If you hold crypto and you’re not doing anything with it, you’re leaving money on the table. YouHodler is the platform I use to earn yield on idle holdings, borrow against crypto without selling, and occasionally take leveraged positions on the market.

I first covered YouHodler back in 2020. A lot has changed since then — the platform survived the 2022 crypto crisis that wiped out competitors like Celsius and BlockFi, expanded its regulatory standing across Europe, and deepened its product lineup considerably. This updated review reflects where things stand in 2026.

What is YouHodler?

YouHodler is a Swiss-based crypto finance platform founded in 2017, headquartered in Lausanne. It sits in the overlap between a crypto exchange, a yield platform, and a crypto-backed lending service. The core pitch: keep your crypto, put it to work.

Where most exchanges make money from trading fees and leave you with idle assets between moves, YouHodler gives you tools to generate yield on holdings, access liquidity without selling, and take leveraged directional positions if that’s your thing.

The main features:

- Yield accounts — earn interest on BTC, ETH, stablecoins, and 50+ other assets

- Crypto-backed loans — borrow fiat or stablecoins against your crypto at up to 90% LTV

- Exchange — buy, sell, and swap crypto

- Multi HODL — leveraged long/short trading (high risk, handle with care)

Not available to US citizens or residents. Primarily serves Europe, where the platform has operated since 2019.

Regulation and Track Record

YouHodler has built a more credible regulatory profile than most crypto platforms of its size. It’s a member of the Swiss VQF self-regulatory organization, which puts it under the Swiss Anti-Money Laundering Act (AMLA-CH). It’s also affiliated with the Financial Services Ombudsman FINSOM and registered as a virtual asset service provider (VASP) in Italy, Spain, and Argentina.

On the EU front, YouHodler has published a MiCA-compliant white paper — the EU’s Markets in Crypto-Assets framework that became fully effective in 2025. This is the same regulatory framework that forced many offshore platforms to either comply or exit European markets. YouHodler chose to engage.

The 2022 crypto crisis was a genuine stress test. Celsius, Voyager, and BlockFi all collapsed under the weight of illiquid positions and mismatched lending practices. YouHodler made it through, kept withdrawals open, and continued operating normally. That matters more to me than any marketing claim about security.

Worth noting: the Yield Account is not available to residents of Switzerland itself, due to local regulatory restrictions. Everything else is available throughout Europe.

Earn: Yield Accounts

This is the feature most long-term holders will care about most. Instead of sitting in a cold wallet generating nothing, your crypto earns a variable rate that YouHodler pays out weekly, directly in the same asset you deposited.

Current rates (as of early 2026, tiered by account level):

- Bitcoin (BTC): up to 7–12% APY depending on tier

- Ethereum (ETH): up to 8–12% APY depending on tier

- USDT: up to 11–20% APY depending on tier

- USDC: up to 11–15% APY depending on tier

YouHodler uses a seven-tier loyalty system — Basic, Jumpstart, Silver, Gold, Platinum, Diamond, VIP. Higher tiers earn meaningfully better rates. The minimum deposit to start earning is $100.

A few things worth knowing before depositing:

- Interest accrues daily, paid out every Friday

- No lock-up period — you can withdraw at any time, though you forfeit that week’s accrued interest if you pull out before the Friday payout

- No fees on the earn product itself

- Some stablecoins have restricted availability in certain EU markets

The rates on stablecoins are genuinely competitive. If you’re already holding USDT or USDC and have no near-term plans to deploy them, parking them at YouHodler makes straightforward sense. See how YouHodler compares in my roundup of the best crypto interest accounts.

Crypto-Backed Loans: Access Liquidity Without Selling

This is the feature that converted me from a passive observer to an actual user. The core idea: you need cash, but you don’t want to sell your Bitcoin or Ethereum because you believe they’re going higher — or because selling would trigger a taxable event.

YouHodler lets you deposit crypto as collateral and borrow fiat (EUR, USD, GBP) or stablecoins against it. Loans are processed in seconds, no credit check required. You repay the loan, you get your collateral back.

