This is part of an ongoing series I am writing as I work my way through the modern web stack from a WordPress developer’s perspective. It …

Headless WordPress: The Bridge

This is part of an ongoing series I am writing as I work my way through the modern web stack from a WordPress developer’s perspective. It …

The Lightweight Video Kit I Use for Drone and Talking-Head

I shoot most of my video with a deliberately light kit. No cinema camera, no bag of lenses. A small drone, my iPhone, a gimbal, and …

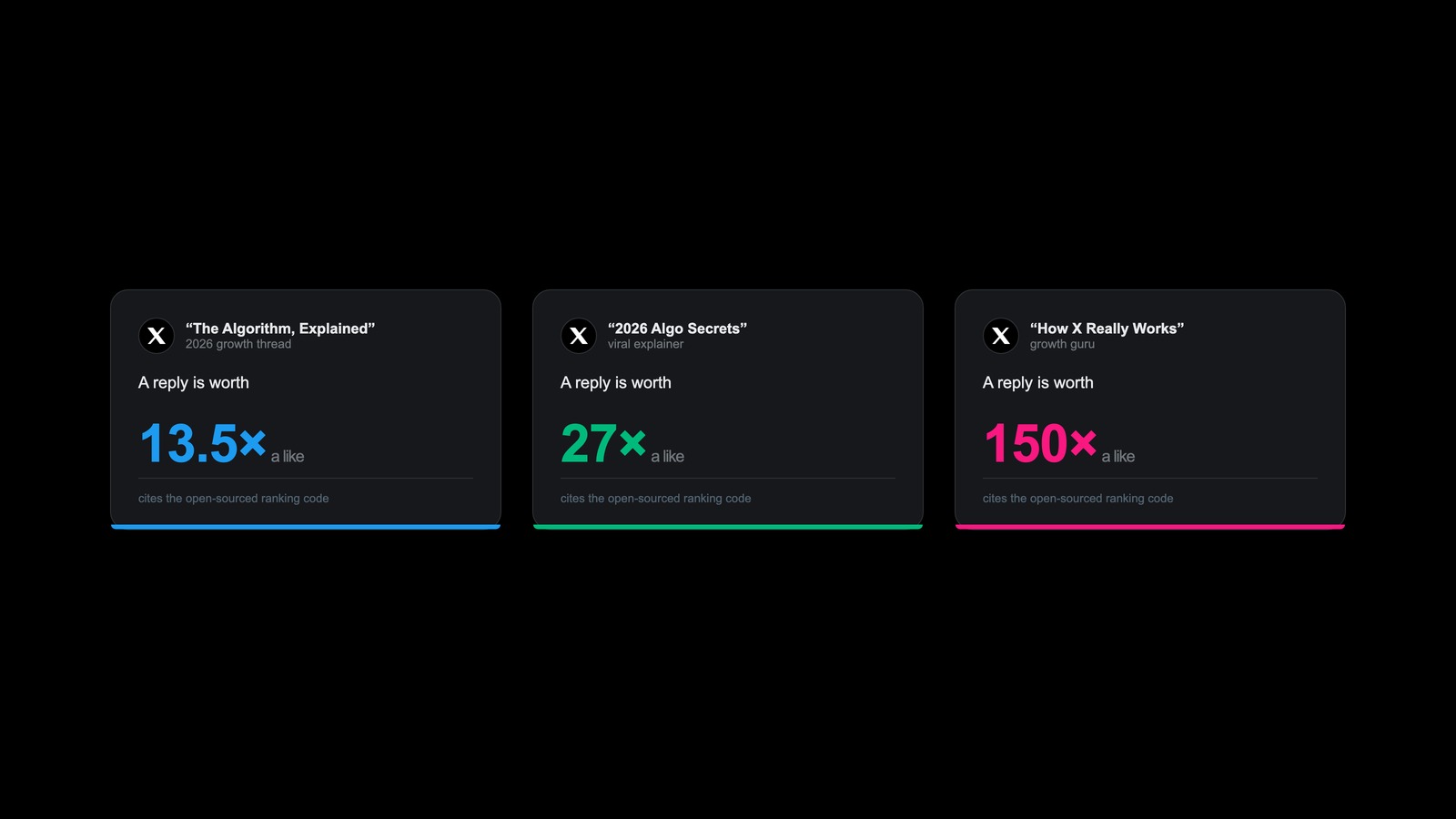

How to Grow on X in 2026: The Durable Rules vs the Algorithm Myths

I went looking for the current best way to grow on X, and what I found was a wall of 2026 “algorithm explained” posts that confidently …

