Spanish banking has improved, but it still has a long way to go. If you’ve lived here for any amount of time, you’ve probably dealt with opaque fee structures, branch-only services, staff who treat you like an inconvenience, and a general culture of extracting money from customers in ways that feel designed to confuse.

I’ve been living in Barcelona since 2012 and have been through the full Spanish banking experience — opening accounts, getting refused, watching fees appear out of nowhere, and eventually finding a setup that actually works. This guide is the result of that experimentation.

The good news: you no longer need to settle for a traditional Spanish bank as your primary account. Digital banks have matured significantly, and a combination of the right online bank plus one traditional option for backup will serve you better than anything a Caixabank branch can offer.

What You Actually Need From a Bank in Spain

Before getting into the options, it’s worth understanding what “working in Spain” actually requires from a bank account.

The key issue is the Spanish IBAN. Spain runs on SEPA direct debits, and a surprising number of Spanish companies — utilities, gym memberships, landlords, insurance providers, government services — will only accept a Spanish IBAN (starting with ES) for direct debits. Some will refuse a foreign IBAN outright, others will accept it in theory but fail in practice.

This is not a minor inconvenience. It affects your electricity bill, your internet provider, your health insurance, your Hacienda tax payments. If your bank can’t give you a Spanish IBAN, it cannot be your primary Spanish account.

Beyond the IBAN, you’ll want:

- No monthly maintenance fees (or very low fees for premium features)

- A debit card that works everywhere

- A decent mobile app

- English-language support (or at least a functional app that doesn’t require calling anyone)

- Access to Bizum (Spain’s peer-to-peer instant payment system — it’s used constantly here)

With that framework in mind, here are the banks I actually recommend.

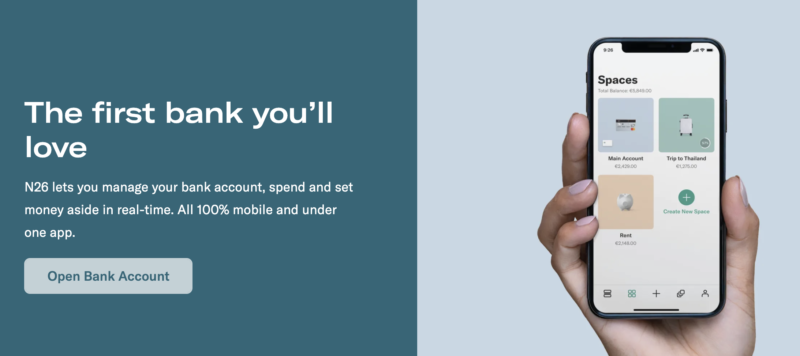

1. N26 — Best Overall for Expats in Spain

N26 is my top pick, and it has been for years. It’s a German bank (licensed by BaFin, Germany’s financial regulator), but it assigns every Spanish customer a genuine Spanish IBAN. You get all the protection of a German bank with an account that behaves like a local one.

This matters more than it might seem. I’ve had zero issues setting up direct debits with Spanish companies using my N26 IBAN — utilities, subscriptions, everything. It just works in the way a Spanish IBAN is supposed to work.

A few things that make N26 stand out beyond the IBAN:

- Desktop access. N26 has a proper web interface, which matters when you’re doing anything requiring a real screen. Revolut has a web app (app.revolut.com) but it’s limited, so N26’s desktop experience is considerably better.

- Clean, fast app. Instant notifications, clear transaction history, easy controls for freezing your card or adjusting limits.

- Bizum support. Available on all plans, so you can split a restaurant bill or pay the plumber without friction.

- Wise integration. International transfers are handled through Wise directly inside the app, which means mid-market exchange rates when sending money abroad.

- €100,000 deposit protection under the German Deposit Guarantee Fund.

N26 has over 8 million customers across Europe, and it’s been operating since 2013 — this is not a startup experiment. That said, it’s Europe-only; if you move outside the EU, your account gets closed.

N26 Plans in Spain

- Standard — Free. No monthly fee, Spanish IBAN, Mastercard debit card, Bizum. This is all most people need.

- Smart — €4.90/month. Adds sub-accounts (Spaces), partner discounts, and a choice of card colors.

- Go — €9.90/month. Travel and purchase insurance through Allianz, unlimited free ATM withdrawals abroad.

