InRento is a buy-to-let property crowdfunding platform that allows investors to put money into carefully curated rental properties across Europe. What started in 2020 as a small Lithuanian platform with three projects in Vilnius has grown into the EU’s largest licensed buy-to-let crowdfunding platform, now operating across six European markets: Lithuania, Poland, Ireland, Spain, Italy, and Latvia.

InRento was founded by Gustas Germanavičius, a Lithuanian serial entrepreneur. As of early 2026, the platform has crossed EUR 80 million in total funded investment volume, paid out over EUR 8.3 million in investor earnings, and still maintains a zero-default track record across all projects since inception. Those are numbers that very few platforms in this space can match.

I had the pleasure of chatting with Gustas on my podcast, where he explained that InRento was born out of the need to tap into a gap that he identified in the European real estate market.

According to Gustas, there are plenty of platforms offering higher-risk property crowdfunding and development deals, but many investors have started to shy away from those riskier bets. When you look at the lower-risk end of the spectrum, the pickings are slim. That is where InRento comes in.

InRento offers lower-risk real estate crowdfunding opportunities focused on rental properties rather than the more popular (and riskier) development loans that dominate many other platforms.

Read more: The Best European Real Estate Crowdfunding Platforms

These investors want reliable, no-fuss returns on their money. They are less concerned about capital appreciation and more interested in the passive income potential of rental properties.

With bank savings accounts still offering paltry returns across most of Europe, finding investment opportunities that deliver meaningful yield while protecting your principal is important. InRento positions itself squarely as an alternative to parking cash in the bank.

In this review, I will first show you how to sign up as an investor on InRento, followed by how to make your first investment.

I will then cover some important details about the platform and give my final opinion.

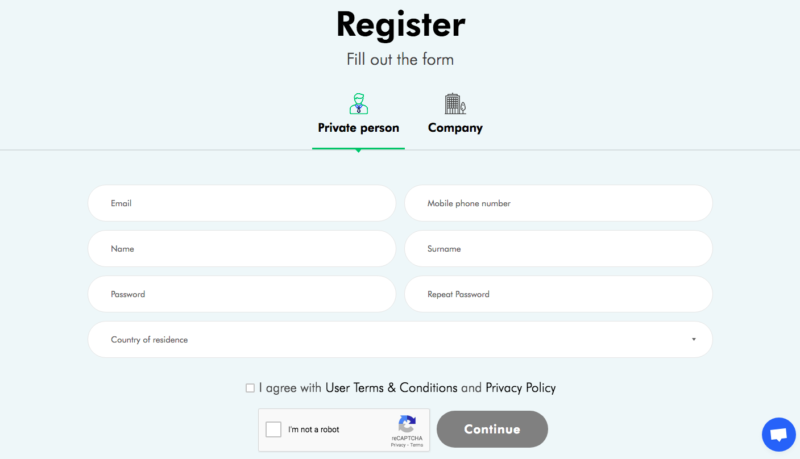

Setting up an Investor Account

At registration, you are prompted to sign up as either a private person or a company. In order to register as an investor, you need to be at least 18 years old and have a bank account, which is standard practice.

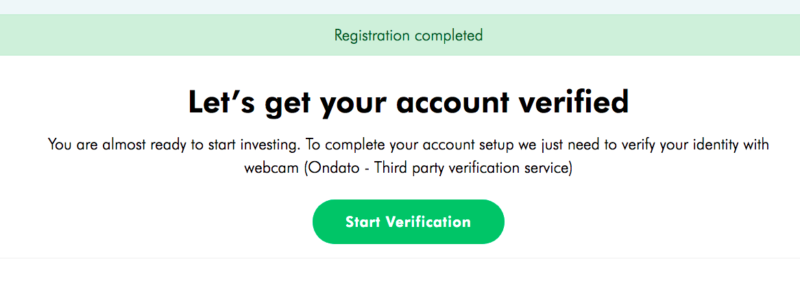

Once you create an account you will be taken through the identity verification process. InRento uses the services of Ondato, a third-party verification provider specializing in KYC, KYB, and AML compliance.

Once you create an account you will be taken through the identity verification process. InRento uses the services of Ondato, a third-party verification provider specializing in KYC, KYB, and AML compliance.

