Contents

Profitus is a Lithuanian real estate crowdfunding platform that connects investors with property-backed lending opportunities. Founded in August 2018 and supervised by the Bank of Lithuania, it holds an ECSP (European Crowdfunding Service Provider) license — making it one of the more established regulated platforms in the European real estate crowdfunding space.

The platform has funded over €354 million across more than 2,000 real estate projects, with approximately 13,800 registered investors. Advertised returns sit around 10-11% annually, though actual delivered returns are closer to 8-9% after accounting for delays and defaults. All investments are secured by first-rank mortgages on the underlying property.

Profitus at a Glance

| Founded | 2018 |

| Country | Lithuania |

| Regulation | ECSP licensed (Bank of Lithuania) |

| Average Returns | 10-11% advertised (8-9% actual) |

| Collateral | First-rank mortgage on all investments |

| Max LTV | 70% (average 65-67%) |

| Secondary Market | Suspended since May 2023 |

| Auto-Invest | Yes |

| Min. Investment | EUR 100 |

| Asset Class | Real estate (residential, commercial, development) |

| Total Funded | EUR 354 million+ |

| Withholding Tax | 15% for non-Lithuanian investors |

How Profitus Works

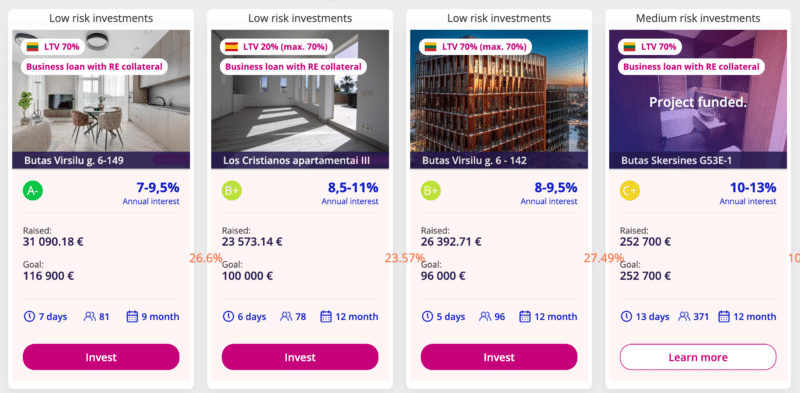

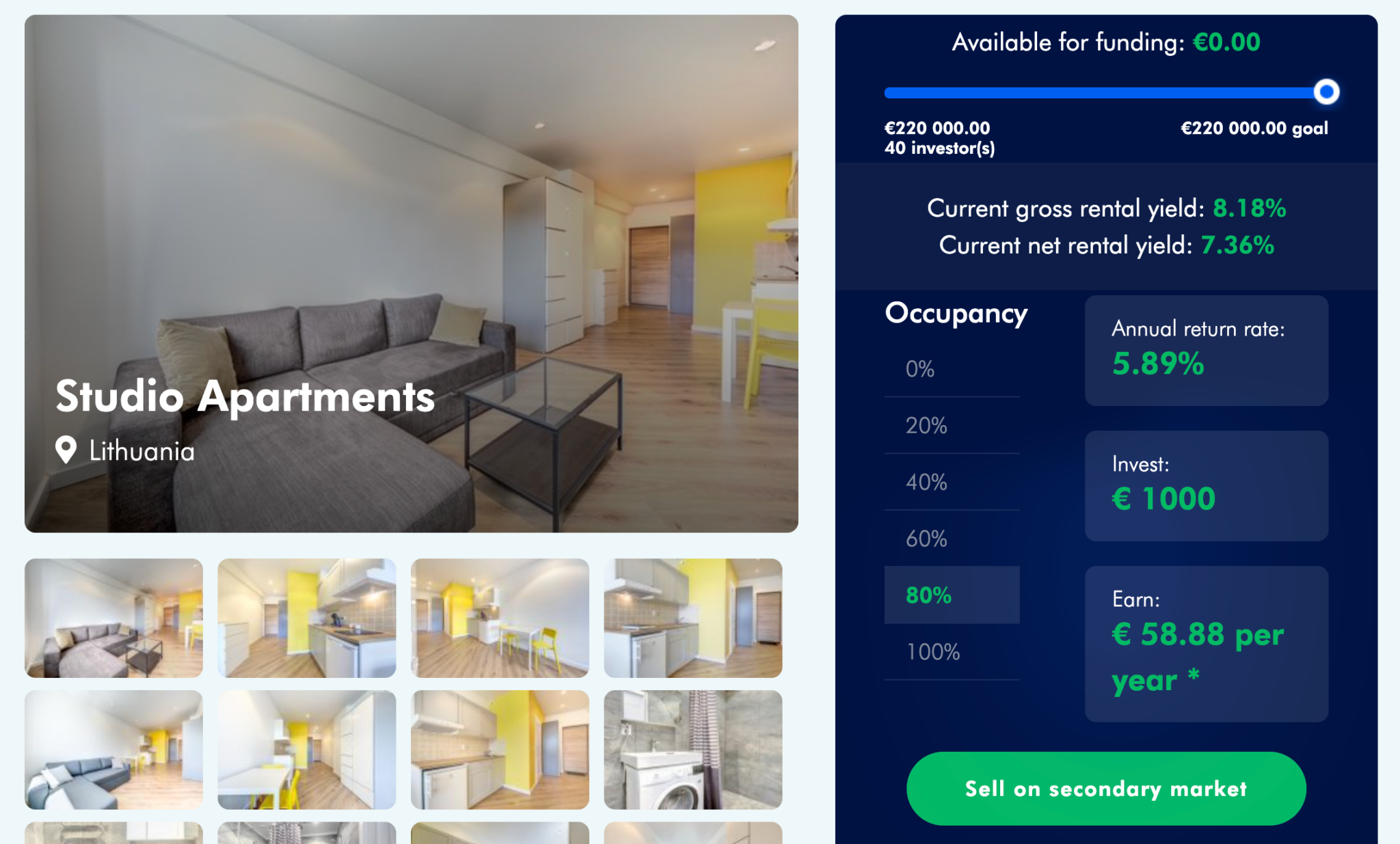

Investments start at €100. Each project is secured by pledging real estate as collateral, and the platform maintains a maximum LTV (loan-to-value) ratio of 70%, with the average LTV currently around 65-67%. The lower the LTV, the more collateral protection you have as an investor.

Profitus accepts investors from across the EU and has been expanding its project base beyond Lithuania into Latvia, Estonia, and Spain.

Key platform stats:

- Advertised annual interest: 10-11% (actual delivered closer to 8-9%)

