Contents

Mintos is a peer-to-peer lending platform in Europe. Like many other FinTech companies of this type, it is based in the Baltic region; in Latvia specifically.

Currently, Mintos has four offices employing more than 160 people in Riga, Vilnius, Berlin and Warsaw.

Mintos started operating in 2015 but has experienced rapid growth due to getting many things right and becoming popular with financial bloggers due to its ease of use and transparency.

The average interest rate is around 12%, with close to 500,000+ investors registered worldwide and 600m euros under administration.

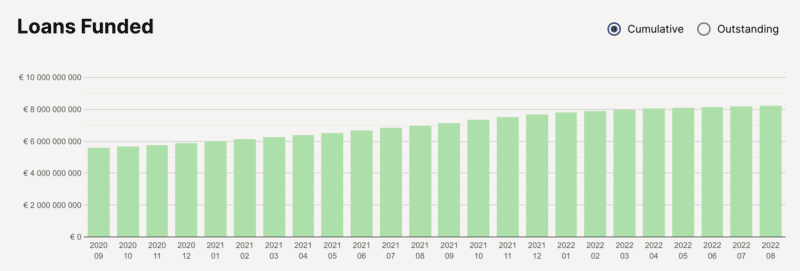

Another important statistic to look at is the loan book growth, and here again, Mintos is doing very well as can be seen in the following screenshot.

The total money invested so far is higher than 8 billion Euros, which is a staggering number for such a young platform. There is no doubt that Mintos is the biggest player in P2P lending in Europe at the moment, with over 50% market share of the total p2p lending market. There are some good competitors, but none of them provide the security and track record that Mintos does.

The management team of Mintos is clearly displayed on the website with links to the Linkedin profiles of each person on the team. Mintos is currently the biggest employer in the P2P lending space.

Being able to view the team and also check out various YouTube videos with their CEO Martins Sulte enhances the feeling of transparency and peace of mind. I am one of those who take a look at these pages on a website and use them when judging whether I should invest on a platform or not. Everything counts.

I have personally interviewed Martins on my podcast Mastermind.fm, so be sure to check out that episode if you like podcasts.

Mintos is a platform that is in line with EU law, so when you invest you won’t have any trouble with your accountant or tax authorities back home in terms of explaining what you are doing.

Finally and very importantly, Mintos as a company is profitable, so they are not only running on investor money but are actually turning a profit, which means that they have a much higher chance of standing the test of time compared to some other competitors that are still in startup mode.

The biggest number of investors come from Germany, Spain and the Czech Republic respectively, but this is mostly a reflection of those countries’ familiarity with this type of investing. There are more than 340,000 investors that have used Mintos and they come from 90+ countries.

More than 60 lending companies offer their loans on the Mintos platform, with over 25,000 people working at these companies and spread over 33 countries, so you can have a global reach when investing on Mintos.

The company supports 10 languages via its multilingual support team, while the website is available in 6 languages and there are loans available in 10 currencies.

⚙️ How Does Mintos Work?

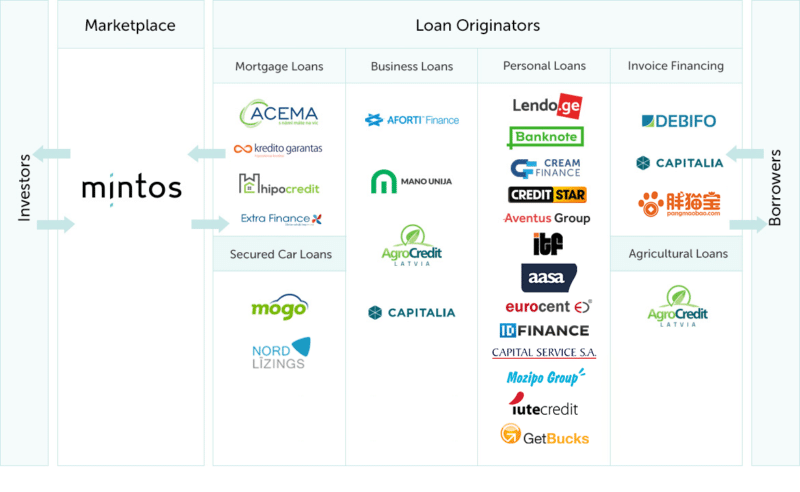

Mintos is a loan aggregator, which means that it partners with loan originators worldwide to bring in their loans onto the platform. These loans would be pre-funded, which means that the originators themselves have supplied the loan to the end customer, and are now reselling part of that loan to us investors via Mintos.

The people at Mintos conduct their research on each loan originator periodically and assign them a score based on various factors. They also provide information pages on each of these originators so that as an investor you can easily learn more about them. No other platform in Europe currently has anywhere close to the number of loan originators that Mintos has. This contributes to the huge loan pool that Mintos currently has and improves liquidity.

Every loan originator is required to have skin in the game, and many of them also provide a buyback guarantee.

The buyback guarantee means that if a borrower defaults, the loan originator will automatically buy back the defaulted loan from the investors and also pay them interest for the period during which the loan was in default.

Some people have thus asked me where is the risk in investing in Mintos when loans come with a buyback guarantee. We will have a look at the risks later but to answer that question, the risk is that the loan originator itself goes out of business. This has so far happened once, with Eurocent, a Polish loan originator, going bankrupt. As of today the funds I had invested with Eurocent loans have not been recovered, although there is still some hope that some funds will eventually be returned to investors. I personally treat those funds as bad debts and assume they won’t ever be recovered.

Some people have thus asked me where is the risk in investing in Mintos when loans come with a buyback guarantee. We will have a look at the risks later but to answer that question, the risk is that the loan originator itself goes out of business. This has so far happened once, with Eurocent, a Polish loan originator, going bankrupt. As of today the funds I had invested with Eurocent loans have not been recovered, although there is still some hope that some funds will eventually be returned to investors. I personally treat those funds as bad debts and assume they won’t ever be recovered.

There are no costs to investors when using Mintos. Taxes are to be declared and paid in your country of residence and Mintos thus not withhold any taxes. Rest assured though that this won’t be a hassle as it’s pretty straightforward to declare your income from P2P platforms in your tax return. I suggest you consult an accountant the first time you do it, and for the subsequent years, you can do it yourself.

