Lonvest is shaking things up in the P2P lending space with its recent expansion into Mexico. For those of us who’ve been watching the P2P world closely, this is a significant development. Lonvest has consistently delivered strong returns, backed by solid security measures, making it an appealing choice for anyone serious about maximizing their passive income. Let’s dive into why this latest launch is worth your attention and how you can take advantage of what Lonvest has to offer.

Lonvest is shaking things up in the P2P lending space with its recent expansion into Mexico. For those of us who’ve been watching the P2P world closely, this is a significant development. Lonvest has consistently delivered strong returns, backed by solid security measures, making it an appealing choice for anyone serious about maximizing their passive income. Let’s dive into why this latest launch is worth your attention and how you can take advantage of what Lonvest has to offer.

Why You Should Pay Attention to Lonvest

If you’re not yet familiar with Lonvest, it’s time to take a closer look. The platform has been steadily gaining traction among P2P investors for its attractive returns and commitment to investor safety. Here’s what sets it apart:

1. Attractive Returns

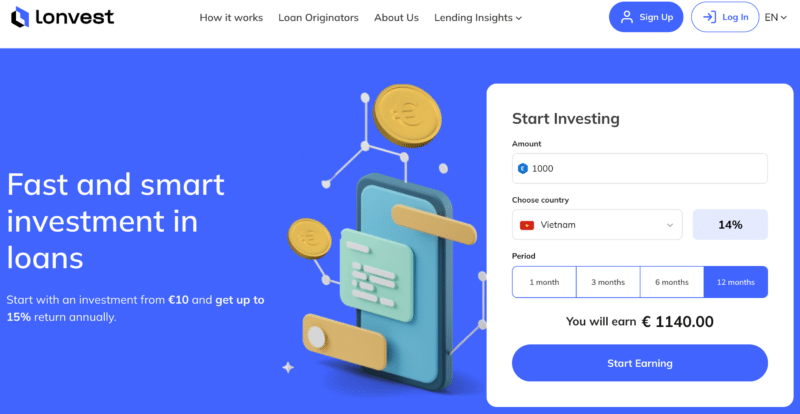

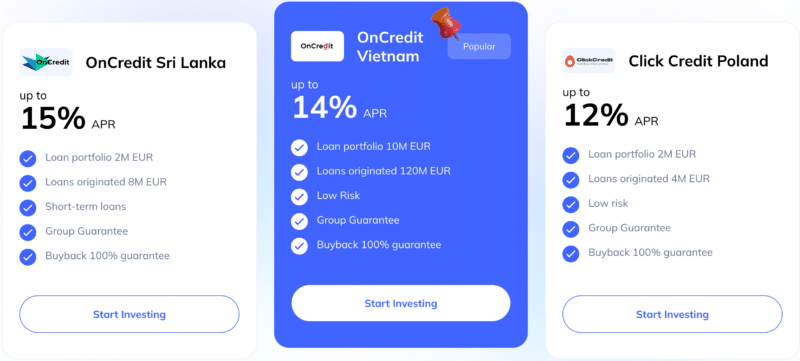

Lonvest’s entry into the Mexican market brings some impressive numbers to the table. We’re talking annual returns between 12% and 13% on loans that come with a buyback guarantee. In today’s market, finding these kinds of returns with such a level of security is not easy. This new opportunity allows you to get in early and capture higher yields before the rest of the market catches on.

2. Strong Security Measures

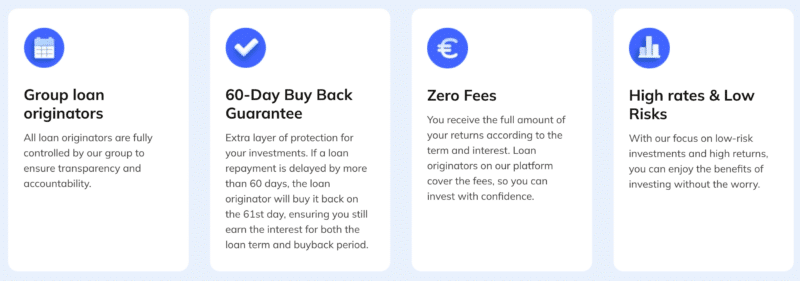

One of the standout features of Lonvest is its focus on protecting investors. They offer a 60-day buyback guarantee, which means if there’s a hiccup in repayments, the loan originator steps in and buys the loan back. On top of that, the loans are covered by a group guarantee from Space Crew Finance, providing an added safety net. These guarantees are particularly reassuring for investors who might be cautious about the risks associated with new market entries.