- Metal — €16.90/month. Premium metal card, comprehensive insurance package, airport lounge access discounts, higher ATM limits.

The free Standard account is genuinely good. I’ve used it as my primary Spanish account without ever feeling like I was missing something essential.

Read my full N26 review for a deeper breakdown.

2. Revolut — Best for Everyday Spending and Travel

Revolut is the most feature-rich neobank out there and, with 70+ million customers, it’s become the de facto spending card for anyone traveling through Europe. Currency exchange at interbank rates, instant spending notifications, easy card controls, a solid budgeting interface — it’s genuinely excellent for day-to-day use.

Revolut now offers Spanish IBANs. If you open a Revolut account in Spain today, you’ll automatically get an ES IBAN. Existing customers with Lithuanian IBANs are being migrated to the Spanish branch — once migrated, you get an ES IBAN as your primary identifier (your old LT IBAN still works). So the old objection about Revolut not working for Spanish direct debits is no longer valid.

That said, I still rank N26 above Revolut as a primary Spanish account. N26 gives you proper desktop access (Revolut’s web app exists but is limited), BaFin regulation (the strongest in Europe), and a longer track record of seamless Spanish IBAN functionality. Revolut is the better spending and travel card; N26 is the better bank account.

That said, Revolut earns its place as a powerful companion account. Use it for:

- Spending abroad — currency exchange at interbank rates with no markup on the standard daily limit

- Splitting costs with friends through the app

- Holding and converting between multiple currencies

- Budgeting and analytics features

- Cryptocurrency and stock trading (paid plans)

Revolut is still mostly a mobile-first experience. There is a web app at app.revolut.com for basics like checking balances and making transfers, but it’s limited compared to the mobile app. If desktop access matters to you, N26 is the better primary account.

Revolut Plans in Spain

- Standard — Free. Currency exchange up to a monthly limit, basic card controls, Bizum.

- Plus — Low monthly fee. Priority customer support, purchase protection, higher limits.

- Premium — €8.99/month. Unlimited currency exchange, overseas medical insurance, higher ATM limits.

- Metal — €15.99/month. Metal card, cashback on card payments, comprehensive travel insurance.

- Ultra — €45/month. Concierge service, highest limits across the board, exclusive Ultra card.

The free Standard plan is useful for travel and currency exchange. Most expats living in Spain will find Standard or Plus sufficient as a secondary card.

Read my full Revolut review or the N26 vs Revolut comparison if you’re deciding between the two.

3. Wise — Best for International Transfers and Multi-Currency

Wise (formerly TransferWise) isn’t a bank — it’s an Electronic Money Institution regulated by the FCA in the UK. That distinction matters: your money is safeguarded but not covered by traditional deposit insurance schemes the way a licensed bank would be.

For international transfers, though, Wise is in a category of its own. It uses the mid-market exchange rate — the real rate you see on Google — and charges a transparent, low percentage fee. No hidden spread, no inflated exchange rates, no surprise charges on the receiving end.

The Wise account also gives you local bank details in over 10 currencies, including EUR, GBP, USD, and AUD. If you receive income in multiple currencies, or regularly send money to family abroad, this is genuinely useful.

Where Wise fits in a Spanish banking setup:

- Receiving international payments in foreign currencies

- Sending money internationally (especially outside the EU)

- Holding balances in multiple currencies simultaneously

- Complementing N26 when you need to do cross-currency transfers

I wouldn’t use Wise as a standalone Spanish account — it’s not designed for that. But as part of a multi-account setup alongside N26, it covers a gap that neither N26 nor Revolut quite fills for complex multi-currency needs.

Read my full Wise review for more detail on how it works. If you also use PayPal for client payments, see my complete PayPal guide for online businesses for how to minimise currency conversion losses.

4. BBVA — Best Traditional Spanish Bank

If you need a traditional Spanish bank — for a mortgage, for dealing with Spanish bureaucracy that insists on a “real” bank, or simply as a backup — BBVA is the one I’d point you toward.

Their Cuenta Online is genuinely commission-free — no maintenance fees, no minimum balance requirements, no conditions. This is notable in Spain, where even “free” accounts often have hidden strings attached. BBVA’s mobile app has consistently won awards and is far better than anything offered by Caixabank or Santander. They also offer English-language service, which alone puts them ahead of most Spanish banks.

