If you’re building an app, digital product, or tool — and want to offer premium features, subscriptions, or supporter perks — you’re faced with a critical decision: 👉 How do you manage payments, entitlements, and gated access without reinventing the wheel? There are more options than ever before. And while tools like Stripe and Gumroad […]

Retro Gaming on the Game Boy – Reliving the Legendary Handheld through Emulation

When Nintendo released the Game Boy in 1989, it didn’t just launch a product—it launched a cultural phenomenon. The Game Boy line would go on to sell over 200 million units worldwide and establish handheld gaming as a core part of the industry. The Game Boy was part of the wave of computers and consoles […]

The Bright Side of Sunlight: How to Enjoy the Sun Safely Every Day

Sunlight often gets a bad rap due to skin cancer warnings and anti-aging concerns, but when used wisely, daily sun exposure is one of the most natural, powerful health boosters available to us. If you’ve been avoiding the sun out of fear, it’s time to rethink your approach. Here’s how to safely enjoy the sun […]

Best Mechanics, Spray Painters and Detailers in Barcelona

Finding a trustworthy mechanic or detailer in Barcelona takes trial and error. After years of living here and owning cars that need regular attention, these are the places I’ve found and can recommend. Mechanics Dasercars — Full-service workshop in L’Hospitalet de Llobregat (Rambla de la Marina, 371) with over 20 years of experience. They cover […]

The Best Beaches in Catalonia: Hidden Gems and Coastal Charm

Catalonia, located in northeastern Spain, offers nearly 580 kilometers of Mediterranean coastline. From wild coves in the Costa Brava to the expansive golden sands of the Costa Daurada, this region is rich in variety and natural beauty. Below is a curated list of some of the most stunning beaches in Catalonia, each with its own […]

I Prefer to Be Happy Than Right

Over the years, I’ve come to realize something that’s quietly changed my life: I prefer to be happy than to be right. It didn’t happen overnight. I’ve always had a sharp mind and a strong opinion about, well, almost everything. I used to thrive on debate, feeling a surge of satisfaction when I could prove […]

How I Appealed a €900 Traffic Fine from the Catalan Transit Agency (and What You Should Know)

In early March, I received a shocking €900 fine from the Servei Català de Trànsit (Catalan Transit Agency). The charge? Failing to identify the driver of my privately owned vehicle for a previous traffic violation. But here’s the twist: I was never properly notified about that earlier request. Like many people, I didn’t find out […]

Charming Venues in Barcelona for Small Events and Birthday Parties

Planning a birthday bash or an intimate celebration in Barcelona? Whether you’re dreaming of a scenic rooftop, a cozy café terrace, or a breezy beachside setup, the city offers a rich variety of venues perfect for small gatherings. Here are some local recommendations that blend style, atmosphere, and charm — ideal for memorable get-togethers. Mirabé […]

