Spanish banking has improved, but it still has a long way to go. If you’ve lived here for any amount of time, you’ve probably dealt with opaque fee structures, branch-only services, staff who treat you like an inconvenience, and a general culture of extracting money from customers in ways that feel designed to confuse.

I’ve been living in Barcelona since 2012 and have been through the full Spanish banking experience — opening accounts, getting refused, watching fees appear out of nowhere, and eventually finding a setup that actually works. This guide is the result of that experimentation.

The good news: you no longer need to settle for a traditional Spanish bank as your primary account. Digital banks have matured significantly, and a combination of the right online bank plus one traditional option for backup will serve you better than anything a Caixabank branch can offer.

What You Actually Need From a Bank in Spain

Before getting into the options, it’s worth understanding what “working in Spain” actually requires from a bank account.

The key issue is the Spanish IBAN. Spain runs on SEPA direct debits, and a surprising number of Spanish companies — utilities, gym memberships, landlords, insurance providers, government services — will only accept a Spanish IBAN (starting with ES) for direct debits. Some will refuse a foreign IBAN outright, others will accept it in theory but fail in practice.

This is not a minor inconvenience. It affects your electricity bill, your internet provider, your health insurance, your Hacienda tax payments. If your bank can’t give you a Spanish IBAN, it cannot be your primary Spanish account.

Beyond the IBAN, you’ll want:

- No monthly maintenance fees (or very low fees for premium features)

- A debit card that works everywhere

- A decent mobile app

- English-language support (or at least a functional app that doesn’t require calling anyone)

- Access to Bizum (Spain’s peer-to-peer instant payment system — it’s used constantly here)

With that framework in mind, here are the banks I actually recommend.

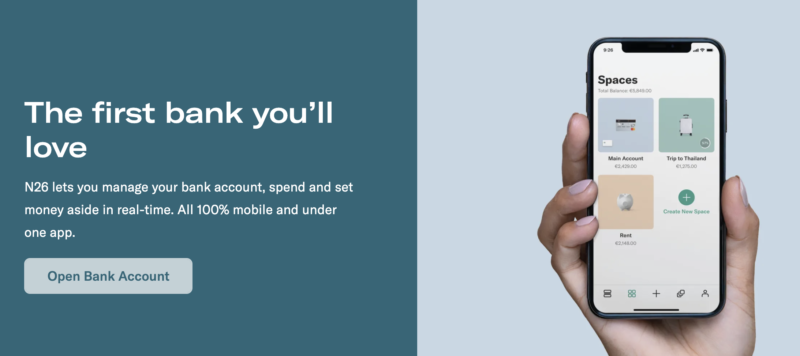

1. N26 — Best Overall for Expats in Spain

N26 is my top pick, and it has been for years. It’s a German bank (licensed by BaFin, Germany’s financial regulator), but it assigns every Spanish customer a genuine Spanish IBAN. You get all the protection of a German bank with an account that behaves like a local one.

This matters more than it might seem. I’ve had zero issues setting up direct debits with Spanish companies using my N26 IBAN — utilities, subscriptions, everything. It just works in the way a Spanish IBAN is supposed to work.

A few things that make N26 stand out beyond the IBAN:

- Desktop access. N26 has a proper web interface, which matters when you’re doing anything requiring a real screen. Revolut has a web app (app.revolut.com) but it’s limited, so N26’s desktop experience is considerably better.

- Clean, fast app. Instant notifications, clear transaction history, easy controls for freezing your card or adjusting limits.

- Bizum support. Available on all plans, so you can split a restaurant bill or pay the plumber without friction.

- Wise integration. International transfers are handled through Wise directly inside the app, which means mid-market exchange rates when sending money abroad.

- €100,000 deposit protection under the German Deposit Guarantee Fund.

N26 has over 8 million customers across Europe, and it’s been operating since 2013 — this is not a startup experiment. That said, it’s Europe-only; if you move outside the EU, your account gets closed.

N26 Plans in Spain

- Standard — Free. No monthly fee, Spanish IBAN, Mastercard debit card, Bizum. This is all most people need.

- Smart — €4.90/month. Adds sub-accounts (Spaces), partner discounts, and a choice of card colors.

- Go — €9.90/month. Travel and purchase insurance through Allianz, unlimited free ATM withdrawals abroad.

- Metal — €16.90/month. Premium metal card, comprehensive insurance package, airport lounge access discounts, higher ATM limits.

The free Standard account is genuinely good. I’ve used it as my primary Spanish account without ever feeling like I was missing something essential.

Read my full N26 review for a deeper breakdown.

2. Revolut — Best for Everyday Spending and Travel

Revolut is the most feature-rich neobank out there and, with 70+ million customers, it’s become the de facto spending card for anyone traveling through Europe. Currency exchange at interbank rates, instant spending notifications, easy card controls, a solid budgeting interface — it’s genuinely excellent for day-to-day use.

