If you’re already investing on PeerBerry and wondering whether to add Lonvest to the mix — or you’re evaluating both for the first time — this comparison should help. I invest on both platforms and they share enough DNA to make a direct comparison useful: both focus on consumer loans, both offer buyback guarantees, and both are easy to use.

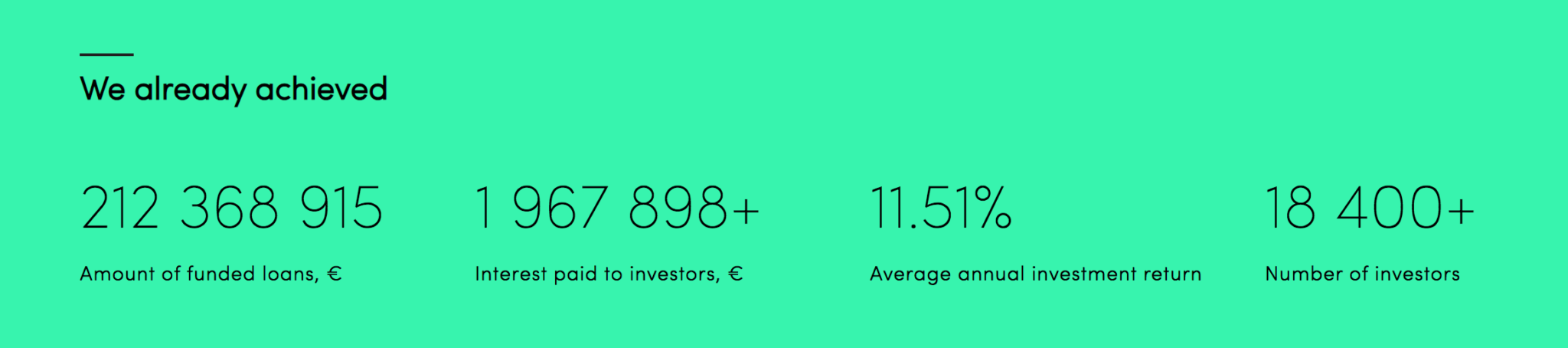

The difference is scale and maturity. PeerBerry launched in 2017 and has funded over EUR 3.24 billion in loans with 110,000+ registered investors. Lonvest launched in 2023 and is still in its growth phase. PeerBerry is the established player with a proven track record; Lonvest is the promising newcomer backed by a team with deep lending experience.

The short version: PeerBerry is the safer, more proven choice with a loyalty program that rewards larger investors. Lonvest offers slightly higher returns and geographic diversification into emerging markets that PeerBerry doesn’t cover. For most investors, PeerBerry should be the primary allocation, with Lonvest as a complementary position if you want broader platform diversification.

Quick Comparison: PeerBerry vs Lonvest

| Feature | PeerBerry | Lonvest |

|---|---|---|

| Founded | 2017 | 2023 |

| Country | Latvia | Croatia (team is Ukrainian) |

| Regulation | Not regulated (Lithuanian licensing) | Not regulated (European license in process) |

| Avg. Returns | ~11% (up to 12% with loyalty) | ~12% (up to 13%) |

| Buyback Guarantee | Yes (60 days) | Yes (buyback + group guarantee) |

| Secondary Market | No | No |

| Auto-Invest | Yes | Yes |

| Min. Investment | EUR 10 | EUR 10 |

| Total Funded | EUR 3.24 billion+ | Early stage |

| Registered Investors | 110,000+ | Growing |

| Loan Originators | 12 (Aventus Group dominant) | In-house (SpaceCrew Finance group) |

