This is a sponsored review. Afranga has paid for this placement, and some links are affiliate links, meaning I may be compensated if you sign up …

Blockpit Review 2026 – Crypto Tax Reports With Prefilled European Forms

TL;DR: Blockpit is an Austrian crypto tax platform that reports in over 100 countries and goes properly deep in ten of them, producing prefilled national tax …

How to Pay International Remote Workers from Europe

Hiring remote workers outside Europe is straightforward. Paying them reliably, cheaply, and legally is where things get complicated. I’ve been running distributed teams from Europe for …

The Science Behind Sauna: Why I Use It After Every Workout

I use the sauna at my fitness club almost every day, usually right after a workout. It started as something I did because it felt good …

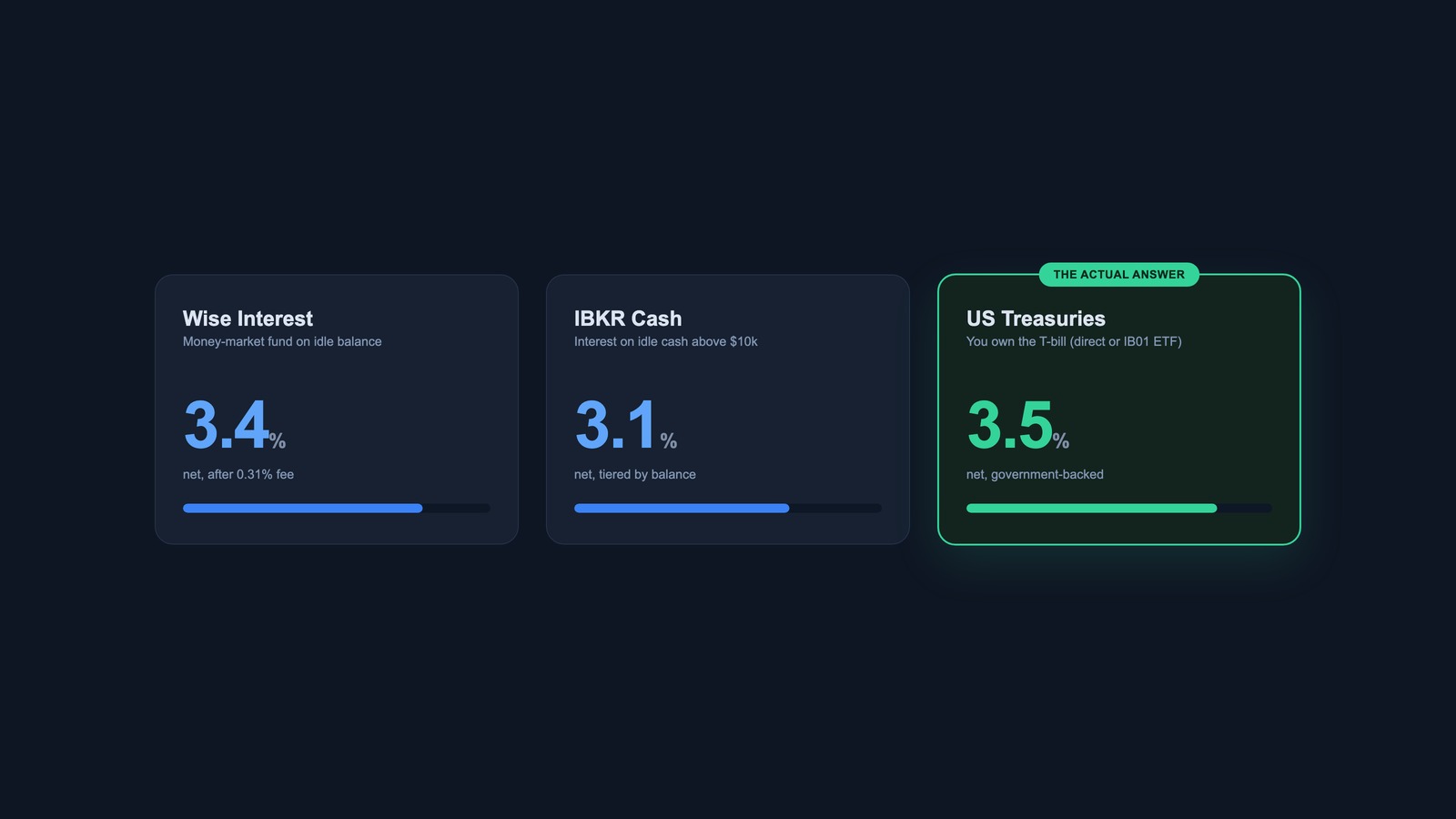

Where to Park USD for Yield: Wise vs Interactive Brokers vs Treasuries

If you earn or hold US dollars in Europe, you’ve probably noticed they tend to sit idle. A client pays you in USD, it lands in …

The Best Bitcoin and Crypto Interest Accounts in 2026

Did you know you can earn interest on the Bitcoin, Ethereum, and other crypto you already hold? The old criticism that crypto is a dead asset …

TokenTax Review 2026: Full-Service Crypto Tax Filing

TokenTax sits in a different part of the crypto tax market from most of the tools I cover. It is both a software platform and a …

CoinTracking vs Koinly 2026 – Which Crypto Tax Tool Wins?

TL;DR: CoinTracking and Koinly are the two heavyweights of crypto tax software. Choose CoinTracking if you want the deepest analytics, the widest range of transaction types, …

Best Crypto Tax Software 2026 – Top 5 Compared

TL;DR: After years of using these tools for my own crypto taxes, six stand out in 2026. CoinTracking is my Best Overall pick: the deepest, longest-running …

Divly Review 2026 – Crypto Tax Software Built for Europe

TL;DR: Divly is a European crypto tax tool built around one thing most competitors treat as an afterthought: your country’s actual tax forms. It generates the …

CoinLedger Review 2026 – Crypto Tax Reports Made Simple

TL;DR: CoinLedger (formerly CryptoTrader.Tax) is a crypto tax tool built around one of the cleanest user experiences in the category. It connects to 1,000+ exchanges, wallets, …

How to Prepare Your Crypto Taxes in Spain (2026)

TL;DR: If you’re tax-resident in Spain, your crypto gains are taxed under the savings income base at 19% to 28%, with no discount for holding long …

- 1

- 2

- 3

- …

- 30

- Next Page »