P2P lending is an alternative investment that comes with its own risks but can deliver strong returns. I’ve been averaging around 12% annually across all the platforms I’ve invested in. Expect some portion of your loan portfolio to default at some point — it’s the nature of the business — but this is typically offset by the interest you earn along the way.

Here are a few of my favorite P2P lending investment platforms:

I’ve written extensively about this topic, so make sure you head over to my post on the best European peer-to-peer lending platforms for the full range of options available.

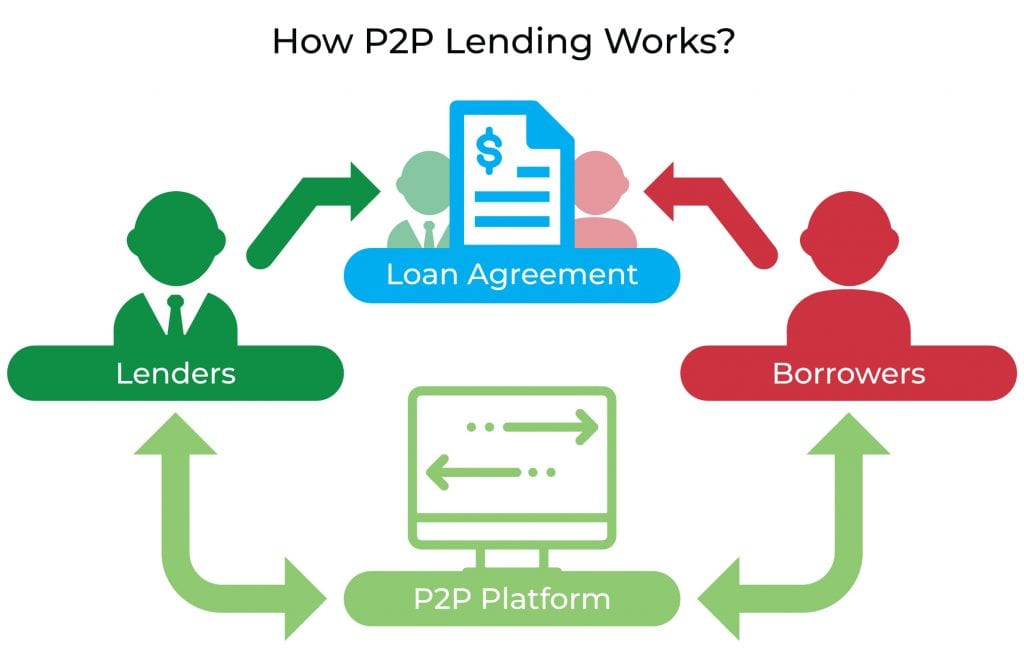

P2P stands for Peer-to-Peer, and the term comes from the world of computing — a network setup with no central coordinator. What some fintechs have done is apply this idea to lending.

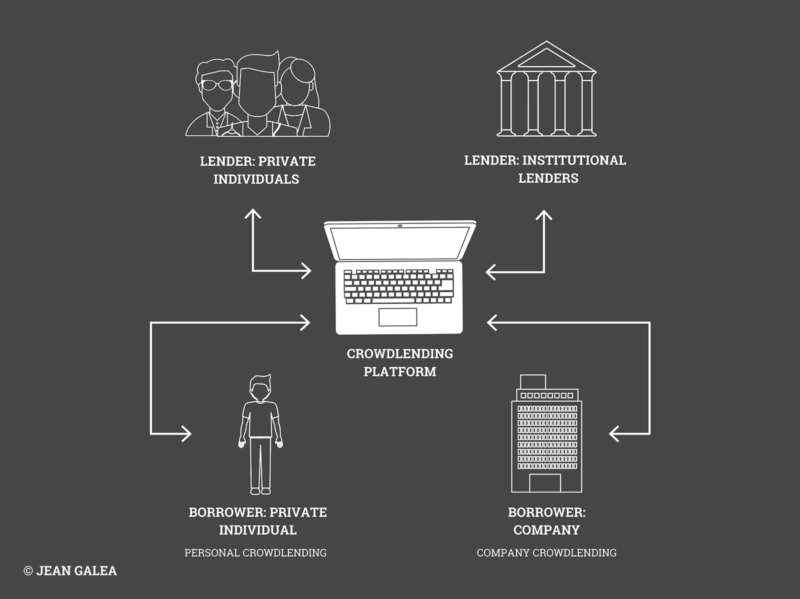

Borrowers and lenders are directly connected through a digital platform, with no traditional financial institution acting as a middleman. The result is better interest rates for both sides than would otherwise be possible.