In the next step, you are asked to approve consent for personal data processing.

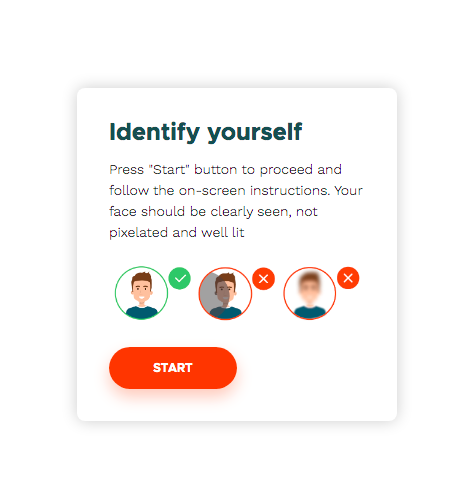

Next up is identifying yourself where you are asked to take a webcam selfie.

In the next step, you are asked to upload a photo of your passport or ID card. I chose to upload my passport photo.

The system will immediately inform you that your identification is being checked while it shows you a countdown timer of around 120 seconds. My identity was successfully verified within a minute, which I found to be very efficient.

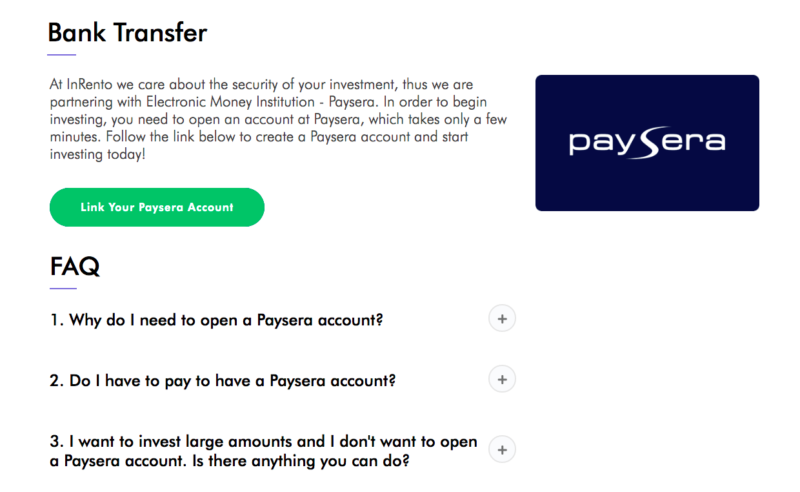

You are then led to your account menu where you can set up your payment method.

InRento now offers two payment providers: Paysera and MangoPay. Paysera is the original option and allows instant deposits and withdrawals via SEPA instant. You can also use your Paysera account independently for personal transfers. MangoPay is a newer alternative that works more like a dedicated wallet for your InRento investments. Deposits and withdrawals through MangoPay may take longer, but it provides a simpler setup for investors who do not need a full-featured payment account.

Opening either account is free of charge, with InRento bearing the transaction costs for primary market investments. There is one exception: investors planning to invest more than EUR 100,000 may have different arrangements.

Once your payment account is linked up, you will be able to start investing from the amount deposited. Any rental income received is also deposited to your payment account, which keeps fund management straightforward.

Making an Investment on InRento

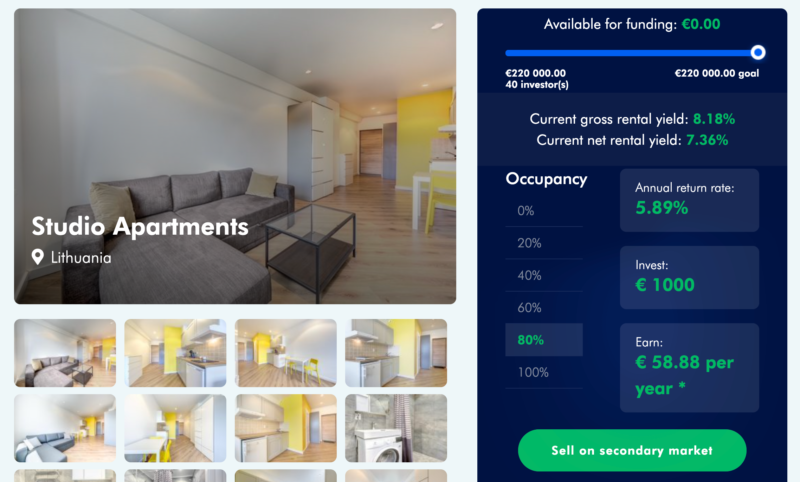

In order to invest in a project, you will need to head to the ‘Projects’ menu where you will be able to see all the project listings at a glance, both the funded ones and the ones which are still open to further investment. Upon clicking on a listing you will be directed to a dedicated listing page.