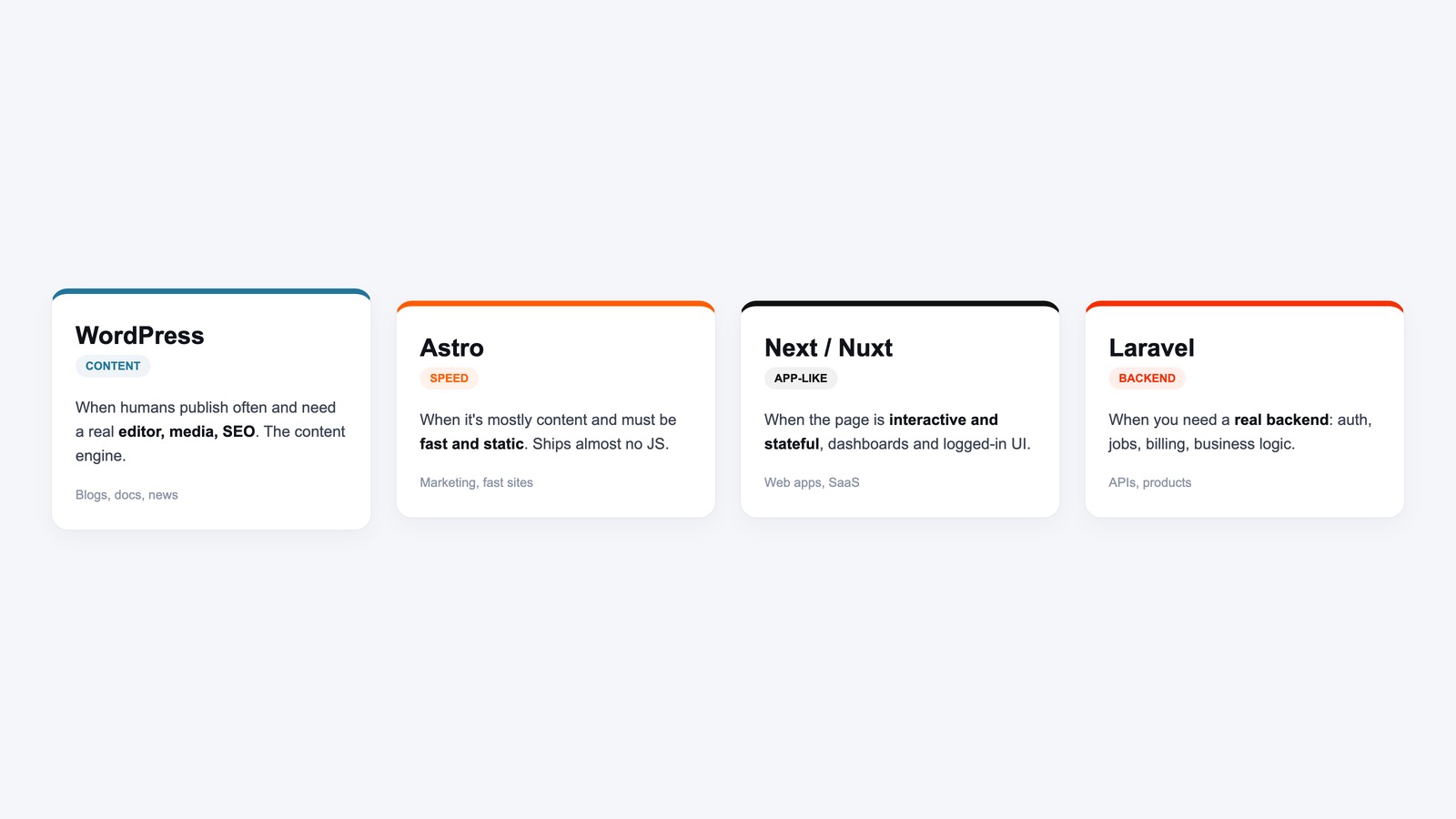

When to Use WordPress, Astro, Next, or Laravel

The question I get most often is some version of “should I build this in WordPress or Astro or Next.” It sounds like a single choice …