BBVA won’t replace N26 as your primary account — the experience isn’t as clean, and you’ll occasionally have to deal with branch visits and Spanish-language bureaucracy — but it’s the most competent of the traditional options and worth having in your toolkit for situations where a local bricks-and-mortar bank is required.

Banks to Avoid (or Be Cautious About)

Sabadell

I had an account with Sabadell for a while and I’d steer clear. The fee structure is opaque, customer support is poor even by Spanish banking standards, and their online banking interface — despite recent updates — still feels like it was designed in 2008. There are better options at every price point.

ING España

ING used to be my top recommendation for commission-free banking in Spain, and for a while it genuinely was. Then things went sideways.

ING has a policy of letting all incoming international transfers through without question — and then, months later, suddenly demanding documentation about every single one of them. I’m talking about transfers that were already processed and settled. They wanted proof of origin, invoices, contracts — for transactions that in some cases were years old. Retrieving all of that is enormously time-consuming and stressful, especially when you’re a freelancer or business owner with complex income sources.

Worse, during the COVID crisis they blocked clients’ accounts while all of this was going on. People who needed access to their money — during a pandemic, when families were under real financial pressure — were locked out. I find that kind of behavior indefensible. A bank’s job is to help during difficult times, not pile on more difficulty.

Their customer support is phone-only, with long wait times, and the staff can barely answer basic questions. On top of all that, the Cuenta NÓMINA is now conditional — you need a minimum monthly salary deposit to keep it fee-free, which rules out most freelancers and self-employed people.

Stay away from this bank.

Caixabank, Santander, and the rest

Spain’s big traditional banks are fine if you have no choice — and sometimes you genuinely don’t, for certain mortgages or specific financial products. But as primary accounts for day-to-day use, they’re expensive, bureaucratic, and their digital products lag far behind the neobanks. Unless you specifically need something only they offer, there’s no good reason to use them.

Documents You’ll Need

This is where a lot of people get stuck. Here’s what each type of account typically requires.

Traditional Spanish Bank (First Account)

Opening your first account with a traditional bank in Spain usually requires:

- Valid passport or EU national ID card

- NIE (Número de Identificación de Extranjero) — your Spanish tax identification number

- Proof of address in Spain (rental contract, utility bill, or padron municipal certificate)

- Proof of income or employment (payslip, employment contract, or tax declaration)

- In some cases: proof of legal residence status

Getting your NIE is the critical step. Without it, most traditional banks won’t open an account for you. The NIE application process involves a trip to a police station (or a Spanish consulate if you’re applying from abroad) and can take weeks. Sort this out early.

Traditional Spanish Bank (Second Account, Once You Have NIE)

Once you have an NIE and an existing Spanish bank account to show, the process is much simpler. Most banks will only need:

- Passport or national ID

- NIE

- Your existing Spanish bank account details

Digital Banks (N26, Revolut, Wise)

This is where the neobanks shine. The requirements are minimal:

- Valid passport or national ID

- A smartphone for identity verification (selfie + document photo)

- An email address

No NIE required. No proof of address. No visit to a branch. The verification is done entirely in-app and usually takes less than 10 minutes. For most expats, this means you can have a working N26 account within a day of arriving in Spain, long before you’ve sorted out the Spanish bureaucracy required for a traditional account.

The Discrimination Reality

I want to be direct about something that gets glossed over in most expat banking guides: banks in Spain discriminate, and they do it routinely.

My wife is Russian. She was refused by multiple Spanish banks before we found one that would open an account for her — not because of any issue with her documentation or finances, but simply because of her nationality. The refusals came without explanation, in the way that Spanish bank staff sometimes refuse things without telling you exactly why.

I’m Maltese — an EU citizen. I was refused at one bank despite Malta being a full EU member state. The staff member apparently wasn’t familiar with Malta and decided that was grounds for refusal. No appeal, no escalation, just a polite no.

This is the reality for a lot of non-Spanish, non-Western European people living here. The discrimination is usually informal rather than codified policy, but it’s consistent enough that you need to account for it. Traditional banks have discretion in who they accept, and they use it.

The practical implication: digital banks like N26 and Revolut don’t have this problem. Their verification is automated and nationality-blind. If your documents are valid and you pass the KYC check, you get an account. This is one of the strongest arguments for making a neobank your primary account rather than trying to force a relationship with a traditional Spanish bank that may not want your business.