On the dedicated front page of every listing, you will find various photos of the property in question together with an occupancy calculator showing a number of relevant financial indicators, such as the remaining amount available for investment, a countdown timer for investing, and yield rates at different occupancy levels. I particularly like the yield rate calculator, as it allows me to make my own calculations rather than relying on idealistic scenarios pushed by the platform.

Each listing has 3 sub-categories: ‘Description’, ‘Documents’, and ‘Project News’:

- The ‘Description’ category sets out a comprehensive description of the project and includes the following information:

- nature and timeline for the current rental contract in place

- timeline of the project in terms of minimum and maximum terms

- gross and rental yield information

- statistics relating to the underlying rental market

- reasons for investing in the project

- the percentage split of rent between investor and borrower and frequency of rental payments

- information relating to vacant property scenarios and the fixed level of income investors would receive in different scenarios

- information on the borrower

- information relating to capital growth split upon sale of property

- key risks of the investment

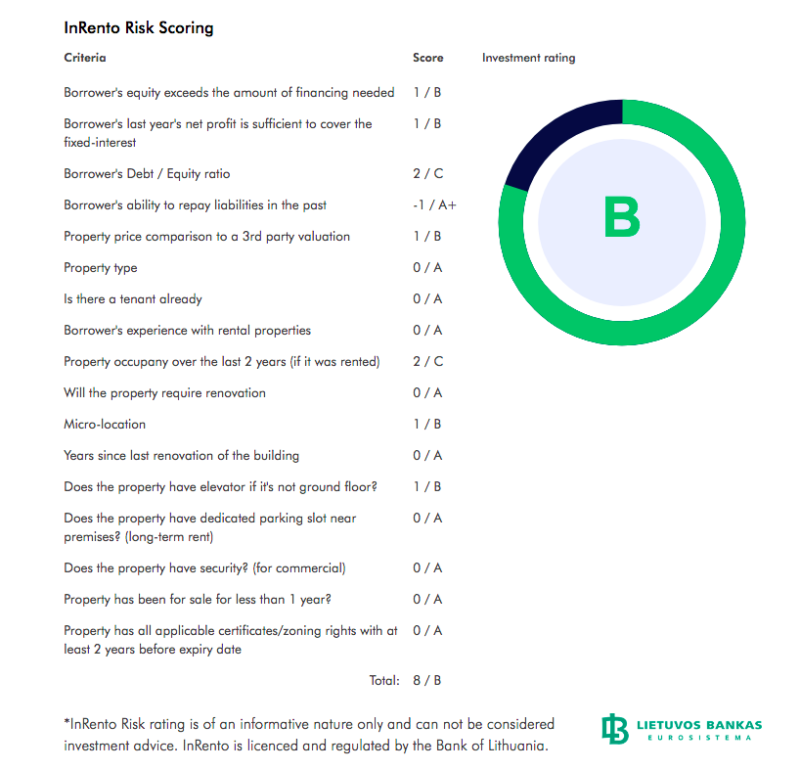

- InRento’s detailed risk score rating

- In the ‘Documents’ category, you can access PDF copies of official signed documentation relating to the underlying agreements on the property and the mortgage.

- As the name implies, the ‘Project News’ category lists any relevant news pertinent to the property, such as mortgage issuance and timing for rental payments to kick in.

In order to invest in a project, you simply need to click on the Invest button. The minimum investment is EUR 500 per project.

I found the information provided to be quite comprehensive in helping an investor make an informed decision.

Portfolio Dashboard

Once you have submitted your first investment you will be able to see a summary of your portfolio within a dedicated sub-menu.

The portfolio dashboard provides a snapshot of the investor’s account value, net annual returns, and monthly earnings. From the dashboard, you can deposit further money and view all past transactions.

