If you’re still using your bank for international money transfers, you’re overpaying — probably by more than you realize. Banks don’t just charge a transfer fee. They also quietly apply an exchange rate markup of 2–5% above the real mid-market rate. On a $10,000 transfer, that’s $200–$500 gone before the money even leaves your account.

The good news is that the fintech alternatives have matured considerably since I first wrote about this. What started as scrappy startups are now multi-billion dollar platforms with real banking infrastructure, debit cards, interest on balances, and genuinely competitive rates. And beyond fintech, stablecoins have moved from being a curiosity to a practical tool for international transfers.

Here’s what’s actually worth using in 2026.

Wise

Wise (formerly TransferWise) is still my top recommendation for most people. They use the real mid-market exchange rate with no markup — what you see on Google or XE.com is what you get. Their fee is charged separately and transparently, and for major currency pairs it typically comes in under 0.5% of the transfer value.

But Wise is no longer just a transfer service. It’s evolved into a full multi-currency account:

- Hold money in 40+ currencies with no monthly fee

- Get local account details in USD, EUR, GBP, AUD, and more — useful for receiving payments internationally

- Order a Wise debit card for a one-time fee of around $9 USD. Spend in any currency at the mid-market rate

- Earn interest on idle balances: as of early 2026, around 3.26% variable on GBP and 3.14% APY on USD, with EUR rates lower but still positive

The interest feature is genuinely useful if you’re holding balances between transfers. The fee is 0.29% annually on USD and 0.26% on EUR, which is modest for what’s effectively a money market fund.

One thing to keep in mind with the debit card: you get two free ATM withdrawals per month up to $100 USD total. Beyond that, you pay 2% on the excess and a $1.50 fee per additional withdrawal. Fine for occasional use, not ideal if you’re withdrawing cash regularly.

Revolut

Revolut is the other major player and worth considering depending on your usage pattern. On weekdays, the free (Standard) plan gives you up to $1,000/month of currency exchange at interbank rates. Above that, you pay a 0.5% fair usage fee. On weekends, there’s a 1% markup for Standard plan users.

Paid plans remove the weekend markup entirely (Premium, Metal, and Ultra) or halve it (Plus at 0.5%). Premium starts at around $9.99/month depending on your region.

Where Revolut has an edge over Wise is the breadth of its banking-adjacent features — budgeting tools, stock trading, crypto, and more — all in one app. If you want a single app for your financial life, Revolut is compelling. If you just want the best rate on transfers and a multi-currency account, Wise is usually cleaner.

