I’ve been investing for over a decade, across stocks, crypto, real estate, P2P lending, and more. I’ve made good calls and bad ones. What I haven’t done is sat on the sidelines, and that’s made a real difference to my financial life.

If you’re new to investing and don’t know where to start, this guide is for you. I’m going to walk you through the essentials, what investing actually is, what to do before you put any money in, and how to build a sensible first portfolio. I’ll also link to my deeper guides on each asset class so you can go further when you’re ready.

Why You Need to Invest

Money sitting in a savings account is slowly losing value. Inflation, even at a modest 3% per year, cuts your purchasing power roughly in half over 25 years. The money you save today will buy less in the future if you don’t put it to work.

Investing is how you fight back. Put your money into assets that grow over time, and you harness the power of compound growth, where your returns generate their own returns. A $10,000 investment growing at 7% annually becomes nearly $75,000 in 30 years. That same $10,000 left in a savings account at 1% becomes about $13,500.

The single biggest advantage you have as a new investor is time. The earlier you start, the more time compound growth has to work in your favor. You don’t need a lot of money to begin, you need to begin.

Before You Invest: Get the Basics Right

Investing before you’re financially ready is one of the most common mistakes beginners make. Before you put a single dollar into the market, make sure you’ve covered the fundamentals.

Build an Emergency Fund First

Keep 3 to 6 months’ worth of living expenses in cash, in a liquid savings account. This is your financial buffer for a job loss, a medical bill, or a car repair. Without it, you risk having to sell investments at the worst possible time to cover an emergency.

This isn’t optional. Build the emergency fund first, then invest.

Only Invest Money You Won’t Need for 3+ Years

Markets go up and markets go down. A stock market index might drop 30% in a bad year. If you need that money in 12 months, you’re forced to sell at a loss. If you have a 10-year horizon, you can wait for the recovery, and historically, it always comes.

A good rule of thumb: if you’ll need the money within three years, don’t invest it. Put it in a high-yield savings account or a short-term bond instead.

Understand Your Risk Tolerance

Risk tolerance is how much volatility you can stomach without making irrational decisions. Some people check their portfolio when the market drops 20% and do nothing. Others panic and sell, locking in their losses. Knowing which type you are before you invest matters.

Be honest with yourself. If you’re going to lose sleep over a 20% drawdown, build a more conservative portfolio with a lower equity allocation. There’s no shame in that, it’s far better than panic-selling at the bottom.

Ignore Tips From Friends and Social Media

Everyone has a hot stock tip, a can’t-miss crypto, or a “sure thing” they want to share. Ignore them. By the time a tip reaches you, it’s already been priced in, or it’s hype built on nothing. Make decisions based on your own research and goals, not someone else’s excitement.

Understanding Asset Classes

An asset class is a category of investment with similar characteristics and behavior. Here’s a quick overview of the main ones, each of which I cover in dedicated guides on this site.

Stocks and Index Funds

When you buy a stock, you’re buying a small ownership stake in a company. If the company grows and becomes more profitable, your stake is worth more. Individual stocks can be volatile, but over long periods, the stock market as a whole has been the best-performing asset class available to regular investors.

For most beginners, the best approach isn’t picking individual stocks. It’s buying index funds. An index fund tracks a broad market index (like the S&P 500 or the global MSCI World) and holds hundreds or thousands of companies at once. You get instant diversification at very low cost.

Stocks and index funds should form the core of most long-term portfolios. Read my stock investing guide for a full breakdown.

Cryptocurrencies

Crypto is the highest-risk asset class on this list. Bitcoin and Ethereum have produced extraordinary returns over the past decade, but they’ve also dropped 70–80% in value multiple times. This is not an asset for the faint-hearted or the short-term investor.

I hold crypto as a small portion of my portfolio, and I think it deserves a place in a diversified portfolio for the right investor, but only money you’re prepared to lose entirely. Don’t allocate more than 5–10% of your portfolio here unless you deeply understand what you own.

Get the full picture in my cryptocurrency guide.

P2P Lending

Peer-to-peer lending platforms let you act as the bank, lending money directly to individuals or businesses in exchange for interest payments. Returns can be attractive (often 8–12% annually), and the income is predictable compared to stocks.

The risk is credit risk, borrowers can default, and if a platform fails, you may lose your capital. It’s also illiquid: unlike stocks, you can’t always sell your loans instantly. I’ve used several P2P platforms over the years with mixed results.

Learn how it works in my P2P lending guide.

Real Estate

Real estate is one of the oldest wealth-building tools there is, but buying physical property isn’t accessible to most new investors, it requires large capital, involves debt, and comes with significant management overhead.

The modern alternative is real estate crowdfunding platforms or REITs (Real Estate Investment Trusts), which let you invest in property with as little as €50–100. You get exposure to rental income and property appreciation without owning a physical building.

Explore the options in my real estate guide.

