If you earn or hold US dollars in Europe, you’ve probably noticed they tend to sit idle. A client pays you in USD, it lands in Wise or your broker, and there it stays, earning either nothing or some quiet rate you’ve never actually checked. I held dollars this way for years before I bothered to work out what they should be earning.

The short version: most people leave real money on the table by holding USD as bare cash. The fix is straightforward once you see the options side by side. Here’s how Wise, Interactive Brokers, and US Treasuries compare for parking dollars, and which one I’d actually use.

To be clear about scope: this is about cash you want to keep within reach while it earns, not money you’re ready to commit to a long-term investment. If your horizon is years rather than weeks, equities are a different conversation.

The Options at a Glance

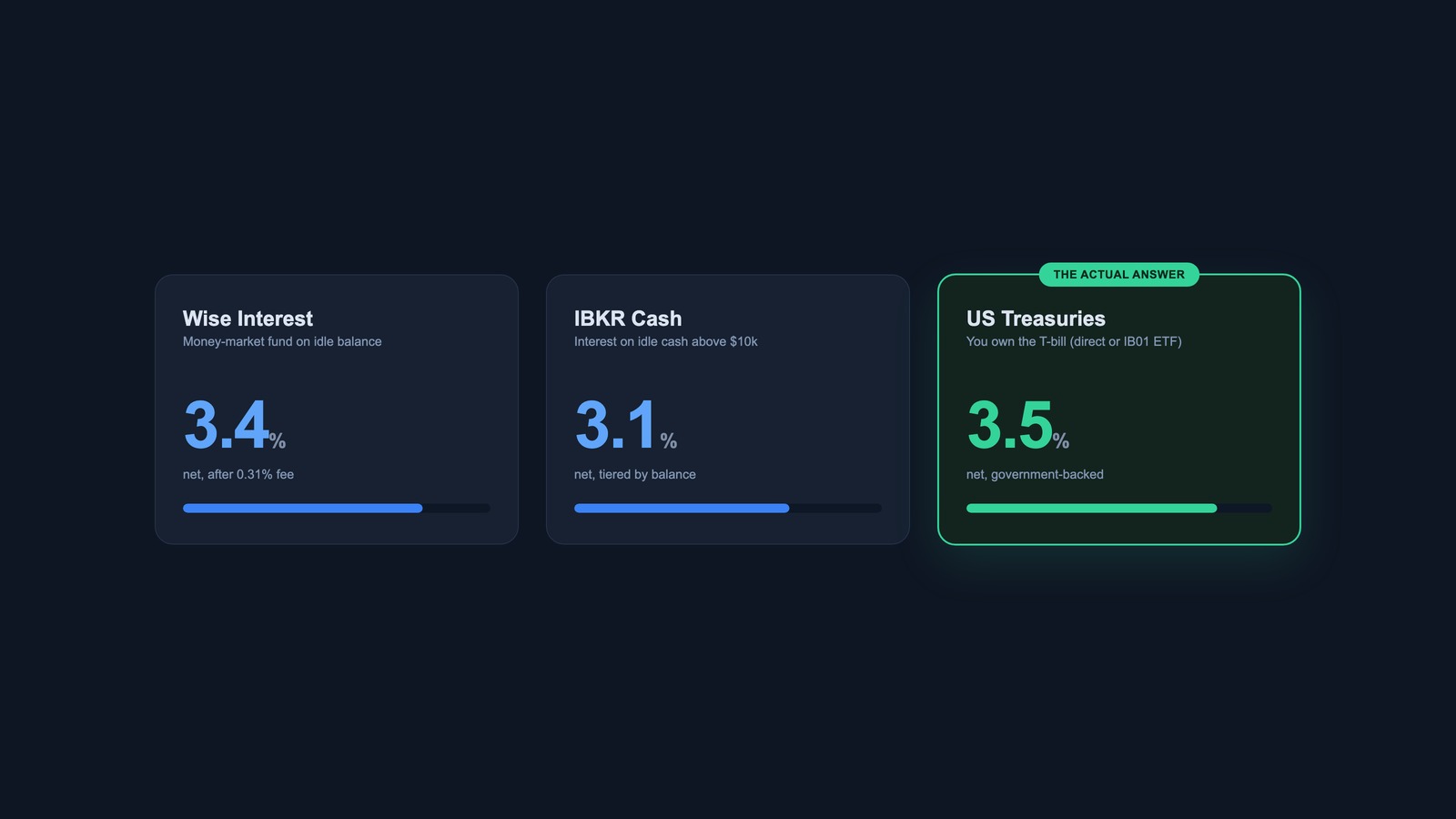

Rates below are as of mid-2026, with the US Federal Reserve’s effective funds rate around 3.6%. Every figure is net of the platform or fund fee, so they compare like for like. The numbers move with the Fed, so treat them as the relationship between options rather than fixed figures.