Revolut now offers Spanish IBANs. If you open a Revolut account in Spain today, you’ll automatically get an ES IBAN. Existing customers with Lithuanian IBANs are being migrated to the Spanish branch — once migrated, you get an ES IBAN as your primary identifier (your old LT IBAN still works). So the old objection about Revolut not working for Spanish direct debits is no longer valid.

That said, I still rank N26 above Revolut as a primary Spanish account. N26 gives you proper desktop access (Revolut’s web app exists but is limited), BaFin regulation (the strongest in Europe), and a longer track record of seamless Spanish IBAN functionality. Revolut is the better spending and travel card; N26 is the better bank account.

That said, Revolut earns its place as a powerful companion account. Use it for:

- Spending abroad — currency exchange at interbank rates with no markup on the standard daily limit

- Splitting costs with friends through the app

- Holding and converting between multiple currencies

- Budgeting and analytics features

- Cryptocurrency and stock trading (paid plans)

Revolut is still mostly a mobile-first experience. There is a web app at app.revolut.com for basics like checking balances and making transfers, but it’s limited compared to the mobile app. If desktop access matters to you, N26 is the better primary account.

Revolut Plans in Spain

- Standard — Free. Currency exchange up to a monthly limit, basic card controls, Bizum.

- Plus — Low monthly fee. Priority customer support, purchase protection, higher limits.

- Premium — €8.99/month. Unlimited currency exchange, overseas medical insurance, higher ATM limits.

- Metal — €15.99/month. Metal card, cashback on card payments, comprehensive travel insurance.

- Ultra — €45/month. Concierge service, highest limits across the board, exclusive Ultra card.

The free Standard plan is useful for travel and currency exchange. Most expats living in Spain will find Standard or Plus sufficient as a secondary card.

Read my full Revolut review or the N26 vs Revolut comparison if you’re deciding between the two.

3. Wise — Best for International Transfers and Multi-Currency

Wise (formerly TransferWise) isn’t a bank — it’s an Electronic Money Institution regulated by the FCA in the UK. That distinction matters: your money is safeguarded but not covered by traditional deposit insurance schemes the way a licensed bank would be.

For international transfers, though, Wise is in a category of its own. It uses the mid-market exchange rate — the real rate you see on Google — and charges a transparent, low percentage fee. No hidden spread, no inflated exchange rates, no surprise charges on the receiving end.

The Wise account also gives you local bank details in over 10 currencies, including EUR, GBP, USD, and AUD. If you receive income in multiple currencies, or regularly send money to family abroad, this is genuinely useful.

Where Wise fits in a Spanish banking setup:

- Receiving international payments in foreign currencies

- Sending money internationally (especially outside the EU)

- Holding balances in multiple currencies simultaneously

- Complementing N26 when you need to do cross-currency transfers

I wouldn’t use Wise as a standalone Spanish account — it’s not designed for that. But as part of a multi-account setup alongside N26, it covers a gap that neither N26 nor Revolut quite fills for complex multi-currency needs.

Read my full Wise review for more detail on how it works. If you also use PayPal for client payments, see my complete PayPal guide for online businesses for how to minimise currency conversion losses.

4. BBVA — Best Traditional Spanish Bank

If you need a traditional Spanish bank — for a mortgage, for dealing with Spanish bureaucracy that insists on a “real” bank, or simply as a backup — BBVA is the one I’d point you toward.

Their Cuenta Online is genuinely commission-free — no maintenance fees, no minimum balance requirements, no conditions. This is notable in Spain, where even “free” accounts often have hidden strings attached. BBVA’s mobile app has consistently won awards and is far better than anything offered by Caixabank or Santander. They also offer English-language service, which alone puts them ahead of most Spanish banks.

BBVA won’t replace N26 as your primary account — the experience isn’t as clean, and you’ll occasionally have to deal with branch visits and Spanish-language bureaucracy — but it’s the most competent of the traditional options and worth having in your toolkit for situations where a local bricks-and-mortar bank is required.

Banks to Avoid (or Be Cautious About)

Sabadell

I had an account with Sabadell for a while and I’d steer clear. The fee structure is opaque, customer support is poor even by Spanish banking standards, and their online banking interface — despite recent updates — still feels like it was designed in 2008. There are better options at every price point.

ING España

ING used to be my top recommendation for commission-free banking in Spain, and for a while it genuinely was. Then things went sideways.

ING has a policy of letting all incoming international transfers through without question — and then, months later, suddenly demanding documentation about every single one of them. I’m talking about transfers that were already processed and settled. They wanted proof of origin, invoices, contracts — for transactions that in some cases were years old. Retrieving all of that is enormously time-consuming and stressful, especially when you’re a freelancer or business owner with complex income sources.

Worse, during the COVID crisis they blocked clients’ accounts while all of this was going on. People who needed access to their money — during a pandemic, when families were under real financial pressure — were locked out. I find that kind of behavior indefensible. A bank’s job is to help during difficult times, not pile on more difficulty.