That said, it introduces its own complexities. Lenders must assess the information available and decide whether a particular investment is worth the risk.

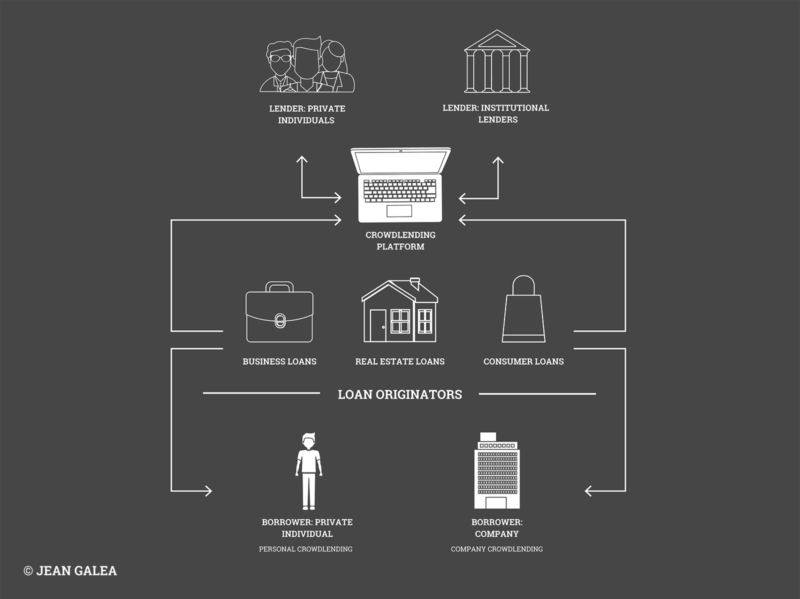

Some platforms operate on a four-party model that introduces another player: the loan originator, who is responsible for sourcing borrowers and underwriting loans.

View the list of best P2P lending platforms

This can raise additional concerns. If an outside party is selecting borrowers, doesn’t that introduce a new layer of ambiguity? And what’s in it for them?

Loan originators put their own capital into the projects they bring to the platform, aligning their interests with those of investors. If you lose, they lose. The amount of their own money on the line acts as a seal of approval that ties their results to yours.

Sounds interesting? Check out my list of best European P2P platforms or read on to understand how these platforms work.

- P2P lending connects investors directly with borrowers through online platforms, cutting out traditional banks

- Returns typically range from 7-14% annually, but defaults are part of the game — diversification is essential

- Most European platforms offer a buyback obligation, where the loan originator repurchases defaulted loans

- The biggest risk is not individual borrower default but loan originator or platform failure

- Start small, spread across multiple platforms, and only invest money you can afford to lock up

The History of Peer-to-Peer Lending

The peer-to-peer technology concept was first popularized by music file-sharing networks like Napster, eMule, and eventually torrents. The idea: remove the intermediary and let regular people exchange directly with each other.

Applied to lending, that means lending money to people who need it without a bank in the middle. Capital flows directly from investors to borrowers.

The traditional loan process required visiting a bank, documenting your assets, submitting an application, and waiting days or weeks for a decision. After the 2008 financial crisis, banks became far more restrictive — particularly in certain countries — leaving many individuals and businesses without access to capital.

This created an interesting tension. Investors in Western Europe (Germany, UK) were sitting on cash and hungry for yield. Meanwhile, people and businesses in Eastern Europe (Latvia, Lithuania, Georgia) were struggling to obtain financing. P2P platforms stepped in to bridge this gap.

Investors now have no geographic borders. They can invest in loans across multiple countries and earn returns that reflect the local demand for credit. The platforms themselves typically take a cut from the spread between what borrowers pay and what lenders receive.