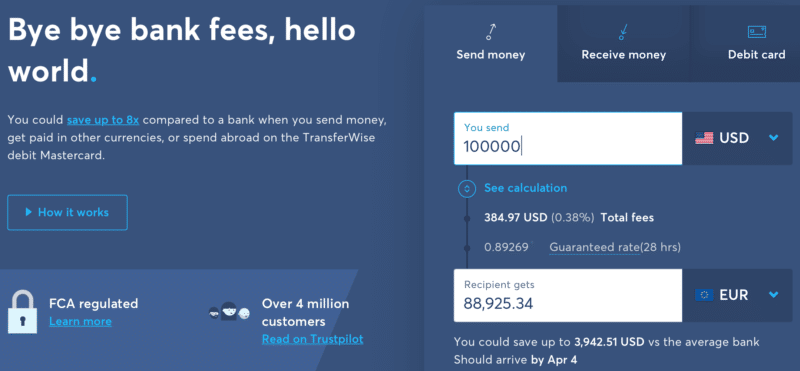

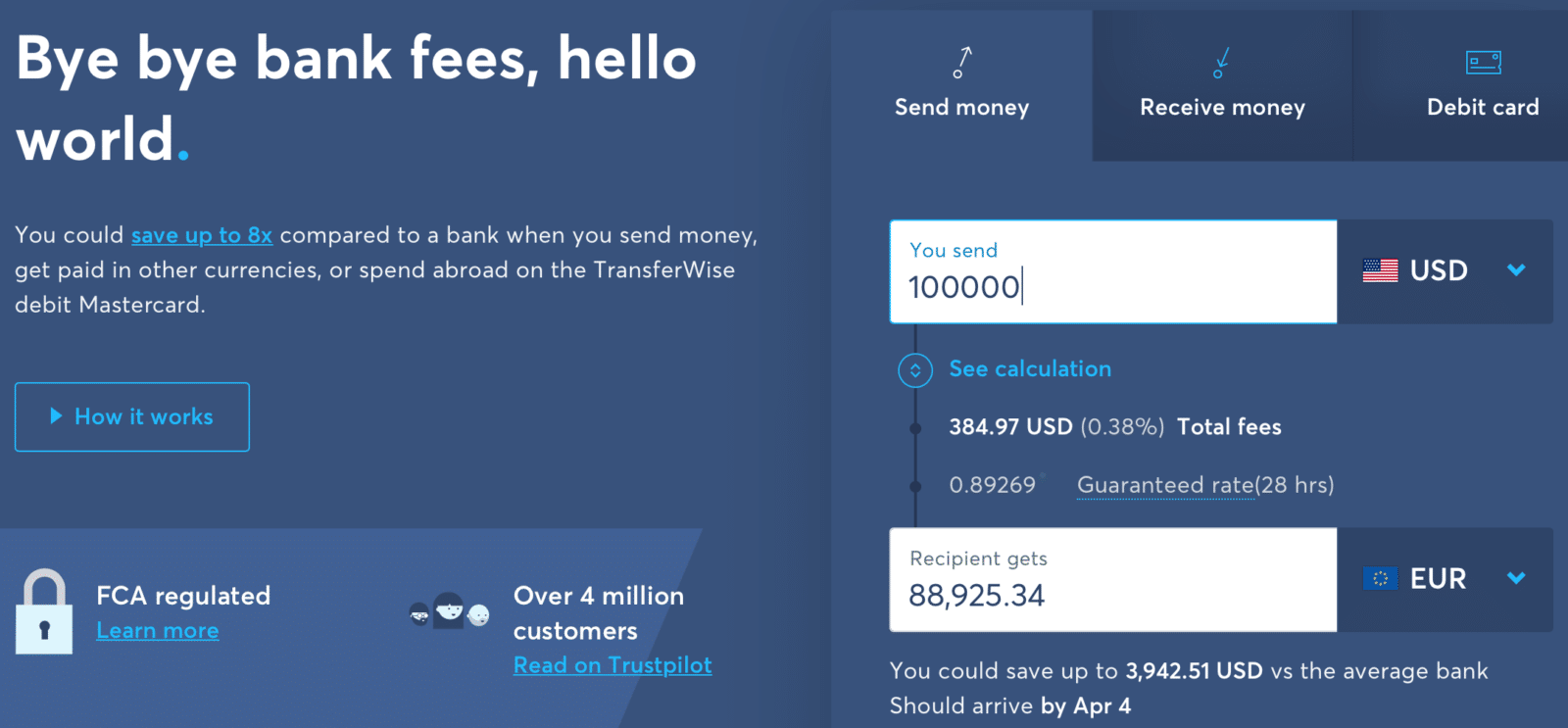

How the Numbers Compare: $100,000 USD to Euro

The Malta bank comparison in this article has been updated below, but first, a note on why these comparisons still matter.

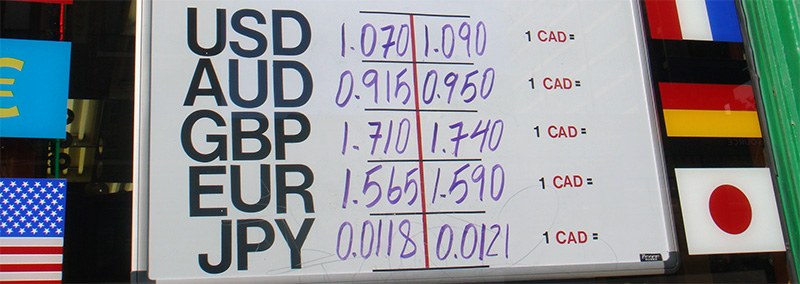

I’ve spent time researching exchange rates offered by Maltese banks, since Malta is where I have family and financial ties. When I checked rates across the main banks for a USD to EUR conversion, almost every bank was offering around 0.745 EUR per 1 USD for smaller amounts, with HSBC consistently coming in worse at around 0.741. Those rates don’t include the wire transfer fees on top.