Their customer support is phone-only, with long wait times, and the staff can barely answer basic questions. On top of all that, the Cuenta NÓMINA is now conditional — you need a minimum monthly salary deposit to keep it fee-free, which rules out most freelancers and self-employed people.

Stay away from this bank.

Caixabank, Santander, and the rest

Spain’s big traditional banks are fine if you have no choice — and sometimes you genuinely don’t, for certain mortgages or specific financial products. But as primary accounts for day-to-day use, they’re expensive, bureaucratic, and their digital products lag far behind the neobanks. Unless you specifically need something only they offer, there’s no good reason to use them.

Documents You’ll Need

This is where a lot of people get stuck. Here’s what each type of account typically requires.

Traditional Spanish Bank (First Account)

Opening your first account with a traditional bank in Spain usually requires:

- Valid passport or EU national ID card

- NIE (Número de Identificación de Extranjero) — your Spanish tax identification number

- Proof of address in Spain (rental contract, utility bill, or padron municipal certificate)

- Proof of income or employment (payslip, employment contract, or tax declaration)

- In some cases: proof of legal residence status

Getting your NIE is the critical step. Without it, most traditional banks won’t open an account for you. The NIE application process involves a trip to a police station (or a Spanish consulate if you’re applying from abroad) and can take weeks. Sort this out early.

Traditional Spanish Bank (Second Account, Once You Have NIE)

Once you have an NIE and an existing Spanish bank account to show, the process is much simpler. Most banks will only need:

- Passport or national ID

- NIE

- Your existing Spanish bank account details

Digital Banks (N26, Revolut, Wise)

This is where the neobanks shine. The requirements are minimal:

- Valid passport or national ID

- A smartphone for identity verification (selfie + document photo)

- An email address

No NIE required. No proof of address. No visit to a branch. The verification is done entirely in-app and usually takes less than 10 minutes. For most expats, this means you can have a working N26 account within a day of arriving in Spain, long before you’ve sorted out the Spanish bureaucracy required for a traditional account.

The Discrimination Reality

I want to be direct about something that gets glossed over in most expat banking guides: banks in Spain discriminate, and they do it routinely.

My wife is Russian. She was refused by multiple Spanish banks before we found one that would open an account for her — not because of any issue with her documentation or finances, but simply because of her nationality. The refusals came without explanation, in the way that Spanish bank staff sometimes refuse things without telling you exactly why.

I’m Maltese — an EU citizen. I was refused at one bank despite Malta being a full EU member state. The staff member apparently wasn’t familiar with Malta and decided that was grounds for refusal. No appeal, no escalation, just a polite no.

This is the reality for a lot of non-Spanish, non-Western European people living here. The discrimination is usually informal rather than codified policy, but it’s consistent enough that you need to account for it. Traditional banks have discretion in who they accept, and they use it.

The practical implication: digital banks like N26 and Revolut don’t have this problem. Their verification is automated and nationality-blind. If your documents are valid and you pass the KYC check, you get an account. This is one of the strongest arguments for making a neobank your primary account rather than trying to force a relationship with a traditional Spanish bank that may not want your business.

My Recommended Setup

Here’s what I’d suggest for most expats in Spain in 2026:

- Primary account: N26 Standard — free, Spanish IBAN, works for all direct debits, desktop access, Bizum. This is your main account.

- Secondary account: Revolut Standard or Plus — use it for travel, foreign currency spending, and any situation where the Revolut feature set is useful.

- International transfers: Wise — whenever you’re sending money outside Spain or receiving income in another currency.

- Traditional backup: BBVA Cuenta Online — keep one if you eventually need it for a mortgage, for Spanish bureaucracy, or as a fallback. But don’t pay fees for it.

If you are a freelancer or digital nomad who wants additional budgeting automation, also consider bunq, which has a Dutch banking license and supports multi-IBAN sub-accounts. For a broader look at digital banking options across Europe, see my guide to the best online banks in Europe. If you’re also looking at investment accounts, I’ve covered the best stock brokers in Spain separately.

Spanish Banking Glossary

Spanish bank documentation loves jargon. Here’s a quick reference for the terms you’ll encounter most often.

- Cuenta corriente — Current account. Your standard everyday bank account.

- Cuenta de ahorro — Savings account. Usually offers a small interest rate and may have withdrawal restrictions.

- Tarjeta de débito — Debit card. Linked directly to your account balance.

- Tarjeta de crédito — Credit card. Spend now, pay later. Spanish banks often push these aggressively — be careful about accepting credit products you don’t need.

- Domiciliación — Direct debit. The instruction you give to allow a company to pull payments from your account. This is why the Spanish IBAN matters — many Spanish companies will only accept domiciliaciones from ES IBANs.

- Transferencia — Bank transfer. Standard SEPA transfer.

- Bizum — Spain’s instant peer-to-peer payment system, linked to your phone number. Essential for splitting bills with Spanish people. Available on N26, Revolut, and bunq.

- NIE (Número de Identificación de Extranjero) — The tax ID number required for most financial and legal activity in Spain as a foreigner. Get this sorted early.