Mintos is therefore just the go-between bringing together loan originators and investors. This allows investors to use one website to diversify their investments across several countries, loan types and even different currencies.

You can deposit either Euros or USD into your Mintos account, and there is a 1% charge for currency conversions. I have actually used Mintos to “save money” on currency conversions, feel free to take a look at my separate post on how to save money with currency conversions.

Mintos is more than a usual P2P lending platform, it is a marketplace for pre-funded loans. Instead of accepting borrowers and listing their own loans, they are working with several loan originators and list loans to the marketplace. This allows investors to diversify the investments between several countries, loan types and currencies. Loan shares are listed on the Mintos marketplace, where the minimum investment is €10 per loan and annual returns as high as 14%.

So, to recap, in simple terms, here’s how Mintos works:

- Lenders place loans on Mintos to finance their operations

- You invest in loans, thus providing financing to lenders

- Borrowers pay back loans in monthly installments

- You get the earnings and invest again or withdraw

Who is Investing on Mintos?

You might think that investing is something exclusive that only very knowledgeable people can partake in, but this is not true. Anyone with a basic knowledge of money and an interest to learn more about it is a good candidate for investing in P2P lending.

I spoke with Mintos and asked them about the typical profiles for their lenders, and they told me that they come from all walks of life and the amounts invested range from a few hundred euros to millions of euros. In the end, it doesn’t matter how much you invest, everyone can get the same returns on their investment in terms of percentage ROI.

You might also be under the false impression that only residents of certain countries are allowed to invest. This is far from the truth, as you can invest from all over the world, with only a few restrictions based on EU regulations. If you’re an EU resident, you can definitely invest.

To give you an idea, the top countries I’m seeing new investors join from after reading my articles or contacting me are the following: UK, USA, Germany, Netherlands, France, Spain, Belgium and Malta.

I’ve also seen strong activity from Asian countries such as India and China. I think Mintos is proving to be an excellent way for non-European investors to gain access and exposure to the European market and earn Euros, which is also a way for them to hedge against currency risks.

Mintos is open to both private and corporate investors. So if you want to invest via your company, you can easily do so.

What Can You Invest in?

At Mintos, investors can invest in different types of loans originated by many different loan originators.

Loans can be of the following types, and you can, of course, limit your investment to specific types when setting up your auto-invest.

- Mortgage Loans

- Car Loans

- Invoice Financing

- Business Loans

- Short-term Loans

- Personal Loans

- Agricultural Loans

In March 2020, Mintos has added Buy Now Pay Later platforms as well. The first one to join is Revo Technologies which is active in Russia, Poland and Romania. For those of you unfamiliar with such platforms, I’ll explain how it works in a nutshell. All across Europe, more and more shops are adopting a microloan facility at checkout, where you are able to buy the product and pay later. These microloans are managed by companies like Revo.

So say I want to buy a Playstation but only have €100 in my bank account; I would be able to choose the buy now pay later option at checkout, then pay it by installments over several months.

Where Can You Invest via Mintos?

Another question is which countries you can invest in via Mintos. To make sure we are well diversified, it’s important that we spread our investments across different countries to reduce our reliance on any one country’s economic performance. We can further add another layer of diversification by investing in loans denominated in several different currencies.

With Mintos, you have the option of investing in 30 different countries and 12 currencies. This makes it the most well-diversified platform that I know about. Over the past two years, Mintos has been expanding the investment opportunities on the marketplace beyond Europe by offering loans in Africa, Latin America, and Southeast Asia.

How I’m Investing in Mintos

I am currently using several auto-invest profiles that I tweak every few months as necessary. If you don’t feel confident setting up all the parameters of auto-invest, you can use one of the three preset strategies offered by Mintos, and I’ll delve into that later in this article.

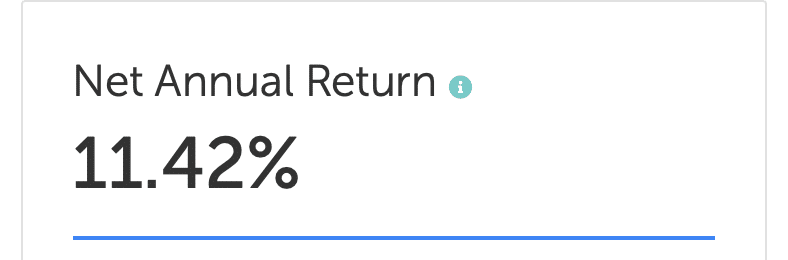

As you can see in the screenshot below, my net annual return is 11.42%, which is a rate I’m very happy with, considering the measly returns obtained if I leave the money in a savings account at the bank. Of course, there is much more risk with P2P loans, but the return rate of more than 11% adequately factors in the added risk.

You might see other financial bloggers report higher returns, which you can certainly achieve if you go for longer-term loans. I tend to stay within the 24-month range for my loans, as I feel it gives me some extra flexibility if I decide to re-allocate my funds to better asset classes at a later point in time.

I’ve been able to achieve 11,42% returns during my two years of investing with Mintos.

I have invested over €150,000 into the platform, and had one loan originator, Eurocent, default. Because I make sure to diversify the funds widely and also use the buyback guarantee feature, I only lost around €600 which is dwarfed in comparison to the profits made so far on Mintos.

Due to having invested a substantial amount in Mintos, I get to have my own personal contact on the platform, so whenever I have any queries I can bypass the general support system and go to my contact directly. I really appreciated this as it gives me extra peace of mind knowing that there is a specific person who knows me and the way I invest and can answer my queries that same day. Although this is not something that is advertised on the Mintos website, I believe they assign a personal contact once you invest more than 50,000 euros on the platform.

However, even if you don’t have a personal contact at Mintos, you will still be able to get great support via email, phone or their online chat. In fact, whenever I need to check something quick I typically use the online chat facility on their website.