Here are links to the exchange rates offered by the main banks in Malta if you want to check current figures yourself:

- HSBC Malta

- Bank of Valletta Exchange Rates

- Banif Exchange Rates

- Lombard Exchange Rates

- APS Bank Exchange Rates

The pattern is consistent: traditional banks apply a 2–5% markup above the mid-market rate on top of their flat transfer fees. For a $100,000 transfer, that’s a $2,000–$5,000 haircut before the money arrives. Fintech platforms like Wise typically bring the total cost (fees plus rate markup) under 0.5–1% for major pairs. The math isn’t close.

CurrencyFair

CurrencyFair was one of the pioneers in peer-to-peer currency exchange, and I used it for years. It’s still operating — it was acquired by Australian fintech company Zai in 2021 and remains active. However, it’s worth knowing that in 2023 CurrencyFair dropped its peer-to-peer matching model (the feature that made it genuinely distinctive), reduced its supported currency list, and effectively became a standard FX platform.

It still works, and may be worth a comparison quote for specific corridors, but it no longer has a structural advantage over Wise. I’d treat it as a fallback rather than a first choice today.

For Specific Corridors: Remitly and WorldRemit

If you’re sending money to emerging markets — Latin America, Africa, Southeast Asia, the Philippines — Remitly and WorldRemit are worth checking. They’ve built out payout networks that include cash pickup, mobile wallets, and airtime top-ups in addition to bank deposits, which matters a lot in markets where banking penetration is low.

Remitly has a Trustpilot rating of 4.6 and is particularly strong for the US-to-Philippines and US-to-Mexico corridors. Exchange rate markups run 1–3.7% above mid-market, so they’re not as competitive as Wise on rate, but for corridor-specific speed and payout options they sometimes win.

WorldRemit covers 150+ receiving countries but has seen more mixed reviews (Trustpilot 3.8). Fees range from $1–$5 flat with 0.5–2% rate markup for bank transfers.

For large transfers ($10,000+) to 50+ currencies, OFX is also worth considering. They charge no flat transfer fee above certain thresholds and apply a rate margin of around 0.5–1.5% — competitive for larger amounts, though their real-time rates aren’t always publicly visible upfront.

Bonus: Negotiate a Better Rate with Your Bank

If you’re processing significant currency conversion volume — I’d say $50,000 and above annually — it’s worth calling your bank and asking for a preferential rate. Most banks will negotiate, and they don’t advertise that this is possible.

To give you a concrete example: I’ve negotiated a special rate with my bank for USD to EUR conversions. On a given day where the official buying rate was 1.1138 and the reference rate was 1.0946, my negotiated preferential rate came in at 1.0998. On a transfer of $66,000, that difference translates to over €700 saved compared to the standard rate.

It’s not always worth the administrative overhead, and for anything under $50,000 Wise will likely beat even a negotiated bank rate once fees are factored in. But if you’re doing regular large conversions, it’s a call worth making.

How to Time PayPal Withdrawals for a Better Rate

![]()

This is for those of you who receive payments via PayPal and need to convert to a local currency before withdrawal.

PayPal’s exchange rates are notoriously poor — they apply a significant markup above the mid-market rate, and then charge a withdrawal fee on top. The better approach, if you have flexibility on timing, is to monitor the exchange rate and withdraw when the rate is favorable.

