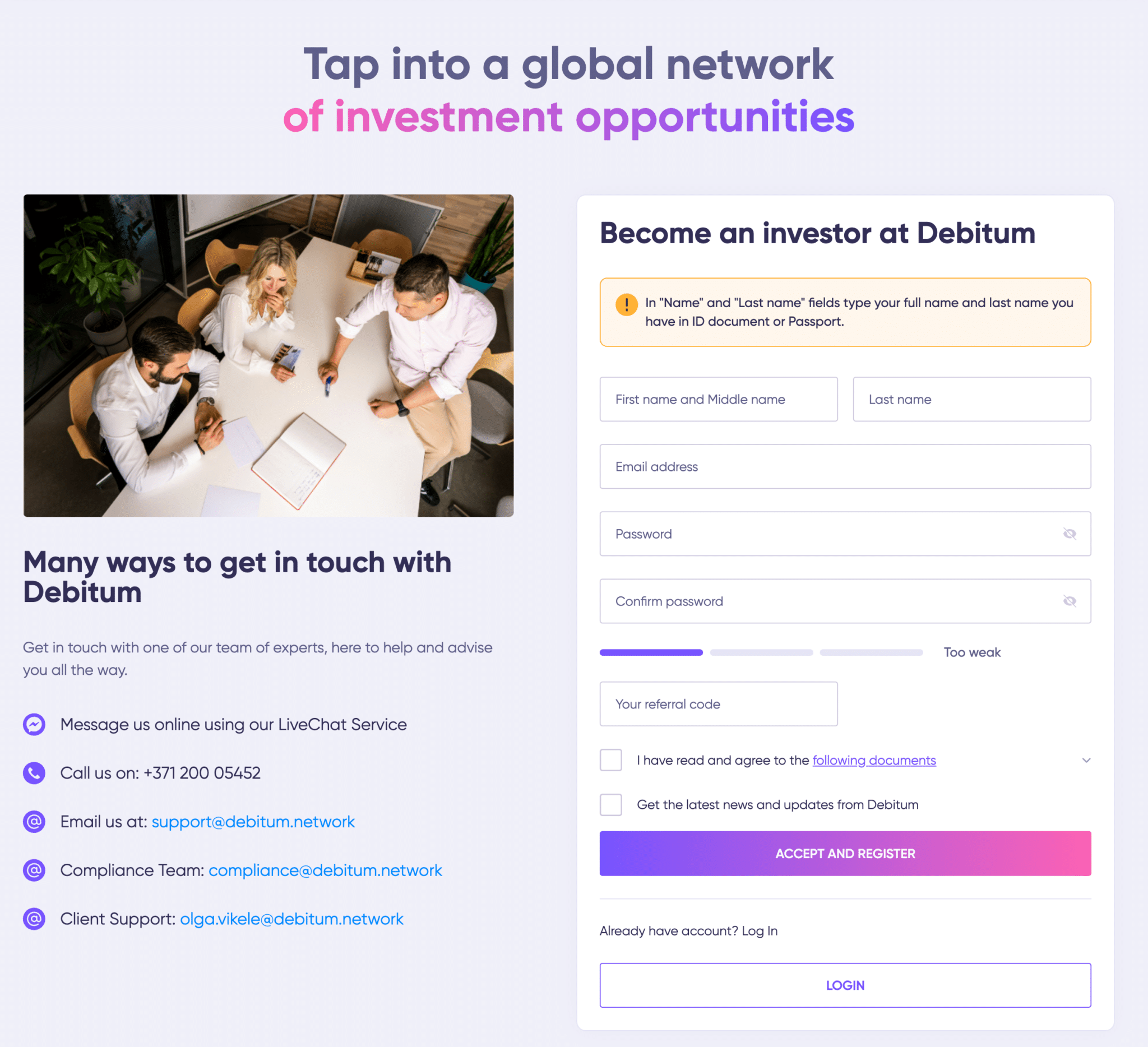

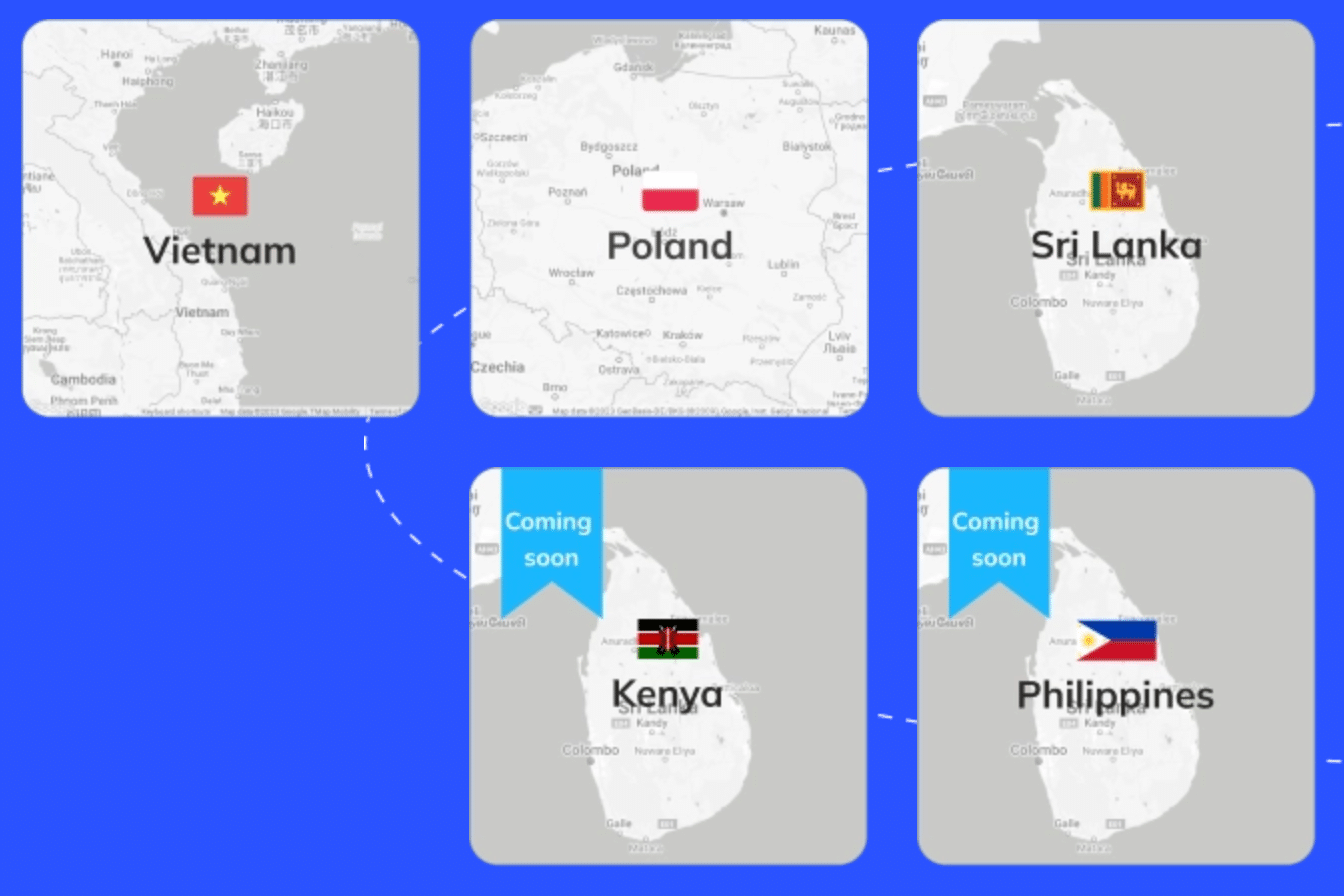

Debitum Investments (formerly Debitum Network, rebranded in February 2024) is one of the most established platforms in the Peer-to-Peer (P2P) lending arena, forging a conduit between investors and borrowers to channel capital towards businesses. Since its inception in 2018, operating from the vibrant city of Riga, Latvia, Debitum has made significant strides. The platform has […]

Three Days in Madrid – What to See & Do

Madrid is one of my favorite cities in the world, and I always love to visit and explore it from different angles, mostly depending on whom I’m visiting with. Here are some ideas for a 3-day visit. First of all, how to get to Madrid. If you’re in Barcelona or one of the major Spanish […]

Lonvest Review 2026 – One of the Best P2P Platforms

Invest with Lonvest When investing in European P2P lending platforms, it’s important to maintain a healthy level of diversification across said platforms, but also to always be on the lookout for new (and perhaps better) platforms to allocate to. Lonvest is one platform that fits the bill, having launched in 2023 in Croatia. The platform […]

Incorporating in Hungary: A Comprehensive Analysis

With its strategic location in Central Europe, robust economy, and attractive tax environment, Hungary has become an increasingly popular choice for business incorporation. However, like any business decision, setting up a company in Hungary comes with its unique set of challenges and opportunities. This article offers an in-depth exploration of the process, pros and cons, […]

The Netherlands: A Key Component in Global Tax Strategies

The Netherlands, with its robust economy, favorable business environment, and strategic location in the heart of Europe, has long been a preferred choice for multinational corporations. A key part of this appeal is the Netherlands’ tax framework, which offers a number of advantages for businesses, particularly those engaged in international operations. In this article, we’ll […]

Ireland – Should You Incorporate There?

