Afranga is a Bulgarian P2P lending platform that has been quietly building a solid track record since 2021. Originally created as a funding vehicle for Stikcredit, one of Bulgaria’s leading online consumer lenders, the platform has since evolved into a regulated marketplace connecting European investors with multiple loan originators.

What caught my attention is the combination of ECSP regulation, zero reported investor defaults, and returns north of 13%. In a P2P landscape littered with platforms that have burned investors over the years, Afranga’s decision to pursue ECSP regulation and rebuild its platform around the new framework deserves a closer look.

The platform is licensed as a European Crowdfunding Service Provider (ECSP) by the Bulgarian Financial Supervision Commission, with approval granted in September 2023. All investor funds are held in segregated accounts managed by Lemonway, a licensed French payment institution. This means your money is kept separate from Afranga’s operational funds, which is a critical safety feature that not all platforms offer.

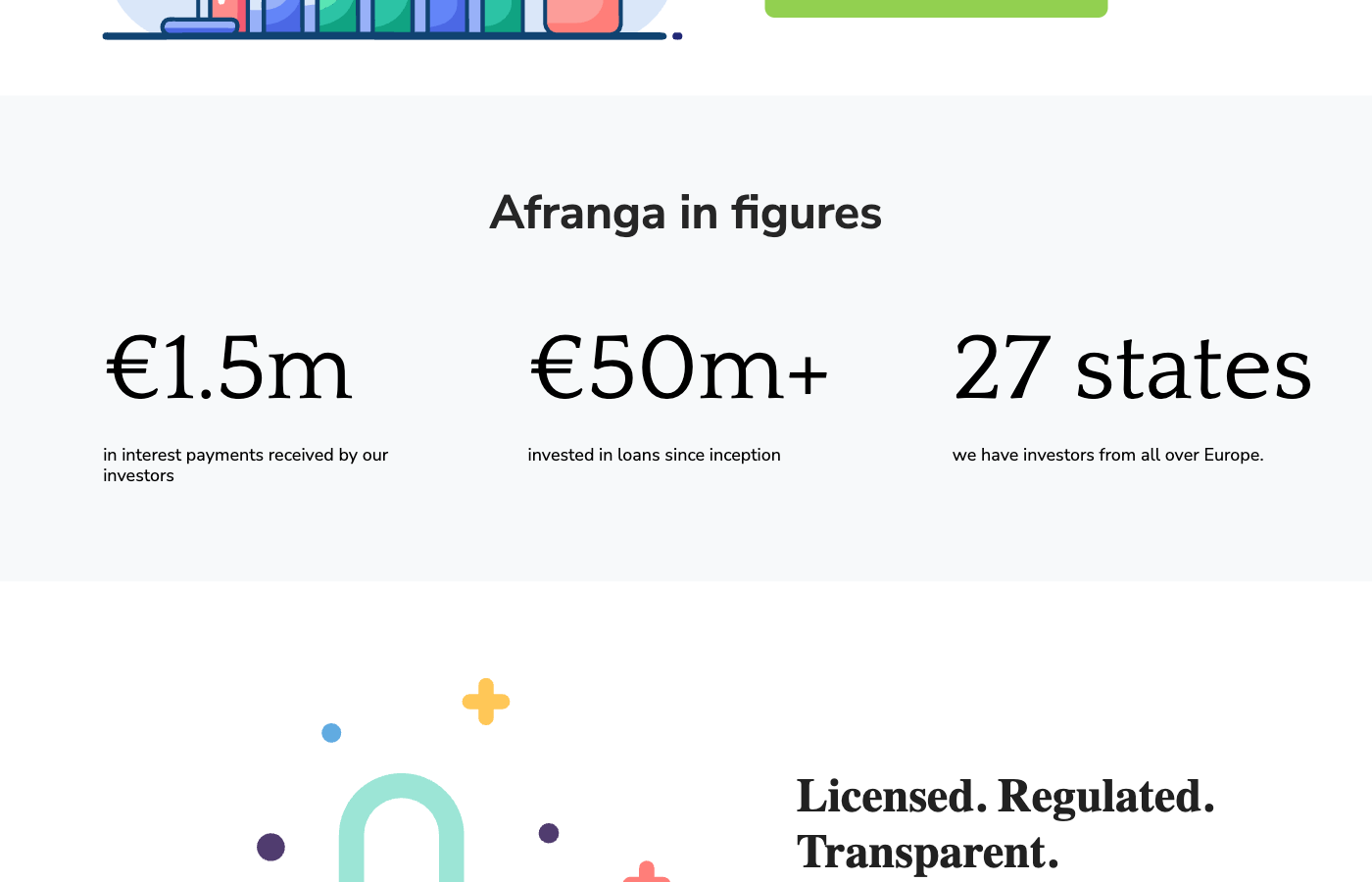

As of early 2026, Afranga has facilitated over EUR 89 million in funded loans, maintains a portfolio of roughly EUR 20 million, and has attracted over 4,000 new investors in 2025 alone. The actual investor return for 2025 came in at 13.92%.

The Stikcredit Connection