Why are InRento Properties Lower Risk?

First of all, InRento has a very experienced team of licensed investment advisors with a solid track record in asset management and real estate. The team vets every property through multiple layers of analysis before listing it on the platform.

Second, the properties listed are already generating rental income and have a track record of doing so. They are located in good areas within real estate markets that show solid fundamentals.

Third, the numbers speak for themselves. InRento has maintained zero defaults across all of its projects since launching in November 2020. Out of 127 realized projects and counting, not a single one has resulted in a loss for investors. The platform does currently show a 4.88% late projects rate, which means a small portion of projects have experienced minor delays in payments or timelines. But delayed is very different from defaulted, and the overall track record remains strong.

What is InRento’s Business Model?

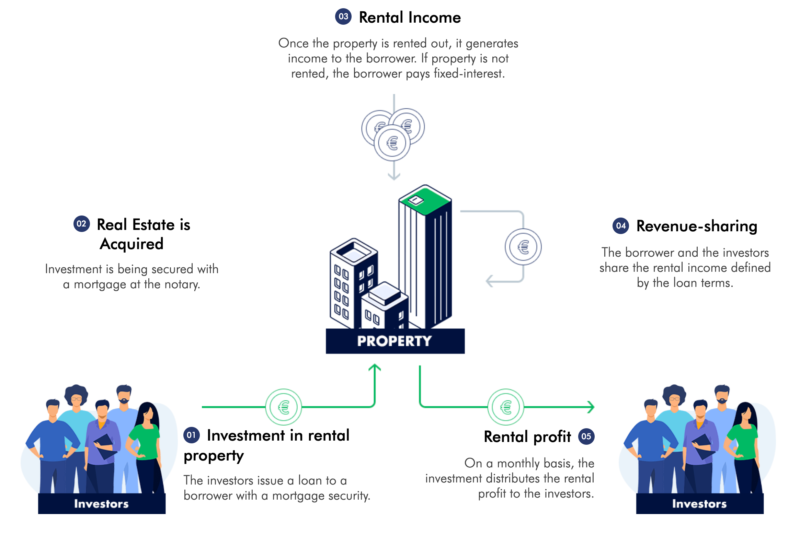

InRento acts as a bridge between property rental administrators who require capital to purchase rental properties and investors who want to earn passive income from rental properties backed by mortgage security, without needing to invest large amounts. The result is a monthly flow of rental income shared between the rent administrator (the borrower) and the investors, whose pooled funds form a loan to the borrower to acquire the property.

On one side, InRento actively sources and vets a pipeline of deals and their underlying borrowers before presenting validated ones as projects on the platform. On the other end, investors can pitch in starting from a minimum of EUR 500 per project. Each property has a target amount of total funding to be obtained by a set deadline. Once the total amount of required funding is reached, the investors start receiving a portion of rental income in line with the proportion of their investment.

If the total amount of required funding for the property is not collected from investors in time, all the collected money is returned to the investors.

Occupancy of property, net rental yield, and value appreciation

Since the investments are structured as loans, the rental income is structured as partly fixed and partly variable. When the property is 100% occupied by tenants, the monthly rental income would be typically split 80%/20% between the investor and the borrower respectively. If the property is fully vacant, the borrower is still obliged to pay the fixed interest rate.

Let’s look at this example:

- Loan value: EUR 100,000

- Monthly rental income at 100% tenant occupancy: EUR 1,000

- Fixed portion of monthly rental income: EUR 600

- At 100% occupancy: investors receive EUR 800, borrower takes EUR 200

- At 0% occupancy: investors receive EUR 600 (all paid by borrower)

- At 80% occupancy: investors receive EUR 600 (fixed portion) plus EUR 160 (80% of the balance of EUR 200), borrowers receive EUR 40 (20% of the balance of EUR 200)

While every project comes with its own specific terms and conditions, generally the longer a property remains vacant, the higher the fixed interest rate grows so that the investor receives the minimum rental yield stipulated at the time of investing.

In vetting potential projects, InRento favors those with multiple tenants over ones with a single tenant. The reasoning is straightforward: the more tenants there are, the lower the exposure to vacancy risk. InRento’s approach has been to only take on loans for properties that already have at least one tenant. This way, investors can accurately predict what the net rental yield of the investment will be.