| Option | Net USD yield | What it actually is | Available to EU residents? |

|---|---|---|---|

| US T-bills direct (at IBKR) | ~3.5% (no fund fee) | You own the Treasury bill | Yes |

| Short-Treasury UCITS ETF (e.g. IB01) | ~3.5% (0.07% fee) | A fund holding short T-bills | Yes |

| Wise Interest | ~3.4% (after 0.31% fee) | Money market fund | Yes (EEA) |

| IBKR cash interest | ~3.1% above $10k | Interest on idle cash | Yes |

| SGOV (US-listed ETF) | ~3.55% | US-domiciled fund | No, blocked for EU retail |

The ranking surprises most people. The best place to hold USD for yield is owning short-dated Treasuries, ahead of any of the savings features. Let me walk through each option and then explain why.

Wise Interest: Fine for Money You’re Already Moving

Wise added interest on USD, GBP, and EUR balances a while back, and for EEA customers it’s now genuinely available rather than the US-and-UK-only feature it once was. It works by putting your idle balance into a government money market fund. The headline rate looks competitive, but read the detail: there’s an annual fee of roughly 0.31%, so the rate you actually keep on USD lands around 3.4% at current Fed levels.

Two things to keep in mind. It’s an investment product, not a savings account, so it carries no deposit guarantee and the value can in theory fall, though a government money market fund is about as low-risk as investing gets. And Wise is an electronic money institution, not a bank, so your underlying balance is safeguarded rather than covered by a deposit protection scheme. I cover the full account in my Wise review.

Wise Interest is a reasonable convenience yield on dollars that are passing through Wise anyway, on their way to being spent or transferred. It is not where I’d park a serious USD position for return.

Interactive Brokers Cash Interest: Better Than It Looks, Worse Than You’d Hope

Leave uninvested USD in an Interactive Brokers account and it earns interest automatically, with nothing to buy. The rate tracks a benchmark close to the Fed funds rate minus a spread of about 0.5%, which works out to roughly 3.1% at the moment. There’s no fee, and you don’t have to do anything.

The catches are in the structure. The first $10,000 of cash earns nothing at all, so a small balance barely moves. And you only get the full rate if your account net value is at least $100,000; below that, the rate scales down proportionally. A €15,000 cash balance in a modest account ends up earning a blended rate well under the headline. IBKR’s cash interest becomes genuinely useful once your account is large enough to clear those thresholds, but even then it’s beaten by the option most people overlook. For the platform itself, my Interactive Brokers review goes deeper.

US Treasuries: The Actual Answer

The highest, cleanest yield on dollars comes from owning short-dated US government debt directly, not from any interest feature. Treasury bills are backed by the US government, yield close to the full Fed funds rate, and as individual securities they’re held in segregated custody in your name rather than sitting as a cash balance on a platform’s books.

There are two ways to hold them as a European investor:

- Buy T-bills directly through Interactive Brokers. You own the actual bill and hold it to maturity for its face value, with no fund fee at all. You pick the maturity, so you can match a date you know you’ll need the cash.

- Buy a short-Treasury UCITS ETF such as IB01 (iShares $ Treasury Bond 0-1yr UCITS). The fund holds a basket of short bills and rolls them for you automatically, with a tiny 0.07% annual fee and the ability to sell any amount on any trading day.

One trap worth naming: you cannot buy SGOV, the popular US-listed Treasury ETF, as an EU retail investor. US-domiciled ETFs don’t publish the disclosure document (the PRIIPs KID) that EU rules require, so every European broker blocks them. IB01 and similar UCITS funds are the EU-legal equivalent, and they give you the same exposure. I explain the workaround for the funds you genuinely can’t access in my guide to accessing US ETFs from Europe.

Direct T-bills or the ETF?

Both yield about the same, so the choice is convenience versus control, not rate.

Direct bills win when you have a fixed sum you can commit to a known maturity and you’d rather pay no fund fee at all. The cost is that you manage the ladder yourself: when a bill matures, you reinvest manually. The ETF wins when your dollars come and go on an unpredictable schedule, you want to sell part of the position intraday, or you simply don’t want to babysit maturities. For most people parking working cash, the auto-rolling ETF is worth far more than the 0.07% fee it charges. The ETF suits dollars with uncertain timing; direct bills suit a lump you can commit to a maturity.