How P2P Platforms Link Investors and Borrowers

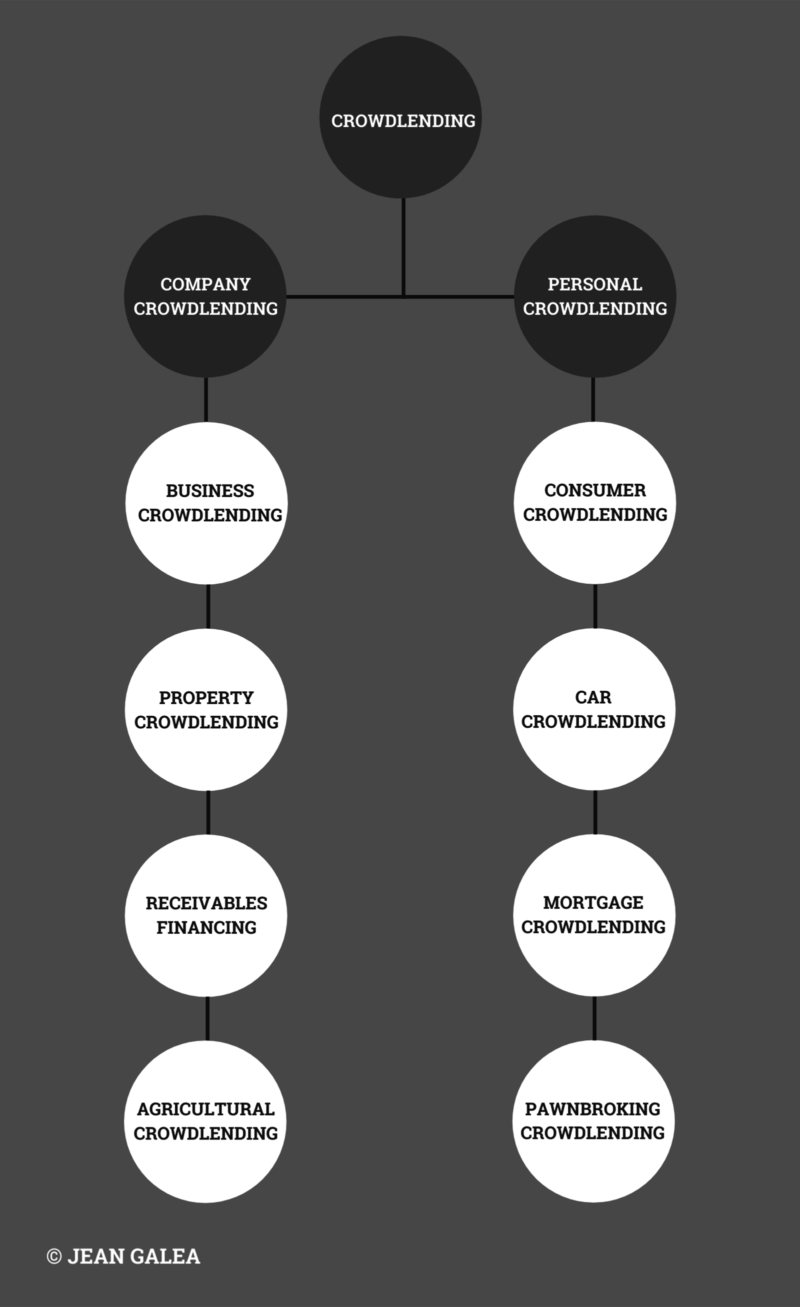

You’ll typically see different kinds of loans — some unsecured, others with guarantees of various kinds.

If the loans you invest in come with a Buyback Guarantee, the main risk becomes the platform itself going bankrupt — whether due to bad management, heavy competition, or outright fraud. The buyback guarantee means the loan originator is obliged to repurchase any loan that goes past a certain number of days overdue, typically 60 days.

