If you’re a European investor looking for a low-cost broker, your shortlist probably starts and ends with two names: DEGIRO and Scalable Capital. These are the two brokers that come up in nearly every conversation about affordable investing in Europe — and for good reason. Both offer access to thousands of stocks, ETFs, and other […]

Binance vs Kraken — Which Is Better in 2026?

Binance and Kraken sit at opposite ends of the crypto exchange spectrum. Binance is the biggest exchange in the world by a wide margin — 40% of global spot volume, 250+ million users, 500+ coins. Kraken is the trusted veteran — never hacked in 14 years, fully MiCA-licensed across Europe, and now building toward an […]

Best Luxury Real Estate Agencies and Developers in Spain (2026)

TL;DR: Spain is now one of Europe’s top three markets for luxury real estate, with prime property prices expected to rise 6-10% in 2026. International buyers account for over 70% of luxury transactions. Below you’ll find my curated list of the best luxury real estate agencies, portals, architects, and developers across Spain — with a […]

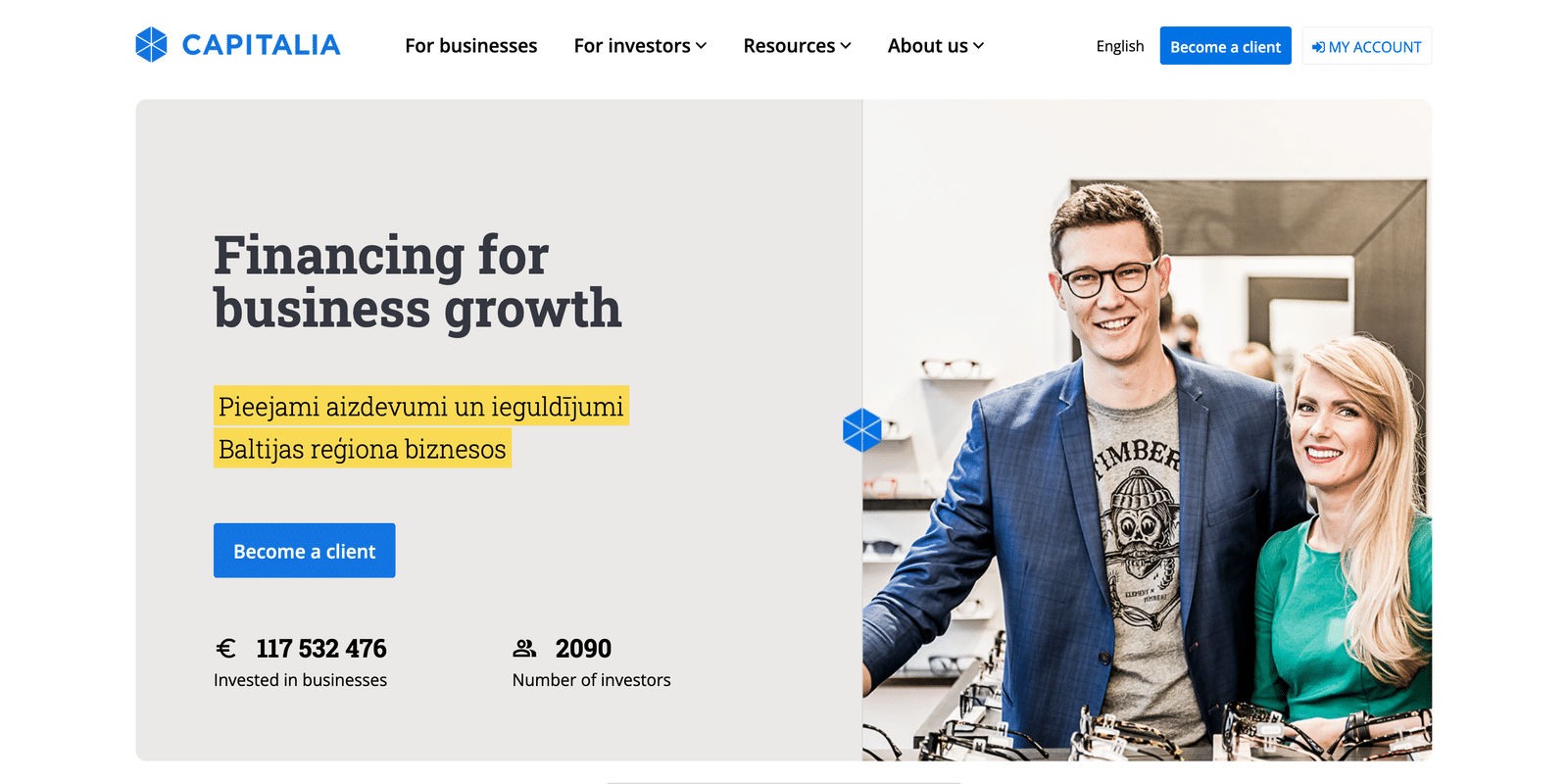

Capitalia Review 2026 – Baltic Business Lending With an 18-Year Track Record

Start investing on Capitalia I first came across Capitalia back in 2021, when I had an introductory call with their team. At the time, the platform was still in its earlier stages of opening up to retail investors. Five years later, Capitalia has become one of the most established business lending platforms in Europe, with […]

Kraken vs Coinbase — Which Is Better in 2026?

I’ve been using both Kraken and Coinbase for years to buy and hold crypto from Spain. They’re the two names that come up in every “which exchange should I use?” conversation — and for good reason. Both are fully regulated in Europe under MiCA, both have never lost customer funds to a hack, and both […]

PeerBerry vs Esketit — Which Is Better in 2026?

PeerBerry and Esketit target a similar type of investor — someone looking for solid returns on European consumer loans without the complexity of a mega-platform like Mintos. I’ve invested on both, and until recently, I would have called them roughly comparable options with different strengths. But 2025 changed the equation. PeerBerry has continued its steady […]

Best Anonymous Bitcoin Wallets in 2026