My Recommended Setup

Here’s what I’d suggest for most expats in Spain in 2026:

- Primary account: N26 Standard — free, Spanish IBAN, works for all direct debits, desktop access, Bizum. This is your main account.

- Secondary account: Revolut Standard or Plus — use it for travel, foreign currency spending, and any situation where the Revolut feature set is useful.

- International transfers: Wise — whenever you’re sending money outside Spain or receiving income in another currency.

- Traditional backup: BBVA Cuenta Online — keep one if you eventually need it for a mortgage, for Spanish bureaucracy, or as a fallback. But don’t pay fees for it.

If you are a freelancer or digital nomad who wants additional budgeting automation, also consider bunq, which has a Dutch banking license and supports multi-IBAN sub-accounts. For a broader look at digital banking options across Europe, see my guide to the best online banks in Europe. If you’re also looking at investment accounts, I’ve covered the best stock brokers in Spain separately.

Spanish Banking Glossary

Spanish bank documentation loves jargon. Here’s a quick reference for the terms you’ll encounter most often.

- Cuenta corriente — Current account. Your standard everyday bank account.

- Cuenta de ahorro — Savings account. Usually offers a small interest rate and may have withdrawal restrictions.

- Tarjeta de débito — Debit card. Linked directly to your account balance.

- Tarjeta de crédito — Credit card. Spend now, pay later. Spanish banks often push these aggressively — be careful about accepting credit products you don’t need.

- Domiciliación — Direct debit. The instruction you give to allow a company to pull payments from your account. This is why the Spanish IBAN matters — many Spanish companies will only accept domiciliaciones from ES IBANs.

- Transferencia — Bank transfer. Standard SEPA transfer.

- Bizum — Spain’s instant peer-to-peer payment system, linked to your phone number. Essential for splitting bills with Spanish people. Available on N26, Revolut, and bunq.

- NIE (Número de Identificación de Extranjero) — The tax ID number required for most financial and legal activity in Spain as a foreigner. Get this sorted early.

- DNI (Documento Nacional de Identidad) — Spanish national ID. Only applicable if you’re a Spanish citizen.

- Comisión de mantenimiento — Account maintenance fee. What you’re trying to avoid.

- Seguros — Insurance products. Spanish banks cross-sell these constantly. Home insurance, life insurance, payment protection — often attached as conditions to loans or mortgages. Read the fine print before agreeing to anything.

- Hipoteca — Mortgage. Spanish mortgage law changed significantly in 2019, giving borrowers more protections. If you’re buying property, get independent legal advice.

- Comisión por descubierto — Overdraft fee. Going into negative balance in Spain triggers automatic fees that can compound quickly. Keep a buffer.

Final Thoughts

Spanish banking in 2026 is genuinely better than it was a decade ago, largely because the neobanks forced the traditional players to improve. But the underlying culture — the bureaucracy, the discrimination, the preference for complexity over clarity — hasn’t changed much.

The smart move is to stop fighting the system and work around it. N26 gives you a Spanish IBAN without the Spanish banking experience. Revolut handles your travel and currency needs. Wise takes care of international transfers. And if you ever need a traditional Spanish bank, BBVA is the least painful option among the incumbents.

That combination covers everything. Use it.

Related

Retired British couple living in Spain with Residencia, own home, occasional trips back to UK. Bank with Sabadell in Spain (costly), Nationwide in UK to have cash for UK visits and buy grandchildren presents online with UK companies such as Amazon UK.

in Spain we have direct debits with Iberdrola and town hall etc so we need spanish Iban. Will be receiving an inheritance in uk in next few months. Will want to share this between UK family accounts and own spanish account.

Can’t choose between Revolut (do they or do they not have Spanish iban?) and Wise. Any advice?

Thanks for great advice so far.

Unfortunately BBVA do not accept foreigners (non EU citizens) to open a bank account even with an NIE and passport. I even went to the police and got a fresh NIE but this was still not good enough. BBVA wanted a Spanish photo id card that I could only obtain if I had a green card and lived in Spain.

So please strike BBVA of you list for non-EU citizens

Good to know, might be one of their derisking policies. Unfortunately it is becoming more and more common.