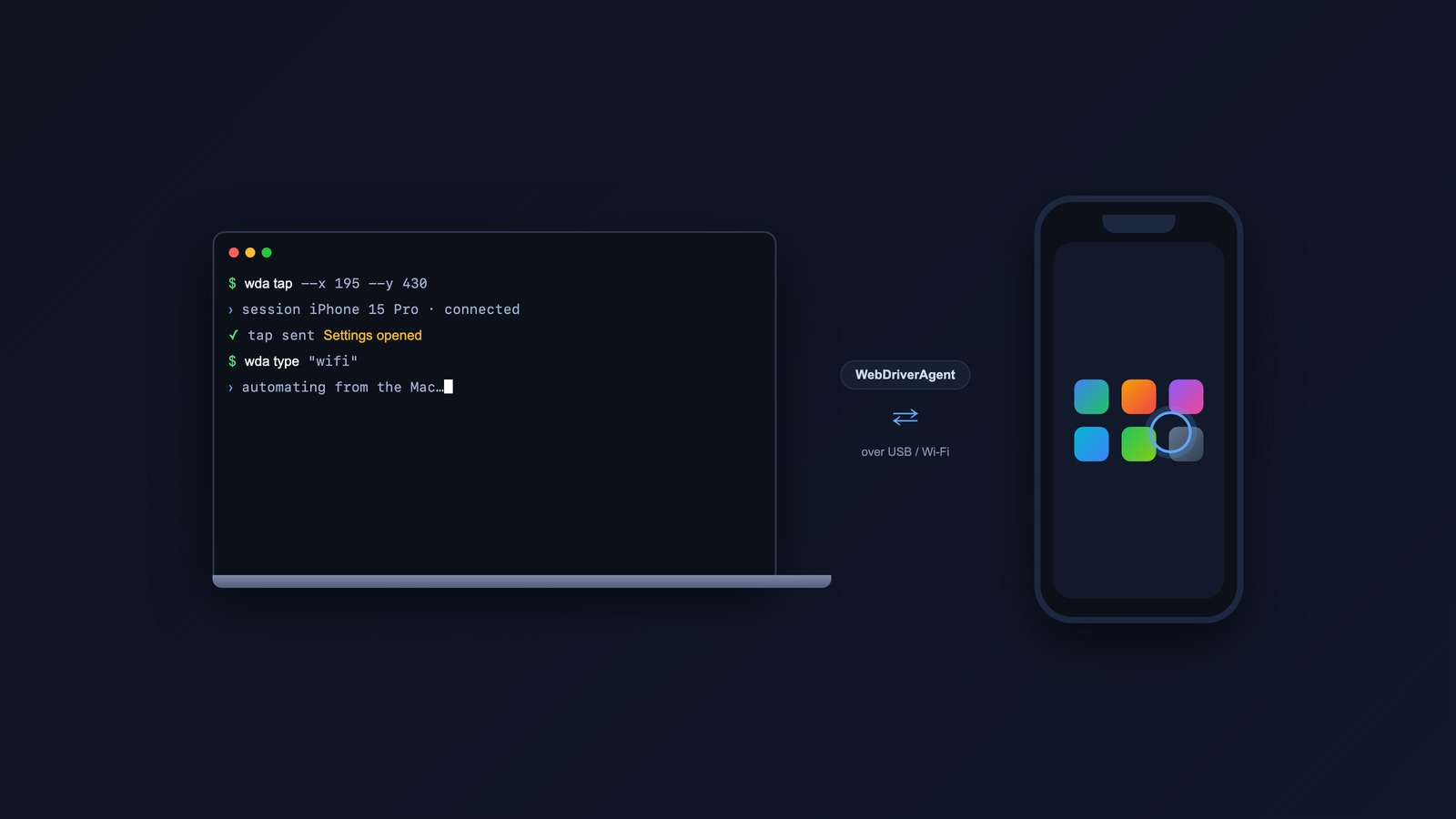

How to Control and Automate an iPhone or iPad With WebDriverAgent

If you bought a Mac in the EU and went looking for iPhone Mirroring, the feature Apple demoed for controlling your iPhone from your desktop, you …

The Science Behind Sauna: Why I Use It After Every Workout

I use the sauna at my fitness club almost every day, usually right after a workout. It started as something I did because it felt good …

Observability When You Can’t Just SSH In

This is part of an ongoing series I am writing as I work my way through the modern web stack from a WordPress developer’s perspective. It …

From Client Call to CRM: An Automation Workflow for Real Estate Agents

Every real estate agent has lived this. You spend twenty minutes on the phone with a buyer. They tell you they want three bedrooms but could …

CI/CD: Goodbye FTP, Hello GitHub Actions

This is part of an ongoing series I am writing as I work my way through the modern web stack from a WordPress developer’s perspective. It …