You cannot understand Afranga without understanding Stikcredit. Afranga is owned by Stik Credit JSC, a Bulgarian consumer lender that has been operating since 2013 under supervision from the Bulgarian National Bank (registration No. BGR00370). Stikcredit has issued over EUR 100 million in loans and serves more than 45,000 customers.

Svetlin Sabev, who serves as Afranga’s CEO, was previously COO at Stikcredit. He founded Afranga in 2021 and has been the sole shareholder since 2023. The management team also includes Yonko Chuklev handling compliance and finance (15+ years experience) and Veniamin Istomin, who joined in September 2024 from Bondster, another P2P platform.

The tight relationship with Stikcredit is both Afranga’s greatest strength and its most obvious risk. On the positive side, Afranga has deep visibility into Stikcredit’s loan book and operations. On the downside, if Stikcredit runs into trouble, Afranga would be directly impacted. This single-originator dependency has been somewhat mitigated by the platform’s expansion to include external loan originators, but Stikcredit still dominates the portfolio.

Stikcredit reported a net profit of EUR 3.48 million in FY2024 with a 54% equity ratio, which are healthy numbers. However, the impairment rate on its loan portfolio sits at around 36.8%, which looks alarming at first glance. The re:think P2P team (who visited Afranga in Bulgaria) suggests this reflects conservative accounting practices and the nature of consumer lending in the region rather than an actual crisis, but it is something to be aware of.