Mintos Preset Strategies

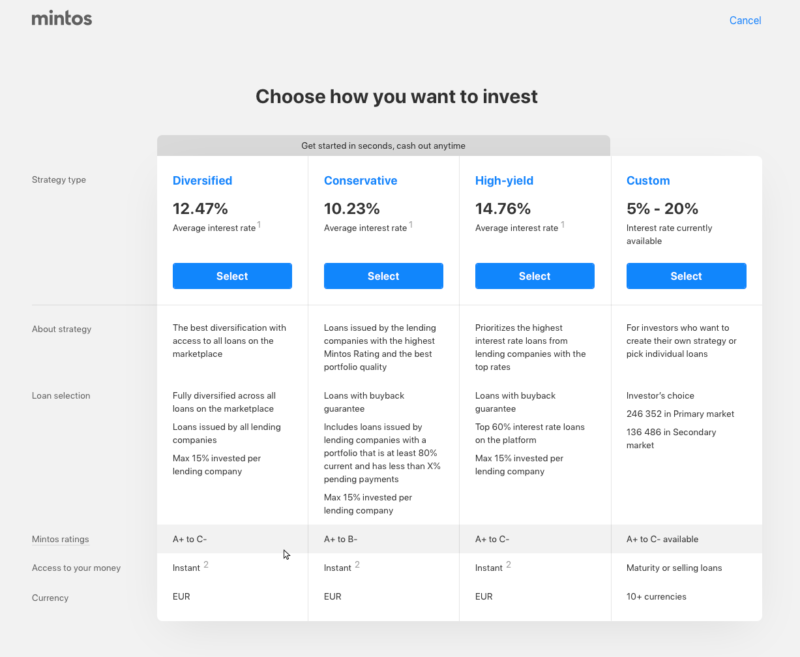

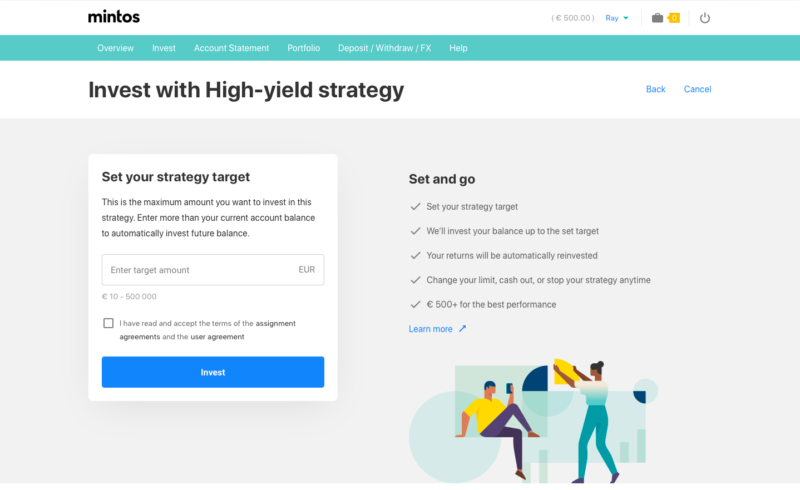

One of the new things Mintos has introduced in 2020 is the Mintos strategies. These are three strategies that have been designed keeping investor feedback in mind and are a convenient way to start investing in Mintos if you don’t have much experience in P2P lending.

Diversified

The Diversified strategy will give you the highest diversification and is the most similar to the new strategies to Invest & Access.

- Fully diversifies your investment across current loans from all lending companies with a Mintos Rating of A+ to C-

- The algorithm prioritizes diversification

- Loans with and without buyback guarantee included – 99% of the loans on Mintos have a buyback guarantee

- Maximum exposure of 15% in each lending company

Conservative

The Conservative strategy invests in loans from lending companies with the best portfolio quality.

- Invests in current loans from lending companies with a Mintos Rating of A+ to B-

- The portfolio of the companies is at least 80% current, and it has less than 10% pending payments

- The algorithm prioritizes risk reduction

- Loans with buyback guarantee

- Maximum exposure of 15% in each lending company

High-yield

The High-yield strategy invests in loans with the highest interest rates.

- Invests in loans with the top 60% interest rates and a Mintos Rating of A+ to C-

- The algorithm prioritizes returns

- Loans with buyback guarantee

- Maximum exposure of 15% in each lending company

Mintos strategies are a fully automated way of investing. To get started, you just select the amount you want to invest. You’ll get a portfolio of loans that is diversified according to each strategy’s priorities. Your exact portfolio mix automatically adjusts to the market.

These strategies offer additional liquidity: If you want to access your money sooner, they come with a cashout option that lets you access your money faster (subject to market demand).

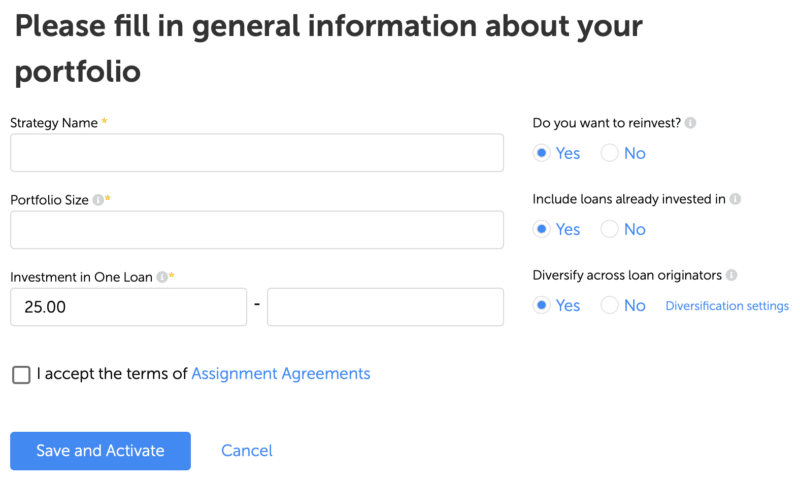

Using Custom Strategies

Obviously manually selecting thousands of loans to comprise your portfolio is a very inefficient way of doing things, although it might be a good way to test the waters if it’s the first time you are dealing with a peer to peer loan platform. It is perfectly OK to invest a set amount and then just wait a month or two to judge the results of your investment and learn how the platform works. Once you’re confident about the platform, you can then set up an auto-invest strategy and be well on your way to passive income.

You have to be careful when setting the auto-invest parameters on Mintos, because the biggest risk you face is that of a loan originator going bankrupt, and that has happened in the past. Check out the Mintos lender ratings post on Explorep2p as well as the Mintos loan scanner to see which are the most trustworthy lenders on the platform.

