It’s been more than ten years now since I left Malta (click here to read my original article about why I left), and in recent years I’ve preferred not to comment much on Malta, both because I had personally moved on from thinking about the country or following its news, and also from a sense […]

Kubera – The All-Inclusive Net-Worth Tracker

Track your wealth with Kubera Up until recently and even to quite some extent today, the asset portfolio of many retail investors will prevalently consist of a standard range of assets. This would often include property, vehicles, company stocks and bonds, retirement accounts and insurance, term deposits and bank accounts. These portfolios are, more often […]

Nexo Review 2026

Get Started With Nexo If you hold crypto and you’re not earning anything on it, you’re leaving money on the table. Nexo is one of the platforms I’ve looked at most seriously for doing exactly that — putting idle digital assets to work while staying invested. In this review I’ll walk you through what Nexo […]

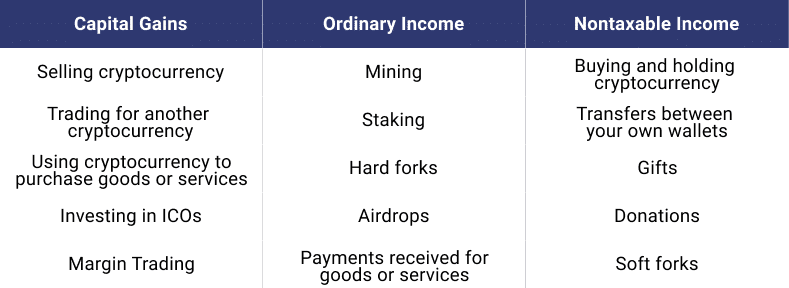

Cointelli Review – Automated Tax Reports for Crypto Transactions in the US

Automize your crypto tax report with Cointelli Over the past years, the cryptocurrency sphere has evolved into a vast and complex reality where enthusiasts and investors alike can access a multitude of financial products that come in all sorts. And if (like me) you are one of them, you will likely be actively using multiple […]

The Best Crypto Podcasts in 2026

One of the main ways that I keep updated with all the stuff that’s happening in the crypto space is through podcasts. I also run my own podcast at Mastermind.fm. Here are my favorites, categorized based on the majority of the topics they cover. The Rabbit Hole These are podcasts that are ideal for understanding […]

How to Find the Right Amateur Padel Tournaments

Padel is not just for the pros. One of the best things about the sport is that anyone of any level and age can have a great time and take part in competitions. I first published this article several years ago and the amateur padel scene has changed enormously since then. Spain now has over […]