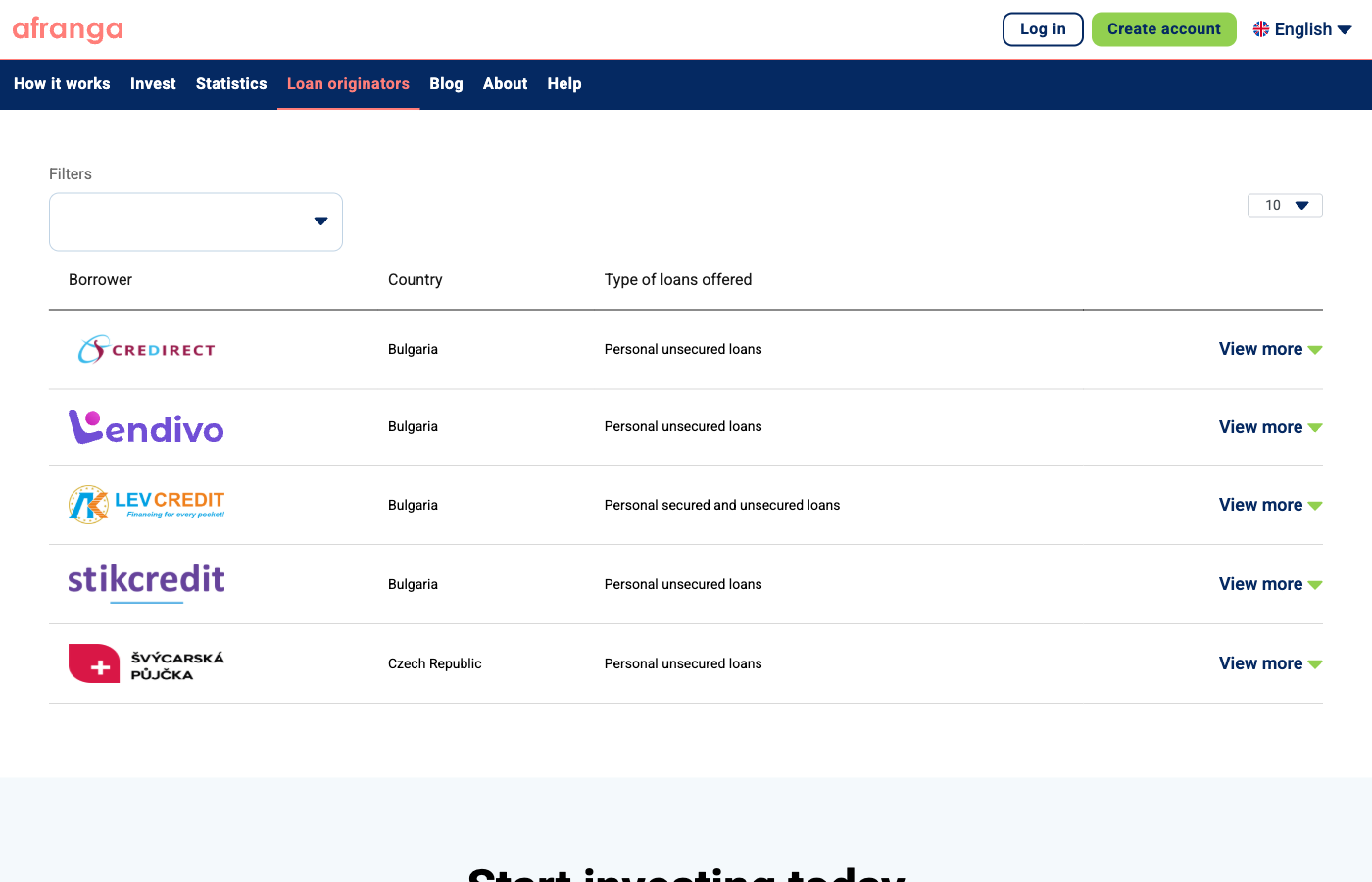

Loan Originators and Diversification

Afranga currently works with six loan originators across two countries.

Bulgaria (5 originators):

- Stikcredit: The anchor originator. Personal unsecured loans, EUR 22 million portfolio on Afranga, 12.78% average annual return. Active since 2013.

- Credirect: Personal unsecured loans (payday up to EUR 700, installment up to EUR 5,100). EUR 5.9 million portfolio, 9.86% average return. Launched in 2017, serves 30,000+ customers.

- Tiberus: Vehicle-secured loans (car leasing). EUR 5.4 million portfolio, 10.91% average return. Offers 24-hour approval.

- Lendivo: Personal unsecured consumer loans. EUR 1.7 million portfolio, 12.16% average return. Operational since April 2024. Notably, co-founded by Afranga’s CEO Svetlin Sabev.

- Lev Credit: Both secured and unsecured personal loans (up to EUR 2,500 unsecured, EUR 50,000 secured). EUR 1 million portfolio, 9.05% average return. Claims 0% impairment on its secured portfolio.

Czech Republic (1 originator):

- Swiss Funds: Short-term consumer loans (CZK 1,000 to 20,000, terms of 15 to 30 days). EUR 1.4 million portfolio, 10.49% average return.

The addition of external originators beyond Stikcredit is a positive development, though it does come with a trade-off. Afranga naturally has less oversight and control over third-party lenders compared to its parent company. Investors should do their homework on each originator before committing funds.

What You Can Invest In

Afranga offers two main investment products.