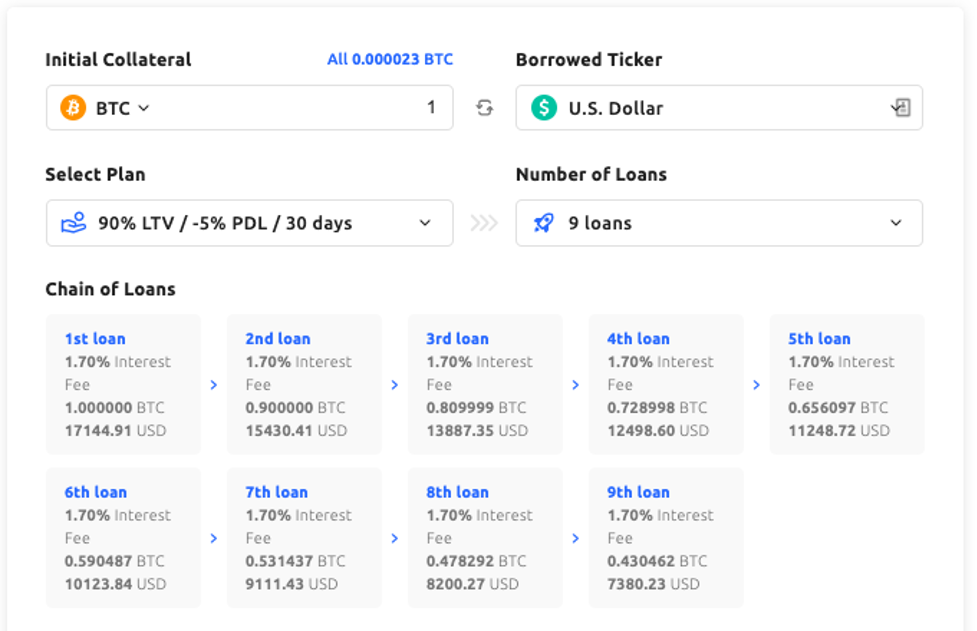

Loan-to-value options:

- 97% LTV — highest risk, closest to liquidation threshold

- 90% LTV — very aggressive, good for short-term liquidity needs

- 70% LTV — moderate, more buffer before liquidation

- 50% LTV — conservative, longest term, most safety margin

Loan terms run from 1 day to 364 days. Daily interest rates start from around 0.0099% depending on the asset and term. Loan origination fees range from roughly 1.70% to 7.50% of the loan value, varying by asset and LTV chosen.

The tax angle is relevant here, particularly for European investors. In most jurisdictions, borrowing against an asset is not a disposal — meaning no capital gains tax is triggered on the loan itself. You only face a taxable event if the platform liquidates your collateral due to a margin call. This makes crypto-backed loans a legitimate tax-efficiency tool for long-term holders who need liquidity. Run this past your own tax advisor, but the principle is well-established.

The “Price Down Limit” (PDL) is the equivalent of a margin call threshold — the price at which YouHodler will sell your collateral to close the loan. You can set and adjust this manually. If the market drops and you’re approaching your PDL, you’ll receive a notification and can add more collateral to extend your buffer.

There’s also a “Walk Away” option on 90% LTV loans: you can voluntarily close the loan, keep the borrowed funds, and surrender the collateral. A last resort, but useful to know it exists.

Exchange: Buy, Sell, and Swap

YouHodler functions as a full crypto exchange. You can buy crypto with a debit/credit card or bank transfer, sell crypto for fiat, and swap between assets directly on the platform.

The exchange is convenient if you’re already using YouHodler for yield or loans, but it’s not where I’d go for large trades — the spreads aren’t built for high-frequency or high-volume execution. Think of it as a utility layer, not a trading desk. For dedicated exchange options, see my list of the best crypto trading apps.

Fiat withdrawal fees are worth being aware of upfront:

- SEPA EUR withdrawal: €5

- SWIFT EUR withdrawal: €55

- SWIFT USD withdrawal: $85

- SWIFT GBP withdrawal: £70

For European users using SEPA, the €5 fee is reasonable. SWIFT fees are steep — factor those in if you’re moving significant amounts to a bank account.

There’s a dedicated exchange interface at YouHodler Exchange if you want to go straight to that feature.

Multi HODL: Leveraged Trading (High Risk)

Multi HODL is YouHodler’s leveraged trading product. It lets you go long or short on crypto with a multiplier up to 70x, built on top of a chain of automated loans that compound your exposure.

You set an entry amount, a multiplier, a take profit level, and a margin call level. YouHodler runs the loan chain automatically. If the trade goes your way, the gains are amplified. If it goes against you, the losses are amplified at the same rate.

This is a tool for people who understand leverage and have clear risk management in place. The minimum position is $10, which makes it accessible — but accessibility doesn’t reduce the risk. At 70x leverage, a 1.4% move against you wipes the position. Treat it accordingly.

Multi HODL was redesigned in recent years — the origination fee was removed, so you only pay a small hourly rollover fee (0.005% per hour on open positions) plus a profit share fee on winning trades.

If this isn’t your area, skip it entirely. The yield and loan features stand completely on their own.