With its strong economic performance, low corporate tax rates, and favorable business environment, Ireland has emerged as a leading destination for entrepreneurs looking to incorporate their businesses. But like any decision of this magnitude, incorporating a company in Ireland has both pros and cons. This article will provide an in-depth look at what it means […]

Incorporating a Company in Bulgaria: The Pros, Cons, and Grey Areas

When it comes to starting a business, the geographical location and legal jurisdiction can significantly influence the success or failure of the venture. Among numerous international options, Bulgaria has emerged as an attractive destination for business incorporation due to its numerous advantages. However, the business landscape isn’t without its challenges and grey areas. Why Incorporate […]

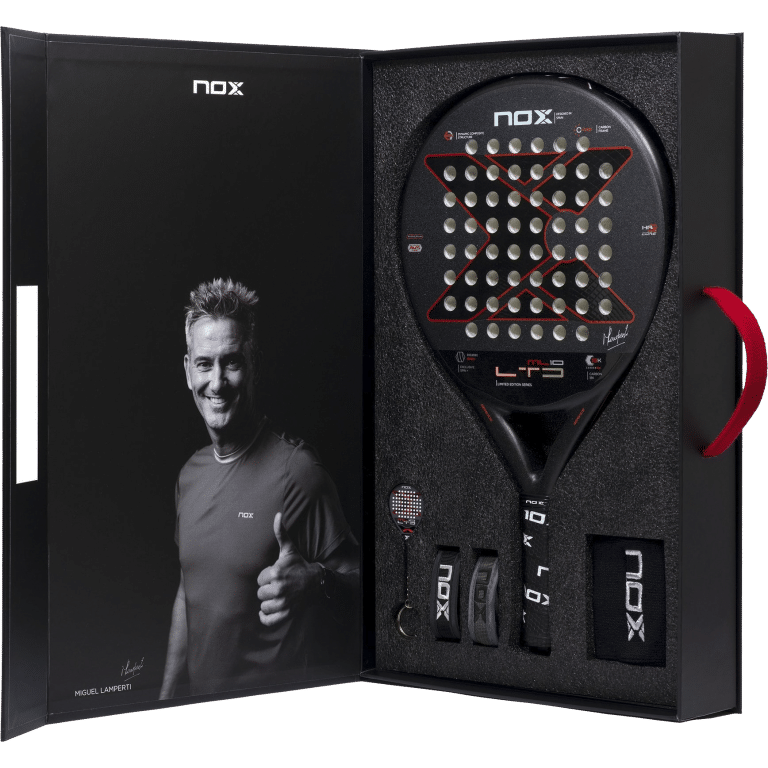

How Padel Rackets are Manufactured

Padel is a racquet sport that combines elements of tennis, squash, and badminton, swiftly rising in popularity around the globe. At its heart, padel is defined by its unique, perforated racket design. This article aims to delve into the intricate process behind the manufacture of padel rackets, shedding light on the materials, techniques, and quality […]

Padel Rackets – Made in Spain VS Made in Asia

Padel, a sport that originated in Mexico, has become hugely popular in Spain, which is often considered the epicenter of the sport. The Spanish take on the sport’s equipment, particularly the padel racket, is regarded as some of the finest in the world. On the other hand, Asia, known for its mass production capabilities, has […]

Fashion Tips for Men

In the fast-paced and ever-evolving world of fashion, it’s easy for men to feel overwhelmed. In the Good Life Collective, we believe that dressing well and having a good fashion sense is an important element both in social environments and for self-esteem. That’s why in one of our regular webinars we focused specifically on this […]

Mass Market Padel Rackets VS Professional Padel Rackets

The question of whether the padel rackets sold to the mass market are the same as those used by the sponsored professional players is one that has been asked in many sports. The short answer is: not always. Professional athletes often have specific needs and preferences that can be quite distinct from those of amateur […]

Backing Up Your Data with Synology

Losing data is one of my biggest fears, so I try to make sure this never happens by using sensible backup solutions for all my data. One of the most important components of my backup strategy is the Synology Diskstation. In this post, I’ll talk about some options and my suggested setup. The assumption here […]

- « Previous Page

- 1

- …

- 8

- 9

- 10

- 11

- 12

- …

- 36

- Next Page »