The practical way to do this without checking manually: set up rate alerts at XE.com. Set your target rate — look at historical rates over the past 90 days to calibrate what’s realistic — and XE will email you when the rate hits your threshold. Then you initiate the withdrawal immediately.

Alternatively, link a Wise account to receive PayPal transfers in USD, then convert manually through Wise at a much better rate than PayPal would give you directly. This adds a step, but the rate difference is usually significant enough to be worth it for larger amounts.

The other option is the simple one: withdraw on a fixed day each month. You won’t always get the best rate, but you eliminate the mental overhead of rate-watching and ensure regular cash flow.

Note: If you have questions about PayPal-specific issues, please leave a comment rather than emailing — due to time constraints I can’t respond to PayPal-related emails individually.

Bitcoin and Stablecoins for International Transfers

When I first wrote about using Bitcoin for international transfers, it was an experiment. In 2026, it’s a legitimate strategy — and in some cases the cheapest option available.

The basic mechanics are the same: convert fiat to crypto at the sending end, send across borders (near-instantly, 24/7, with no correspondent banks involved), then convert back to local fiat at the receiving end. For a $1,000 transfer, this can cost under 1% end-to-end compared to 3–7% for a traditional wire or PayPal.

The main practical route:

- Open an account on Coinbase (or Kraken, which has strong EUR support)

- Complete identity verification — required for regulatory compliance, takes a day or less

- Sender deposits the USD equivalent in crypto to your deposit address

- You sell the crypto for EUR and withdraw via SEPA — Coinbase’s SEPA withdrawal fee is around €0.15, arriving within 1–2 business days

Trading fees on Coinbase Advanced (formerly Coinbase Pro) run 0.60% for makers and 1.20% for takers at standard volumes, dropping with higher 30-day volume. For occasional large transfers this is competitive, though Wise may still win on simplicity and total cost for EUR transfers.

The stronger case: stablecoins

The volatility risk with Bitcoin is real — the few minutes between receiving BTC and converting it to EUR is enough for the exchange rate to move against you. Stablecoins solve this.

USDC (USD Coin) is now a $74 billion market cap asset backed 100% by cash and short-dated US Treasuries, attested monthly by independent auditors. Sending USDC is essentially moving digital dollars. On networks like Solana or Base, transactions settle in seconds with gas fees often below $0.01.

The workflow for remittances increasingly follows a “stablecoin sandwich” model: convert local currency to USDC at the sending end, send USDC across borders, convert USDC to local currency at the destination. All-in costs including the on/off ramp typically run 1.5–2.5%, compared to 6–8% for traditional bank wire transfers on the same corridors.

This is particularly compelling for sending money to regions where Wise and Revolut have limited coverage, or where the recipient doesn’t have a bank account — MoneyGram’s integration with the Stellar network lets recipients convert USDC to cash at participating branches.

For regular USD/EUR conversions where both parties have accounts at regulated exchanges, the crypto route is genuinely practical today. The regulatory environment has also improved significantly: the GENIUS Act passed in mid-2025 established a clear US framework for stablecoins, and Visa launched USDC settlement in December 2025.

One caveat: cryptocurrency transactions can have tax implications depending on your jurisdiction. In most European countries, converting crypto to fiat is a taxable event. Make sure you understand your local rules before using this approach at scale.

The Bottom Line

For most people doing international transfers in 2026, the hierarchy looks like this:

- Wise — best default for transfers and multi-currency accounts. Real mid-market rate, transparent fees, debit card, interest on balances.

- Revolut — strong alternative if you want more app features. Watch the weekend markup on the free plan.

- Remitly / WorldRemit — better for specific emerging market corridors with cash pickup or mobile wallet payout needs.

- OFX — worth comparing for large transfers ($10,000+) with no flat transfer fee.

- Crypto/stablecoins (Coinbase, Kraken) — genuinely competitive for tech-comfortable users, especially for corridors where fintech coverage is limited.

- Negotiate with your bank — for high-volume users doing $50,000+ annually, still worth the conversation.

- CurrencyFair — still operating, but no longer distinctive. Compare rates, but don’t expect it to beat Wise.