Security

YouHodler stores client crypto assets using Ledger Vault, the enterprise custody arm of Ledger. Private keys are held in hardware security modules (HSMs), isolated from day-to-day operations and protected by multi-signature access controls. No single person or operator can move funds unilaterally.

The Ledger Vault integration comes with crime insurance coverage of up to $150 million, which covers client assets against employee theft, third-party theft of private keys, and physical breach of hardware security. That’s a meaningfully higher coverage level than the $1 million figure I mentioned in my original 2020 review.

Fiat deposits are held with regulated European banking partners. Two-factor authentication (2FA) is available and should be enabled on every account. YouHodler does not currently publish proof-of-reserves — a transparency gap worth noting, though it’s a common gap across the industry.

Who Should Use YouHodler

Good fit if you:

- Hold crypto long-term and want to earn yield without active trading

- Need liquidity but don’t want to sell your holdings or trigger a capital gains event

- Are a European investor comfortable with a regulated, Swiss-based platform

- Want a single platform covering earn, borrow, and exchange in one place

Look elsewhere if you:

- Are a US citizen or resident (YouHodler is not available to you)

- Are a Swiss resident looking for the Yield Account specifically (not available due to local regulation)

- Want the lowest possible trading spreads for high-volume execution — a dedicated exchange will serve you better

- Are not comfortable with centralized custody of your assets — if self-custody is a hard requirement, this platform isn’t for you

YouHodler Review: My Take

YouHodler has matured into a credible platform for European crypto investors. It’s not trying to be everything — it’s specifically built for people who hold crypto and want to do more with it than just wait.

The yield rates are competitive, particularly on stablecoins. The crypto-backed loans are genuinely useful for anyone managing a long-term position who occasionally needs liquidity. The regulatory groundwork — VQF membership, MiCA engagement, VASP registrations across multiple jurisdictions — gives it a more solid footing than most of the platforms that imploded in 2022.

The things I’d want to see improve: proof-of-reserves disclosure, and more transparency around how the yield rates are generated and sustained. These aren’t dealbreakers, but they’re the questions a careful investor should be asking of any yield-bearing crypto platform.

If you’re a European holder looking to put idle crypto to work without selling, YouHodler is worth a close look.

Summary

Youhodler is an excellent tool for those who are holding Bitcoin and other cryptos for the long term, as well as those who need to borrow. This platform is right there at the forefront of the DeFi wave that is taking over the Fintech and Crypto spaces this year.

Pros

- Good interest returns

- Make use of your crypto

- Many cryptos and stablecoins available

Cons

- Not available to US citizens

Related

Hi Jean. if YouHodler went bust would we lose our crypto?

Hi Jean,

Thanks for the review. I have been looking into the defi/cryptosavings apps to put my money in. Most critically I care about a scam/exit. The cover story can be a hack or whatever.

How reliable do you find youhodler? It has a postbox address in switzerland, where also some escort agency is located (just checked on google maps). their ceo/team seems all Russians. They claim to be legit but I do not know if they exit on me, can I actually find and sue them.

Reason I ask is: I love their app and the ease. I also love the customer service. I just cannot get my head around trusting or not. the 12% on EURS is unique, although purchase requires 1% fee.

Similarly, NEXO is great experience but website doesnt even say which country they are based in. T&C seems generic lingo, cant find the real company behind.

What does not help youhodler is they only have 17 employees on linkedin, all russian. How can we avoid few of them running away with the funds, imagine this company holds millions in savings; why would they not run? Same applies to NEXO. Compared to BlockFi i find them very low trust. But they offer the products i need (EURO savings) at better rate. (net 8% and 11% respectively)

Hi Ahmet,

Thanks for the good points raised.

BlockFi is arguably the most trusted name in the space at the moment because they are backed by some giants in the crypto space, and they have managed to amass the biggest amount of crypto under management.

I think that so far, being an American company has helped them become the leaders – most investors trust American companies and legislation. Not to mention that probably the majority of crypto investors are American. They don’t offer any gimmicks or tokens, unlike Nexo and Celsius. On the other hand, their new interest rates are quite low compared to their competitors.

YouHodler has a special space in this niche in my opinion because they have been quite innovative with their products. In my view, there is little risk that any of these mentioned platforms will run away with your money. All of them are run by competent and public figures who are trying to build sustainable businesses. The two big risks remain custody (it’s a significant problem in the whole crypto space) and the longevity of the platforms themselves. Crypto borrowing lending is quite a new thing, and we don’t know if all these platforms will be profitable enough to survive in the long term, although things are certainly going well for them during this bull market.