TL;DR: True anonymity in Bitcoin is harder than ever. Regulators shut down Samourai Wallet in 2024, Binance now requires full KYC, and the EU’s MiCA regulation plus Travel Rule mean exchanges must collect identity data on transactions over 1,000 euros. Your best options in 2026: a Ledger hardware wallet for long-term storage, Sparrow Wallet for […]

Scramble Review 2026 – Consumer Brand P2P Investing

Start investing on Scramble Scramble is a European P2P investment platform with an unusual pitch: instead of funding consumer loans, mortgages, or small business debt, it provides working capital to early-stage consumer goods brands — think food startups, beauty labels, pet care companies, and fashion brands, mostly based in the UK and Europe. I’ve been […]

Mintos vs Esketit — Which Is Better in 2026?

If you’re comparing Mintos and Esketit, you’re looking at two platforms in very different stages of their evolution. Mintos is the established market leader — 700,000+ investors, EUR 12 billion funded, MiFID II regulated, and pursuing a banking license. Esketit is a younger platform that’s going through a significant transition after losing its parent company […]

The Fastest Video Creation Stack (iPhone + Mac)

Most people massively overcomplicate video creation. They search for a single tool that does everything: recording, editing, captions, podcast production, social clips, YouTube videos, and tutorials. The result is usually a slow workflow and lots of friction. A much better approach is to use a small stack of tools where each one does a specific […]

The Shrinking World

When I was a kid growing up in Malta, everywhere else felt like another planet. Foreign countries were enormous, impossibly distant places full of people who spoke languages I couldn’t understand, ate food I’d never seen, and lived in ways that seemed completely alien to my tiny island existence. Now I’ve been living abroad for […]

TradingView Review 2026 – The Best Charting Platform for Traders

Try TradingView for Free If you spend any amount of time analyzing financial markets, you have almost certainly come across TradingView. It is the dominant charting and analysis platform on the web, used by over 100 million traders worldwide. Whether you are charting stocks, crypto, forex, or commodities, TradingView covers it all under one roof. […]

- « Previous Page

- 1

- 2

- 3

- 4

- 5

- …

- 29

- Next Page »