- DNI (Documento Nacional de Identidad) — Spanish national ID. Only applicable if you’re a Spanish citizen.

- Comisión de mantenimiento — Account maintenance fee. What you’re trying to avoid.

- Seguros — Insurance products. Spanish banks cross-sell these constantly. Home insurance, life insurance, payment protection — often attached as conditions to loans or mortgages. Read the fine print before agreeing to anything.

- Hipoteca — Mortgage. Spanish mortgage law changed significantly in 2019, giving borrowers more protections. If you’re buying property, get independent legal advice.

- Comisión por descubierto — Overdraft fee. Going into negative balance in Spain triggers automatic fees that can compound quickly. Keep a buffer.

Final Thoughts

Spanish banking in 2026 is genuinely better than it was a decade ago, largely because the neobanks forced the traditional players to improve. But the underlying culture — the bureaucracy, the discrimination, the preference for complexity over clarity — hasn’t changed much.

The smart move is to stop fighting the system and work around it. N26 gives you a Spanish IBAN without the Spanish banking experience. Revolut handles your travel and currency needs. Wise takes care of international transfers. And if you ever need a traditional Spanish bank, BBVA is the least painful option among the incumbents.

That combination covers everything. Use it.

Related

ING has stopped its account SIN NOMINA in September 2018. Now if you want an account without commissions you still can have it but it has to be an online only account.

More info here (in Spanish): https://www.ocu.org/dinero/cuenta-bancaria/noticias/fin-cuenta-sin-nomina-ing

I used to think Revolut was an awesome account to have for traveling, and I WAS recommending it to everyone, but not anymore!

Customer support is non-existent! Avoid! Check the reviews before you take out a premium account.

A month before I was traveling to Dubai, Australia, New Zealand and Singapore, they sent me a message to verify a code they added to my last deposit. There was no code, so I contacted support. A couple days later they responded saying I will be contacted by compliance. 2 months later and after sending them many messages, I am still waiting and my account is suspended especially after witnessing their child-like responses.

I have requested their complaints procedure and they will not send me anything. There is no other method to contact them.

I have now asked for a refund from my premium account and cancel the account. That was a week ago and still no response.

My next move is to report them to the financial ombudsman.

Why EVO Banco is not included?

Based on your list, I opened an account with Sabadell back in 2018, now I’m looking for a replacement as they will start charging fees quarterly on Expansion accounts.

Spanish banks are great, customer service is perhaps debatable, however the technology is highly advance to carry out your day to day payments, wire transfers and consists of user friendly apps. On the other hand it is true that the service and maintenance charge is quite high whereas a lot of Bank offers online accounts if one wishes to avoid fees.

According to my experience and opinion, people with jobs/businesses earning above 900 euros may seek for a Brick-And-Mortar Bank (having the option to operate physically by visiting a Bank) and may choose any of the Spanish Banks. In addition, there are people who are unemployed or earn from time to time and even students may consider opening an online account, and my suggestion will still be choosing a Spanish Bank.

Both type of users are somewhat privileged to visit their respective Bank offices but mostly clients (having a traditional account) will get efficient and rapid feedback to their queries and their problems will be sorted out quickly. Online users can as well benefit from these sort of services but it may cost them a charge, response may be delayed and even there might be limitations. To me, You get what you paid for, no complain from my side. A couple of them only operates online without any offices that I am not comfortable with and I rather prefer to visit an office than talking or chatting to a representative over the phone in finding solution to my problems. And lastly, regardless whether you are opting for an online or tradition account, do not forget to check their offerings like discounts, interest on deposits, ATM fees and other facilities. Just shared my personal views.

This is how I rank some of the Banks : 1. Santander, 2. BBVA, 3. Caixa, 4. Bankia, 5. Open Bank, Caixa Popular, Liber Bank & ING.

Great article, thanks for publishing. I had an ING account years ago in Spain but now have a Sabadell. It’s crippling me as I have to send Euro 700 a month into it – otherwise it’s free!! So I’m looking for an alternative that is low or free from charges without this crazy monthly deposit. Any suggestions or advice?

Hi,

May I suggest you get the Revolut App. I use this to transfer money every month to my Sabadell account. I send 250 to sabadell. Once credited I send it back to Revolut, I repeat the process until I’ve hit the minimum deposit. It’s free and takes seconds over a 4 day period.

I have the same account (“Expansion”), but unfortunately from 01/01/2020, it’s no longer free. 🙁

“maintenance fee will be €15 quarterly”

https://www.bancsabadell.com/cs/Satellite/SabAtl/Expansion-Account/1191346505022/en/

That’s not good news, thanks for the update.

I can second that. Sabadell expansion added conditions to be free, either be younger than 30 or you could upgrade to their premium account, but take additional insurance.