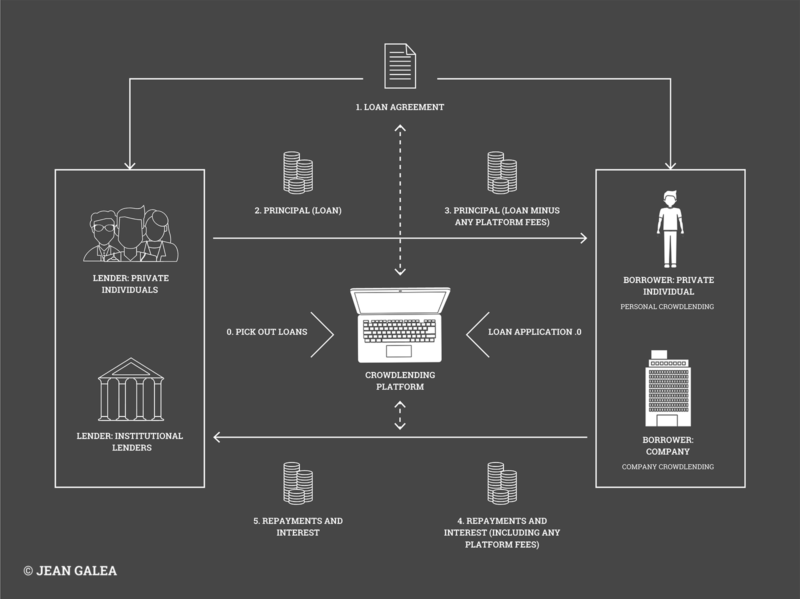

Peer-to-peer platforms service the loans and collect payments from borrowers. Those payments are then divided proportionally among all investors who funded that particular loan.

As soon as a borrower repays their loan, you start receiving payments of both principal and interest for the investment period. These are automatically transferred to your account. You can reinvest the received money into available loans or request a withdrawal directly to your bank account.

Each loan has a specific repayment date, so you receive money in your account according to the payment schedule of each individual borrower.

How Do P2P Lending Sites Make Money?

As investors, we should always be clear-eyed about where we put our money. As Warren Buffett likes to say:

“The first rule of investing is not to lose money.”

So whenever someone presents me with an opportunity, my first question is:

“What’s in it for them?”

Let’s apply that to the European P2P lending platforms we’ve been discussing.

P2P lending companies are intermediaries between lenders (individual investors) and borrowers (typically smaller businesses or individuals). We therefore have three parties involved, with the possibility of a fourth if the platform aggregates loan originators — Mintos is the clearest example of this model.

In the early days, platforms charged fees to both lenders and borrowers. Today, I’ve yet to come across a platform that charges fees to investors — except occasionally on withdrawals or currency conversions. Charging investors is simply a bad marketing look. Instead, platforms make money from the spread: they earn the gap between what they charge borrowers and what they pay lenders.

For consumer loans, a typical structure might look like this: the platform charges the borrower 25%, pays the lender 14%, and keeps the remaining 11% for itself. For larger business loans, flat fees to borrowers are also common.

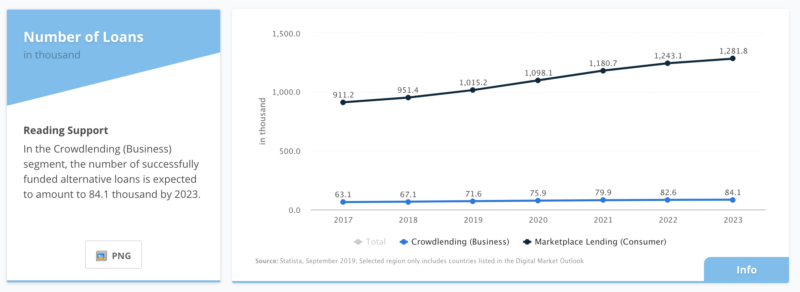

Is P2P Lending Growing in Europe?

P2P lending volume has grown consistently in Europe, though the post-pandemic years have brought both opportunity and turbulence.

By 2025, the European P2P lending market had reached approximately €3.2 billion in annual volume, with consumer lending accounting for the lion’s share at around €2.7 billion. The market is now entering a consolidation phase after years of rapid growth — many smaller platforms have folded or been absorbed, and the landscape is increasingly dominated by established names.

For 2026 and beyond, market projections point toward steady growth in the €2.8–3 billion annual range as the sector matures and regulatory frameworks take hold.

Two sources I regularly check for market data are:

Both remain actively updated and are worth bookmarking. If a platform doesn’t publicly share its loan volume and performance data, I treat that as a red flag. Transparency on these numbers is a basic bar that serious platforms should clear.

ECSP Regulation: What It Means for Investors

One of the most significant developments in European P2P lending since 2021 has been the introduction of the European Crowdfunding Service Provider (ECSP) regulation. Since November 2023, all EU-based crowdfunding and P2P lending platforms within the scope of the regulation are required to hold a formal license.

This is a meaningful change. For years, the European P2P lending space operated in a regulatory grey zone, with platforms registered under a patchwork of national rules. The ECSP framework establishes a single EU-wide passport: one license, valid across all 27 member states.

