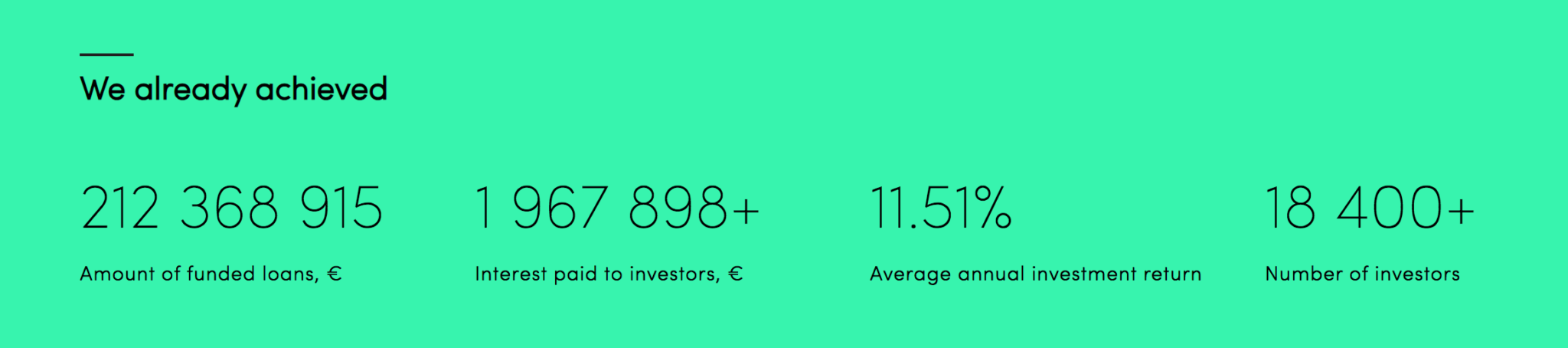

PeerBerry has earned its reputation as one of the most reliable P2P lending platforms in Europe. EUR 3.24 billion funded, 110,000+ investors, zero major originator defaults, and ~11% annual returns. Hard to argue with that track record.

So why look elsewhere?

Two reasons. First, PeerBerry has no secondary market — once you invest, your money is locked until the loan matures. If you need liquidity, that’s a problem. Second, PeerBerry relies heavily on the Aventus Group for around 80% of its loan supply. That concentration creates a dependency risk that diversification across other platforms can offset.

I’ve been investing on PeerBerry for years and it remains in my portfolio. But here are the platforms I use alongside it.

Quick Comparison: PeerBerry vs the Alternatives

| Platform | Best For | Avg. Returns | Regulation | Secondary Market | Review |

|---|---|---|---|---|---|

| Mintos | Diversification and scale | ~12% | MiFID II licensed | Yes (0.85% fee) | Review |

| Esketit | ECSP license + secondary market | 10-14% | ECSP licensed | Yes | Review |

| Swaper | Maximum returns + loyalty bonuses | ~14% | Not regulated | No | Review |

| Robocash | Short-term loans with fast buyback | ~12% | Not regulated | No | Review |

| Lonvest | Promising new platform | ~12% | Not regulated | No | Review |

| Income Marketplace | Junior/senior tranches | ~12% | Not regulated | Yes | Review |

Mintos — The Market Leader

Mintos is the obvious first alternative — and for good reason. It’s the largest P2P lending platform in Europe with over EUR 12 billion funded, 700,000+ registered investors, and a MiFID II license that provides the strongest regulatory protection available in this space.

Why it works as a PeerBerry alternative: Where PeerBerry concentrates around 80% of its loans through Aventus Group, Mintos spreads investments across 60+ loan originators in 33 countries. That diversification is the single biggest advantage. Mintos also offers a secondary market, which solves PeerBerry’s liquidity problem — you can sell investments before maturity if needed.

The trade-offs: Mintos is not without its own issues. The platform carries around EUR 130 million in unresolved defaults from originator failures over the years. My personal net return over 9 years averages ~9% — lower than the advertised ~12% — because of these defaults. Mintos also recently introduced a 0.29% annual fee on Custom Portfolios. PeerBerry has no fees at all.

Key differences from PeerBerry:

- MiFID II regulated with EUR 20,000 investor protection — PeerBerry is not regulated

- Secondary market available (0.85% fee) — PeerBerry has none

- 60+ originators vs PeerBerry’s 12

- Additional products: fractional bonds, ETFs, and a High-Yield Bonds Portfolio

- Annual management fee of 0.29% on Custom Portfolios — PeerBerry is fee-free

- History of originator defaults — PeerBerry has none

Best for: Investors who want maximum diversification across originators and countries, a secondary market for liquidity, and the strongest available regulation. Mintos is the natural complement to PeerBerry — their strengths and weaknesses are almost perfectly inverted.

See my full Mintos review or the Mintos vs PeerBerry comparison.

Esketit — Regulatory License Plus Liquidity

Esketit solves two of PeerBerry’s main gaps simultaneously: it has a regulatory license (ECSP) and a secondary market. Returns range from 10-14%, with a buyback guarantee on most loans.

Why it works as a PeerBerry alternative: If PeerBerry’s lack of a secondary market concerns you, Esketit provides an exit option for your investments. And its ECSP license provides regulatory oversight that PeerBerry doesn’t have.

What to watch: AvaFin’s withdrawal from P2P operations in 2025 changed Esketit’s dynamics. The platform is rebuilding its originator base — Jet Finance joined in February 2026 — but it’s in a transitional phase. The loan portfolio declined slightly in 2025, going from EUR 48 million to EUR 45 million. Monitor this closely.

Best for: Investors who want the combination of a secondary market, a regulatory license, and competitive returns that PeerBerry can’t provide.