30 Euro/quarter fee, or 15/Q, but again with conditions (average 2.5k Euro in account)

I’ve never had to pay in my life for bank accounts, with greatest conditions. I’m not going to start now…

Thanks for the article, I’ll be using it to help me find my next match 🙂

Good luck 🙂

Unethical and amoral bank! Sabadell made an admin error in Summer ’19 whereby they charged me twice for an Airbnb stay without adjusting the balance to make me aware of the lack of funds I now had due to this double charge. It happened at a financially critical moment during my stay in Spain which forced me to arrange an emergency loan in order to pay for a flight back to the UK.

Sabadell have refused to compensate me for their error which put me in the financial predicament and subsequent debt. They have communicated with me in an unprofessional way, accepting my complaint PDF file from my email address yet refusing to send the outcome back to my email address.

Furthermore, Sabadell fails to keep its ATMs in Madrid stocked with banknotes. One of the reasons why I chose Sabadell is because two of their ATMS were close to my apartment in Chamartin. Yet one, sometimes both, ATMs were out of money, costing me ATM charges using other banks’ ATMS.

Over all the bank’s conduct, certainly in the handling of my complaint and claim for at least some renumeration due to Sabadell’s maladministration, has not matched the standards required for an EU banking institution and I am currently seeking advice from the EU’s Financial Ombudsman as a result.

I’m with Bankia and been told that I don’t qualify as an existing client to set up an ON account. This is so out of line compared with the UK.

Banks in Spain are regarded as predatory in their fees and charges so don’t get to comfortable with this one, which was the biggest to fail in the recent crisis. I’m looking for another bank but one way or another they all fall short in the reviews. Expect to pay a monthly fee with some like N26. Compare notes with me if you wish

Sorry to hear that Barry. I’d say the entire financial sector in Spain is of a predatory and unprofessional nature (admittedly I’m generalising). You can sign up to the N26 free account with no monthly fees.

Thanks for the excellent article Dominic. In my case, I will be making regular transfers into the account from the UK (in GBP). Do you know if either Bankia Now or ING Direct would add charges to receive those payments?

Excellent post, very interesting! I want yo share with you guys something that could be useful for you to know and It is that Sabadell bank allows you to open a dollar account (Cuenta Divisas, witch is like to say “currency account” or something like that) actually It is called so because you can have whatever currency you want to have in there, not only dollar. It’ not free, but I think it’s not that expensive, around U$ 10 monthly. This way you can avoid the currency exchange fees (witch are truly high).

What I would like you to tell me is if you know some good and not expensive, but “reliable” broker I could link my bank account with in order to buy-sell stocks.

Thanks in advance.

Hi Leonardo, check out my post about brokers in Spain.

I have a Cuenta On account with Bankia. I own an apartment as a non resident and opened the account in September 2018. The account is free of management charges as long as the account is managed online.

On 16th December I received a letter (via Bankia’s online messaging system) containing revised terms and conditions. My understanding of the letter (9 pages long) is that current users of the Cuenta On account are being moved, on 23rd February 2020, to another account type: “Por Ser Tu” which appears to have much more stringent conditions for it to remain free of charges.

The Cuenta On account is still available to new clients.

I just wondered if anyone else has this account, has received the letter and has formed the same view as me (the letter was in Spanish and I could not guarantee my interpretation is 100% accurate.

Hi Tony.

I opened a Cuenta ON around the same time as you (although as a resident, rather than a non-resident) and I’ve just discovered the same letter in my inbox.

The letter sets out new conditions for around 15 of Bankia’s account types, stating that the Por Ser Tú programme will apply to them from 23 February 2020. Under this programme, account holders are exempt from account maintenance charges and annual card fees as long as they have their pay cheque, pension or unemployment benefit paid into their account every month. If not, there will be a monthly account maintenance charge of either 6 euros or 14 euros (!) per month, depending on whether the holder also meets certain other conditions, PLUS a charge of 28 euros per year for the debit card.

As I read through this letter (9 pages long, as you say), I was all set to close my account. However, I then discovered this paragraph at the bottom of page 8:

“Comisión de mantenimiento Cuenta On: la comisión de mantenimiento de la Cuenta On seguirá siendo de cinco (5) euros mensuales. No obstante, si cumples el perfil digital, la comisión de mantenimiento de la Cuenta On y la cuota anual de la Tarjeta de Débito On será de cero (0) euros.”

If I understand this correctly, this means that the exemption from account maintenance and card fees that we currently enjoy will continue as long as we maintain the account online and have the mobile app set up correctly. (There are full details of the requirements at the top of the same page.) If not, then we revert to the terms of Por Ser Tú.

I’m going to check this with my girlfriend, who is Spanish, just to make sure she interprets it in the same way. However, I think I’ve got it right. The letter is certainly written in a confusing way, because everything apart from that one paragraph suggests that new charges will be applied unless we meet the terms of Por Ser Tú.

It’s also worth mentioning that on page 7 the letter quotes my account number along with “Denominación Actual: Cuenta ON” and “Nueva Denominación: Sin cambio”, indicating that the account will remain a Cuenta ON. You should check that this is also the case for your own account.

Hope this helps!