For investors, the practical implications are:

- Licensed platforms must meet transparency and disclosure standards

- They are subject to ongoing supervision by their national financial regulator

- An EU passport makes it easier for compliant platforms to expand across borders

- Platforms that failed to obtain a license by November 2023 were required to cease operations in the EU

As of 2024, ESMA data showed 181 licensed crowdfunding service providers active across 21 EEA countries, collectively facilitating €4.25 billion in funding. The licensing requirement has had a predictable consolidating effect: platforms that couldn’t meet the bar have exited, which on balance is good for investor protection.

The most prominent example of a platform that went further than just ECSP compliance is Mintos, which obtained a full European investment firm license from the Latvian regulator in 2021 — a significantly more demanding standard. As of early 2026, Mintos has announced it is pursuing a banking license in Latvia, which would allow it to offer deposit accounts alongside its investment products.

What Returns Can You Expect from Peer-to-Peer Lending?

I think peer-to-peer lending is one of the better ways to earn passive income that most investors overlook. Real estate gets all the attention, but in my experience P2P lending can produce comparable or better returns with considerably less effort.

I’ve been averaging around 12% returns annually across the various platforms I’ve used.

A common question is what counts as an acceptable minimum return. My answer is that it depends on the risk-free rate at the time — and that baseline has changed dramatically since I first started writing about P2P lending.

When I originally published this guide in 2019, European central bank rates were near zero and US Treasury yields hovered around 2.5%. That context made 9–10% P2P returns look exceptional. Today the picture is different. European Central Bank rates have risen sharply through 2022–2024, making government bonds and even bank savings accounts more competitive than they’ve been in over a decade.

The practical implication: the risk premium you need to demand from P2P lending is higher now than it was in 2019. You’re no longer comparing P2P returns against near-zero deposit rates — you’re comparing them against 3–4% on short-dated European government bonds or 4–5% on savings accounts. I’d therefore be looking for at least 10–12% from a P2P platform before I consider the risk-adjusted math to make sense. Anything below 8% on a consumer loan platform doesn’t excite me in the current rate environment.

The good news is that platforms have adjusted. Average P2P returns across European platforms sit around 11–12% annually as of 2025, which still represents a meaningful spread over traditional fixed income.

Who Can Invest in P2P Lending Sites?

European P2P lending sites are generally open to all European investors, and some accept investors from outside Europe as well.

The majority of platforms that accept international investors are based in the Baltic states — Latvia, Estonia, and Lithuania in particular. Mintos and Bondora are the two original success stories from that region and remain among the largest platforms in Europe by investor count.

There are also country-specific platforms. CrowdProperty, for instance, is one of the UK’s leading specialist property lenders and is restricted to UK-based investors. It’s been operating since 2014 and is authorized by the FCA.

Many platforms support multiple languages — a sensible approach given Europe’s linguistic diversity. Mintos, for example, is available in English, Spanish, German, Czech, Latvian, Polish, and Russian.

Investor eligibility is something to verify on a platform-by-platform basis. Requirements around minimum age, country of residence, and KYC documentation are standard, and a handful of platforms restrict access to certain jurisdictions for regulatory reasons.

How to Diversify Across Several P2P Lending Platforms

Diversification is a basic investment principle, and it applies inside P2P lending just as it does across other asset classes. Serious long-term investors typically hold:

- Stocks and bonds

- Real estate

- Ownership of businesses

Others diversify further into commodities, cryptocurrencies, peer-to-peer loans, or precious metals. All of the above has a role depending on your circumstances — but P2P lending works best as one component of a broader portfolio, not the whole thing.

A question I get frequently from new investors is:

“Should you spread your P2P investment across many platforms?”

If you read certain other blogs, you’ll see writers investing in a new platform almost every month, claiming they do it “for the benefit of readers.” I’d encourage some skepticism here.

Managing investments across multiple platforms is time-consuming — and it’s not linear. Every platform you add creates administrative overhead: tracking balances, following up on delayed payments, filing tax documentation, and staying on top of any developments with the platform itself. If you’re investing through an audited company, each additional platform also adds to your audit cost, since auditors need to get familiar with that platform and assess the impairment risk on your loan portfolio.

How to invest €10,000 in P2P Lending

My honest recommendation: keep the number of platforms small.