I have an account with the BBVA, I am a Spanish citizen and a UK citizen, and the BBVA CHARGES me for transferring Euros from the UK. Please correct your site

Thanks

Ephraim

Been with Sabadell for 9 years. The first few years they were great, then there started to be a few fees here and there but nothing major.

Then early this year there was an unexplained auto payment taken out for our expansion line. We quibbled it and overnight our expansion line was frozen with no explanation. We had just been assigned an account manager so we asked him to look into it.

While they were looking into it 1800 euros left our account (we didnt have 1800 euros in there) and we discovered that while they were looking into our account, they forgot to log out and then performed a bank transfer for a different person, hence the money leaving our account, they apologised (nothing in writing) and the money came back in two days later (half an hour before our autonomo payments were due to go out.

Three weeks ago there was another auto payment we didnt recognise, so we quibbled that. And then the next day our expansion line was frozen again, no notification or explination.

We spoke to someone on the phone and he said the only thing he could see is we were late with two payments in April (when they had emptied and frozen out account) but we need to go in to a branch and speak to someone face to face.

We just had our appointment and the manager refused to look at our account, wouldnt give us a name or number of anyone we could escalate it to, just said that the local branch would not be able to help with issue of expansion lines. Fine we said so who do we speak to? he said customer service. But they said you. Sorry i cant help you. Then he got annoyed that we werent listening to him. At no point did he ask for our details or look at the account.

I would strongly recommend never using Sabadell, We have a revolut and are opening a BBVA (for payments to Spanish Tax etc)

Hi Jean,

I’ve been dipping into your site/blog over the past couple of years and find it very informative, thanks for sharing your knowledge.

I’m now a Spanish resident and am looking to change bank, currently with bS Sabadell. I’ve got a UK Revolut account and am considering changing to the Revolut ES service. Do you know if the Spanish authorities now accept a Revolut account or any other challenger bank (N26/Wise) for direct debit to pay taxes?

Regards

Mark

Had an account with Sabaddell till last week and after a disagreement with lady at bank, closed my account and took the money (in cash). Went to Caixa today to open a free account, but told to buy insurance for a property I am helping my wife to buy – about 30 euro per month, so no free account and I am sitting with a lot of cash! Any advice?

Hi Jean,

Do you know of Non-resident accounts with Caixabank for non EU nationals?

I had caixa but there charges for non EU nationals have gone through the roof, like 40+ euros per month, so don’t bother.

I tried to use Spanish N26 for my Autonomo account but my accountant found that tax office will not accept their Spanish IBAN for direct debits of fees and taxes. Have you (or anyone else) had experience of this?

Appreciate any comments

I have the same issue with N26. It’s not accepted by the Spanish government for paying Spanish taxes using direct debit.

Anyone got a Selfbank account as a non-resident?

Just wrote to Sabadell re their commision-free account, and, if we understood each other correctly, they said there is no such account. 120€ a year account management fees they charge….

Bankia have now been acquired by Caixabank and the terms applicable to the Cuenta On account will be changed in November 2021 with charges of €36 per card per annum applicable from January 2022. Charges for some other accounts will be deferred until June/July 2022.

One account missing from this blog is the Cajarmar Wefferent account which is a no charge account as long as it is operated online. It is open to residents and non-residents. Non residents need to visit the branch to open the account. I understand that, if you visit a branch to undertake a transaction you would be charged €7 for that month which would cover any other visits made in that month.

I can now confirm, as I am now in Spain, that setting up a N.26 account for non Spanish residents is easy. It took less than 15 minutes, all via internet initially and then the app. I used my Spanish address for the account address and my UK passport/address for my tax residence. The app appears to need your location to check that you are where you say that your account is. Within minutes I was able to lodge money into the account and within 24 hours my debit card had been despatched.

I also set up a joint Wefferent non resident account with my wife at the El Campello branch of Cajamar. Initially the assistant suggested I do this myself online however when I told her that I had been advised that non resident accounts needed to be initiated at the branch she asked us to come in the following day. We brought passports, NIE, National Insurance, P60s etc to prove earnings. Also names, addresses etc of account holdersWe did not need utility bills or proof of property ownership. The assistant completed all of the forms and then provided us with initial user names and passwords to access the account. Lots of forms to sign but the staff were really helpful. The process took about 45 minutes. I hope this helps others.