Hi Dominic

Thanks for your extremely helpful response. In the meantime I had emailed Bankia and also messaged them on Facebook and both channels responded by stating that the Cuenta On account remained free of commissions as long as the digital profile was maintained. They confirmed on FB that my digital profile was correct. Judging from their FB site I am not the only one to conclude that the majority of the Bankia accounts were being migrated to their Por Ser Tu programme – many Spaniards had assumed the same. On another matter I’ve also had deductions made from my account for both of our joint account debit cards. I received a response to a written complaint recently that stated that these will be refunded. It has yet to happen but at least I’ve had a positive response. I don’t want to move banks as I like the Bankia app and they do respond to the various contact channels – not always clearly though.

Thanks again

Tony

That’s great news! I’m really pleased that you had a positive response from Bankia.

My girlfriend agreed with my interpretation of the text, although she also felt that it was confusing – especially with the added reference to a 5 euro monthly fee (instead of 6 or 14) if one doesn’t maintain a digital profile. We were debating whether to go and check with my gestor at the local branch, just to be absolutely sure.

The responses that you’ve received do give me added confidence, though. Many thanks for following up on my reply.

Hi,

I’m also received the online message about tariffs and am a non resident. Today have made 3 phone calls to Bankia regarding configuration of my Cuenta_ON account. One said my account is ok, 2nd said need to setup profile / notification alerts (setup 5 Cuantas & 1 Tarjetas) and 3rd said create profile / notification alert otras / Acceso a canales digitales.

Hi Jean and other readers.

Jean, thanks again for your excellent post / page.

I wanted to add a bit of info from my experience so far.

Firstly, like you i had initial good experience with ING on a day to day basis, where i had issues was there “Checking info” policy that you have described, that department has the task of checking up on automated security notices. This are now standard and from what i can see the politicians have passed on this responsibility to the banks. So there now caught between the middle of having to collate info about transactions to cover their backs. But….. some banks are better at dealing with the communication of this process. I’m afriad ING in Spain is very poor, frustrating and lacking understanding of how to deal with its customers.

I moved to N26, that as you mention do seem very good.

The only issue i have encountered is that they do not have a list of “commission free” ATMs for you to use. I spoke to the agent, its trial and error. Put your card in and see if they charge for a fee & cancel. The money will be debited & then refunded. But it is in this day and age a slightly inefficient way for customers to find out.

Does anybody have any recommendations for commission free ATMs in Spain? (As of 30 December 2019)

Hi Jean Good evening,

I would like to ask you two questions and It would be helpful if you kindly answer them based on your knowledge and experience.

1. Will I be questioned if I intend to receive a total below 10000 euro through a Bank transfer to my Spanish account from another EU country ?

2. The money is going to be sent like a gift for my personal use and I am thinking of opening a small business as well. Will that be an issue ?

Waiting for your answer and thank you in advance.

Hi Alek,

1. Impossible to answer unfortunately as banks don’t publicly share their policies and it depends on a ton of factors anyway.

2. As far as I know, gifts are taxable when received by a Spanish resident, so you’d probably first need to discuss that with your tax advisor.

Hello Jean,

Good post. Perhaps you wish to take a look to Abanca and Evo Banco, or even Ferratum (a Maltese bank for EU nationals in EU including Spain).

One question, if you had to compare access to banking between Maltese and Spanish banks, who would you say is less pain in the ‘bottom’?

Narak!!

Thanks for the suggestions. For opening a bank account and technology (apps, web etc) the Spanish banks are far superior. For reliability and fees the Maltese ones are better.

Hi Jean,

Good site!! My question, we want to live in Spain as non-resident (so max 6 Months), and we like a simple Bank solution as N26. Is it possible to use N26 as “non-resident”? I had a chat with N26 online, but the support person was not 100% sure. He basically said: just try when you are in Spain 🙂 But we are not there yet.

Thanks for your reply

Bob

It will work, as long as you have an Spanish address when you signup, if you do not have a Spanish address when you signup you will probably get their German IBAN account number, and you will have problems when you are going to sign up for direct debits like phone, internet, power, and water. I would recommend to wait for signing up until you have an Spanish address, I would guess even the address for an airbnb would work – you could just change the address father you get the Visa debit card.

Hi Jean

Thanks for writing the article, really useful. I started googling ING, as i too am having issues with incoming transfers. Exactly as you mentioned, all fine. Now they seem to have blocked all incoming transfers from services like” Transferwise, Revoult.”

I think your right, there not up to speed with managing incoming foreign transfers. We all know that banks have to be careful in the age to help protect us. But likwise i’m being asked to provide information from 20 years ago. I don’t know what will happen next, wether i can move my money away or i will get more calls. Off course we can provide information, but as you mention in your article. Its quite random the requests and in some cases impossible.

How did it eventually work out for you?

As i belive im now in that same situation.

Once again, thanks for writing and sharing as now realise its not just me.

