Contents

Real estate crowdfunding is one of the most practical ways European investors can get exposure to property without the hassle of direct ownership. I’ve been using these platforms since 2015, and it remains one of my preferred asset classes alongside P2P lending.

Here’s a quick list of my recommended platforms for 2026:

- Raizers — French real estate, AMF-regulated

- Fintown — Prague short-term rentals and development, see my Fintown review

- LANDE — agricultural loans in the Baltics, see my LANDE review

How Real Estate Crowdfunding Works

Real estate crowdfunding platforms pool money from individual investors and deploy it into property projects — either as loans to developers or as equity stakes in properties. That’s the core of it. But the structure of your investment matters a lot for risk and return.

There are three basic approaches: secured loans, unsecured loans, and equity investment.

- Secured loan (senior debt) — collateral backs the loan, typically a first-rank mortgage on the property. You are first in line to be repaid, and in a default scenario, the asset can be sold to recover capital. Lower risk means lower yield, but the downside protection is real.

- Unsecured loan (mezzanine debt) — no collateral. The interest rate is higher to compensate, but if the project fails you are not backed by any asset. You are depending entirely on the platform’s ability to recover funds through legal action. Treat higher yields here as a risk premium, not a free lunch.

- Equity investment — you own a slice of the project. If it succeeds, the upside can be substantial. If it fails, equity holders are last in line — after creditors and employees — and can lose everything. Best suited to investors who understand the specific project and market well.

A useful rule of thumb: the lower the risk of the investment, the lower the yield. Any platform advertising 20%+ annual returns on real estate deserves intense scrutiny. That kind of figure usually means the loan is unsecured, the platform is desperate for capital, or both.

My Experience with Real Estate Crowdfunding

I’ve been investing across European real estate platforms since 2015. Over that time, my average annual return has been around 5-7%, which I consider an honest benchmark for what a diversified, risk-conscious approach looks like in this space.

Not every experience has been good. The Spanish investments have been my biggest disappointment — partly due to the operational incompetence of certain platforms, and partly because of sudden and damaging legislative changes in the Spanish market that undermined what looked like reasonable investments at entry.

The UK has also underdelivered. Brexit was the main culprit — it knocked property valuations sideways and made exits extremely difficult. And Lendy, which I used for a period, turned out to be an outright fraud. Not delayed. Fraud.

The Baltics have been a different story. The combination of well-run platforms, first-rank mortgage security, and a property market with genuine fundamentals has produced consistently solid results for me. It’s where I have the most confidence right now.

The lesson after eleven years is simple: platform quality and loan structure matter far more than headline yield. I’ve been burned by chasing the top of the rate table. The platforms below have earned my continued attention because of how they operate, not just what they offer.

See also: How to evaluate private real estate investment proposals and the yield vs. risk relationship in real estate investing.

1. Raizers

Raizers is the platform I recommend for investors who want exposure to French real estate. It has been operating since 2014, is regulated by the AMF (France’s financial markets authority), and has financed over 430 million euros across more than 430 projects.

The most important thing to understand about Raizers in 2026 is that its record is not as clean as its marketing suggests — but it’s also not as bad as some critics claim. The platform has recorded zero permanent capital losses to date, which is meaningful. However, roughly 22% of loans by volume are currently delayed by more than six months. The French real estate market went through a rough patch with rising interest rates and developer stress, and this showed up in Raizers’ portfolio. The platform has assembled a legal team to manage recoveries, and the first-rank mortgage collateral on most projects gives investors real protection — but patience is required.

I have had the chance to speak with Raizers co-founder Maxime Pallain on my podcast. He was candid and knowledgeable, and I came away with genuine confidence in the team’s competence and integrity. These are not people who are hiding the ball. They’re working through a market cycle that has been difficult across the entire French property development sector.

Average returns run around 9-10% on active projects. That’s above what I’d call the safe zone, which reflects the real risk involved. Go in with eyes open.