Primary Market (Manual Investing)

The primary market lets you browse available loan listings and invest manually. Each loan comes with a Key Investment Information Sheet (KIIS) that provides details about the borrower, the loan terms, and the risk profile. Minimum investment is EUR 10 per loan.

Interest rates typically range from 10% to 14%, with promotional rates occasionally reaching 16% or higher. Loan terms vary from 6 to 60 months depending on the originator.

Under the ECSP framework, the investment structure works as a corporate loan rather than a traditional P2P assignment. This means investors hold a direct claim against the loan originator, secured by a pledge on company assets. It is a different model from the assignment-based approaches you see on platforms like Mintos.

SaveSmart (Fixed-Term Product)

SaveSmart is Afranga’s fixed-term investment product, designed for investors who prefer a more hands-off approach. The rates are straightforward:

- 3 months: 8% per year

- 6 months: 10% per year

- 12 months: 12% per year

Interest is paid monthly to your Afranga wallet, with the principal returned at the end of the term. You can enable automatic reinvestment at maturity. The minimum is EUR 10.

The catch is that SaveSmart investments cannot be withdrawn before maturity, and they are not covered by any deposit guarantee scheme. This is not a bank savings account. It is an investment product with inherent risk.

Fees and Costs

This is one area where Afranga stands out: there are zero fees for investors. No account fees, no deposit fees, no withdrawal fees, no investment fees, and no secondary market fees (when available).

The platform makes its money from loan originators, who are charged up to 10% annually as a brokerage fee, plus a one-time EUR 3,000 evaluation fee. The average brokerage fee in the industry is 2 to 3%, so Afranga is charging originators significantly more than the norm. This is worth noting because it means the total cost of borrowing is higher, which could theoretically affect originator profitability over time.

What is Missing

This is where things get less impressive. As of early 2026, Afranga still lacks two features that most experienced P2P investors consider essential.

No Auto-Invest

Every loan investment must be made manually. For anyone with a meaningful portfolio, this creates unnecessary friction and cash drag. Afranga has been promising auto-invest for a while now, and it is reportedly coming in the next few months. Until it arrives, be prepared to log in regularly if you want to stay fully invested.

Limited Secondary Market

The secondary market was available on the old (pre-ECSP) version of the platform but has not yet been fully reintroduced on the new regulated platform. This means your liquidity options are limited. If you invest in a 36-month loan, you may need to hold it to maturity.

Both features are expected to launch within the first half of 2026. The platform has also mentioned a potential Go and Grow style product in the pipeline. These would be significant improvements that could change the overall assessment of the platform.

No Buyback Guarantee

Unlike many P2P platforms that offer a buyback guarantee (where the loan originator buys back defaulted loans from investors), Afranga does not provide one. Under the ECSP regulatory framework, the security model is different. Investors hold corporate loans secured by the originator’s assets rather than individual consumer loans with a buyback promise.

This is an important distinction. On the one hand, you do not have the comfort of knowing a defaulted loan will be bought back automatically. On the other hand, the regulated structure with direct claims and asset pledges arguably provides a more robust legal foundation than the buyback guarantees offered by unregulated platforms, which are only as good as the originator’s ability and willingness to honor them.

That said, Afranga has reported zero investor defaults to date. Whether this is because of excellent risk management or simply because the platform is still relatively young is an open question.

Taxes

Bulgarian loan originators withhold 10% tax on interest income at source. Depending on your country of residence and applicable double taxation agreements, you may be able to credit some or all of this against your local tax liability.

Afranga provides annual tax statements to simplify reporting for investors. If you are investing from an EU country, check the specific double taxation agreement between your country and Bulgaria, as the creditable amount may be limited. For example, German investors can only credit 5% of the Bulgarian withholding tax despite 10% being deducted.

User Experience

The platform’s interface is clean and functional, if not exactly cutting-edge. Registration involves standard KYC verification, and deposits are processed through Lemonway (which means you get an individual IBAN for your investment account).