What It Nets After Fees and Tax

Every yield above is already after the platform or fund fee. Wise’s roughly 0.31% annual charge is baked into that ~3.4% net. IB01’s 0.07% fund fee sits inside its ~3.5%. Direct T-bills carry no fund fee at all. The gap you see is real and fee-inclusive, not a headline that shrinks once you read the small print.

The Interactive Brokers side has one extra cost, and it’s small: a one-time commission to buy the ETF or the bills, usually a few euros, with no monthly account fee and nothing charged to hold the position. Spread over the months you hold it, that commission rounds to nothing. The cost that can bite either platform is currency conversion, if you’re turning euros into dollars first. Wise charges around 0.4% and up for that, while Interactive Brokers converts close to the interbank rate for a couple of euros. If you already hold dollars, neither applies.

Then tax goes on top, at whatever rate your country charges, and it lands broadly the same on all of these. Wise interest, IBKR cash interest, a T-bill coupon, and a distributing fund’s payout are normally taxed as savings or investment income in the year you receive them. Tax doesn’t rescue Wise or sink Treasuries; it trims every option by a similar amount, so it doesn’t reorder them.

The one real tax lever is the accumulating fund. A distributing holding pays out cash that’s taxed each year. An accumulating short-Treasury ETF rolls the income back in and is taxed only when you sell, which defers the bill and, in some countries, turns it into a capital gain taxed at a different rate. Whether that helps depends entirely on where you live, and on whether you hold personally or through a company, where the rules shift again. The same iShares fund comes in both a distributing line (IB01) and an accumulating one, and if you don’t need the income paid out as cash, the accumulating share class keeps things simplest, with no distributions to track.

There’s also reporting. Several countries make you declare foreign accounts and holdings above a threshold, Spain’s Modelo 720 being the familiar one, and a broker position and a Wise balance both count. None of this is a reason to leave dollars at zero. It’s a reason to run your own numbers, and your own residency, past an accountant before sizing a position. I’m laying out the options, not giving tax advice.

Safety: Where Your Dollars Actually Sit

Safety argues hardest for owning Treasuries rather than holding cash. At a broker like Interactive Brokers, the bills and ETFs you own are client assets, held segregated and off the broker’s own balance sheet. If the broker failed, those securities are yours. Bare cash is covered only up to a much smaller investor compensation limit, and the exact scheme depends on which legal entity holds your account.

Wise, by contrast, is an electronic money institution. Your funds are safeguarded in segregated accounts, which is real protection, but there’s no deposit guarantee scheme behind it, and the Interest product is a capital-at-risk investment with no scheme at all. For larger sums, owning segregated securities is the stronger position.

Which Option Fits Your Situation

The right choice depends less on chasing the top rate than on how you’ll use the money. A few common cases:

- Dollars passing through Wise on their way to being spent: switch on Wise Interest and leave them there. The convenience outweighs the fraction of a percent you’d pick up by moving them, and you’re not holding long enough for the gap to add up.

- Working cash you might deploy into an investment at any moment, and you want it instantly tradable: hold it in your broker. Bare USD cash at Interactive Brokers earns the credit rate, around 3.1%, with no lock-up and instant buying power, so you can act the day you decide.

- Cash you’ll hold for weeks or months and can wait a couple of days to free up: a short-Treasury ETF like IB01 at Interactive Brokers. Best net yield with daily liquidity, and you sell whenever you need the money. This is the case most people are actually in.

- A larger sum parked for a while: the same short-Treasury route, and at size the protection counts for more, since the bills and the ETF are securities you own rather than a balance on a platform’s books.

- A small balance already sitting in Wise: don’t bother moving it. The yield gap is a few euros a year, not worth the setup.

- Money you can commit to a fixed date: buy T-bills directly to that maturity and skip even the ETF’s small fee.

- A horizon of years rather than weeks: that’s investing, not cash management, a different decision with a different risk profile. This guide is about earning on cash you want to keep accessible.

The Bottom Line

If your goal is to earn a real return on USD you’re holding for a while, buy short US Treasuries at a broker like Interactive Brokers, either as direct T-bills or through a UCITS ETF like IB01. You get around 3.5%, with your money held as a security you own rather than a balance you’re owed. That edge survives every fee, and since tax falls about the same on each option, it doesn’t change the order.

Wise Interest at roughly 3.4% net is genuinely usable now, and fine for dollars already flowing through Wise, but treat it as convenience yield rather than a home for the position. IBKR’s plain cash interest is the fallback for dollars you haven’t deployed yet, and only really earns its keep once your account is large. The one thing I wouldn’t do anymore is let dollars sit at zero.

Related

Leave a Reply