- All investments secured by first-rank mortgage

- Maximum LTV: 70%

- Average loan term: approximately 11 months

- ECSP licensed, supervised by the Bank of Lithuania

- Approximately €98 million funded in the last 12 months

- 10.2% of portfolio currently in recovery — up significantly from the historical 2-3%

- Secondary market suspended since May 2023 — limited liquidity

Types of Investments Available

Profitus offers several categories of real estate investment:

- Residential property: Apartments, houses, and townhouses — generating returns through interest on loans secured against the property.

- Commercial property: Office buildings, retail spaces, and warehouses with business tenants.

- Property development: Loans to developers for new construction, renovation, or expansion projects. These are typically higher-risk but also higher-return.

- Real estate-backed loans: General-purpose loans secured by property collateral.

The vast majority of projects are based in Lithuania, which provides concentrated exposure to the Lithuanian real estate market. The platform has been gradually expanding into other Baltic and European markets.

Risk Assessment and Due Diligence

Profitus assigns each project a risk rating from A+ to F based on their internal assessment algorithm. The vetting process involves:

- Initial evaluation by a Project Manager, including review of financial statements, business plans, company data, and independent property valuations.

- Financing protocol formed using data from local registers — credit history, shareholder checks, property registration, and existing restrictions.

- Credit committee evaluation using their risk assessment algorithm, including a cross-check of property values against comparable market transactions.

- Final decision by the credit committee on whether to approve financing.