The worst option in every scenario is letting your bank handle a conversion at their advertised rate without question. The gap between what banks charge and what fintech platforms charge has only widened over the past decade.

How do you manage your currency exchanges? Leave a comment below — I’m particularly curious whether anyone has been using stablecoins regularly for remittances.

Related

This method does not work. If you want the best rate from PayPal looking at real time rates on any app/website or elsewhere only tells part of the story. You have to actually watch the PayPal exchange rate as well which does NOT follow actual rates. In fact the Payl exhange rate is only periodically updated. I’m trying to figure that one out. At this point it appears they may update their rate once or twice a day but I am verifying that myself.

Use this method instead: watch for actual rates to rise on your favorite app then watch for PayPal rates to update to follow the rise. PayPal charges 4%. If the actual exchange rate rises and the difference between the posted rate and PayPal’s current rate is more than 4% then you are really being hosed. If PayPal’s rate is only update once or twice a day at least wait till it’s closer to 4% or you are being taken to the cleaners. If the actual rate is on an upswing at least wait till PayPal catches up and updates their rate to get the best actual rate.

Hello Jean,

I’m about to set up an online translation business. While I finally decided what legal setup is best, I’d like to start operating with no register at all, kind of testing the service and the idea.

I guess the most simple is PayPal at first? Apparently Paypal doesn’t allow linking to Transferwise which is a bit of a pain… I was ready to use my Transferwise borderless card but I need a connecting platform such as PayPal to make payments from clients possible. My PayPal is linked to a UK account and also N26 (although they say they do not support virtual banks?) Any recommendation?

I am Spanish citizen, digital nomad with no fixed resident at the moment (latin america), and aiming at setting up this biz mainly for US clients (US).

Stripe only allow registering with an actual company registration – I could do a UK LLC although not sure about the long term tax rate and so on. Or perhaps a US LLC but not ready to make this investment yet (500$ register fee).

Sorry for the long message! just trying to make sure what’s the best option to start out. Thanks

Hola Maria,

I don’t think N26 is treated as a virtual bank since for all intents and purposes it functions like a normal bank account, including having a unique IBAN number.

PayPal, with all its problems, would probably be the easiest way to start for you.

Further on, as you you correctly state, you could set up a US, UK or even Spanish company and accept Stripe payments.

It wouldnt be better to do the money transfer by using transferwise to mintos and there to keep the money 1 month?

That could also be an option. Why do you think it’s better?

If one where to withdraw USD funds from Paypal to local Maltese banks, the funds received in EUR will actually be higher with HSBC than with BOV (I’ve tested this on multiple withdrawals).

But if I’m not mistaken credit card withdrawals use VISA’s exchange rates and not the Bank’s exchange rates. The concerned bank will then add its fees and that explains the difference in funds received.

On regular transfers it’s advantageous to use Transferwise or CurrencyFair.

Hmm, how would you explain the fact that HSBC works best in that case? It has worse conversion rates compared to BoV.

If I’m not mistaken this is how it works… Once you withdraw funds to a VISA card the USD funds will get converted to EUR by VISA(an international company that uses up-to-date exchange rates) and then VISA forwards EUR funds to your EUR bank account. So the conversion has already taken place before the funds land in your bank account.

The rates you found are only used by the bank to make currency conversion(bank transfers mainly), in this case the currency exchange is made by VISA and not by the bank.

http://www.visaeurope.com/making-payments/exchange-rates

Right. I’ve checked my account and I can see that there are no charges related to inward transfers via the VISA card. The transaction details the exchange rate used and nothing else.

When I do a SWIFT transfer in USD, BoV charges an inward fee since they charge feeds for incoming USD. This seems to support what you are saying.

What I don’t understand, however, is how doing the transfer to HSBC results in more money in your account versus BoV. If the conversion is done by VISA themselves, then the resulting EUR in the bank account should be the same for both banks, right?