Hi Rich, thanks for commenting on the issue. From my conversations with them it seems that they are just ticking boxes. There seems to be a total disconnect between management and the people who are sending out emails and replying to phone calls about these issues. Basically whenever I spoke to them they struggled to even understand what I was calling about then scrambled to find out why they were actually asking me for the information, and finally concluding by repeatedly asking in a bit of a menacing way whether I would send the information. In the end given the ridiculous requests I decided to wait it out and so far nobody has contacted me again.

Hi Jean – I am in the process of relocating from South Africa to retire in Spain. I have therefore read your blog with interest. Whilst I have an EU passport, I dont have a NIE number yet. I will be travelling to Spain in September to try and sort out a lot of things, bank acount being one. Will I be able to open an account online from South Africa or should I do it when we’re there in September?

Also, trustpilot has terrible reviews of ING-Direct? https://www.trustpilot.com/review/ingdirect.es

I would definitely recommend that you open the account once you’re here. ING Direct still works well for me but they do have several bad reviews as you stated. The only problem I’ve encountered is their average customer care and annoying justification requests for incoming transfers.

As I state in the post, if I were to open my accounts from scratch today I would do away with the archaic Spanish banks and use N26. I have an account with them and have had zero problems so far, and you get a Spanish IBAN so you can use it for things like renting an apartment or gym memberships where they need direct debit access.

Visited N26 website and chatted online to a consultant. They do not offer credit cards, no joint accounts and no term deposit accounts at this stage, which is what I require. Other than that, their mobile app and web platform is very slick and mod with great features and look-and-feel. As a simple mobile banking offering/app it’s first class.

Hi Jean!

Thanks for the useful post.

You mention Open Bank in the list but you didn’t review it then.

I’ve seen poor reviews here: https://www.trustpilot.com/review/openbank.es

Any thoughts?

Thank you!

I haven’t tried them so I would rely on the Trustpilot reviews and stay away from them unless the ratings improve. I would only recommend N26 at the moment.

Currently with Sabadell, get charged 30 euros a year for a card…which I have to have to put cash into the account as staff refuse to do this now!

In addition, I’m charged 30 euros every 3 months!!? And also accrue other “charges/commissions” which they cannot explain to me what they are for!? A 5 euro payment to local school parents group had a “charge” of 6:55!!!? MORE than the charitable group receiving it…every child in every school at E6:55 cents is a very good day for Sabadell!

Following the change in LAW I asked to have a “Basic Banking Account” as entitled to by LAW…after numerous attempts to convince me that this or that was required and my proving it wasn’t… they told me “If you are not happy, go to another Bank”

The Manager…said that?!!!

Thieves, liars and arrogant #@£% that care nothing about their customers.

Check out the caja mar wefferent account. No commissions or maintenance fees. Apply online only. Courier comes to do door to sign papers then card comes in post. Cajamar.es

Has broker options and decent app. Card is a bit ugly and the name is questionable but account good.

I think this caja mar offer is the best, I did prefer bankia but they closed my account after I transferred a big amount of cash in and refused to accept evidence of the origination of funds. They also threatened to confiscate my money and I was quite worried.. I would still recommend bankia for small holdings and free cash withdrawals, cuenta on account.

Self bank have dripped association with CaixaBank so not such a good proposition any more. N26 is a better option now than self bank. 5 free withdrawals a month instead on 1 with self bank.

Finally jean, your blog helped me a lot getting set up in spain so i hope this information helps someone else. Thanks

Glad my blog was helpful Jonny. How did it end with Bankia, did they send the funds back or allow you to transfer them to another local bank?

Hello, i’m creating an offshore company in Spain and i need an account in a spanish Bank. The company through which i’m creating my company suggests i use the banks in this list http://www.confiduss.com/en/banks/list/spain/ . What do you think, which bank should i choose?

I stand by my recommendations so far, and I haven’t tried all the banks mentioned in that list so I can’t comment on those.

N26 don’t support non resident accounts. I’ve tried to open an account and if your tax liability is in the UK then you can’t open the Spanish account, even with a Spanish address.

Just worth noting..

Hi Jean,

I notice that you now recommend N26.

There’s more good news.

N26 have recognised the difficulties in Spain where companies appear to ignore European law requiring acceptance of all bank accounts throughout the Eurozone. So, new N26 customers in Spain are now given a Spanish IBAN rather than a German IBAN. Existing customers will be able to switch from a German to a Spanish IBAN.

This should overcome the difficulties of deliberately awkward companies like Movistar!

Life gets better all the time…

Yes, see my latest post on the blog 🙂

I had very bad experience with openbank. They made it hard for me to open an account, including requesting me to visit a santender bank and make 10 euros transfer. I felt like its a scam. I opened an account without problems in sabadell.

Surprised you first mention Open Bank as an alternative, then list other banks but not Open Bank and lastly recommend no banks at all. I’ve been a customer of Open Bank for 5 years. Never paid anything for my account or card. The website is in Eng/Spa and so is their app. Check it out!

I don’t speak Spanish. I’ve sent a query to ING about opening the account in English. Reply came in Spanish. I’m so done with this. Any recommendations? Revolut doesn’t work, it’s not recognized by authorities as a Spanish account, I cannot even use their card to recharge my prepaid phone.