This process is more thorough than what some P2P platforms offer, though the rapid volume growth (800+ projects funded) does raise questions about how much individual attention each project receives.

The Withholding Tax Issue

This is the most significant consideration for non-Lithuanian investors. Profitus withholds 15% tax on interest income for non-residents, as required by Lithuanian tax law. This is notably higher than the 5% withholding tax applied by Latvian platforms like Mintos, TWINO, and ViaInvest.

If your country has a Double Taxation Avoidance Treaty with Lithuania, you can apply for a reduced rate — typically 10%, or 0% for investors in Latvia or the UAE. The withheld tax can also usually be credited against your domestic tax liability, so it’s not necessarily a net cost — but it does reduce your immediate cash flow and adds administrative complexity.

For a full breakdown of how P2P taxation works across Europe, see my P2P lending tax guide.

Growing Concerns: Defaults and Financial Health

There are two significant issues to flag as of early 2026.

Rising default rates: Profitus’s recovery portfolio has grown sharply — approximately 10.2% of active loans are now in recovery, up from a historical average of 2-3%. BBB-rated projects specifically carry an 18% default rate over 60 months. No investors have lost capital yet thanks to the mortgage collateral, but recovery processes take time and there’s no guarantee every property sale will cover the outstanding amount. This deterioration is the primary reason the platform’s community ranking dropped from 2nd place in 2024 to 17th in 2025.

The company’s financial health: Profitus moved into negative equity in FY2024, with equity dropping from €439K to -€123K. Net losses grew 40% to €562K despite 39% revenue growth (to €3.29M). Current assets dropped significantly.

This is important to understand: even when the underlying real estate loans are performing well and secured by collateral, the platform company itself needs to remain financially viable to service investors, manage loan administration, and handle any defaults or recoveries. A platform in negative equity isn’t immediately dangerous — many startups operate this way temporarily — but it’s something to monitor.

Secondary market suspended: Profitus suspended its secondary market in May 2023. This means your capital is locked until each loan matures — there’s no way to exit early. For a platform with average 11-month terms, this is a meaningful liquidity constraint.

The company’s financial statements are not publicly shared with investors, which limits transparency on all these fronts.

Team Behind Profitus

Profitus was founded by Viktorija Cijunskyte, who is also co-founder of asset management company Victory Funds and real estate development company CITUS. The about page shows a reasonable-sized team with LinkedIn profiles linked.

Alternatives to Profitus

If you’re interested in real estate crowdfunding in Europe, the main alternatives include:

- EstateGuru — Multi-country European real estate lending, also property-backed. However, EstateGuru has been experiencing severe problems since 2024, with over 60% of its portfolio now in recovery. Profitus is currently the more reliable option despite its own issues.

- InRento — Lithuanian rental property platform focused on buy-to-let investments with rental income distribution.

- Reinvest24 — Estonian-based platform offering both rental income and development projects across Europe.

For consumer loan P2P lending (different risk profile but often higher liquidity), see my best European P2P lending platforms ranking.

Frequently Asked Questions

Is Profitus safe?

Profitus holds an ECSP license from the Bank of Lithuania and all investments are secured by first-rank mortgages with a maximum LTV of 70%. These are strong protections. However, the default rate has risen to 10.2% in recovery, the company itself has negative equity, and the secondary market has been suspended since May 2023. No investor has lost capital yet, but the trend requires careful monitoring.

What returns does Profitus offer?

Profitus advertises 10-11% annual returns, but actual delivered returns are closer to 8-9% after accounting for late payments and defaults. A 15% withholding tax applies for non-Lithuanian investors, reducing net returns further.

How does the 15% withholding tax work?

Lithuania requires a 15% withholding tax on interest income paid to non-resident investors. If your country has a Double Taxation Agreement with Lithuania, you may qualify for a reduced rate (typically 10%). The withheld tax can usually be credited against your domestic tax liability.

How does Profitus compare to EstateGuru?

