Crypto assets can go through weeks of flat price action, and then suddenly go into a frenzy in a few hours. It is not practical for investors who are not professional traders to keep on top of the crypto markets themselves, also because the market is open 24/7. How can we get crypto price alerts […]

My Best Travel Tips – Accommodation, Flight Prices Etc

Getting the chance to travel is not something to take lightly. Many possibilities need to be taken into consideration before you begin. You can anticipate much hassle when it comes to packing for a trip. You cannot forget anything, and you cannot go back anytime soon. Keeping these two things in mind, simplify your traveling […]

My Thoughts on WordPress in 2020

I’ve been using WordPress since the early days, 2006 to be exact. I fell in love with the idea of open-source CMSs a few years before that, after experiencing firsthand how cumbersome and expensive closed-source CMSs were. The big open source players at the time were Drupal and Joomla, but then WordPress came along and […]

Best Apps for Trading Crypto in 2026

I bought my first Bitcoin in 2013. Back then, the process involved wiring money to a Slovenian exchange through a series of steps that felt more like money laundering than investing. The whole experience was confusing, slow, and more than a little sketchy. In 2026, buying crypto is as straightforward as buying a stock. The […]

Binance Review 2026 – Is This Crypto Exchange Right For You?

Binance is the world’s largest cryptocurrency exchange by trading volume — and by a wide margin. It handles roughly 40% of all global spot crypto trading, processes over $34 trillion in annual volume across all products, and serves more than 250 million users worldwide. If you want to buy and trade crypto, Binance gives you […]

Kraken Review 2026 – One of the Best Crypto Exchanges

Buy crypto on Kraken Kraken is one of the most established and secure crypto exchanges in the world, and it remains one of my favorites heading into 2026. It still holds the title of the largest Euro-based crypto trading exchange globally, and it’s a solid competitor to my other favorite exchange Binance. A lot has […]

N26 vs Revolut – Why I Think There is a Clear Winner

Back in 2020, I wrote a comparison of N26 and Revolut and concluded that N26 was the better bank. At the time, I stood by that call — N26 felt more like a real bank, had cleaner design, and Revolut was still finding its footing. A lot has changed since then. I still use both, […]

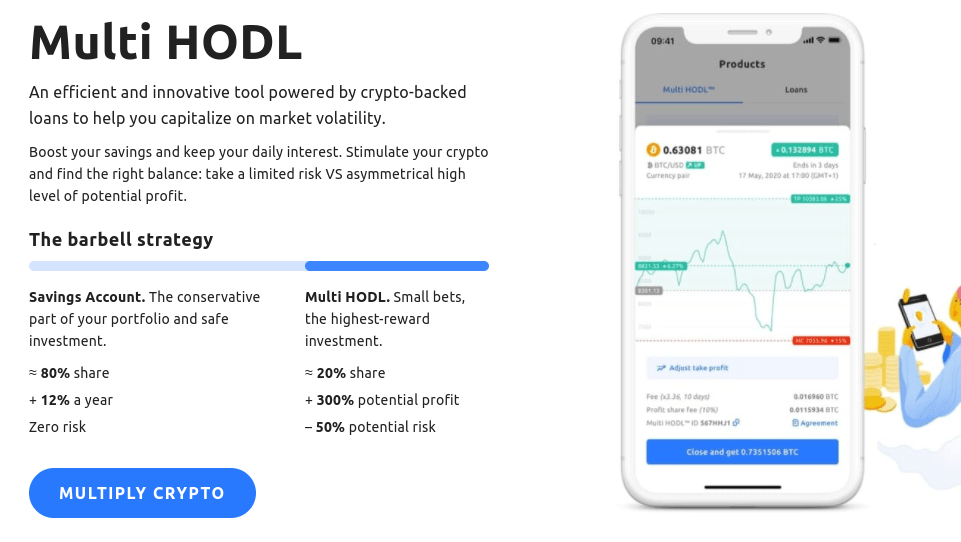

YouHodler Review 2026 – Earn Up To 12% Interest on Your Cryptos

If you hold crypto and you’re not doing anything with it, you’re leaving money on the table. YouHodler is the platform I use to earn yield on idle holdings, borrow against crypto without selling, and occasionally take leveraged positions on the market. I first covered YouHodler back in 2020. A lot has changed since then […]

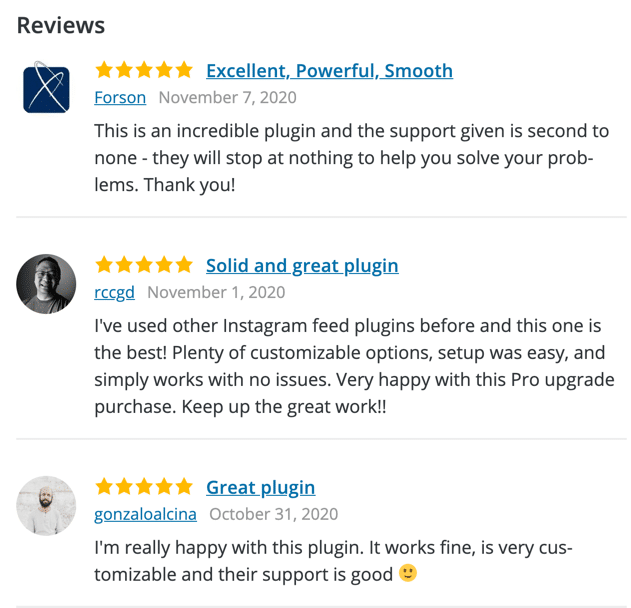

Spotlight Review – Easily Add Instagram Feeds to Your Site

This week was a very special one for us at RebelCode. It marks the launch of our latest plugin: Spotlight – a simple and effective way to add your Instagram feeds to your WordPress site.

What Are Good Operating Margins for WordPress Businesses?

WordPress businesses sit in a strange spot. The underlying platform is free and open source, but the businesses built on top of it — plugins, themes, hosting, SaaS products, managed services — can be extraordinarily profitable. The challenge is knowing what “good” actually looks like. Having run WordPress businesses for over a decade across plugins, […]

How to Start a Blog with WordPress

Starting a blog is a fun and rewarding experience. However, on the other hand, it can also be portrayed as being as daunting as it is interesting. Often, people are very interested in starting their own blog but struggle to get to grips with how to go about starting one from scratch. The purpose of […]

Swaper Review 2026 – A Top P2P Lending Platform

In this review, I’ll be taking a look at Swaper, one of my favorite P2P lending platforms in both function and design. Swaper is one of the latest entries into the P2P lending space in Europe, having started operations in May 2019. They have found success pretty quickly though, amassing more than 4000 active investors, […]

- « Previous Page

- 1

- …

- 18

- 19

- 20

- 21

- 22

- …

- 35

- Next Page »