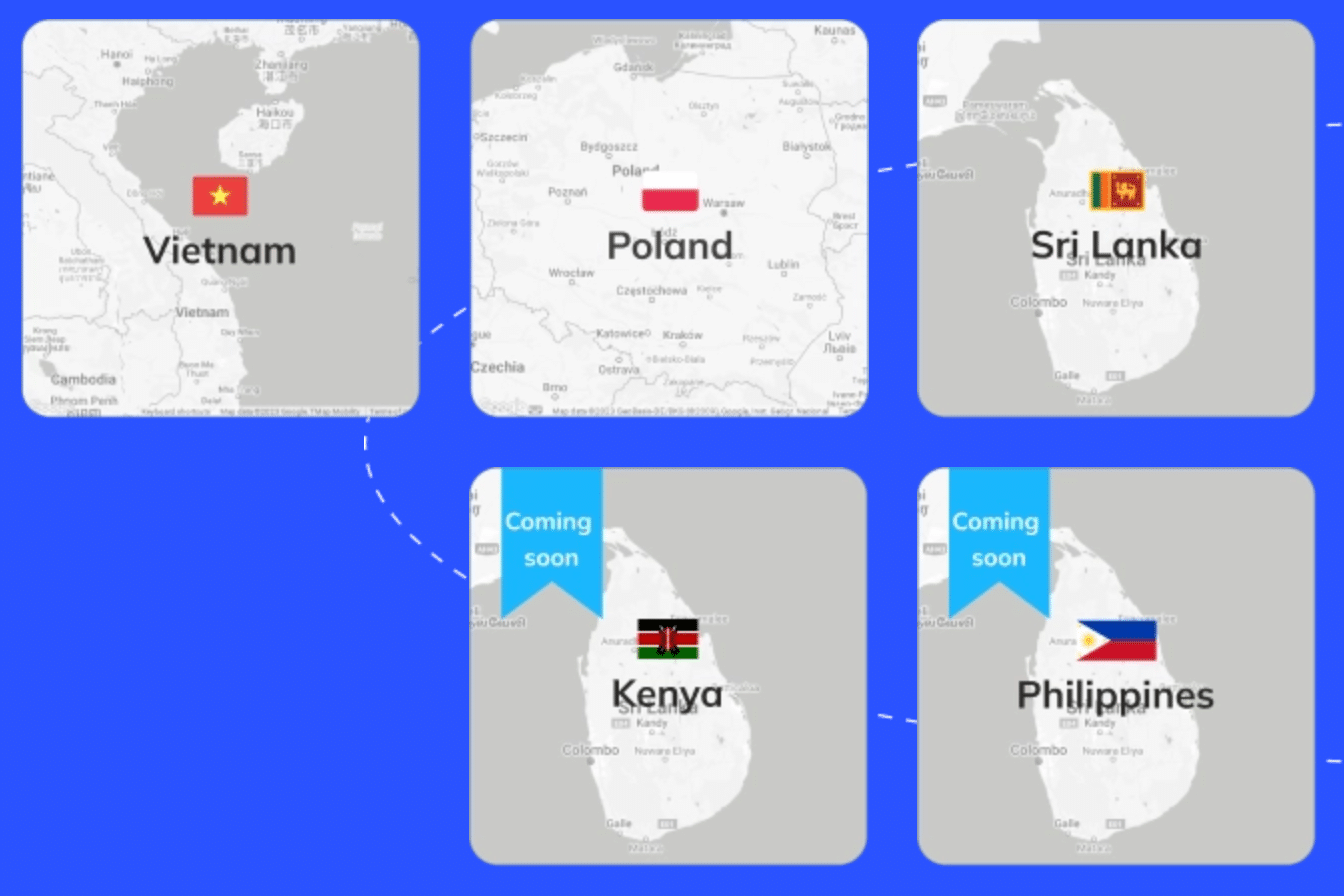

| Countries (loans) | 8 (European + Central Asian) | 4 (Sri Lanka, Poland, Philippines, Vietnam) |

| Fees | None | None |

| Loyalty Program | Yes (+0.5% to +1%) | No |

| Loan Types | Consumer (short/long-term, real estate, leasing) | Consumer loans |

Returns and Performance

The return profiles are close but not identical.

PeerBerry’s base rate averages around 11%, which already makes it one of the better-yielding platforms in Europe. Add the loyalty program — Silver (+0.5% at EUR 10,000), Gold (+0.75% at EUR 25,000), Platinum (+1% at EUR 40,000) — and you can push effective returns to 12% on a substantial portfolio. For investors who commit meaningful capital and stay long-term, the loyalty tiers make PeerBerry increasingly competitive the more you invest.

Lonvest targets an average annual yield of 12%, with some loans paying up to 13%. There’s no loyalty program, so the advertised rate is what you get regardless of portfolio size. For smaller investors (under EUR 10,000), Lonvest actually offers better base returns than PeerBerry. For larger investors hitting PeerBerry’s Platinum tier, the rates converge.

Both platforms focus on short-term loans (mostly 30-day maturities), which means your money recycles quickly and stays invested with minimal cash drag. This is a meaningful advantage over platforms with longer loan terms, where your funds can sit idle if auto-invest supply runs low.

In terms of consistency, PeerBerry has a longer track record of stable returns. The platform has operated since 2017 through COVID, the Russia-Ukraine crisis (which affected some of its loan geographies), and various market disruptions without major return interruptions. Lonvest’s two-year track record is consistent but short — we don’t yet know how the platform would perform through a serious lending crisis.

Regulation and Safety

Neither platform is regulated under MiFID II or ECSP — an important point for investors who prioritize regulatory frameworks. If regulation is your primary concern, a platform like Mintos (MiFID II) is a better option.

PeerBerry operates under Lithuanian licensing, which provides some oversight but significantly less investor protection than MiFID II. There’s no investor compensation scheme. The platform’s safety proposition rests on the financial health of its loan originators. Aventus Group (80% of loans) posted a net profit of EUR 12.6 million in 2019, and both Aventus and Gofingo (15% of loans) publish audited financial statements.