3. Transparent Fee Structure

Let’s face it: hidden fees are a drag on your returns. Thankfully, Lonvest keeps things simple—no sneaky fees that eat into your returns. All fees are covered by the loan originators, so what you see is what you get. This level of transparency ensures that investors receive their full earnings without unexpected deductions, making the platform stand out in the competitive P2P space.

Mexico: A New Frontier for P2P Investors

The Mexican market is an exciting new addition to Lonvest’s portfolio, and it’s a market with plenty of potential. While investing in new markets always involves a bit more risk, Lonvest has put solid measures in place to mitigate these. The Mexican loan originator is new, but with robust buyback and group guarantees, this venture offers promising returns with added security, making it an attractive option for those looking to diversify their investment strategies.

The focus here is on short-term loans, which is great if you’re looking for frequent reinvestment opportunities or prefer to keep your investments flexible. The dynamic nature of these loans lets you respond to market shifts quickly, keeping your strategy agile and adaptable.

What Makes Lonvest Stand Out?

User-Friendly Platform and Advanced Tech

Investing with Lonvest is straightforward, and their platform is designed to be intuitive, even for newcomers. Their use of AI-powered identity verification keeps things secure, which is crucial when dealing with any kind of financial platform. Lonvest has put in the effort to make sure the user experience is smooth, from sign-up to investment. The platform’s clear interface and ease of use make managing investments a hassle-free experience.

Proven Track Record

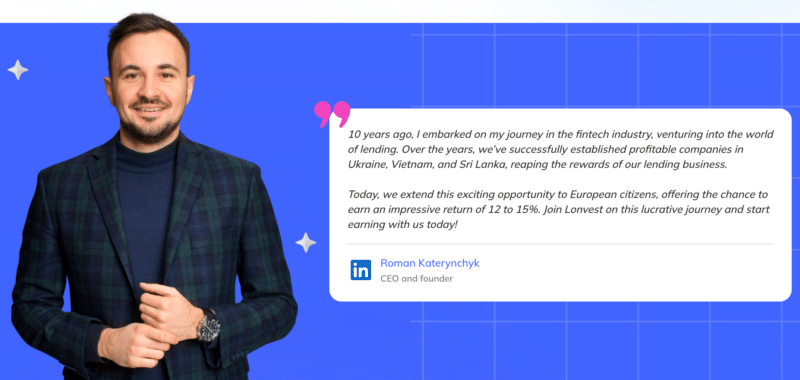

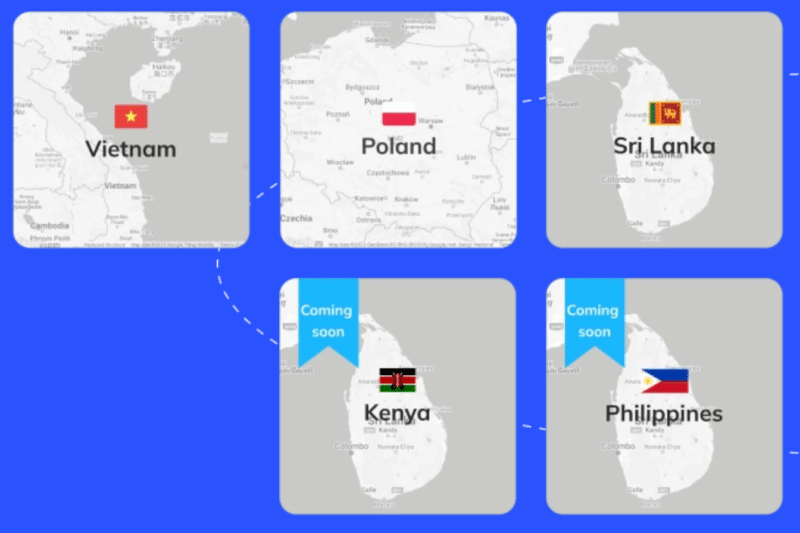

Lonvest’s success in other regions, like Vietnam and Poland, shows that they know how to navigate different markets while keeping investor returns high. Their adaptability and focus on maintaining robust security measures make them a reliable choice for P2P investors looking to explore new opportunities without compromising on safety.