See my full Esketit review or the PeerBerry vs Esketit comparison.

Swaper — Push Returns Even Higher

Swaper offers the highest base returns in European P2P lending — around 14%. Add the loyalty program (Silver +0.5% at EUR 5,000, Gold +1% at EUR 10,000, Platinum +1.5% at EUR 25,000, VIP +2% at EUR 50,000) and the effective rate climbs toward 16%.

Why it works as a PeerBerry alternative: PeerBerry and Swaper share a similar structure — both are relatively simple platforms focused on consumer loans with auto-invest and buyback guarantees. Swaper just pays more. If you’re comfortable with PeerBerry’s unregulated status (since Swaper is also unregulated), the higher return is a straightforward upgrade.

The risk: Swaper relies primarily on Wandoo Finance as its loan originator. That’s a similar concentration risk to PeerBerry’s Aventus dependency. Using both means you’re diversifying across platforms but maintaining single-originator exposure on each.

Best for: Yield-focused investors who want to step up from PeerBerry’s ~11% to Swaper’s ~14%+ while keeping a similar platform experience.

See my full Swaper review or the PeerBerry vs Swaper comparison.

Robocash — Fast Buyback on Short-Term Loans

Robocash focuses on short-term consumer loans with a distinguishing feature: a 30-day buyback period instead of the standard 60 days. That means if a borrower defaults, the loan originator buys back the investment twice as fast as on PeerBerry.

Why it works as a PeerBerry alternative: Similar returns (~12%), similar loan types (short-term consumer), but with a faster buyback mechanism. For investors who want their capital recycled quickly, that 30-day window matters.

What to know: My review flagged concerns about the financial health of UnaFinancial, Robocash’s parent group. These risks haven’t materialized into losses, but they’re worth tracking. Like PeerBerry, Robocash is not regulated and has no secondary market.

Best for: Investors who favor short-term loan exposure with quick buyback resolution. Use as a smaller allocation alongside PeerBerry, not as a replacement.

See my full Robocash review or the PeerBerry vs Robocash comparison.

Lonvest — A Promising Newcomer

Lonvest launched in 2023 and has quickly established itself as one of the more interesting new platforms. Returns sit around 12% with a 60-day buyback guarantee, and the platform has a clean, modern interface that’s easy to navigate.

Why it works as a PeerBerry alternative: Fresh originator exposure. PeerBerry’s strength is also its constraint — you’re investing through the same handful of originators every time. Lonvest introduces different lending companies and geographies, which adds genuine diversification to your overall P2P portfolio.

Best for: Investors who want to diversify across platforms and originators with a smaller allocation to a newer platform with solid early results.

See my full Lonvest review or the PeerBerry vs Lonvest comparison.

Income Marketplace — Junior/Senior Tranche Structure

Income Marketplace takes a different approach to risk management. Instead of a standard buyback guarantee, it offers a junior/senior tranche structure where loan originators invest their own money in the “first loss” piece. If defaults happen, the originator’s capital absorbs losses before investors are affected.

Why it works as a PeerBerry alternative: The tranche structure provides a different kind of protection than PeerBerry’s buyback guarantee. It also offers a secondary market for early exits — something PeerBerry lacks. Returns are around 12%, comparable to PeerBerry’s ~11%.

Best for: Investors who like the idea of structural protection (originators taking first losses) rather than relying solely on buyback promises.

See my full Income Marketplace review.

Which PeerBerry Alternative Should You Choose?

If you want proper regulation: Mintos (MiFID II) or Esketit (ECSP).

If you need a secondary market: Mintos, Esketit, or Income Marketplace.

If you want higher returns: Swaper (~14% + loyalty bonuses).

If you want a similar experience to PeerBerry but different originators: Lonvest or Robocash.

My recommendation: combine PeerBerry with Mintos as your core holding for diversification and liquidity, then add one or two smaller positions from the alternatives above based on your priorities.

For the full landscape, see my ranking of the best European P2P lending platforms.

Frequently Asked Questions

Why doesn’t PeerBerry have a secondary market?

PeerBerry has chosen to keep its platform simple. Since most loans are short-term (many maturing within 30 days), the need for a secondary market is less pressing than on platforms with longer-term loans. Your capital recycles quickly through buyback and maturity. However, if you have a large allocation and might need early access to funds, this is a meaningful limitation.

Is PeerBerry safe without regulation?

PeerBerry operates under Lithuanian licensing but is not regulated in the way Mintos (MiFID II) or Esketit (ECSP) are. What PeerBerry does have is a strong track record — EUR 3.24 billion funded with no major originator defaults, and all loan originators publish audited financial statements. Track record matters, but it’s not the same as regulatory protection. See my full PeerBerry review for more detail.

Can I earn more than 11% on PeerBerry alternatives?

Yes. Swaper offers ~14% base + loyalty bonuses up to +2%. ViaInvest offers ~13% with MiFID II regulation. Esketit ranges from 10-14%. Even Mintos’s advertised average of ~12% is slightly higher than PeerBerry’s, though real-world net returns can vary.

What’s the biggest risk of staying only on PeerBerry?

Originator concentration. Aventus Group accounts for approximately 80% of PeerBerry’s loan supply. If Aventus faced financial difficulties, it would affect the vast majority of your PeerBerry portfolio. Diversifying across platforms with different originators is the primary mitigation strategy.

Should I leave PeerBerry entirely?

No. PeerBerry’s clean track record and reliable returns make it worth keeping. The goal isn’t replacement — it’s diversification. I keep PeerBerry as one of several P2P platforms in my portfolio, each serving a different purpose.

Related

Leave a Reply