I’m still trying to figure that out. It could be that the conversion is being done by the bank itself but they use exchange rates from VISA and add a conversion fee of their liking on top of the exchange rates.

Hmm, that would be pretty bad, since they are not disclosing any other fee.

You can see all BOV’s fees here – https://www.bov.com/documents/bov-tariff-of-charges.

If you search fees for other banks you’ll find a similar doc.

Yes I know and there are no fees relating to incoming VISA income in Euro.

Very easy to calculate pricing for currency conversion by comparing their buying and selling rates;

BOV: (1.1005+1.1398)/2=1.12015 which is the actual rate they are comparing to

So their charge is (1.12015-1.1005)/1.12015=1.75%

HSBC: 2.5%

Good point, thanks Francarl.

Possibly of interest, Payoneer is using Hyperwallet on their backend. If anyone is looking to build a system like Payoneer, check them out. They have some powerful possibilities. Speaking to that is the fact that they recently got acquired by PayPal in Jun 2018 (iirc). Braintree was acquired by PayPal in Sep 2013, so they might be leading to some mass integration of services soon across all three platforms.

I noticed that neither of the sites mentioned in the article are working today.

So today I found this tool on the site of Transferwise. I also offers email alerts.

https://transferwise.com/tools/exchange-rate-alerts/

Let’s see if it works in the coming weeks.

hello!

im searching in google if is possible change the balance of my paypal in usd to EUR im spanish and sell in dollars but nothing only can do that with the conversion of paypal to buy if possible choose different conversion but to sell not…

maybe im confuse but do you know that info?

thanks!!

Great post, I was wondering why my balance is kept in USD even though i’m in Euro zone.

Hi Jean,

Isn’t there a fee for buying bitcoin in the first place?

You’re right John, in my case I didn’t pay that fee as my friend was sending me money so I received Bitcoin directly.

I updated the fee schedule above to reflect the full cost if you had to transfer USD/CAD to EUR between two of your own accounts.

As you rightly consider, you’d have to pay both the maker and taker fee commission when doing the transfers.

In any case it would still be a very low fee and lower than what banks charge.

Hi there. But you also need to factor in the price to send bitcoin from your friends wallet to yours.

Isn’t it quite expensive to send bitcoin?

Most people use ltc and then convert.

What was the btc transfer fee?

It depends on the current transaction fee levels. They tend to vary. You could even use stablecoins nowadays, but ltc is also an alternative.

Thanks. Works for me (in Australia) 🙂

Still the same “Question” Is there any alternate to the Pay pal for India.(While receiving payments from Canada)

I’ve heard people mention Payoneer for cases like yours, but I’m not an expert on that.

Hi, thanks for your article – its a clever way to make sure you’re not getting ripped off.

I have a specific problem, and I was wondering if you or anyone else could help…

I receive payments from a foreign client in British pounds and usually convert to USD when accepting payment. Thereafter I withdraw the money to my South African bank account (which means another fee to convert it to South African rands). Should I rather keep the funds in the currency they were sent in? Does that mean no conversion is done until I choose to do so?

Any advice would be greatly appreciated.

Lars

If you are using PayPal then yes I’d keep them in GBP and only convert them to South African rands when I want to.

Thank you for advice

Wow great tool! The problem I have is that the 3 month currency conversion ($ to £) looks to be at a high right now of .62 but paypal is only paying .60 today. So is the tool then useless if paypal doesn’t match the current exchange rate?

Read my other post about PayPal exchange rates, PayPal are usually not the best place to have your conversions happen, and I’ve found a way around that.

And that way around is?^^

Check out my latest update on this subject https://jeangalea.com/changing-paypal-withdrawal-currency/

Is there any way to just work my way around their horrendous exchange rates? I want to withdraw $582 but I’m losing $17 just because of their outdated rates.

My money is converted into rupees.

PayPal charge me double. Why?

Just fir trying paypal I order some thing that cost 1 us dollars = 60 INR but they charge me 120 INR.

That means 2 dollar. Can anyone tell me why?

Wonderful info! Thank you.