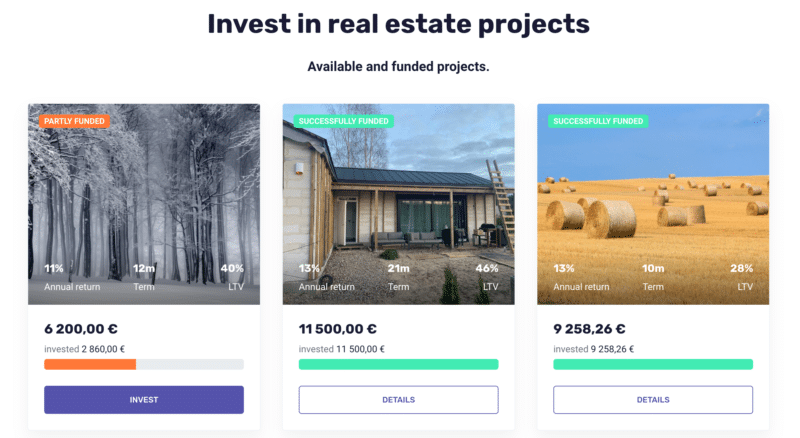

2. Fintown

Fintown is backed by the Vihorev Group, a Czech real estate developer with over a decade of operating history in Prague. The platform focuses primarily on short-term rental apartments in Prague’s Smichov district, with the team investing at least 20% of their own capital in every project — which is the kind of skin-in-the-game alignment I want to see.

Returns run between 8% and 14% annually, paid with daily interest accrual. The minimum investment is just one euro. There are no platform fees on deposits, withdrawals, or investments. Fintown publishes annual reports and has audited financials from the Vihorev Group — a level of transparency that is still rare among smaller European platforms.

The main caveat worth knowing: Fintown’s investments are not under specific Czech regulatory oversight, and liquidity is limited. Early exit is possible through their Early Exit 2.0 program, but it comes with a 10% fee if you exit between 6 and 12 months into a project, and payouts can take up to 30 days to process. This is not a liquid instrument — treat it as a 12-to-24-month commitment. Read my full Fintown review for the complete picture.

3. LANDE

LANDE occupies a niche that no other European crowdfunding platform covers well: agricultural loans secured by farmland in Latvia, Lithuania, and Romania. It was founded in 2019 by Nikita Goncars and Edgars Talums, both from backgrounds in secured lending, and the entire platform is built around one principle — low LTV, first-rank mortgage security only.

Every loan on LANDE is backed by a first-rank mortgage. Not second-rank, not a personal guarantee — a first-rank mortgage on the underlying agricultural land. This is the most creditor-friendly structure available, and it’s why the platform has recorded zero capital losses despite a 4.8% all-time default rate on individual loans. When defaults do occur, the collateral does its job.

LANDE obtained its European Crowdfunding Service Provider (ECSP) licence in February 2024, which means it operates under EU-wide regulation and can serve investors across all member states. Returns range from 4% to about 11%, paid monthly, with terms starting from a few months. The platform is actively expanding into Poland and targeting a managed portfolio of 100 million euros by 2030.

If you want the safest structural setup available in European real estate crowdfunding, LANDE is it. The agricultural niche also provides genuine diversification away from the development loan and urban rental apartment risk that most platforms concentrate on.

Read more: My full review of LANDE

Platforms That Have Failed — A Word of Caution

Real estate crowdfunding has been running long enough in Europe that we now have a clear picture of what failure looks like. Lendy in the UK collapsed entirely and turned out to be fraudulent. Housers in Spain was not fraudulent but was operationally incompetent — a slow-motion disaster for investors. Privalore was undermined by Spanish legislative changes on tourist rentals that the platform could not have fully anticipated, but the outcome for investors was still poor. Rendity in Austria permanently shut down in February 2026 after reporting a EUR 1M loss in 2024 and liquidating its German subsidiary.

The sector has also been hit hard by the interest rate environment since 2022. Higher rates raised developer financing costs, slowed property sales, and caused delays across platforms that were exposed to French, Spanish, and Southern European development loans. Some of those delays have become defaults. Not all of them will be resolved favorably.

Diversification across platforms and loan types is not optional in this space — it’s the basic unit of risk management. I would not put more than 5-10% of a portfolio into any single platform, and I’d lean toward secured, first-rank mortgage structures wherever possible.

If you’re investing as a Spanish resident, I also recommend reading my article on how crowdlending and real estate platforms are taxed in Spain. And for platform-specific due diligence, this guide on evaluating real estate investment proposals walks through exactly what to look for.

For Spanish-specific platforms, I’ve written a separate roundup: the best real estate crowdfunding platforms for Spain.