In terms of capital appreciation, should the property be sold at a higher value than the cost at which it was purchased, 50% to 70% of the capital-growth share would flow to investors, with the balance shared between the borrower and InRento. This would be an additional return over and above the net rental yield in the year of sale.

With all of this in mind, it becomes clear that the InRento business model is designed to incentivize the borrower to produce the highest possible return. The higher the return is for the investor, the higher it is for the borrower as well.

The revenues for InRento come from the following:

- commission on the total funds collected for a project

- commission on every sale affected in the secondary market

- share of appreciation amount on the resale of the property

- late payment fees and contract termination fees payable by borrowers

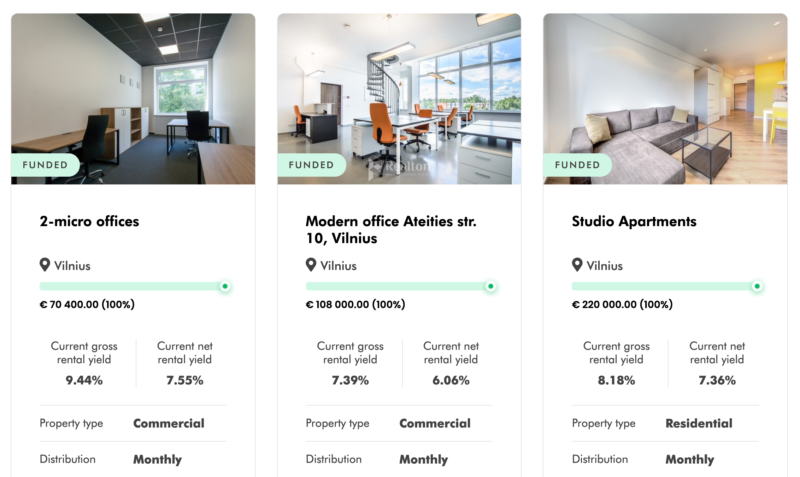

A Look at the Projects Available

Since launching in November 2020, InRento’s growth has been impressive. The platform started with just 3 projects in Vilnius and a total funded volume of EUR 353K. Fast forward to early 2026, and the platform has crossed the EUR 80 million mark in total funded investments, with 127 realized projects and over 4,300 active investors from 42 countries worldwide.

The geographic expansion has been particularly noteworthy. InRento now operates in six EU markets: Lithuania, Poland, Ireland, Spain, Italy, and Latvia. More than half (53%) of all projects financed in 2025 were completed outside Lithuania, which shows the platform has genuinely diversified beyond its home market. The company opened a Warsaw office to support its growing Polish operations, where it has become the leading buy-to-let crowdfunding platform.

Italy was the most notable market entry in 2025. The first Italian project, Hotel Catania in Sicily, raised EUR 520,000 in funding in just over an hour. Latvia followed in August 2025, with projects in Riga focused on the short-term accommodation and boutique hotel segment.

The properties listed on the platform continue to look modern and well-maintained. From my experience visiting the Baltics on numerous occasions, the Lithuanian projects live up to Baltic standards which are comparable to Nordic ones in terms of interior design. With the expansion into Western, Central, and Southern European markets, investors now have access to a genuinely diversified geographic portfolio.

In terms of returns, 2025 was a record year. The average annual return across the platform came in at around 11.77%, with some projects delivering even higher. For example, the Krynica-Zdroj apartment complex in Poland delivered 12.35% against a projected 11.5%, and the Floatel Vilnius project came in at 10.87% versus a projected 10%. Investor profits grew from EUR 3.1 million in 2024 to EUR 7.3 million in 2025, and the total amount of funds returned to investors reached EUR 27.19 million.

These are excellent numbers for a platform that positions itself on the lower-risk end of the spectrum. I believe the risk-return profile here is very competitive.

Is InRento Regulated?

InRento is authorized and regulated by the Bank of Lithuania. The platform received its European Crowdfunding Service Provider (ECSP) license on November 10, 2023, which means it operates under the EU-wide harmonized crowdfunding regulation framework.

The ECSP regulation provides a single set of rules for crowdfunding platforms operating across the EU, which gives investors enhanced protections and standardized disclosures regardless of which country a project is located in. This is a big deal for InRento’s cross-border expansion, as it allows the platform to passport its license and operate across the EU without needing separate approvals in each country.

