of the offering. It primarily targets European investors, requiring a European bank account for deposits and withdrawals.

As an auto-invest platform, it eliminates the need to manually pick loans. You specify how you want your funds allocated and Robocash handles the rest.

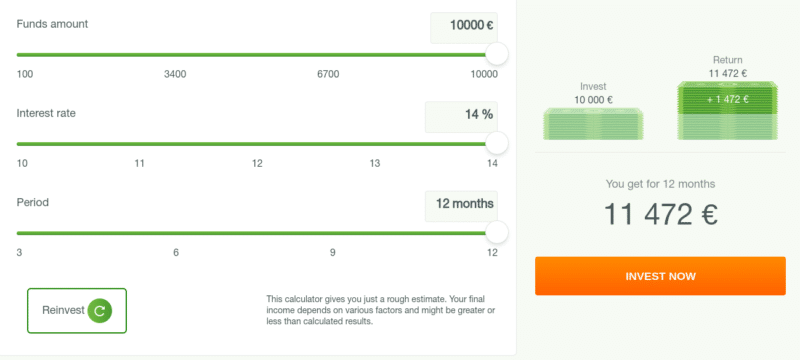

Current interest rates on the platform run between 8% and 12% annually. The historical average return sits at around 9.93% according to the platform’s own statistics. Those are meaningfully higher yields than you will get from a savings account, but they come with corresponding risk — which I cover below.

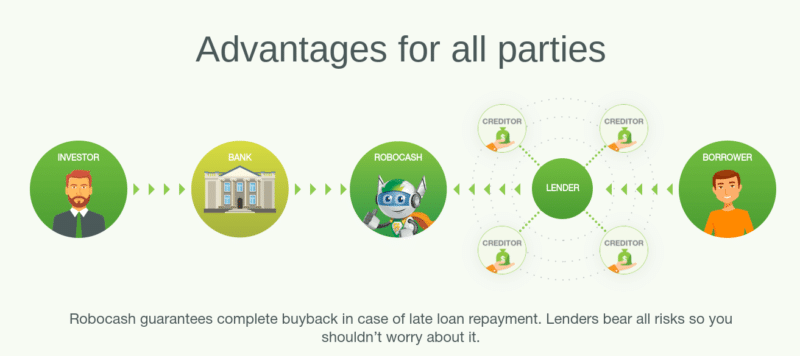

The platform also offers a 100% Buyback Guarantee. If a borrower is more than 30 days late on repayment, the relevant subsidiary repurchases the loan — principal and accrued interest included. That protection is only as solid as the financial health of the originator behind it.

Who Can Use Robocash?

Robocash accepts investors who are at least 18 years old and resident in Europe (EU, UK, or Switzerland). You also need a European bank account to handle deposits and withdrawals.

Both individuals and legal entities can invest. Companies need to supply a certificate of incorporation and the credentials of their representative.

Note that Robocash is not currently regulated under the EU’s European Crowdfunding Service Provider (ECSP) framework. The platform operates from Croatia and does not hold a formal investment services license. That is a meaningful distinction compared to more heavily regulated alternatives — something to factor into your risk assessment.

How Does Robocash Work?

Because Robocash is fully automated, you do not hand-pick individual loans. Here is how the process works:

- You deposit funds into your Robocash account and create a portfolio based on your chosen criteria.

- Borrowers apply for loans through UnaFinancial’s lending subsidiaries in their respective countries. Each application goes through a credit assessment process.

- Approved loans are assembled via the Robocash marketplace.

- Robocash automatically allocates your capital to loans matching your portfolio settings.

How to Get Started With Robocash

Robocash does not lend to borrowers directly — it acts as the marketplace layer between investors and UnaFinancial’s lending subsidiaries. Here is a quick walkthrough of signing up as an investor.

Step 1: Create Your Account

Registration is straightforward. Fill out the sign-up form with your personal details and submit a passport or national ID to satisfy KYC requirements. Account verification typically completes within a few hours.

Step 2: Add Funds to Your Account

Robocash currently supports bank transfers only — no debit card deposits. The minimum investment amount is €10. Monthly deposit limits apply (€15,000 per month / €180,000 per year).

Once credited, your funds are split between a personal balance and an investment balance. You move money from personal to investment balance when setting up a portfolio.

Step 3: Create Your Portfolio

This is where you define the parameters Robocash uses to allocate your capital automatically.

The available settings include:

- Portfolio size

- Minimum and maximum per single loan

- Minimum and maximum interest rate

- Repayment period (up to 367 days)

- Investment strategy

- Choice of lenders

If you prefer a hands-off approach, the “Maximise Profit” option lets Robocash configure the portfolio to target higher returns automatically.

Note: If a loan is repaid earlier than its stated term, you earn interest only for the actual repayment period — not the full original term.