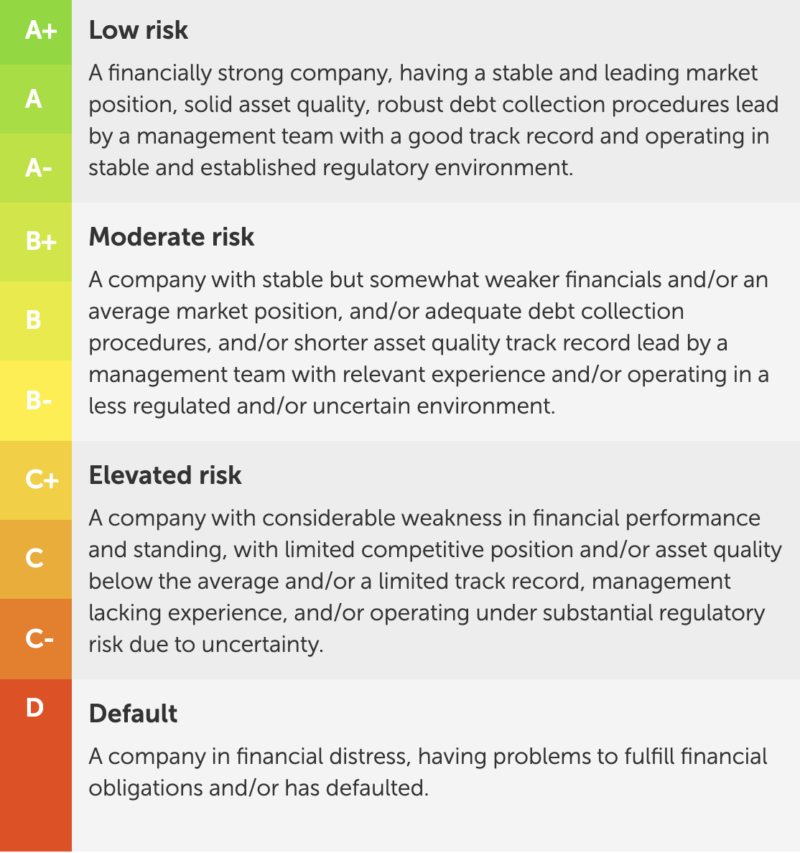

In 2018 Mintos also introduced risk ratings for loan originators offering their loans on the marketplace. The Mintos Ratings are on a scale from “A+” to “D”, representing the lowest and the highest counterparty risk respectively.

Here’s how I go about building a custom strategy.

By setting up auto-invest with a custom strategy, we are looking to combine the benefits of compounding interest with the safety of the buyback guarantee.

The first step when creating a custom strategy is that of choosing the loan originators you want to invest in. Keep in mind that there are several loan originators that are not profitable and are relying on their seed investment runway until they do achieve profitability. I prefer to use those that have already proven that they know what they are doing and are turning healthy yearly profits.

We have to keep in mind that peer to peer loan investing is in itself a risky proposition, so there is no sense in increasing that risk by going for unprofitable loan originators. Once you consider all loan originators, you might end up with 15-20 of them that you are comfortable investing in.

Beyond that, you can set up a bunch of other parameters like the loan duration, rate of return, countries, loan types, whether they have buyback or not etc.

A lot of these parameters will depend on your goals, so there is little sense in telling you my exact parameters, because even then, I go in and change them every now and then depending on what I want to achieve during a particular period.

Real Estate Investment Opportunities with Mintos

Mintos offers a unique opportunity for individuals looking to diversify their investment portfolios with real estate, without the need to purchase entire properties or take on the burdens of property management. Through the Mintos platform, investors can easily participate in rental residential real estate projects, starting with as little as €50. This low entry point makes real estate investment accessible to a broader audience, providing an easy and affordable way to get started in the real estate market.

One of the key advantages of investing in real estate through Mintos is the ability to earn a regular income stream from rent payments. By investing in rental residential properties, investors can receive a share of the rental income collected from tenants, providing a steady and predictable cash flow. Additionally, investors may also benefit from potential capital appreciation, as property values tend to increase over time. This dual income stream helps enhance overall returns, making it a highly attractive investment option.

Mintos also offers liquidity through its Secondary Market, allowing investors to buy and sell their investments if needed. This provides flexibility for those who may need access to their funds before the investment term ends. The platform’s approach simplifies real estate investing, eliminating the complexities of direct property ownership and management while maintaining the benefits of income generation and potential capital growth. This makes Mintos an ideal solution for those looking to diversify into real estate while keeping the process hassle-free.

Investing through Mintos not only provides a way to gain exposure to the real estate market, but it also offers an easy and efficient approach to portfolio diversification. Whether you’re a seasoned investor or just starting out, Mintos provides a straightforward way to access the potential benefits of real estate, with minimal capital requirements and without the headaches typically associated with managing rental properties.

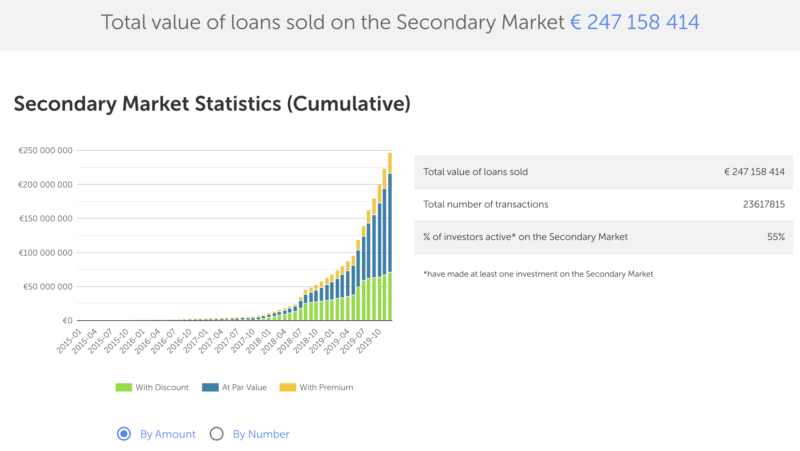

The Mintos Secondary Market

I think the secondary market deserves its own section as it has become such an important part of the platform. The secondary market is what gives Mintos the capability to have such high liquidity for its investors. I know investors who have sold over 1 million euros from their portfolio in just a few days’ time. The way to offload loans if you need cash is to sell them on the secondary market.