How to Get Started with Lonvest

Thinking about giving Lonvest a try? It’s a simple process to get up and running:

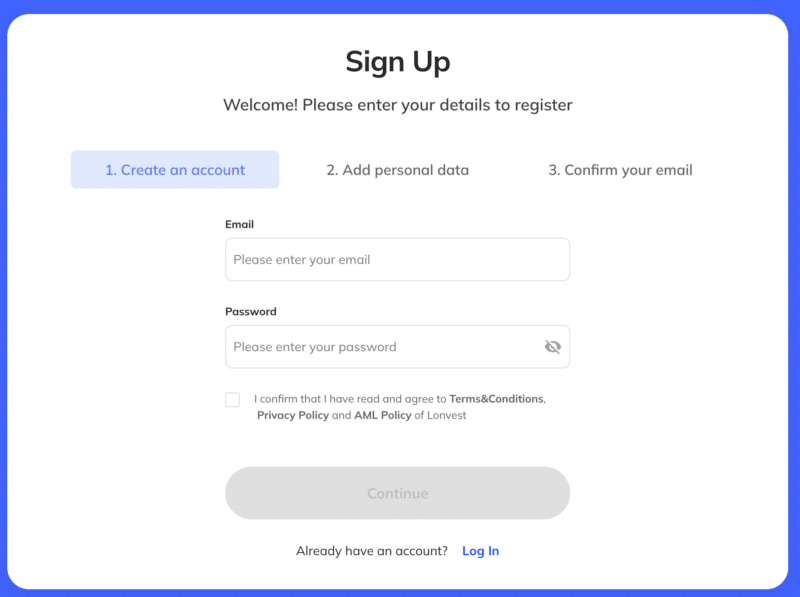

- Create Your Account: Registering is quick and painless. You’ll need to verify your identity, which is done efficiently with their AI-driven system.

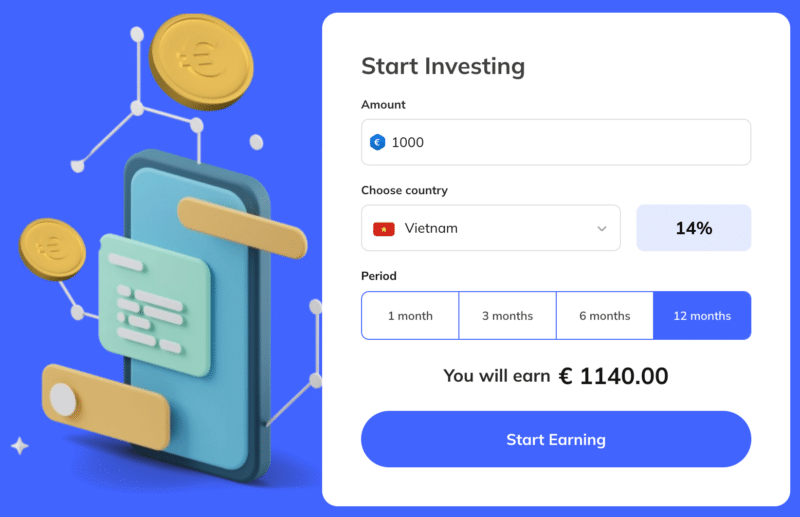

- Fund Your Account: Add funds via their Revolut account in Euro, which keeps things efficient and straightforward.

- Start Earning: Use their easy-to-navigate dashboard to select your investments, adjust your settings, and set up auto-investment if that’s your style.

Final Thoughts: Seize the Opportunity with Lonvest

Lonvest’s move into Mexico is a strategic step that offers P2P investors a chance to tap into a new market with high returns and excellent security measures. If you’re looking to diversify your portfolio and take advantage of a unique opportunity, Lonvest should be on your radar. The combination of competitive returns, robust guarantees, and a user-friendly platform makes it a standout choice.

Don’t miss out—explore what Lonvest has to offer and see how this new venture could fit into your investment strategy. As always, do your due diligence, but from my perspective, this is one of the more promising opportunities in the P2P space right now.