Investment Strategies

You have four options for how Robocash handles your principal and interest:

- Balance: withdraws returns to your investor funds within the platform

- Payout: automatically transfers both principal and interest directly to your bank account (minimum portfolio balance of €50 required)

- Reinvest principal + interest: compounds both back into new loans

- Reinvest principal only: reinvests capital while paying out interest

Loyalty Bonuses

Robocash runs a loyalty program that adds a rate bonus on top of your base return, depending on your total portfolio size. The bonus tiers increase as your invested balance grows, giving larger investors a modest edge on returns.

Selecting the Lenders

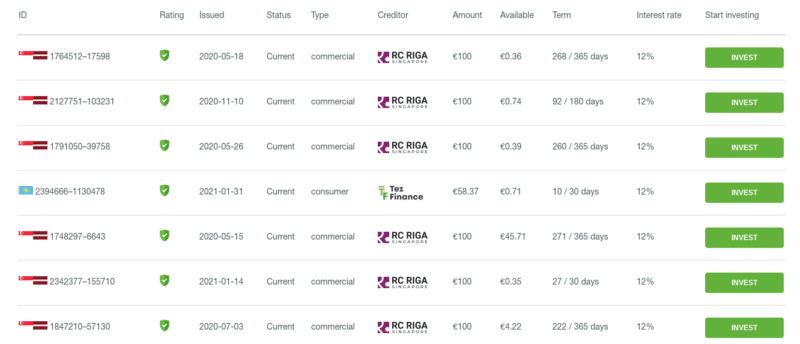

While you cannot choose individual borrowers, you can select which UnaFinancial lending subsidiaries to include in your portfolio. All loans on the platform originate from within the UnaFinancial Group across five countries: Philippines, Kazakhstan, Sri Lanka, Singapore, and Spain.

Once you lock in your criteria, the platform shows you how many matching loans are currently available and projects your expected 12-month earnings under that strategy. You can also create separate portfolios for individual lenders if you want to track performance by originator.

Loan Types

Robocash facilitates two categories of loans:

- Short-term loans: seven to 30 days, smaller ticket sizes

- Long-term loans: one to 12 months, larger amounts, typically issued on an installment basis

Secondary Market

Robocash has a secondary market that lets you sell funded loans before they mature. Unlike some competing platforms, the secondary market here carries no fees, and liquidity is typically available within 24 hours. This gives you a meaningful exit option without having to wait out the full loan term.

Note that the secondary market on Robocash does not support discounted selling — you cannot offload loans below face value to attract buyers faster. What you get is par value plus earned interest.

Once your portfolio is running, you can download individual assignment agreements for each loan, access the full loan book, and generate charts to visualize how your capital is distributed.

Robocash Safety and Risk Management

Safety in P2P investing always comes down to two questions: how transparent is the platform, and how financially solid is the entity behind the loans?

On transparency, Robocash scores reasonably well. UnaFinancial Group publishes audited annual financial reports (audited by Grant Thornton to IFRS standards), and the platform provides individual financial reports for each loan.

On the numbers: as of early 2026, over 42,000 investors have funded more than €1.3 billion in loans through the platform since launch, with investors collectively earning over €38 million in interest.

The Buyback Guarantee has been honored without exception to date. If repayment is delayed by more than 30 days, the originator is obligated to repurchase the loan — covering both principal and any interest accrued.

That said, a few risk factors are worth flagging clearly:

Single-originator concentration. Every loan on the platform comes from UnaFinancial’s own subsidiaries. There is no third-party originator diversification. If UnaFinancial runs into financial difficulty, the Buyback Guarantee and your invested capital are directly exposed.

UnaFinancial Group guarantee. In April 2026, Robocash’s investor relations team provided an on-record clarification of how the Group-level guarantee functions. Investments on the platform are structured as direct assignment agreements between the investor and a specific UnaFinancial loan originator, which means the underlying claims remain legally binding even if Robocash itself were to cease operating. If a loan originator becomes insolvent, UnaFinancial states that it steps in to settle liabilities and facilitate continued repayment before any formal bankruptcy process is triggered. The group cites five supporting layers: 100% direct ownership of every originator, active liquidity management at the holding level, IFRS-audited group financials, a track record of transferring liabilities between originators when one ceases operations, and the 30-day direct Buyback Guarantee at the originator level. This is useful context, but it is important to note that this is a group-level operational commitment rather than a legally enforceable third-party guarantee to individual investors. Its practical value depends on UnaFinancial’s own solvency, which is precisely what the 2024 equity decline and 25:1 leverage ratio have put in question. I will revisit this assessment once the 2025 financial statements are public.

UnaFinancial’s 2024 financials. The 2024 annual report showed some pressure: operating net interest income declined and credit loss provisions increased significantly, though the group remained profitable. Currency translation losses also weighed on comprehensive income. Worth monitoring.