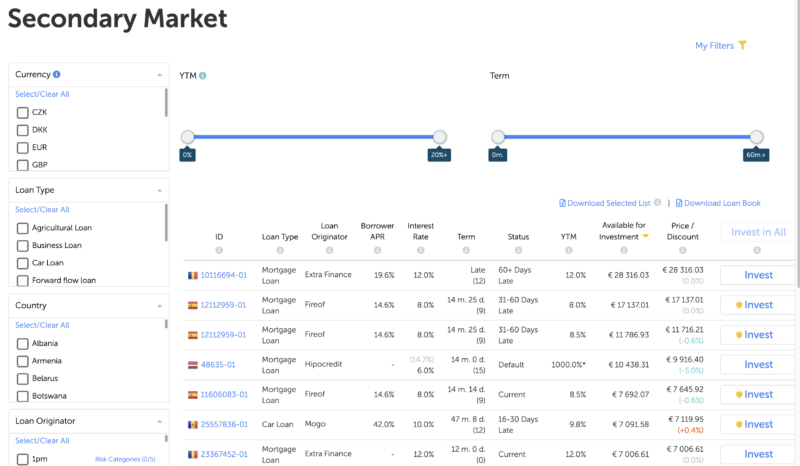

Buying and selling loans on the secondary market is very easy. If you want to buy, you can set up an auto-invest strategy to pick up loans specifically from the secondary market, with the same criteria as you are able to set up for the primary market.

You can also manually buy loans from the secondary market from the dedicated page on the Mintos website (shown above). You can of course filter according to your wishes and then click the Invest button to buy those loans. Many investors try to pick up good loans at a discount and thus improve their rate of return even further.

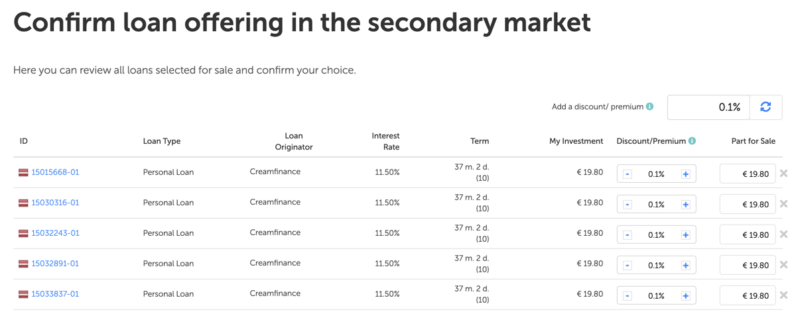

If you are looking for very quick liquidity, you can select the loans you possess, and then hit the Sell All button to sell them off on the secondary market. Before you do that, it would be a good idea to set a small discount on those loans, as that will make them much more likely to be picked up by other investors looking for bargains and extra profits.

The secondary market is huge on Mintos. As of writing this post, there are in fact more loans available on the secondary market than on the primary market.

There is a small 0.85% fee for selling loans on the Secondary Market. I think it’s a fair and transparent fee that will help Mintos stay profitable, and it’s on par with or below other leading platforms in Europe and the UK. Mintos reports 38% of active investors having used the Secondary Market, and about € 700 000 worth of loans sold each day on average during the last year. This 0.85% fee will apply to investors selling their investment on the Secondary Market, and will be applied after the sale.

The Secondary Market thus offers considerably liquidity to those investors who want to exit an investment early and is a very important component in this platform. If Mintos did not have such a good secondary market, I would not have invested such a big amount of money here.

Depositing and Withdrawing Money

You can withdraw money and deposit it without any delays when using this platform, and there are no costs for doing so. I know a lot of you have reached out to me to ask how they can avoid fees that are charged to them by their banks when withdrawing or depositing money from P2P platforms, and I can offer you a good piece of advice on that front.

I have several digital bank accounts set up that help me avoid any fees and also enable me to do currency exchanges at the best rates.

I currently use the following digital banks:

I can recommend all three of them. They all give you a free debit card as well so you can use it for shopping or when traveling. They work just like your local bank account but will likely have a better user interface, the comfort of online support and no ridiculous fees.

You can check out my post about depositing and withdrawing money from peer to peer lending platforms for more information about the topic.

Mintos Investor Club

A little-publicized aspect of Mintos is the investor club. This is a program that Mintos has created for its most valuable investors. Think of it as VIP treatment for investors.

We created this program to offer greater benefits to the most valuable and influential investors. It’s a way of showing our appreciation for having you on Mintos.

If you invest more than €50,000 on Mintos, you get a personal investor service associate who is available via phone or email to discuss things with you should you have any queries or problems.

I’ve had two service associates so far and they have both provided a fantastic service, responding to my email queries within a day and providing information that was not publicly available on the platform.

Here are all the perks for being in the investor club. Once you reach €50,000 invested, you will see a notification when logging in to Mintos, telling you that you are now part of the club.

- Skip waiting lines and reach your personal Investor Service Associate whenever you need assistance on Mintos Marketplace.

- Be the first to know and try our new features, pre-launch versions of our upcoming products on Mintos, and get to share your feedback.

- Get special deals for fintech events sponsored by Mintos. When possible, join investor meetups with Mintos CEO and team.

- If you need specific data of your current or historic investments on Mintos, we can export custom spreadsheets on your request.

I had, in fact, asked my service associate to send me a weekly report showing the performance of my investments, a request which was duly and rapidly attended to. I find receiving an email report more productive for my workflow than having to login to the platform regularly. I like to keep my investments as hands-off as possible.

In the near future, I don’t think I will need the reports that much, as the mobile app does such a fantastic job, as I detailed earlier.

Mintos Loan Originator Ratings

When you set up an auto-invest strategy, you will notice that all loan originators have been assigned a Mintos Rating. The Mintos Rating is meant to be a gauge for each loan originator’s financial and operational stability. According to Mintos, the loan originator’s ability to service and originate loans is the most important factor when assessing loan originators. In addition, the financial standing of the loan originator is a material factor when the buyback guarantee is provided to investors.

Ultimately, the Mintos Rating measures the counterparty risk or risk of loss resulting from a loan’s originators’ failure to service and/or transfer the received payments from borrowers to investors or meet other contractual obligations (including but not limited to the buyback obligation). Counterparty risk is capturing operational and default risk of the company acting as a loan originator, servicer of loans and obligor of the buyback guarantee to investors. The materialization of those risks would cause a disruption in loan servicing and the buyback fulfillment which are the core risks related to loan originators on Mintos.