Both offer real estate-backed investments, but their current situations differ significantly. Profitus has a solid ECSP license and €354M+ funded, with 10.2% in recovery. EstateGuru has been experiencing major problems since 2024, with over 60% of its portfolio in recovery. Profitus is currently the more reliable option, though its own default trajectory deserves attention.

What happens if a borrower defaults on Profitus?

All investments are secured by first-rank mortgages on real property. If a borrower defaults, Profitus initiates a recovery process that may include selling the underlying property. The average LTV of 65-67% provides a meaningful buffer, but recovery can take time.

My Opinion on Profitus

Profitus has genuine strengths: ECSP regulation, real estate collateral on all loans, a reasonable LTV policy, and a growing track record with over €354 million funded. The Lithuanian real estate market has been one of the stronger performers in the Baltics, and the platform’s expansion into other European markets adds diversification.

The downsides are significant and have been growing. The default rate climbing to 10.2% in recovery is the most concerning trend — this is a material deterioration from the platform’s historical performance. The secondary market suspension since May 2023 removes your ability to exit positions early. The 15% Lithuanian withholding tax is a significant drag for non-Lithuanian investors compared to Latvian alternatives at 5%. And the company’s own financial health — negative equity and growing losses despite revenue growth — needs watching.

Actual returns of 8-9% (after accounting for late payments and defaults) are respectable for a mortgage-backed platform, but they’re not the 10-11% headline rate. Factor in the 15% withholding tax for non-residents, and your net return drops further.

Profitus makes the most sense for:

- Lithuanian residents — no withholding tax disadvantage, access to local market knowledge

- UAE residents — 0% withholding under the DTA treaty

- Investors specifically wanting Lithuanian real estate exposure — Profitus is one of the best options for this specific niche

For investors outside these categories, the withholding tax makes platforms in Latvia or Estonia more competitive on a net-return basis, even if Profitus’s gross returns look attractive.

Summary

Profitus offers an accessible and user-friendly platform for investors looking to diversify their portfolios with real estate investments. However, it is essential to consider the illiquidity, market risks, and potential platform risks associated with this type of investment.

The biggest attraction is the quantity of Lithuanian real estate projects offered. Ideal for Lithuanian residents, but for the rest, the 15% withholding tax is a bit problematic. Great platform if you want to specifically invest in Lithuania.

Pros

- Good market: Lithuania is a rising star in Europe.

- Diversification: Profitus allows investors to diversify their investment portfolio by investing in different types of real estate projects, reducing overall investment risk.

- Accessibility: The platform offers a low minimum investment amount, making it accessible to a wide range of investors.

- Passive income: Investors can earn passive income through rental income or interest payments from property developers.

- Expertise: Profitus conducts due diligence on the projects, ensuring that they meet certain criteria before being listed on the platform. This can provide a level of assurance for investors.

- User-friendly platform: Profitus has an easy-to-use interface, which makes it simple for users to navigate and manage their investments.

Cons

- Withholding tax: 15% tax retention

- Illiquidity: Real estate investments tend to be illiquid, meaning that it can be challenging to sell or withdraw your investment quickly, especially in the case of economic downturns or project delays.

- Market risk: Real estate markets can be volatile, and the value of the properties in the portfolio may fluctuate, impacting the returns on investments.

- Limited secondary market: Profitus currently does not have a well-established secondary market, which means that investors may have difficulty selling their investments before the end of the investment term.

- Platform risk: As with any crowdfunding platform, there is a risk that Profitus may face financial difficulties, operational issues, or even closure, which could impact the management of investors’ funds.

- No guarantee on returns: The returns on real estate investments are not guaranteed, and investors may not receive the expected returns due to factors such as market conditions or project delays.

Related

Jean, tal y como está el mercado comienza a dar algo más que respeto que, en mercados bastante estrechos como son los inmobiliarios de los países bálticos, surjan cada mes plataformas diferentes con objetivos demasiado elevados de rentabilidad.

Muy buen comentario con todos los datos concretos a esta plataforma.

Ánimo con tu proyecto!!!

Unfortunately they keep withholding tax that makes the platform unattractive.

Agreed, that is a major minus point for Profitus.