No ECSP regulation. Robocash is not regulated under the EU Crowdfunding Regulation framework. That means there is no investor protection scheme and no regulatory oversight equivalent to what licensed platforms offer.

None of this makes Robocash a bad choice — but it does mean you should size your position accordingly and not treat the Buyback Guarantee as a risk-free guarantee.

Robocash Fees

Robocash charges no fees to investors. The platform covers payment processing and account maintenance costs. Check with your bank separately to understand whether any charges apply on wire transfers in or out of your account.

Robocash Customer Support

You can reach the customer support team by email or phone. Support hours run from 7 am to 3 pm UTC. Email response times can be slow — Robocash quotes up to 72 hours, which is not ideal if you have a time-sensitive issue.

Robocash Pros

- Simple, clean interface that requires no prior investing experience

- Fully automated — set your criteria and let the platform work

- Buyback Guarantee with a strong track record of being honored

- Geographical diversification across five lending markets (Philippines, Kazakhstan, Sri Lanka, Singapore, Spain)

- Secondary market with zero fees and fast liquidity

- Low minimum investment (€10)

- Audited annual financial reports from UnaFinancial Group

Robocash Cons

- All loans originate from UnaFinancial’s own subsidiaries — there is no third-party originator diversification, which concentrates platform risk

- Not regulated under the EU’s ECSP framework — no equivalent investor protections

- Bank transfer deposits only — no card payment option

- Customer support response times can stretch up to 72 hours

- Secondary market does not allow discounted sales, limiting your ability to exit quickly in stressed conditions

Who Should Invest in Robocash?

Robocash is a straightforward, passive platform. You do not research individual loans, pick borrowers, or manage a portfolio actively. That simplicity is its strongest selling point.

It is best suited to investors who want P2P exposure without operational complexity — specifically those comfortable accepting single-originator concentration risk in exchange for a hands-off experience. The €10 entry point makes it easy to start small and build familiarity with the asset class before committing larger sums.

More experienced P2P investors who want originator diversification or regulated platform options will likely look elsewhere.

Frequently Asked Questions

Is Robocash safe?

Robocash has a meaningful track record with over EUR 1.3 billion funded and 42,000+ investors. The Buyback Guarantee has been honored without exception. However, the platform is not ECSP regulated and all loans come from a single group (UnaFinancial), which concentrates risk. UnaFinancial publishes IFRS-audited financial reports (audited by Grant Thornton).

What returns can I earn on Robocash?

Current interest rates range between 8% and 13% annually, with the historical average around 9.93%. Loyalty bonuses can push returns higher for larger portfolios.

Is Robocash regulated?

No, Robocash is not regulated under the EU’s European Crowdfunding Service Provider (ECSP) framework. The platform operates from Croatia without a formal investment services license. This means there is no investor protection scheme comparable to regulated platforms.

Does Robocash charge any fees?

Robocash charges no fees to investors. There are no account fees, no investment fees, and no secondary market fees. Your bank may charge for incoming or outgoing wire transfers.

How does Robocash compare to PeerBerry?

PeerBerry is significantly larger (EUR 3.24B funded vs EUR 1.3B) and works with multiple loan originator groups, while Robocash is a single-originator platform. Robocash is fully automated with no manual loan picking, while PeerBerry offers both manual and auto-invest options. PeerBerry lacks a secondary market; Robocash has one with zero fees.

Can I withdraw my money from Robocash at any time?

You can sell loans on the secondary market for immediate liquidity (typically within 24 hours). Otherwise, you receive funds as loans mature. The Payout strategy automatically transfers returns to your bank account.

How Does Robocash Compare?

See how Robocash stacks up against other popular platforms:

Robocash Review — My Verdict

Robocash has come a long way since its 2017 launch. The platform has facilitated over €1.3 billion in loans and paid out more than €38 million to investors — that is a meaningful track record for a platform in this space.

Returns have settled into the 8–12% range, with the average sitting closer to 10%. That is competitive, if somewhat lower than the headline 14% figures that were floated in earlier years. Add in the loyalty bonuses for larger portfolios, and active investors can push returns toward the top of that range.

The main caveats are clear: single-originator concentration, no ECSP regulation, and some financial pressure visible in UnaFinancial’s 2024 numbers. None of those are dealbreakers, but they do mean Robocash works best as one component of a diversified investment strategy — not as your only P2P platform.

If you are new to P2P lending and want a simple, automated entry point, Robocash is a reasonable place to start.

Summary

With a solid 10-14% return on offer, the site allows you to grow your money at a much faster rate than you will get at more traditional investment platforms.u00a0

Pros

- Many years of successful operation

- Survived some significant issues, suggesting great leadership

Cons

- Other platforms are able to generate a higher volume of loans

- Not my favorite P2P platform interface

Related

Leave a Reply