Have you used any of the platforms above, or come across one I haven’t mentioned? Let me know in the comments.

Related

Hi Jean, thank you for this review! A year ago, thanks to your review of Reinvest 24, I started to invest via this company. So far, everything goes extremely smooth. However, I didn’t see any audit report of the company on their website. Would that be something you would look at when choosing a crowdfunding company? Would that be a red flag for you?

Thank you in advance for your answer.

Aviv

You’re welcome Aviv! Yes, audit reports are one of the things I look for, but the lack of it is not a red flag for an established platform like Reinvest24. It’s a platform that has earned the trust of investors over the years. I would suggest that you contact them about it, however. They might be able to provided it privately, and if enough investors are asking for it, I imagine they will also be happy to post it on the site.

Hi Jean,

gongrats , excellent job!

Could you please check nibble platform ?

Thanks

hey jean,

I did not see the two biggest ones in germany and europe in your list.

did you have a look at the realized fundings and volumes?

Unfortunately a lot of the German ones are only available in German, so I can’t really use them.

Hi Jean,

Please have a look at Max Crowdfund. We only obtained the approval from the Dutch regulators un July 2020 but the founders of the group, Max Property Group, have been in real estate for decades. Our CTO is also the ex CTO of Collin Crowdfund, which is now the biggest SME crowdfunding platform in the Netherlands.

It would ve great to have a chat with you when you have a moment.

Best regards,

Jan Angel

You really need to look at CrowdProperty – seriously good… I appreciate you say you’re happy with your UK platform, but do a comparison… Oh, and watch the space their in. I don’t believe they’ll be sticking only to the UK, and they’re firing on all cylinders. I’m an investor. Fantastic platform, strong returns, great schemes, very professionally vetted. The auto invest tool has taken off enormously. Best wishes.

Thanks for pointing that out Nick, I’ll definitely check them out.

Hi Jean,

Thank you for sharing such a great article!

I’m from the US, based out of Mallorca, Spain. I’m interested in becoming a promoter as opposed to an investor. Are there any non-Spanish crowdfunding platforms in Europe you can recommend to get a projects funded in Mallorca?

All the best,

Constanza

Hi Constanza,

Could you please contact us as we are looking to expand Max Crowdfund to Spain?

Best regards,

Jan Angel

These are great options!

This is one of the best articles I have come across for getting introduced to some the best crowd funding European real estate sites. Thanks a lot for sharing this valuable information here, very helpful!!

What do you think about CrowdProperty?

I haven’t looked at that yet, but it’s been around for a long time and that’s a good sign. It seems to be a platform focused on UK property. At the moment I’m quite happy with Property Partner for all my UK property investments, so I don’t think I’ll be switching anytime soon.

Dear Jean,

Nice post, thank you for keeping it updated!

I wonder what’s your perspective about these platforms and, in general, about the real estate crowdfunding “industry” in these turbulent times. What would be your suggestion of a good investment strategy for this crisis that is already starting?

Thanks a lot!

You’re welcome Bruno. Over the past years I’ve been growing less and less enthusiastic about certain aspects of real estate crowdfunding. I would stay away from development loans, especially in countries that are less reliable (I’m looking at Spain, Italy and some of the Baltics in particular). In countries with weak business ethics, lots of bureaucracy, and swings in the political climate loans become a dangerous game as these factors highly increase the chance of the project going off course, with loan repayment being delayed significantly, if it ever gets repaid at all.

In the coming year I would keep an eye out for projects that involve buying properties that have all the fundamentals right. There will definitely be a lot of real estate for sale at a discount, and that opens a window of opportunity for thoes platforms that have strong negotiators on their team and expertise in refurbishing and repurposing buildings.

The idea would therefore be to negotiate a great price for a property with good fundamentals, then spend the next months (while the market is down or in the early stages of recovery) hard at work at refurbishing, before putting them back to the market for sale or for rent when the market is in a better shape.

Hi Jean,

nice article as always.

The downside of the majority of the crowdfunding sites in the Baltic region is that there is nothing to invest in at the moment. Most (Reinvest24, Crowdestate, Bulkestate etc.) have only a couple projects running that are already taken and there is no way to take part in it. Unless I’m doing something wrong and am unable to find anything.