Run Claude Code on a Hetzner Box and Drive It From Your Laptop and Phone

A friend showed me his Claude Code setup and it was the cleanest version of an idea I’d been circling for a while. Claude Code runs …

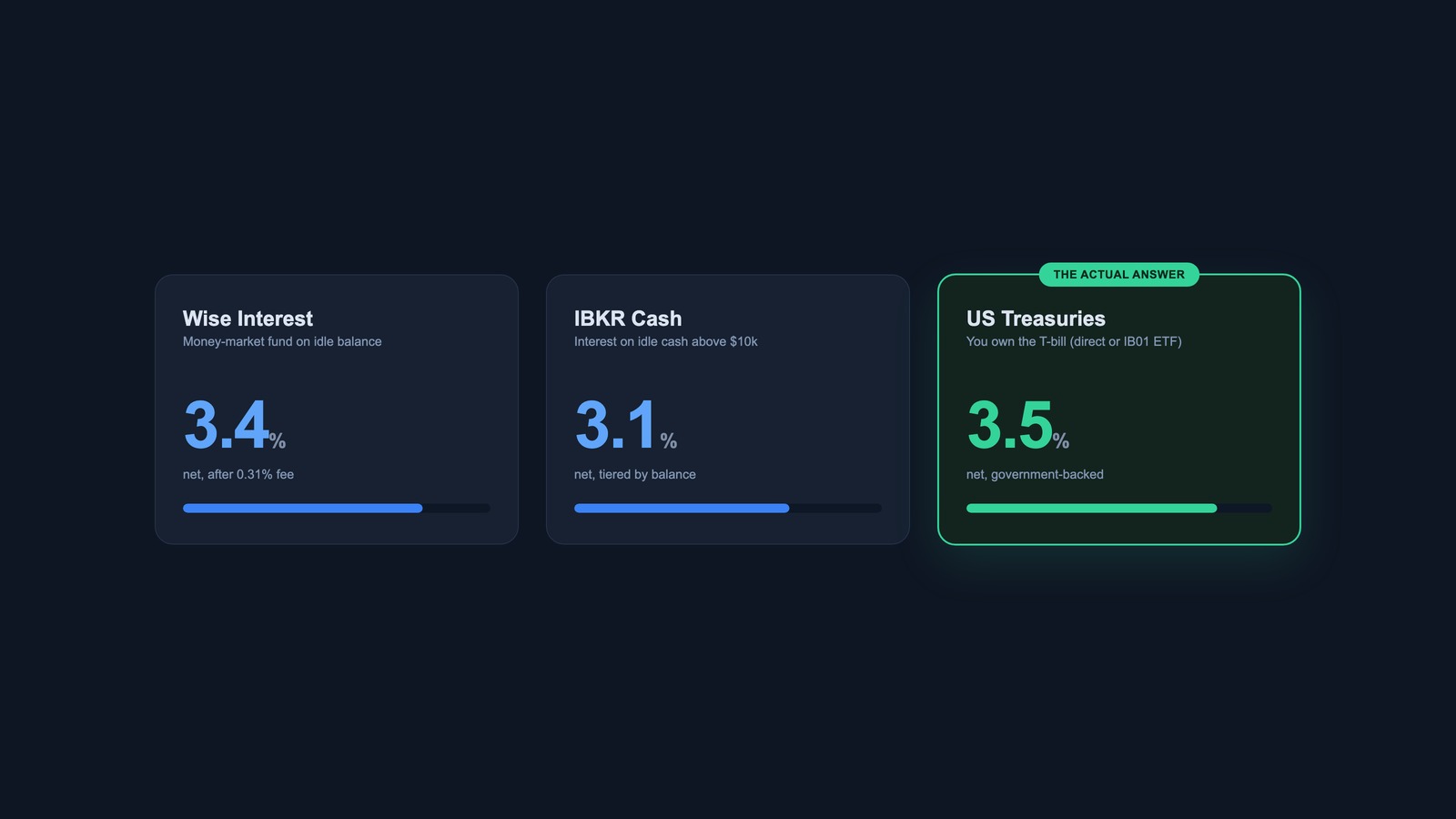

Where to Park USD for Yield: Wise vs Interactive Brokers vs Treasuries

If you earn or hold US dollars in Europe, you’ve probably noticed they tend to sit idle. A client pays you in USD, it lands in …

- « Previous Page

- 1

- 2

- 3

- 4

- …

- 46

- Next Page »