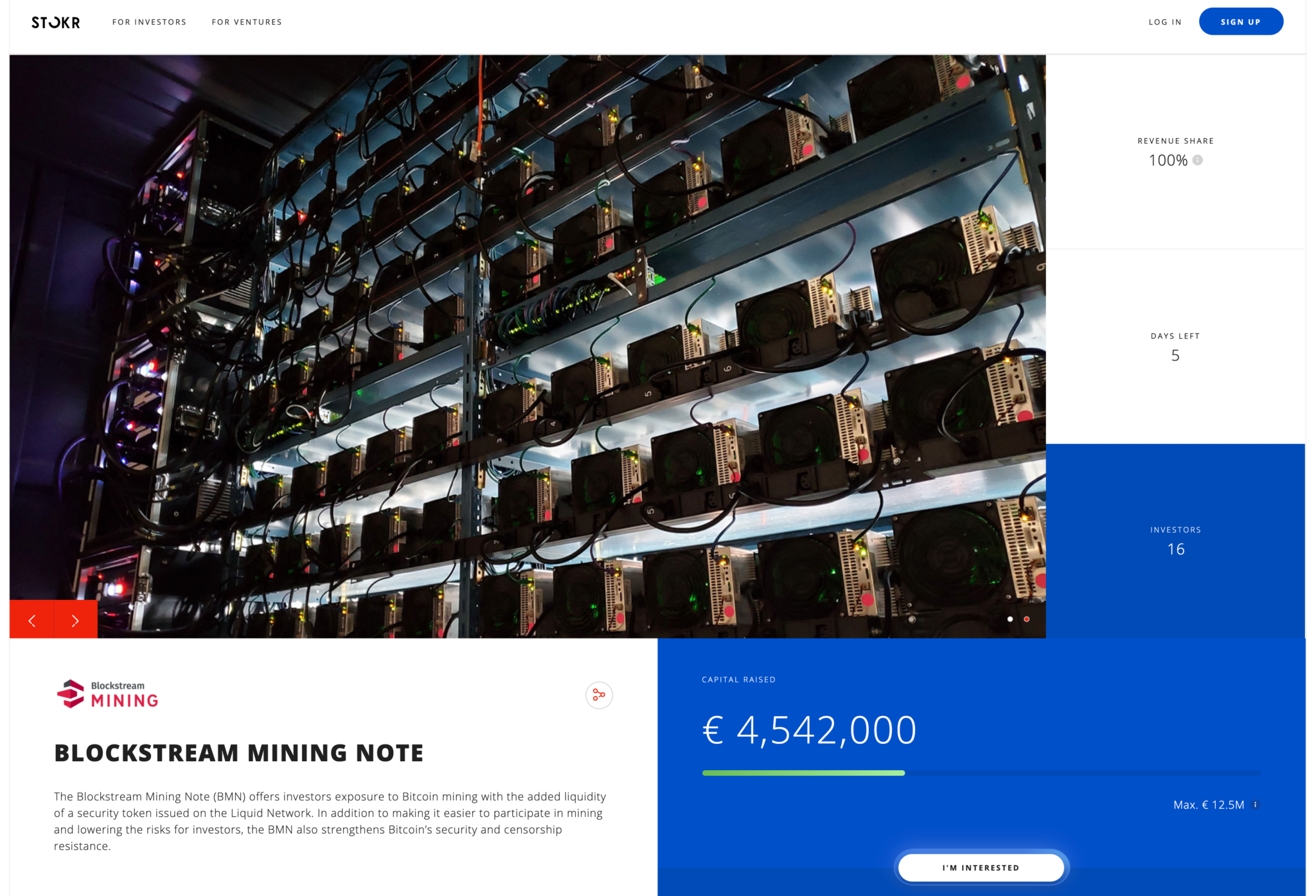

How to Invest in Bitcoin Mining

Bitcoin mining is a great way to approach investing in Bitcoin from a different angle. There are several ways that you can get involved with Bitcoin mining for profit. In this post, I’ll take a look at how you can get exposure to Bitcoin mining in various ways, and some considerations to keep in mind. […]

Best Platforms for Dollar Cost Averaging in Crypto

Let’s start off the article by making sure everyone is on the same page. It’s time to define this mysterious term and explain what DCA means. DCA (or Dollar Cost Averaging) is a technique that’s used to average your buying price or is used as the “Martingale technique”, which you use when a position is […]

Are LASIK Eye Surgeries Safe?

I’m currently doing some research on LASIK (Laser-Assisted In Situ Keratomileusis) surgeries, and this includes related procedures too. I’d love to know from any readers who have done such surgeries, so please leave a comment below or contact me via email. I’d really appreciate your thoughts as I am considering having this procedure done myself. […]

How I Replaced Netflix with Better Evening Habits

For years, my default evening move was to open Netflix. Not because I wanted to watch anything specific — just because it was there, and the day felt done. I’d scroll through thumbnails for ten minutes, pick something mediocre, and fall asleep on the couch. At some point I noticed I couldn’t tell you what […]

Are Acquisitions in the WordPress Space a Good or Bad Thing?

This is an article that reflects on the high number of acquisitions we’ve seen happen in the past few years (2018-2021) within the WordPress space. There are basically a handful of companies behind all the big acquisitions, so there is no doubt that the product space is becoming more centralized, and these big companies now […]

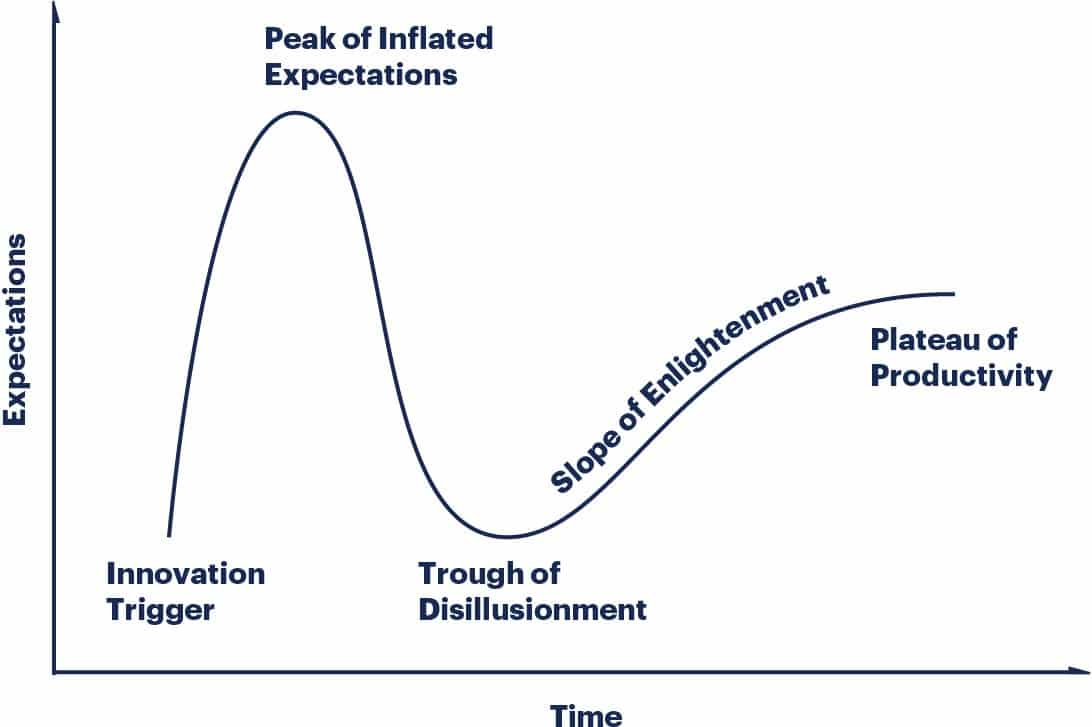

Making Money in the Second Wave

Over the years I’ve come to realize that my best investments happen during the second wave of the product or industry lifecycle. The idea is loosely based on the Gartner Hype Cycle curve, the [amazon link=”0062292986″ title=”Chasm”] concept, the Hero’s Journey and the theory of Diffusion of Innovations. Let’s take an abbreviated at these models […]

- « Previous Page

- 1

- …

- 12

- 13

- 14

- 15

- 16

- …

- 36

- Next Page »