For €10,000 or less, I’d put it all on one platform — the most established, transparent, and liquid one I could find. For €25,000, I’d spread across two or three platforms at most. And I wouldn’t add a fifth or sixth platform unless I was managing well over €100,000.

If you see bloggers invested across 10 or more platforms simultaneously, the most likely explanation is affiliate commissions, not investment strategy. A referral bonus from a new platform sign-up is worth far more to a blogger than the actual interest on a small investment. The incentive structure is not aligned with yours.

Keep in mind that your reporting and tax compliance costs increase with each platform you add. Your accountant will bill you for time spent, and the time goes up with complexity. If you are based in Spain, balances held on foreign platforms may also need to be declared on the Modelo 720.

Risks of P2P Lending

Every investment class carries risks, and P2P lending is no exception. There’s a lot to cover on the safety side — enough that I wrote a dedicated guide on whether P2P lending can be considered safe — but let me highlight the key risk categories here.

Platform risk. If the platform itself goes under — due to mismanagement, fraud, or a liquidity crisis — recovering your funds can be difficult and slow. This happened with several platforms during the COVID disruptions of 2020 and again when some loan originators exposed to Eastern European markets ran into trouble following the 2022 invasion of Ukraine. Platform risk is the one you can’t diversify away from by spreading across loans within a single platform.

Loan originator risk. On aggregator platforms like Mintos, the intermediary layer of loan originators adds a second point of failure. If a loan originator collapses, the platform may struggle to recover funds on your behalf. Several Mintos loan originators went into default during 2020–2021, and the recovery process for affected investors was lengthy.

Buyback guarantee risk. A buyback guarantee is only as good as the financial health of the entity backing it. If the loan originator providing the guarantee becomes insolvent, the guarantee is worthless. This is not a hypothetical — it has happened.

Liquidity risk. Many P2P investments are illiquid by nature. Secondary markets exist on some platforms, but they’re not always liquid. If you need your money quickly, you may not be able to exit at par.

Regulatory and political risk. Platforms operating in or funding loans in politically unstable regions carry additional tail risk. The Russia-Ukraine conflict froze a meaningful volume of loans on several platforms. This is a real risk that wasn’t priced in before 2022.

The overall picture: P2P lending is a legitimate asset class with real returns, but it requires ongoing attention and a clear-eyed view of the downside scenarios.

Alternatives to P2P Lending

If you want to diversify beyond P2P lending, I’d suggest looking at real estate crowdfunding platforms. Returns are typically 2–4 percentage points lower than P2P consumer lending, but the underlying collateral — property — provides a layer of protection that unsecured consumer loans don’t.

You can also consider crypto interest accounts, though these carry their own distinct risk profile and the regulatory landscape around crypto lending has shifted significantly since 2022.

And of course, in the current rate environment, government bonds and even high-yield savings accounts are more competitive than they’ve been in over a decade — worth including in your thinking. If you’re still weighing whether P2P lending fits your portfolio at all, I’ve written a dedicated piece on why (or why not) to invest in peer-to-peer lending that covers the comparison against other asset classes in detail.

Questions?

Do you have any questions about peer-to-peer lending? I’ve been active as an investor in the space for close to a decade and have learned a great deal through both experience and direct conversations with some of the people behind the top platforms.

Questions and open discussion are how this topic is best understood, so I welcome them in the comments below. Please leave your questions there rather than sending an email — your question and my answer will be visible to every reader who comes after you.

Related

Hi Sir,

I have red somewhere that Mintos is not free for a French man.

In other words I cannot invest in Mintos because I am French.

Can you say the same,

Smiling Paul

PS: excuse my bad English!

thax

Why do you recomend Bulkestate? For the level of transparency?

I also like Viainvest for the track record and transparency.

And what´s your opinion for Crowdestor?

I should have probably made a separate category for real estate crowdfunding websites, in which I would also include Reinvest24 and Property Partner.

I’ll update the post.

Thanks for your post. What makes you recommend those 3/4 platforms over the others?

Several factors, I would say these are some of them that are important for me:

Happy to answer other questions you may have and discuss further.

Thanks for your replay Jean. Do you no longer recommend Twino?

Did you try any factoring P2P sites yet? Investly seems interesting and has a low default rate. I’m not sure I understand how it works yet though.

All thes best

Thanks! Happy first advent.