But uhho… PayPal has only auto-withdrawal for India… 🙁

guys, leave PayPal and move to TranferWise whenever you can.

They are really two services with different uses. PayPal is most commonly used for accepting payments online, and there isn’t an easier service than that at the moment.

Great share ! Thanks 🙂

Right now I’m really confuse whether use PayPal or Payoneer to receive my online payment as freelancer.. Currently I use Paypal, since at that time I don’t know about Payoneer.. PayPal takes a lot of money from difference currency exchange rate each time I need to withdraw to my local bank account.. It quite hurts ! :(..

My question is, is Payoneer currency exchange rate is better than PayPal for withdrawing money to local bank ? If yes, is it still worth ? Since Payoneer is charge some fee also as membership subscription base what I know..

PS: My PayPal base currency is USD, and my local bank account is IDR..

Thanks in advance for any advices..

Regards,

Ronny

Welcome! I haven’t used Payoneer lately so I can’t give you any advice on that comparison unfortunately.

That was good. Wish it worked here in India as according to rules here, we have to transfer PayPal balance to bank account within 7 days of receiving money or else PayPal will automatically transfer it on the last day at whatever the exchange rate is then. PayPal is already ripping me off a lot of my money with their ridiculous exchange rates..

I do withdraw USD to EUR just above 100 € so to avoid the 1 EUR fee.

This morning the exchange rate, according to major sites was like this:

$ 138 = € 101.6646

but paypal calculate like this:

$ 138 = €98,89 EUR, and still wanted the 1 EUR fee.

Isn’t this called stealing?

It is. I am wondering, aren’t there alternatives? paypal is becoming so widely used and I don’t understand why when the fees are such. does it mean people don’t see the “price” of the service? no one else can compete?

Paypal have established a footprint so large that it’s hard for anyone else to compete. However there are other ways of accepting payments which are growing more and more popular every day. Check out Stripe, PayMill, 2CheckOut, Avangate.

Awesome tip!! thank you very much mate. I was going to withdraw a couple of minutes ago but smth stopped me this time. I started to google and found your article. Just what the doctor ordered. 🙂

For 2 years, I’ve been transferring USD to Czech Crowns every time I get paid from my freelancing gigs without a second thought. Of course, waiting for the opportune moment to withdraw money is ultimately a bit of a gamble, but this info will likely earn me quite a few extra beers per month. Thanks for the info. 🙂

I’ll be sure to join you for a few beers then when I visit the Czech Republic 😉

thanks for the tip jean 🙂 really useful!

Welcome Matthew!

That’s something I should really do but I just keep the money in USD and then convert it to GBP when I withdraw the money. PayPal’s fees are ridiculous though. I hate the idea of them ripping me off at the conversion stage, especially after taking off a hefty fee.

I was actually referring to the stage of withdrawing the money, where PayPal does not actually charge a fee (as far as I know). Are you referring to occasions when you pay someone in another currency rather than what you have in your account? I keep most of mine in USD too, then they get automatically converted when I withdraw to my bank account.

I’d be interested in some further advice on this matter if you’re still watching this board as of 2015 and the new PayPal changes…

I keep my USD PayPal payments in a USD balance and convert when withdrawing to my (GBP) bank account. However, on doing so, PayPal then converts my balance to GBP itself automatically on withdrawal and applies the same extra 2.5% conversion rate to its exchange rates that it would when converting in any other manner. I’d love my bank to handle the conversion but PayPal refuses to allow me to withdraw USD to a British bank account. I even considered setting my account up as a USD account so that I could handle conversion manually, but apparently, when PayPal is asked to withdraw in USD to a USD account in Britain, it nonsensically converts the currency TO GBP and then converts it BACK again, basically just so it can levy the charges multiple times. So can you think of any way around this?

Well this is exactly what I asked Paypal to change for me and they did it without any problem. It seems to be an arbitrary decision though, depending on who the support tech on the other end is. It could also be that they got newer instructions from above to stop making these exceptions.