Since InRento is regulated by the Bank of Lithuania, it has to abide by strict share capital regulations. In the worst-case scenario, if InRento were to go bankrupt, it would be sufficient for a contractual entity to be appointed to service the claims between the investors and borrowers. I have gone through such a winding-down process with Lendy, a UK platform that went bust a few years ago, and it was a very orderly process with no drama at all. This shows that once proper regulations and processes are in place, the platform risk for investors is greatly decreased.

Lithuania has been very conservative from a regulatory standpoint compared to neighboring Latvia and Estonia, and this offers an extra layer of assurance to investors who have been burned by scam platforms from Latvia and Estonia. That is not to say that every platform from those countries is dubious, but as investors, we should welcome regulation and favor platforms that operate within stable, well-enforced frameworks.

What is InRento’s Financial Health?

InRento’s financial position has strengthened considerably over the past few years. The platform initially raised EUR 130K in seed funding from Startup Wise Guys and business angels. Since then, InRento has raised EUR 40 million to fuel its EU-wide expansion, a significant vote of confidence from investors in the company’s growth trajectory.

The company has been profitable for two consecutive years. In 2024, sales revenue grew 53% to EUR 1.16 million, up from EUR 758K the previous year. Net profit dipped slightly due to heavy investment in the international expansion, but the underlying business model is clearly working.

Startup Wise Guys is an international institutional investor which has also invested in other well-known real estate crowdfunding platforms such as EstateGuru. It was recognized as the best venture capital fund in Central and Eastern Europe (CEE) in 2019. Tera Ventures, a VC fund focused on fintech and PropTech, also participated in the funding round. Another listed institutional investor on InRento’s website is Verslo Angelu Fondas II, one of the leading venture capital funds in Lithuania with a proven track record.

In 2022, InRento also merged with EvoEstate, Europe’s largest real estate crowdfunding aggregator at the time, which brought in over 12,000 additional investors and further solidified InRento’s position as the dominant buy-to-let platform in Europe.

InRento was also recognized as “LendTech of the Year” at the European FinTech Awards in 2025, which is a nice third-party validation of what they have built.

Investor Security

A primary concern that an investor has when investing in a loan is the creditworthiness of the borrower. In this regard, when receiving loan applications InRento performs thorough due diligence on the borrower. This includes evaluating their experience in the real estate market or administration of rental property, their reputation, any existing liabilities, disputes, or other factors that may impact the successful outcome of a project.

As the platform has scaled, the borrower base has diversified considerably, but InRento’s prudent appetite for risk remains evident in its selection process. The zero-default track record across 127 realized projects is the strongest evidence of this.

InRento analyzes the location of the asset and favors those in prime areas with a large count of transactions so as to reduce the level of vacancy risk. Additionally, the general asset condition is reviewed in determining whether it needs significant investment in renovation during the loan period. Consideration is also given to the difference between the acquisition cost and an independent third-party valuation.

Each loan is backed by mortgage security (first-rank mortgages). In 2025, the platform highlighted several projects with notably conservative loan-to-value ratios. For example, the Alvernia Planet project in Poland, which was the first financing of a publicly-listed company on the platform, had a loan-to-value ratio of just 21%.

In the case of a borrower default, InRento will take all the necessary measures to protect investors and, if needed, enforce the mortgage and repossess the property. The fact that this has never had to happen in over five years of operation is reassuring.

Investor money is handled in a risk-averse fashion. Prior to investing on the platform, investors are required to open either a Paysera or MangoPay account where investor funds are separately held. When a user decides to invest in a project and submits funds accordingly, the funds are held in an escrow account and only released to the borrower when a mortgage is secured. While this may feel like an extra step compared to some other crowdfunding platforms, it serves as an important layer of security for the investor. Given the scams and bankruptcies of lending platforms that we have seen in Latvia and Estonia, this precaution is well worth the minor inconvenience.

InRento also offers two-factor authentication through Google Authenticator to protect investors from unauthorized account access.

Liquidity

InRento provides access to its own secondary market where investors can sell their stakes or acquire others at a premium or discount. This provides added liquidity in the event of an investment not meeting expectations or if the investor needs cash.