I am six weeks behind you in trying to set up an account with N26 for use in Spain but their website does not seem to allow UK residents to open an account? Did you claim to be a spanish resident to overcome this? I am going out to Spain tomorrow so could easily do this…

Hi Peter,

Yes I stated that I was a Spanish resident using my Spanish address. I stated that I was from the UK and used my UK passport as personal ID. I can’t recall whether or not I needed my National Insurance number as Tax ID but worth having available. The app requested access to my location. I was at my Spanish address at the time so this may have been an additional security measure.

I hope this helps.

Hi just reading your comments and at first you say you set up an account as a non resident then in your 2nd reply you said you were a resident . We are looking to set up an account with an ES iban number ,but having problems as we are not residents, but do have our own appt .

Thanks Sue Holden

Hey I saw you use n26 for degiro but not sure it’s still up to date?

Need to open another account. We already have a Spanish account, Bankia, but need one that’s accessible in Ireland (for temporary work) without too many charges and also be able to bank a sterling cheque that’s arrived from HMRC whilst in Ireland. Urgent. Thanks

This page IS NOT as up to date as you claim. BBVA is my Bank and it’s a HUGE money grabbing scam of a Bank. They totally ignore the SEPA agreement and make illegal charges for € transfers from UK to Spain. Additionally they charge hundreds of €’s annually if you don’t comply with a mountain of crazy conditions. I’m having a very hard time finding even one decent Spanish Bank.

You can use N26 which works perfectly fine and has no charges. No need to trust Spanish banks.

BBVA charges me zero fees.

I shall probably give N26 a go, so thanks for that. I still don’t understand how you pay zero fees/commissions to BBVA though. You should look at the reviews of BBVA on Trustpilot, possibly the worst reviews i’ve seen. Thanks for replying.

Agree. N26 are the best. Was just trying to persuade them to add a “Spanish” IBAN to my account with them. No luck. The only way is to terminate the German (default) IBAN account I am using with them now and apply to new Spanish one. And all just beacuse some authorieties in Spain insist on Spanish bank for the Direct Debit yearly invoices (e.g. IBI)…

What is the best commission free bank account for non residents of Spain who need an account utilising direct debits and communion free withdrawals from ATM ?

I have attempted to open a Commission free account with BBVA but they say on the second page that this is not eligible to existing BBVA customers. I have a mortgage account with BBVA and they are now charging me 40euros per quarter maintenance charge despite me having Direct Debits for gas water electricity community charge and Suma.

Why should this be so, and why can I not open a commission free account as an existing customer?

Thank you for the information, Jean. This has been really helpful.

After a dreadful experience with Santander, I took your advice and opened an N26 account. I could not be more delighted. The process was easy, the app is user friendly, and I got my physical debit card within a week.

I have opened bank accounts in three Euro countries and Santander was definitely the most difficult. I had to visit a branch a number of times to sort things out.

I didn’t care for their attitude either. They acted like they were doing me a favour by opening my account. And their insistence on buying one of their financial products or the account would attract additional charges was off putting.

Traditional banking is going to die out, primarily because they have lost customer-focus and exactly as you stated – act as if they are doing us a favor.

In 2016, I purchased a flat in Barcelona and used Sabadell for my loan as the attorney said it had the best rates for a non-resident. I paid very little fees for my regular checking for a few years. Starting in 2019, the commissions and fees became astronomical. I was charged 59€ this quarter because I had a a higher balance in my account. I am also charged 30€ per year for my debit card, even though I have not even used my card in almost two years ( I can’t travel to Spain due to Covid restrictions).

I have to keep this bank due to my mortgage but I would like to store money in a better bank with less charges and just transfer the money over to pay the mortgage and expenses.

I do not recommend Sabadell at all. They are thieves.

Please can you tell me why a small non-profit making Association is charged €10 a month for holding a small amount of funds in the account, with very few movements through the year?

I am moving to Spain later this year on a Non Lucrative Visa and am currently starting the process of buying a property in Spain as a rental. I already have a NIE as I collected that recently upon visiting my parents who are now residents since last year. I am looking at which banks to join that suit me for 1. Bills inc. Tax payments as part of my future property 2. Online banking 3. english speaking 4. avoid all the fee’s and charges I am reading about. My lawyer organising my Non lucrative Visa mentioned too me N26 the bank I was originally going to use doesn’t offer the facilities for taxes etc concerning my house but can i confirm this is true, and does anyone recommend anything else ?