The rating is driven by five core factors characterizing each loan originator: operating environment (10% factor weight), company profile (15%), management and strategy (15%), risk appetite (20%) and financial profile (40%). Additionally, a support factor is incorporated for loan originators who receive guarantees from the group or a related company.

The Mintos Rating is based on information obtained during the initial due diligence process and data from ongoing monitoring. This includes the primary information from loan originators such as management interviews, site visits, audited and interim financial statements, corporate presentation, credit policy and risk control documents. The rating is updated annually, except in certain instances where a loan originator’s rating requires an immediate change. This could be due to a cash injection, positive or negative regulation being implemented in the country of the loan originator and so on.

I would recommend doing your own research in loan originators if you are investing big sums of money, else you can definitely use the Mintos loan originator ratings as your guide for smaller amounts.

💡 Potential Downsides of Investing with Mintos

Let’s have a look at the main risks of investing in P2P lending and Mintos in particular.

Loan Originator Risk

As we have already mentioned, P2P lending is a moderate-risk investment, and you must be aware that loans can default. With Mintos, you get a buyback guarantee as we discussed earlier. Thus the biggest potential downside of investing with Mintos is that a loan originator goes bankrupt, as I described with the Eurocent case above.

The only way to mitigate this risk is to keep an eye on the profitability of the loan originator. Most of them release their financial reports to the public every year, so you can see how they are doing. This is not as easy as it sounds, however.

Only 38% provide audited financial statements. Unaudited financial statements are not as trustworthy when compared to audited ones. You’re basically relying on what the business is saying about itself rather than what a trusted 3rd party (audit firm) is saying.

Almost 45% of loan originators are not profitable. It’s quite normal for new businesses in this space to be unprofitable for the first few years, but you also have to factor in the increased risk of them spending all the investor money before they turn profitable, which leads to complications including bankruptcy.

Around 80% of the loan originators are less than 10 years old, which means that they were founded after the last great world recession and we don’t know how they will perform if another one hits in the coming years. During a world recession, credit companies are some of the hardest hit as borrowers default on their loans due to having lost their jobs or having experienced severe pay cuts.

Interest Rate Risk

One other risk is that interest rates rise in the future, making it harder for you to sell your existing loans with lower interest returns on the secondary market, if you wished to do that. Of course, you could also just let the loans run their course and continue receiving payments until maturity.

When investing on P2P platforms, it’s best to invest money that you can afford to use without running into severe financial troubles. That way, you minimise the chances of having to sell loans prematurely, potentially at a time that is not advantageous.

Cash Drag Risk

Cash drag varies among different P2P lending sites, and thankfully this hasn’t been a problem with Mintos. Mintos is extremely liquid meaning that you can throw thousands of Euros at the platform and see them invested within minutes, and conversely, you can also sell your loans on the secondary market within a day or two.

Although it is not currently a problem, it could become so at any point in time, even though it might only be for a short time. If there is a surge in popularity for P2P lending platforms, we will have a situation where lots of lenders are competing to lend while there are not enough borrowers, which will result in a higher cash drag, because you have to wait your turn.

To put this into practice, let’s say that the interest rates you earn when lending are 10%, but, on average during the year, half your money is sitting as cash in your lending account with no borrowers available. With just half your money being lent and the other half in cash, it means you’re actually earning just 5%.

That’s an extreme example. Cash drag is not usually anything like that much. In fact, it typically reduces a 10% rate down to between 9.4% and 9.8%.

Considering these potential downsides, I think that investing in P2P lending platforms and Mintos, in particular, is a very good deal for investors, because there aren’t any other readily available investment opportunities with such a favorable risk-return profile.

Moreover, Mintos is currently the biggest platform in Europe and has proved itself to be competent by providing great communication with its investors as well as a very liquid primary and secondary market for loans for several years now.

Foreign Exchange Risk (or Opportunity)

You can invest in loans across 12 other currencies apart from EUR, including USD, GBP and RUB. This means that when you convert back to Euro, you might lose money depending on how the rates have moved in the meantime. This could, however, also be an opportunity to make extra returns. I’ve seen investors using currency arbitrage to raise their overall returns to 15-20% which is really impressive.

I like to keep things simple myself so I only invest in Euro. I also use Mintos to minimise the cost of currency conversions.

If you want to invest in other currencies, I would recommend using a platform like Wise; in that way, you’ll avoid the Mintos commission on exchanges.

❓Frequently Asked Questions about Mintos

I’ve spoken to many people about Mintos and I get to hear many questions that investors seem to have in common, so I’ll try to address them in this section. If you have any other questions you’d like me to address, just leave a comment below the post.

How can I reduce the number of late loans? e.g. 1-15, 15-30, 30-60 etc

I don’t think you can really avoid that unless perhaps you study your portfolio’s performance and identify if there are any specific factors that result in loans being regularly late, for example, loans from a particular country or a particular type. This is not something that I’m too concerned about, plus I don’t really get into hyper optimization with my portfolios as I don’t feel it justifies the time investment given the yearly returns. Therefore I haven’t done such a study myself. However, if any of you reading this post do conduct such a study, I’d definitely be interested to know what you find out.

What are pending payments?

In your dashboard, you will sometimes see some money that is marked as pending payment. This means that Mintos is gathering the money and preparing it for distribution.

If this happens, you will be compensated for the delays in settling pending payments.

The interest on pending payments is 1.2x the interest of the loan in question. You can expect to receive the interest weekly, once it’s paid by the respective lending company.

The interest will be calculated for both the principal and interest and the calculation will begin after the settlement period (7 days) has ended.

How are loan returns taxed?

Mintos sends you the returns gross of tax; they don’t withhold any taxes. You will, therefore, have to declare the income in your country of residence, as explained in further detail in my post about P2P lending platform taxation. I’ve also written a post about how crowdlending is taxed in Spain specifically.

Do you recommend just investing in Mintos or do you recommend spreading your money across different platforms?

Mintos is my preferred platform and its where I invest most of my P2P portfolio, but I would always recommend spreading your capital across different platforms.

What returns can I expect?

Over the past three years, my experience and that of my fellow investor friends have shown that you can achieve anywhere between 10% and 14% returns depending on how you invest. Every platform has its own average return and that also depends on the amount of risk that you are assuming with the loans on that particular platform.