The transition to Lemonway did cause some friction for early adopters, with automatic account creation not going smoothly for everyone. Transfers take about one business day, which is standard for SEPA payments.

Where the platform does well is transparency. Each loan listing includes detailed documentation, financial statements from the originator, and the required KIIS. You can review originator profiles with portfolio sizes, return histories, and background information before investing a single euro.

The compliance team deserves a mention here. Yonko Chuklev, who heads compliance and finance, was recognized in the Forbes 30 Under 30 Bulgaria list. For a platform of this size, the regulatory and compliance infrastructure seems well-established.

How Afranga Compares

In the European P2P lending landscape, Afranga occupies an interesting position. It is not the biggest (that would be Mintos), not the highest-yielding, and not the most feature-rich. But it does offer something that many larger platforms cannot: full ECSP regulation from day one of its current iteration, combined with returns that consistently exceed 13%.

Compared to Mintos, Afranga is far smaller and less diversified. Mintos offers 60+ loan originators across 30+ countries, while Afranga has 6 originators in 2 countries. Mintos also has auto-invest, a secondary market, and is pursuing a banking license. But Afranga’s returns have been higher, and its zero-default track record is notable.

Compared to InRento, the risk profile is completely different. InRento focuses on lower-risk buy-to-let property with first-rank mortgages, while Afranga deals primarily in consumer loans. The returns reflect this: Afranga’s 13.9% versus InRento’s 11.8%.

The closest comparison might be platforms like PeerBerry or Esketit, which also focus on consumer lending with above-average returns. Afranga’s regulatory status gives it an edge over unregulated competitors, but the lack of auto-invest and a limited secondary market hold it back.

Referral Program

Afranga runs a referral program where existing investors earn 1% of their referral’s invested funds during the first 30 days (capped at EUR 500 per referral). The referred investor must deposit and invest at least EUR 500 within 30 days of signing up. Bonus funds must remain invested for at least 3 months before withdrawal.

New investors signing up through a referral link receive a 0.5% cashback bonus on investments during their first 90 days.

Should You Invest on Afranga?

Afranga is a platform that does a few things very well. The ECSP regulation, segregated funds through Lemonway, zero defaults, and returns above 13% make a compelling case. The expansion from a single-originator model to a marketplace with six lenders shows the platform is maturing.

But there are real limitations to consider. The lack of auto-invest is a significant inconvenience. The absence of a fully functioning secondary market limits your exit options. The heavy reliance on Stikcredit and the Bulgarian market creates concentration risk. And the 10% withholding tax eats into your net returns.

I would consider Afranga as a secondary allocation in a diversified P2P portfolio rather than a primary destination. It works well alongside larger, more diversified platforms. For experienced P2P investors looking to add a regulated platform with above-average returns and who do not mind hands-on management of their investments, Afranga is worth considering.

If the auto-invest and secondary market features launch as promised in 2026, and if the platform continues its default-free trajectory while adding more originators, my assessment could shift significantly upward. For now, it is a strong performer with some growing to do.

Summary

Afranga is a Bulgarian ECSP-regulated P2P lending platform offering 13%+ returns through consumer and business loans from six originators. Zero investor defaults since inception, segregated funds via Lemonway, and a growing marketplace model make it a solid option for experienced P2P investors. The lack of auto-invest and limited secondary market functionality hold it back, along with concentration risk from its heavy reliance on parent company Stikcredit.

Pros

- ECSP-regulated by Bulgarian Financial Supervision Commission

- Zero investor defaults since platform inception

- Actual returns of 13.92% in 2025

- Segregated funds via Lemonway (French payment institution)

- No investor fees (zero account, deposit, withdrawal, or trading fees)

- Six loan originators across two countries

Cons

- No auto-invest feature (manual investing only)

- Secondary market not fully available yet

- Heavy reliance on parent company Stikcredit (concentration risk)

- 10% Bulgarian withholding tax on interest income

- Limited geographic diversification (Bulgaria and Czech Republic only)

Related

Leave a Reply