Gold

Gold is a store of value and a hedge against inflation and currency crises, not a growth investment. It tends to hold its value during economic turmoil when other assets fall. A small allocation (5–10%) can reduce overall portfolio volatility, but don’t expect gold to build your wealth over time. It doesn’t produce income, it just sits there.

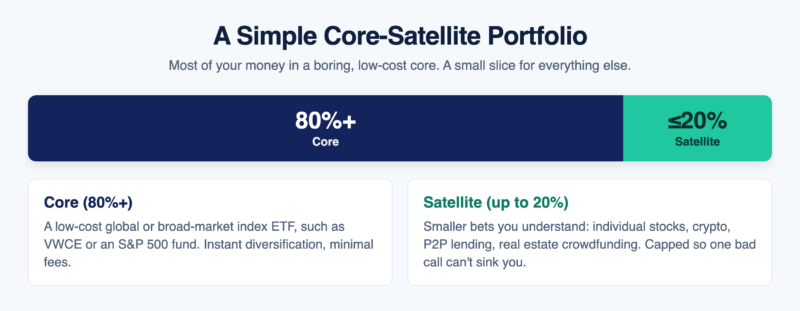

Building Your First Portfolio

You don’t need a complex strategy to invest well. In fact, keeping it simple is usually better. Here’s how I’d approach a first portfolio:

Core: Broad Market Index ETF (80%+)

The bulk of your portfolio, ideally 80% or more, should go into a low-cost global or broad market index ETF. Something like the Vanguard FTSE All-World ETF (VWCE) or a US-focused S&P 500 ETF gives you exposure to hundreds of companies across the world with a single purchase and minimal fees.

This is boring. It’s also exactly what works for most investors over the long run. Warren Buffett has publicly said the same thing repeatedly, and he knows a thing or two about investing.

Satellite: Alternatives (Up to 20%)

Once you have your core position, you can add smaller positions in individual stocks, crypto, P2P lending, real estate crowdfunding, or whatever else interests you. This satellite allocation is where you can take a bit more risk or experiment, but keep it capped at around 20% so it doesn’t sink your portfolio if one of those bets goes wrong.

Adjust for Age and Goals

A 25-year-old with a 40-year horizon can afford to be almost entirely in equities. A 55-year-old approaching retirement should gradually shift toward bonds and more stable assets to protect what they’ve built. The general rule: the older you are, the more conservative your allocation should be.

Opening a Brokerage Account

To buy stocks and ETFs, you need a brokerage account. For European investors, I recommend DEGIRO as a starting point. It has very low fees, a clean interface, and access to a wide range of global markets. It’s where I’d send someone who wants to open their first account today.

Key Investing Principles

Forget stock-picking schemes and complex trading strategies. These are the principles that actually move the needle for long-term investors.

Diversify

Don’t put all your money in one company, one sector, or one country. Spread it across different assets and geographies so that one bad outcome doesn’t wipe you out. Index funds handle a lot of this automatically.

Dollar-Cost Average

Instead of trying to invest a lump sum at the “right” time, invest a fixed amount at regular intervals, monthly, for example. This is dollar-cost averaging (DCA). When prices are high, you buy fewer units; when prices are low, you buy more. Over time, it smooths out volatility and removes the temptation to time the market.

Play the Long Game

The stock market has returned an average of roughly 7–10% per year over the long run, but that includes plenty of years with 20–30% drops. Short-term volatility is the price of long-term returns. Investors who stay invested through the downturns capture the full upside. Those who panic-sell miss the recovery.

Keep Fees Low

Investment fees are a silent killer. A 1% annual management fee might not sound like much, but over 30 years it can reduce your portfolio by 25% or more compared to a 0.1% fee index fund. Always check the expense ratio of any fund you buy. With index ETFs, you should be paying 0.05–0.25% per year. Anything above 1% is hard to justify.

Don’t Try to Time the Market

Countless studies have shown that investors who try to time the market, getting out before crashes, getting back in at the bottom, consistently underperform those who simply stay invested. The problem is that markets move in ways nobody can reliably predict. Missing just the 10 best trading days in the S&P 500 over a 20-year period cuts your returns roughly in half.

Learn From Losses

You will make bad investments. I have. Every experienced investor has. What separates good investors from bad ones isn’t avoiding all losses, it’s learning from them and not repeating the same mistakes. Keep a record of your decisions and reasoning so you can review and improve over time.

Common Beginner Mistakes

I’ve seen these patterns repeatedly, both in others and in my own early investing. Avoid them.

- Investing money they can’t afford to lose. If you need that money for rent, an upcoming expense, or you have high-interest debt, don’t invest it. Pay down the debt first. A 20% return on investments doesn’t help if you’re paying 18% interest on a credit card.