That’s true Kris. I’ll try to reach out to some of these platforms to ask why we are seeing a general slowdown in projects available. On the other hand, I’d rather see fewer and better projects than lots of scantly verified projects. If you want an alternative to the Baltics, I would suggest taking a look at the German real estate platforms.

I had a quick look at iFunded. It looks interesting at first glance, but need to dig a bit deeper and also check out other western European platforms.

Btw. would you konw of any website where one can check newly emerging platforms or any other way to keep track of it?

Thanks for all info and quick replies.

Kris

I would suggest bookmarking eurofinanceblogs.com as I will be adding this feature soon.

Looks great. Lots of info. I’ll definitely add that one to my bookmarks. Thanks very much for your help.

All the best

Kris

Hello how i can investment and take profits i your projects?

Can i work with little capital and earn a monthly profit?

I’m not really sure what you mean there, could you explain further?

Hi Jean,

Again great and helpful article! Two questions from my side as a starter in real estate crowdfunding:

– Which platform should I chose to start (‘practice’) on?

– What amount would you advise to invest as a start?

thank you,

Alexander

Or would you advise me to start on the EvoEstate platform? (however it seems very new)

The guys at EvoEstate are also competent and they are introducing an innovative concept. Be aware that real estate crowdfunding and P2P lending carry a certain degree of risk, so it’s impossible for anyone to give you any guaranteed advice. As investors, the best we can do is look at each platform’s track record as well as the management team in place. We can then use our common sense and financial experience to evaluate each deal put forward by the platforms.

EvoEstate tries to help those who are inexperienced or unwilling to commit the time to do their own research on each opportunity, by acting as the curators of projects, with the premise that they will do good research on all opportunities on the market and only bring the best opportunities to their users. It’s a good concept but again you are trusting others.

As you’re learning the ropes, a good strategy to try and avoid getting burnt on bad projects is to diversify as much as possible. In that way, if you make any bad judgment calls, you won’t lose your whole investment, but only say one or two out of fifty small investments. In my Mintos review, for example, I mentioned my losing money on the Eurocent loans when the loan originator went bankrupt. It was a negative episode but since I was very diversified, it meant that I didn’t lose any of my principal and only took a small hit on my overall returns.

Hi Alexander, one of my favorites at the moment is Reinvest24, they’ve got a great track record and the people managing the platform are very competent.

You should decide for yourself how much to invest; don’t trust anyone who makes any suggestions on how much you should invest unless he is your paid and trusted financial advisor. If you’re new to these types of investments and you’re doing this to learn, you can start off with the minimum investment possible on each platform, and that will give you full access to the project details and outcomes with very little risk.

Jean,

Thank you for rapid reply and the tips that you are giving me! As you are stating I will start small, and get to know the platform(s) and learn/understand how it works. Hopefully it will go well and I can grow into it (my learning curve and the investments).

Will not only diversify within property crowdfunding, but also diversify towards P2P lending platforms.

thank you,

Alexander

You’re welcome Alexander, best of luck!

I use Estateguru. They offer business loans & development loans from the 3 Baltic countries and Finland.

Yes they’re very good too and I’m using them as well, will add to the list.

Jean,

how come most of the property crowdfunding sites seem to originate from the baltic countries?

There are several reasons Chris.

Great Article as usual! I am heavily invested on Mintos and wish to try in estate as well….Do these (all or some) have buyback guarantees as well like Mintos? Thanks

Good choice, no they don’t have as the risk is much lower, being property and not personal loans.

Noted 🙂 Thanks

Hi Jean,

Super interesting information, and very well presented! Thank you for sharing.

Best regards from Amsterdam!

Alex

Welcome Alex and thank you for commenting. Are you aware of any platforms for real estate crowdfunding in the Netherlands?

Hi Jean

Thanks for your work on this site.

All the best

Jorge

Welcome Jorge, keep an eye out on my newest project Euro Finance Blogs for the latest news from other blogs and crowdfunding platforms.

Hi Jean

Have you heard about RealT.com? Is it same investment style with those you are reviewed?

Seems to be a broken link unfortunately.

Sorry …. I mean https://realt.co

Got it, I can’t take a platform with that domain seriously unfortunately. It shows me that they don’t have the basics in place. They should have either chosen another brand name or bought the .com.

It might seem strange of me to dismiss a platform based on a technical detail, but it’s one of the shortcuts I use when evaluating platforms.