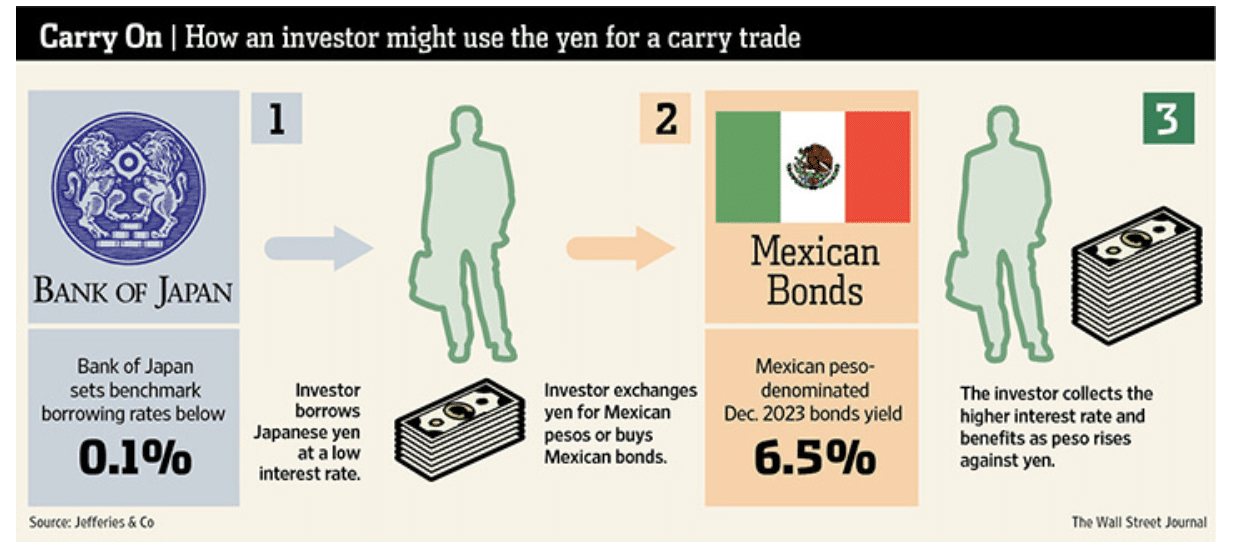

A carry trade or “carry trading’ is a unique trading strategy where one takes a loan at a low-interest rate and then takes that loan to invest in an asset that provides a significantly higher rate of return. It’s a strategy that has been used in traditional markets for many years between various fiat currencies […]

DEGIRO Review 2026: Is This the Best Low-Cost Broker to Invest Online?

If you’re looking to invest online – whether that’s in the form of stocks, ETFs, or other asset classes – you need to ensure that you are getting a good deal for your money. In other words, you’ll want to pick an online broker that offers competitive fees and commissions. One of the most notable […]

How to Buy Bitcoin in Europe – The Best Exchanges

Buy Bitcoin In March 2020 Bitcoin was priced at ‘just’ under $5,000. And today? The very same digital currency has gone beyond $40,000. Put simply, this means that Bitcoin has increased in value by over 800% since March 2020. With this in mind, it goes without saying that interest throughout Europe in this cutting-edge cryptocurrency […]

CFD Trading Guide: What are CFDs and Should you Trade Them?

If you’re simply looking to buy shares or invest in an index fund – CFDs won’t be for you. But, if you’re looking to deploy more advanced trading strategies – such as applying leverage or short-selling, then CFDs might be the solution. Put simply, CFDs are tasked with tracking the value of an asset like-for-like. […]

Building Muscle – My next Health and Fitness Project

Over the past 25 years or so, I’ve been practicing sports on a very regular basis. I’ve tried several different sports, with football and cycling being the main ones in my twenties. Then, in my thirties, padel became my main focus, with other racket sports (beach tennis, tennis, frescobol) complementing it. Cycling was still present, […]

How to Deal with Loose Ankle Ligaments

I was born with hypermobile joints, especially in my knees, ankles, elbows and shoulders. Hypermobility is a connective tissue condition (usually inherited) in which the body’s collagen is more elastic than the ‘norm’, leading to increased flexibility. For some people, notably musicians, gymnasts, dancers and sports people, this natural flexibility gives a very useful advantage, […]

How To Hire Great Remote Workers (Legally)

Remote companies like RebelCode tend to hire people from all over the world. This sounds like a great idea to reduce the costs of having an office, as well as have a more diverse workforce and also reduce labor costs. How is it done in practice? Hiring Foreign Workers – Legal Implications There are two […]

How to Get Crypto Price Alerts

Crypto assets can go through weeks of flat price action, and then suddenly go into a frenzy in a few hours. It is not practical for investors who are not professional traders to keep on top of the crypto markets themselves, also because the market is open 24/7. How can we get crypto price alerts […]

My Best Travel Tips – Accommodation, Flight Prices Etc

Getting the chance to travel is not something to take lightly. Many possibilities need to be taken into consideration before you begin. You can anticipate much hassle when it comes to packing for a trip. You cannot forget anything, and you cannot go back anytime soon. Keeping these two things in mind, simplify your traveling […]

My Thoughts on WordPress in 2020

I’ve been using WordPress since the early days, 2006 to be exact. I fell in love with the idea of open-source CMSs a few years before that, after experiencing firsthand how cumbersome and expensive closed-source CMSs were. The big open source players at the time were Drupal and Joomla, but then WordPress came along and […]

Best Apps for Trading Crypto in 2026

I bought my first Bitcoin in 2013. Back then, the process involved wiring money to a Slovenian exchange through a series of steps that felt more like money laundering than investing. The whole experience was confusing, slow, and more than a little sketchy. In 2026, buying crypto is as straightforward as buying a stock. The […]

Best Anonymous Bitcoin Wallets

Irrespective of what your long-term investment goals are – if you plan to buy and hold Bitcoin or even alternatives like Ethereum from exchanges like Coinbase, you will need to store your coins in a digital ‘wallet’. Depending on what your needs and requirements are, there are hundreds of anonymous Bitcoin wallets to choose from. […]

- « Previous Page

- 1

- …

- 18

- 19

- 20

- 21

- 22

- …

- 36

- Next Page »