With the platform’s growth, the secondary market has become more active and provides a realistic exit option for investors looking to sell their positions before term. InRento has also introduced a “Grand Sale” feature that enables the sale of larger secondary market positions in smaller pieces, making it easier for bigger holdings to find buyers.

One thing to note: InRento does not currently offer an auto-invest feature, so all investments need to be made manually. For a platform focused on carefully curated properties where you probably want to evaluate each deal individually, this is not a major drawback. But if you prefer a fully hands-off approach, it is worth being aware of.

Taxation

With the exception of Lithuanian resident investors, individual investors are subject to a 15% withholding tax on the earnings from interest.

This tax is then forwarded by InRento to the Lithuanian tax authorities. Depending on the residence of the individual investor, he or she will then need to check with local authorities on whether this tax is final (which would be the case where double-taxation treaties with Lithuania are in place) or otherwise pay additional tax on the receivable income in the country of residence. For EU residents this should generally be less problematic than for non-EU ones who may find it difficult to recover the withheld tax, particularly when it comes to small amounts.

On the other hand, Lithuanian resident investors will receive the full rental yield and are thereafter required to declare this income separately on their personal tax return.

No tax is withheld in the case of corporate investors. This makes it easier to invest through a corporate structure, in a similar way that I detail in my post about tax strategies in Europe.

Website

The website has a clean interface and is generally user-friendly with a dedicated FAQ section. Users are able to switch the website content between English and Lithuanian.

The website contains a blog section that has been updated consistently since the platform launched in November 2020. The quarterly investor updates are particularly useful, providing transparent breakdowns of portfolio performance, new market entries, and key metrics. This level of transparency is always a positive indicator.

Fees

Investing in a project is free of charge. When operating within the secondary market, there is a 2% fee on the principal value of investments sold.

There are no fees for using either payment provider (Paysera or MangoPay) on InRento.

Customer Support

The website offers support via email and upon sending a couple of queries through I was attended to within a mere few minutes. Responsiveness has been consistently good in my experience.

My Thoughts on InRento

I have been following InRento since its early days, and the trajectory has been genuinely impressive. The growth from a small Lithuanian platform with 3 projects and EUR 353K in volume to a pan-European operation with EUR 80+ million in total funded volume, 127 realized projects, and zero defaults is remarkable. Very few platforms in the real estate crowdfunding space can point to that kind of track record.

The 2025 numbers tell a compelling story: average annual returns of around 11.77%, investor profits more than doubling to EUR 7.3 million, and successful expansion into six European markets. The ECSP license, the EUR 40 million fundraise, the EvoEstate merger, and the “LendTech of the Year” recognition all point to a platform that has moved well beyond the startup phase and into a serious growth trajectory.

There are a few things I would like to see improved. An auto-invest feature would be a welcome addition for investors who want a more hands-off experience. And while the 4.88% late projects rate is not alarming, it is worth monitoring as the platform scales further into new markets. As deal volume increases, maintaining the same level of underwriting quality becomes more challenging.

Overall, InRento provides multiple layers of security for investors: ECSP regulation, first-rank mortgage backing, escrow accounts, and a diversified geographic portfolio. For investors looking for lower-risk rental property exposure across European markets, InRento is one of the strongest options available today.

As always, I recommend that you do your own research before making any investment decision. Diversification across platforms and asset classes remains key.

Summary

InRento has grown from a small Lithuanian startup into the EU's largest licensed buy-to-let crowdfunding platform, now operating across six European markets with EUR 80+ million funded and zero defaults. The platform delivers strong returns (around 11.77% average) backed by first-rank mortgages and ECSP regulation. A solid choice for investors seeking lower-risk rental property exposure in Europe.

Pros

- Zero defaults across 127+ realized projects since 2020

- ECSP-licensed and regulated by Bank of Lithuania

- Diversified across six European markets

- Strong average returns (~11.77%) for a lower-risk platform

- First-rank mortgage backing on all loans

Cons

- No auto-invest feature

- 4.88% late projects rate worth monitoring

- 15% withholding tax for non-Lithuanian investors

Related

Love how InRento is filling that much-needed gap for lower-risk, rental-focused real estate investing! It’s refreshing to see platforms catering to more cautious investors