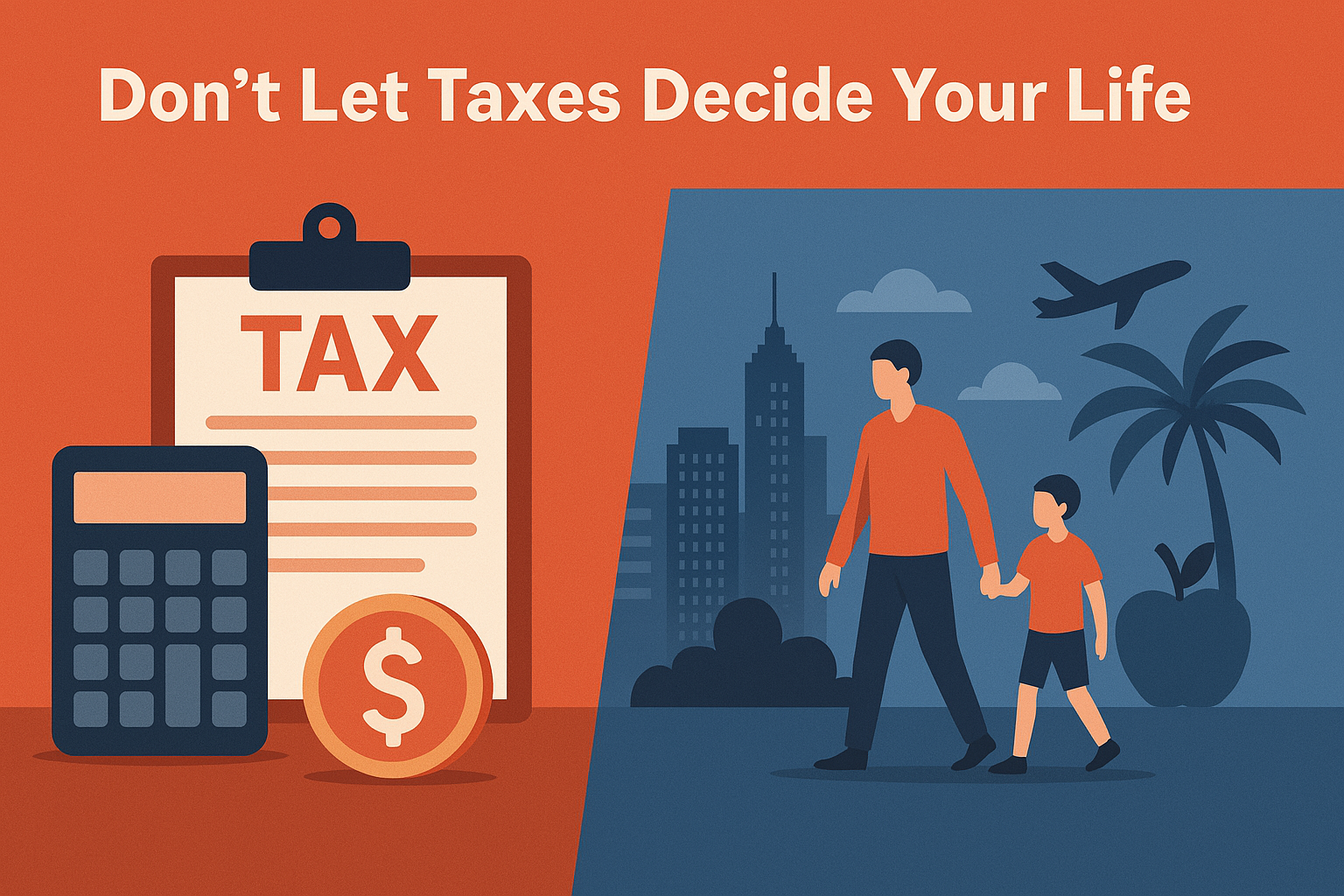

Tax vs. Life: Making the Right Move for You and Your Family

One of the biggest mistakes people make when deciding where to live is placing tax considerations above everything else. While taxation is certainly an important factor, making it the sole or primary reason for relocation—or for not moving—is often a short-sighted decision. You’re saving €20,000 a year in taxes—but what is it costing you? I’ve […]

Best Travel Insurance Options for Europeans

When planning a trip, travel insurance is something I always consider, especially if I’m venturing out of Europe. Many digital banks and fintech companies offer insurance coverage as part of their premium subscription plans, which makes things convenient if you travel frequently. In this article, I’m sharing my comparison of the travel insurance options provided […]

Is It Too Late? Love, Family, and Reinventing Your Life at 40

A Conversation on Timing, Priorities, and the Pursuit of a Meaningful Life I have many friends approaching midlife, and a good number of those who are not yet married and raising kids are grappling with the question of whether it’s too late to find the right partner, have children, and build a life that balances […]

Getting an Online Extranjeria Appointment in Spain

If you’ve ever tried to book an online appointment with extranjería (Spain’s immigration office), you know the drill. You load the government website, select your province, pick your procedure, and hit submit. Then you get the same message you got yesterday, and the day before that: “No hay citas disponibles.” No appointments available. This isn’t […]

- « Previous Page

- 1

- …

- 5

- 6

- 7

- 8

- 9

- …

- 35

- Next Page »