Lonvest is registered in Croatia, where there are no regulatory compliance requirements for P2P operations. The team has stated they are pursuing a European license but it hasn’t materialized yet. What Lonvest does offer is a group guarantee — since all loan originators are part of the SpaceCrew Finance group, there’s both a buyback guarantee and a group-level guarantee backing every loan. The parent group has operated lending businesses profitably for over 10 years.

On a pure regulatory comparison, PeerBerry’s Lithuanian licensing (even if limited) puts it slightly ahead of Lonvest’s unregulated Croatian registration. But honestly, neither platform offers the kind of protection that MiFID II-regulated platforms provide. You’re relying on the financial strength and integrity of the lending groups behind each platform in both cases.

The more practical safety question is: how profitable and stable are the underlying businesses? PeerBerry’s Aventus Group and Lonvest’s SpaceCrew Finance both have profitable track records, which is more meaningful for day-to-day operations than the presence or absence of a regulatory license.

Originator Model and Diversification

Both platforms use a similar model — in-house or affiliated loan originators rather than open marketplace aggregation — but the specifics differ.

PeerBerry has 12 loan originators on its marketplace, but Aventus Group accounts for 80% of all loans and Gofingo another 15%. So while you technically have 12 originators to choose from, the loan supply is heavily concentrated. This concentration is PeerBerry’s biggest structural risk. If Aventus faces financial difficulties, the platform’s entire loan pipeline is affected. The remaining originators couldn’t fill the gap.

PeerBerry’s loans cover 8 countries, including Lithuania, Poland, Czech Republic, Kazakhstan, and Moldova, among others. The geographic spread provides some diversification, even if the originator concentration doesn’t.

Lonvest takes the in-house model further. All loan originators belong to the SpaceCrew Finance group, and the platform is explicitly not an aggregator. The advantage is direct quality control — Lonvest knows exactly what’s in its loan book because the parent company originated every loan. The disadvantage is the same as PeerBerry’s: if the parent group falters, there’s no backup.

Lonvest’s geographic footprint includes Sri Lanka, Poland, the Philippines, and Vietnam — markets that don’t overlap much with PeerBerry’s European-heavy portfolio. This is actually a strong argument for using both platforms: the loan geographies are genuinely different, providing real diversification that goes beyond just spreading money across two websites.

Ease of Use and Features

Both PeerBerry and Lonvest are clean, modern platforms that don’t require a learning curve. If you’ve used any P2P platform before, you’ll be comfortable on either within minutes.

PeerBerry’s auto-invest is straightforward: set your criteria for loan originator, interest rate, term, country, and buyback preference, and the system allocates your funds automatically. The platform provides daily and weekly transaction summaries, tax statement generation, and clear loan-level detail including borrower demographics. The interface is available in English, German, and Spanish.

Lonvest’s automated investment strategies are similarly well-designed, with options starting from 30-day terms. The KYC process uses Veriff and takes minutes. The platform is available in English, Spanish, and German. The team’s tech background shows in the polish of the user experience — everything works smoothly and the design is contemporary.

Neither platform has a secondary market — you invest and hold until maturity. Since both focus on short-term (30-day) loans, your capital recycles quickly, making this less of a constraint than on platforms with longer terms.

PeerBerry has a slight edge in reporting and analytics, reflecting years of iteration. Lonvest is still building out these tools and has a secondary market on its roadmap.

Track Record: Established vs New

This is where PeerBerry has its clearest advantage.

PeerBerry has been operating since 2017 — eight years through a pandemic, a European war, rising interest rates, and intense competition. EUR 3.24 billion+ in funded loans, 110,000+ investors, no major default events. Aventus Group and Gofingo publish audited financial statements showing consistent profitability. That track record is hard to argue with.

Lonvest launched in 2023. Two years is short, and no P2P platform can be fully evaluated until it’s weathered a downturn. But the SpaceCrew Finance group has been running lending operations profitably for over 10 years. I’ve met the founder, Roman Katerynchyk, and was impressed by his depth on both the technology and finance sides. The team is transparent about their backgrounds, with LinkedIn profiles linked from the platform.

For risk-averse investors, PeerBerry’s history is the deciding factor. For those comfortable looking beyond platform age to team experience, Lonvest’s parent group credentials offer meaningful reassurance.

Fees and Costs

Neither platform charges fees. Zero investment fees, zero withdrawal fees, zero management fees on both PeerBerry and Lonvest. This is a genuine advantage both share compared to platforms like Mintos (0.29% annual fee on Custom Portfolios) or Bondora (EUR 1 withdrawal fee on Go & Grow).