Update: I asked if they could answer my queries in english. Got an arrogant reply that they only provide services in Spanish. The reply came, of course, in Spanish. This from their official Facebook account. They really work hard on not having me as a client. Any suggestions?

Unfortunately I’m not surprised as this happens quite frequently and not just with this bank but with the majority of businesses in Spain. It’s mostly due to them not being equipped to support English-speaking clients rather than any malice, although I understand how sometimes it does come across as arrogant as they lack the apologetic attitude typically taken by support in English-speaking countries. I have learnt Spanish myself so I’m afraid I can’t really give you any suggestions.

I’m not even from an English speaking country and I’d consider their reply rude. I just moved here and the only other languages that I speak, apart from my native Czech, are English and German. I think I will go with Bankia for now, as they were prompt to answer my questions in English, even though some of the reviews here are not very favourable. I’m planning on learning Spanish, but this is my day #11 in Spain 🙂

Absolutely, you’re right to expect a nice reply and an accommodating attitude from any service provider. Bankia are heavily criticised by many, however my experience with them has been good, they’ve always been very nice to me at the branch. They also have Apple pay integration which Ing don’t have.

Hi Jean,

We have internet banking with Caixa Bank in Santander and have just had a message about KYC which appears to be about money laundering etc.

Some posts on the internet suggest that bank accounts can be frozen.

We have had out account for over 10 years and this is the first time this has been mentioned to us.

Can you give us some information on this please.

Thanks.

KYC can be annoying but as long as you provide the info they request there should be no problem. Accounts are only frozen in extreme cases where there are problems.

Hey Jean,

Checking ING and they only seem to have a cuenta nómina available now- which means there needs to be a minimum deposit each month (like the drawback you mention with Sabadell). Any suggestions for people that don’t have this option? (Aka starting one business with no guaranteed monthly income)

Hi I’ve recently moved to Spain for nine months – have started the bank account process,sadly with Sabadell before seeing these posts. My account is not fully open until they see my NIE which is on is way. How easy is it to cancel/close an account soon after opening? My language proficiency is not great!

My experience with Bankia is pure disaster. I speak Spanish (and English and German), and we have had accounts with Caja Granada (worked resonably well, except for some criminal action) and BMN (worked well), but since Bankia took over, the internet access is blocked. To de-block the access, I had to go to the branch, which I did about ten times. People there were friendly, but incompetent. I gave them all the documentation they claimed they needed (BMN did not need all that), and still no internet access. I cannot call in, because my identity card has letters and numbers, and the telephone machine accepts only numbers. We pay by direct debit things like power, IBI or telephone. I tried to change that process to the bank of my European homecountry, which is absolutely possible under European law – except that some companies do not want to do that. Without internet access, I don’t know, whether there is enough money in the account, so we get our power turned off. In my experience, Bankia is absolutely worthless.

Great info Jean !

However I just tried to open an account in ING bank and they only let me open it if I have the “tarjeta de residencia” only with my NIE and job contract they don’t open it.

You managed to open it only with your NIE?

Best Regards,

Elson

Tarjeta de residencia is a NIE. I’m not sure what happened there but you should definitely be able to open it once you present your NIE (it’s a flimsy card-like thing like this one).

NIE is foreigners identity number, which you can get easily. Residencia is a different accolade, meaning you are resident in Spain. I’m guessing ING no longer offer non-resident accounts if they require Residencia

NIE counts as residency, in fact on the card there is the date when you started residing in Spain. I did not need any other papers apart from perhaps empadronamiento or flat rental contract (I don’t remember if this was necessary).

Not any more Jean. They are two seperate applications, with different requirements. I believe they used to be one application for both, not anymore

Since when has this changed Richard?

I don’t know Jean. I moved to Spain in January and was advised by the translation service I used that it’s now two seperate applications. For Residency you have to provide proof of healthcare (private insurance not enough due to limitations on care covered), your NIE, a current Certificado De Empadronmiento, three months bank statements, proof of employment (translated by an official Spanish translator if not in Spanish language, plus all the usual identification and proof of address stuff. It’s a four to six week wait for an appointment with the Policia Nacionale around these parts

I think we’re talking about the same thing as those are the documents I needed to get my NIE (the one like I linked to in my previous comment). I know that there used to be a paper that gave you a NIE but not residency, and now with the card I have it serves both as a record of my NIE number as well as a residency permit.

Perhaps you can apply for residencia and nie at the same time, but one is not the same as the other. If you need residencia to open a resident account, having only an nie will not work as it isn’t proof of residency

If we’re referring to NIE purely as the number, then yes, I agree. If we are referring to the NIE as in the card I linked to, then I say it should be enough to prove residency.

Richard,

I was working in a spanish Bank for many years. Try in BBVA with nie and passport, easy on line. 1 week takes all the process. Bankia online is fine, also.

My suggest is not complicate the life. If ING makes you difficulties, just pass to others interfice.