- Chasing hype and FOMO. When everyone is talking about a stock or a coin, the easy gains are usually already gone. Buying at the peak of a hype cycle, GameStop, Dogecoin, meme coins, is how beginners lose money fast.

- Checking their portfolio too often. Daily or even weekly portfolio checks don’t give you useful information, they just expose you to short-term noise that triggers emotional decisions. Check in monthly or quarterly. You’re a long-term investor, not a day trader.

- Paying high fees to fund managers. Actively managed funds charge high fees and the majority still underperform their benchmark index over 10+ year periods. The data on this is clear. Pay for index exposure, not for someone’s stock-picking instincts.

- Not doing their own research. Before you invest in anything, understand what you’re buying. What does the company do? What are the risks? What are you paying for? Investing in something you don’t understand is speculation, not investing.

- Asking strangers online for financial advice. Every person’s situation is different: income, debts, family, risk tolerance, country of residence, tax situation. Nobody online can responsibly tell you where to put your money without understanding all of that. Read widely, adopt a skeptical attitude, start small, and if you need guidance, pay a qualified financial advisor who will actually study your situation. It’s far better to invest in professional advice than to invest irresponsibly and lose money later.

Where to Go From Here

This guide gives you the foundation. Now go deeper on the areas that matter most to you. I’ve written detailed guides on each major asset class, start with the one closest to where you want to begin.

- Stock investing guide, how to buy stocks and ETFs, what to look for, and how to build an equity portfolio

- Cryptocurrency guide, how crypto works, which assets are worth understanding, and how to manage the risk

- P2P lending guide, the platforms I’ve used, the returns I’ve seen, and the risks to watch for

- Real estate guide, how to get exposure to property without buying a building

The best investment you can make right now is starting. Even a small amount, invested consistently in a low-cost index fund, will put you ahead of most people. Don’t wait for the perfect moment. It doesn’t exist.

Related

Hello everyone,

On the same topic of co-investing, I have recently discovered an app called Diversified (https://www.diversified.fi), an investment platform for rare and profitable products.

Did anyone try this service ?

Thank you,

have a great day !

I found it interesting when you talked about investment opportunities for your needs. In my opinion, everyone should think about their financial future and how to achieve their goals. I believe investing could be the next step for a business owner, and if it were the case, I’d look for professional guidance to get started. Thanks for the information on how to know where to start investing your funds.

Hi, can you advise on the online platforms / apps that allow European citizens to invest in ETF/US stock? Apart from Revolut

Check out my review of DEGIRO.

Hi Jean,

Thanks for lots of useful info!

Do you have any experience with the OnFolio platform? I’ve checked it out after reading your post, and the general idea seems great.. I’m just not sure how reputable the platform is.

Cheers,

Aleksa

Great list! On the property crowdfunding side, I also considered Rendity.

On the same crowd-investing topic for European investors, I have recently discovered an app called Konvi (https://konvi.app/), an investment platform for luxury goods. They have an amazing track record (11% appreciation per year at worst) because they are able to use their expertise when choosing assets 🙂

Welcome. Rendity is a good platform that I’ve also used myself and reviewed here.

I’m not sure how Konvi can have a track record if they haven’t even launched the private beta yet. I wouldn’t invest on that platform for the time being. It feels very experimental.

Online trading is trading in financial markets via the Internet. Previously, all trading was held in the exchange building in person or by phone.

First, you need to learn business fundamental then you should jump business. I would like to suggest you do affiliate marketing.

Hi Jean I totally agree with you, and I followed your advices about cryptocurrencies and Property crowdfunding etc… but I have recently found the best way to invest, for me, it’s “social trading”, it’s not mentioned in your article, why?

I just haven’t tried that yet Marco, could you tell us more about your experience? You’re welcome to write a guest post on the blog too if you wish.

I am using etoro and is working great, it’s 2 months I am study any details about the platform, commission, risks and warranties and I can say it’s the best way I found for investing. As you prefer I can write a guest post or just share with you all the infos I have about that.

You can now find my eToro review on this site as well.

$10k!

That aged well haha (Bitcoin price at the time).

Great article, thanks for sharing

You’re welcome Luke.

Great overview Jean – thanks for sharing! I’ve been toying with investing online but never got around to setting time to read up on the subject – mostly due to the fact that I know that you need some extra effort to really be careful what to read, and which sources to trust since you’re the entering territory where online scammers like to wait for their next target 😉

Glad you like the post Daniel. Since most of these things are relatively new, it’s normal to feel a bit hesitant about trusting your money on these platforms. On the other hand, being an early adopter gives you the opportunity to possibly make higher returns. It’s just a matter of educating yourself as much as possible by reading and asking other people for their experiences. One example of the early adopter advantage can be found in the area of loans. People who started doing loans on platforms like Bondora and Mintos just two to three years ago obtained returns of up to 20% yearly. As the platforms became better known and more investors joined, the returns went down, and now the average is only around 11%.

The platform is very fine and good