Where PeerBerry adds extra value is the loyalty program. After 90 days of membership, investors with EUR 10,000+ get an additional 0.5-1% on their returns. This is effectively a negative fee — the platform pays you more for investing more. Over time, this compounds meaningfully. An investor with EUR 40,000 on PeerBerry earns an extra EUR 400 per year from the Platinum bonus alone.

Lonvest doesn’t have a loyalty program, so the advertised ~12% rate is the rate you get regardless of portfolio size or tenure. For smaller investors, this is a non-issue. For investors allocating EUR 25,000+, PeerBerry’s loyalty tiers represent a real economic advantage.

Who Should Choose Which?

Choose PeerBerry if you:

- Value a proven track record (8 years, EUR 3.24B+ funded, 110,000+ investors)

- Are investing EUR 10,000+ and want to benefit from the loyalty program

- Prefer a larger, more established platform with more loan originators (12)

- Want more loan type variety (short-term, long-term, real estate, leasing)

- Want a platform that has weathered multiple market cycles

Choose Lonvest if you:

- Want slightly higher base returns (~12% vs ~11%) without needing a large portfolio

- Like the in-house originator model with group guarantee

- Want geographic diversification into emerging markets (Sri Lanka, Philippines, Vietnam)

- Value the direct quality control of a vertically integrated lending group

- Are comfortable with a newer platform backed by an experienced team

Use both if: You want genuine geographic diversification within your P2P allocation. PeerBerry’s loans are predominantly European (Lithuania, Poland, Czech Republic, etc.), while Lonvest covers emerging markets (Sri Lanka, Philippines, Vietnam, plus Poland). Using both gives you exposure to different economic regions, borrower profiles, and lending markets. This is what I do — spreading across multiple European P2P platforms to reduce platform-level risk while accessing different markets.

Verdict

PeerBerry is the stronger overall choice. Eight years of operation, EUR 3.24 billion+ in funded loans, consistent returns, zero fees, and a loyalty program that rewards committed investors. If I could only use one of these two platforms, PeerBerry would be the pick.

But Lonvest isn’t just a weaker alternative — it’s a genuinely complementary platform. The emerging market loan geography, the in-house originator model with group guarantee, the higher base returns for smaller investors, and the experienced team behind it all make it worth a position alongside PeerBerry rather than instead of it.

My approach: PeerBerry as a core P2P holding, Lonvest as a diversification play. The two platforms don’t overlap much in geography, so you get real risk reduction by using both.

For more detail, read my full PeerBerry review and Lonvest review. Also check out my guide to P2P lending.

Frequently Asked Questions

Is PeerBerry safer than Lonvest?

PeerBerry has a longer track record (since 2017) and operates under Lithuanian licensing. Lonvest launched in 2023 and is registered in Croatia without specific P2P regulation. However, Lonvest’s parent group (SpaceCrew Finance) has 10+ years of profitable lending history and offers a group guarantee in addition to the standard buyback. PeerBerry is the safer bet based on platform history; Lonvest’s team experience provides meaningful, if less visible, reassurance.

Which has better returns — PeerBerry or Lonvest?

Lonvest offers higher base returns (~12% vs ~11%). However, PeerBerry’s loyalty program adds up to 1% for investors with EUR 40,000+, bringing effective returns to ~12%. For smaller portfolios (under EUR 10,000), Lonvest has better returns. For larger portfolios at PeerBerry’s Platinum tier, the rates are comparable.

Do either PeerBerry or Lonvest have a secondary market?

Neither platform offers a secondary market. You hold loans until maturity. Since both platforms focus on short-term loans (typically 30-day maturities), your capital recycles quickly. Lonvest has indicated a secondary market is on its development roadmap.

Should I use both PeerBerry and Lonvest?

Yes, if you want geographic diversification. PeerBerry’s loans are primarily European (Lithuania, Poland, Czech Republic), while Lonvest covers emerging markets (Sri Lanka, Philippines, Vietnam, Poland). Using both provides exposure to different economic regions and borrower profiles, which is good practice in P2P investing.

Is Lonvest too new to invest in?

Lonvest the platform launched in 2023, so it has limited history. However, the SpaceCrew Finance group operating the lending side has 10+ years of experience across multiple countries. The team is experienced and the lending operations are proven, even if the investor-facing platform is newer. Start with a smaller allocation and increase as the platform builds its track record.

What is PeerBerry’s loyalty program?

After 90 days of membership, PeerBerry adds a return bonus based on portfolio size: Silver (EUR 10,000+) adds 0.5%, Gold (EUR 25,000+) adds 0.75%, and Platinum (EUR 40,000+) adds 1% to your interest rate on all new investments. An investor earning 11% at the Platinum level effectively earns 12%. Lonvest does not have a loyalty program.

Open a PeerBerry account Open a Lonvest account

Related

Leave a Reply