I don’t have as much capital as you to invest, what is the minimum to invest at Mintos or P2P sites in general?

I would say that you can start with as little as €1,000 to see how things work on any of my recommended platforms, but to make any meaningful income you need to invest at least €10,000. Anything less than that is not worth the time and hassle in my opinion. If you have more than that amount to invest, then it’s even better.

Does Mintos allow investments in cryptocurrencies?

No, this is not something that Mintos provides at the moment, but I wouldn’t be surprised if they branch into this area in the future. For now, you could have a look at my article on the best P2P crypto loan platforms.

I am a bit worried about having a significant number of loans that are late. Is it normal?

Yes, it’s normal to have a good portion of your loans being late with their principal and interest payments. Here’s my breakdown in percentages:

- Grace Period: 3.4%

- 1-15 Days Late: 7.5%

- 16-30 Days Late: 12.6 %

- 31-60 Days Late: 6.7%

As you can deduce, around 30% of my loan portfolio is late, but that doesn’t mean I should start to worry, as all my loans are covered with a buyback guarantee.

There should be no loans beyond 60+ Days Late if you’re using buyback guarantee, as that would mean that the loan originator is having problems buying back the loans and is likely going to go bankrupt. The only loans I have in my account that are 60+ Days Late are in fact all the loans belonging to Eurocent, which went bankrupt last year and is currently in administration.

How long would it take for me to sell all my loan portfolio should I need quick liquidity?

From my experience in tests I’ve conducted and also those done by other investors I’ve spoken to, it takes between 24 to 72 hours to sell a complete portfolio. Size doesn’t seem to be a problem, as I know people who have sold 7 figure portfolios on the secondary market in this short timeframe.

Whether you can sell your loans at par or whether you’d need to apply a discount depends on what kind of rates loan originators are offering at the moment you decide to sell versus what rates they were offering when you bought. For example, if you invested in Mogo loans at 11% 6 months ago and the average for Mogo loans is now 12%, nobody is going to buy your loans unless you offer them at a discount.

In the end, you might have to give up an equivalent of a week or two of interest income to sell your loan portfolio, which I think is a good tradeoff.

I see capital gains in my account, how is that calculated?

Mintos calculates the positive gain on a loan-level for investments on the Secondary market. For example, if an investor invested into a loan this year and it will be fully repaid only the next year then in the capital gain of this year the gain will not be calculated as the income from the loan is lower than the invested amount. Unfortunately, it is not easy to calculate as Mintos looks at all the previous years as well.

Here is an example: In 2018 an investor invested 90 EUR in a loan and in that year he received 100 EUR from the borrower and the loan finished. Then for 2018, the capital gain will be 10 EUR.

If however in 2018 an investor invested 90 EUR into a loan and only half of the principal was repaid, then for 2018 the capital gain will be 0 EUR. If the loan will be repaid in full in 2019 and the total funds received will be 100 EUR, then the capital gain for 2019 will be 10 EUR etc.

The data can be found under Account Statement, but then you have to look at all the previous years in which you have earned with Discount / Premium on Secondary market transactions and which loans were fully repaid in 2019.

Mintos Mobile App

The Mintos mobile app, another new addition in 2020, provides a significant differentiator for Mintos when compared to other competitors in the space. It’s extremely well-made from a technical and usability point of view. My background is in creating software so I know a well-made product when I see one. I’ve also used and cursed at a ton of banking apps that had the most horrifying UI and nonsensical errors thrown at their users.

There are no such mishaps with the Mintos app. It has a light and dark mode (white or black background) and it shows you all the most important stats about your investments. You can also withdraw or deposit money directly from the app, and soon you will also be able to operate in the primary and secondary markets.

With that last feature in place, you will most likely never need to login to the website again. Given that most people operate exclusively from their phones these days, it’s an obvious step for platforms such as Mintos as they strive to reach a wider audience and make things easier for their existing investors.

I especially like the stats section as I can quickly check the vital stats on my money, including the countries I’m invested in, the lending companies, the average interest rate, average remaining term and amount of late loans. These are all stats that are also available on the site, but they are not as easily and readily available. Let’s not forget that there is much more friction in sitting down at your desk, opening a website, logging in and navigating to the pages you need, when compared to opening a mobile app that’s always logged in and shows pretty and easy-to-read stats immediately.

What Improvements Would I Like to See from Mintos?

Better Statistics

We can see the cumulative number of investors on the Mintos statistics page, however, there is no clear indication of how many joined users joined every month and more importantly how many of them are even active. Many users can sign up but then never invest, and that is not reflected in the stats.

The same goes for the investment volumes section of the statistics. We can see the cumulative investment growing month by month, but we don’t have information on how many new loans were issued each month. This would give a clearer of volumes month by month.

With regards to loans, Mintos gives us a breakdown of Current vs Delayed loans, but in reality, the term “Current” is not 100% accurate. It is a catch-all for recently issued loans that have not reached their first repayment date, as well as those loans that have been paying back principal and interest successfully. There is obviously more uncertainty and risk with loans that have not started their repayments, so they should not be bundled together with the others that are being repaid already.

Ownership & Related Parties Transparency

There are some long-standing doubts about the ownership of Mintos and its relation to some of the loan originators on the platform. The ultimate beneficiary owner of Mintos is Aigars Kesenfelds. He is currently the true beneficiary of 81 Latvian companies. At the same time, he owns no shares in any company.

This businessman is the true beneficiary in several real estate companies, as well as a firm that offers self-service carwash – SIA Wash and Drive, AS Skanstes Biroju Centres, SIA Mintos Finance and others. Kesenfelds’ interests in those companies are represented by AS ALPS Investments, as well as Malta-based Dyonne Trading & Investments Limited and other companies of this kind.

Since June 2018, the number of businesses in which Kesenfelds is registered as the true beneficiary has increased by a total of 19 companies.

More Details on Loan Originators and Their Loans

I’d like to see more details such as audited statements for each loan originator, as well as a breakdown of loans issued by country, default rates and recovery rates.

Previous Concerns that Have Been Addressed

I have previously criticized Mintos over its lack of profitability and lack of transparency in the ownership structure. However, both issues are now solved, as Mintos is profitable and has a healthy cash balance in the bank, and the shareholders and original founders are clearly mentioned on the site now.

As for regulation, there is an upcoming European-wide regulation that Mintos will abide by, so I’m not so worried about this aspect.