That’s all that I can say as an investor on YouHodler and BlockFi myself, unfortunately, I don’t have further insight into the workings of these companies. However, I will reach out to YouHodler directly in the hope that they can address some of the other concerns you mentioned.

Hello Ahmet,

Thank you for your interesting questions to Jean.

Jean thank you for replying to Ahmed’s comment.

My name is Leo, and I’m on behalf of Youhodler here.

From our side, we can assure you that we are definitely not a scam and we are here for a long time. Our company is 100% legit and we do our business in the legal field only, since the very beginning. You can check our licenses and documents on our website.

We would like to point your attention to the legal basis of the other companies which you mentioned. It’s not legal to pay interest on non-crypto currencies, please be careful with your funds when you see if somebody paying interest on fiat without a banking license.

Please feel free to visit our office in Lausanne during your next Swiss visit, we will pour you a coffee and make an excursion.

Should you have any doubts, questions, or concerns about Youhodler, feel free to address them to our customer support.

Cheers!

What about EURS, can I trust that stable coin to be hodling it in youhodler ?… not sure what amount to deposit as this kind of business doesn’t look as safe as a bank at all, if something happens you are not covered, am I right ?

EURS is one of the most trustworthy stablecoins as the reserves are audited; you can have a listen at my interview with the founder of Stasis (the company behind EURS) on Mastermind.fm for more information.

I wonder if you can assist. I am having trouble accessing my YHODER account. I did not get the authentication sms sent to me??I sent an email but have had no response

Amelia te felicito por andar en estos menesteres. Soy nuevo también en estos. Ya te resolvieron tu detalle con tu correo?

Y habilitantes tu cadena de préstamos? Bhas aumentado tus CRIPTOS?

ÉXITO!

Sr. Cortéz

When you do the transfer from transferwise, which option should i select, transfer to myself, someone or business/charity?

Business will work fine.

This no longer works. Wise does not support transfers to crypto sites anymore

That’s right, you can now only withdraw with Wise.

I was very happy to see the partnership of ledger with youhodler. Its a great move to help the company with the security of the funds. I sincerely will be very grateful if there will be a way youhodler will have a link with the ledger wallet to help investors directly link their hardware wallet to their platform.

I believe this will be an outstanding move only if it is a possible move. I wish youhodler a greater height.

Agreed.

Who is owner of private key on this youholder wallet? Isn’t it successor of cloud wallet which is a scam?

12% too good to be true 🙁

What makes you think this is related to cloud wallet? Youhodler work with Ledger Vault for securing their cold storage of crypto. Other lending companies also offer similar returns so it’s not something out of the ordinary.

Love all your writing Jean, thanks.

I am wondering if you suggest that you buy without fee let s say bitcoin and then the 4% fee doesn’t apply, right?

What do you think it matters what stablecoin i choose to earn the 12% interest?

Also curious how do you diversify between crypto platforms?

Ben Carlson and other passive indexing guys started How i invest my money, which helped me a lot, maybe we would be interested some similar post from you.

Hi Richard, you’re welcome. You can buy crypto from other platforms such as Kraken or Binance instead.

Tether is the biggest stablecoins and the most used on centralised exchanges. However there are doubts on whether it is fully backed by dollars and I wouldn’t want to keep much of my assets tied up in USDT for long periods. Tether the company has been battling multiple lawsuits accusing it of not properly backing its currency with collateralized reserves.

Paxos’ stable of stablecoins, including Paxos standard token (PAX), Binance USD (BUSD) and Huobi (HUSD), are all approved by regulators and are fully backed on a one-to-one basis with U.S. dollars.

USDC and DAI have market caps of $2.74 billion and $608 million, respectively. Yet, unlike on centralized exchanges, where tether is the go-to stablecoin in dollar-based crypto trades, USDC and DAI seem to have found their niche as the preferred stablecoins in decentralized trades.

USDC is issued by Circle which has been very transparent so far. DAI is decentralised which also is a good thing for transparency.

If I were to choose from the list of stablecoins we have available today to use on YouHodler, I would use USDC or PAX. Possibly even DAI. You could split your funds between all these three stablecoins. However, I prefer BTC for long-term holdings, even though the 12% interest on stablecoins is tempting. Bitcoin is just a superior store of value in my opinion, and long term the return on Bitcoin (through the rise of BTC vs USD) will probably be superior to the 12% interest you get on stablecoins.

I tend to keep a pulse on many platforms but ultimately choose a few that I like best. Since this is a space that changes fast, I might sometimes switch from one platform to another due to the first platform introducing some changes that I don’t like. At the moment, I really like what YouHodler is doing, they’re among the most innovative platforms in the crypto lending space.