Mintos Alternatives

Many people are skeptical about P2P lending platforms and prefer to diversify their investments across multiple platforms in case things go south on one of them. While I think Mintos is currently the best platform in Europe, there are others that are right up there vying for that number one position with Mintos. They would be worth looking into and possibly used to diversify your portfolio along with your Mintos investment.

Here are my favorites:

- Peerberry (11.54% average return)

- Swaper

- Lendermarket

Another related sector you can consider for investing at good rates is that of crypto-backed loans. Basically, the idea is that borrowers provided their crypto as collateral when obtaining funding. You can read my review of the best crypto-backed lending sites for more information. YouHodler and Nexo are my favorites.

Final Thoughts on Mintos

I’ve been investing on Mintos for over four years now, and I’ve seen the platform grow from strength to strength.

I think one should be realistic and understand that this is an area of investment with a certain degree of general risk, and I would like to see Mintos to improve in certain areas as mentioned above, however, when I balance the risks versus the return I feel that investing in such platforms, and Mintos in particular, is justified.

I keep a certain part of my net worth constantly invested in P2P lending platforms to take advantage of their fantastic returns, and Mintos by far holds the biggest portion of this investment. I have no plans of changing that in the near future as I have been very happy with the performance so far.

Therefore, we can wrap this up by saying that Mintos comes highly recommended from me. Please leave any questions you have about the platform below and I’ll be happy to answer them.

Summary

I’ve been investing on Mintos for the past four years with great results. I highly recommend Mintos for any P2P lending portfolio.

Pros

- Great liquidity

- Straightforward to start investing

- Well established platform

- Buyback guarantees

- Mobile app

Cons

- Risk of loan originators defaulting

I just would like to say i really Hate mintos .. i lost more than 15k on LO that went bankrupt. And mintos is doing nothing about it .. its basicly a big scam money dissapears in to thin air . Fack you mintos 🖕

I’m sorry about your loss Michael, and understand how frustrating it feels, however that doesn’t make Mintos a scam.

I’ve also lost money on this and other platforms due to loan originators going bankrupt (it might still be recovered when the court case is finalised, but nobody is counting on that). However loan originators going bankrupt is not terribly uncommon, especially in the current economic crisis we are in. The P2P lending game is all about diversification and there’s a decent element of risk as well, given that we are dealing with an alternative investment class with high returns.

I define a scam as being one where there is gross negligence from the platform’s leadership team or the platform being a scam by design. I’ve written about those platforms that I think fall under this heading, but Mintos is certainly not one of them.

I used to have a very positive opinion on Mintos, but currently ~1/3 of all my funds are ‘in recovery’ meaning that I am quite likely to never see them again…

So instead of +10% ROI I will have -25% ROI…

And some of those ‘defaulted’ companies had B/ B+ ratings, so not that I was just hunting for the highest rates from the most risky lenders

I’m sorry to hear that Bart, although all is not lost yet and they still have a chance of being recovered. While I still get the returns described in my review, it is also true that depending on the choices made with auto invest you might be unlucky, and that is why it’s important to diversify among the top loan originators to minimise these kinds of big swings in returns.

Yea same here mintos is just coming with bullshit answers . Lost more than 15 k here 👍

Hi Jean,

Really good information you shared here!

I have one question though that is not covered: what diversification settings do you use in the custom auto investment settings where it says “diversify across loan originators”?

Some use for every loan originator the same share, as 2%, but does that even make sense, I’m wondering. Because originator A offers many many more loans than originator Z, for example. Like this, you would have to wait for a loan from originator Z, because you reached your 2% with originator A.

What’s your view on that?

Thank you very much!

Good question. I look at the ratings on Mintos as a first filter, and only invest on the top rated platforms. There are other websites that also review loan originators, so I look at those two, and finally I also take a look at the websites of the originators and their financial performance in recent years. I only invest in the loan originators that pass all the mentioned filters.

Are there any p2p platforms in EU who will lend to an Australian resident?

Hey!

You mentioned Mintos as platform is profitable and the importance of that fact when comparing with other platforms – I agree with this point 100%.

However, Mintos just released their Consolidated annual report for the year 2019 a few days ago on 14.07.2020 and it looks like they made a loss in 2019. What’s more it looks like 2018 was not a profitable year either.

I was interested what are your thoughts on that? Thanks!

Good point Georgi, the answer to that question is that Mintos was in high growth mode in 2019 and they hired many people in order to expand into other countries and attract both new loan originators and new investors. They had to downsize in 2020 when COVID hit and were able to do so without significant problems. The funding they have allows them to run at a loss while pursuing growth, but as a model it is profitable.

Hey! Thanks for getting back to me on that one – appreciate that!

I agree with you in general – it’s normal for a growing company to not be profitable. I thought they were out of that stage after the reported profitable year, but apparently they were still expanding. Even though I would be more confident if they were making money I don’t see it as big risk either.

Se fai i 600 ora, quando saranno fatti i restanti 2100?

I’m not sure what this is referring to.

Hallo Jean ,

I did like you blog very much !I am new in P2P lending and indeed i took much information from you !

So thanks and stay safe !

Thanks for your comments Georgios.

I tried the 0.5% bonus link, but it doen’t seem to work. Could it have anything to do with COVID-19?

They have temporarily deactivated that promotion.

I have been an investor with Mintos for more than 3 years with $xx,xxx amount invested into their loans. However, after I decided to withdraw the money all the issues started appearing.

It has been more than 2 weeks with me chasing their CS team daily to report on withdrawal transaction that allegedly happened a day after my request.

Thus far, no money, just promises to investigate by Mintos team have been made. Beware, unfortunately, a good investment vehicle has suddenly turned a headache with a potential significant loss.

Hi Juius, I’m sorry to hear about your experience. Have you tried asking your bank as well? I have made several small withdrawals in the past two weeks and they arrived within 2 days in my TransferWise account. I usually recommend using a digital bank such as TransferWise as all things happen faster and more efficiently. Many local banks are now in crisis mode as they are not used to have a distributed workforce, so things might be more delayed than usual.

Any update on getting your money back?

I can only agree with Juius comment. Once I tried cashing out investments, the problems started. First customer service said it was a bug, then everything was working perfectly and they just had a delay in the transaction. The fact is, that it has taken more than 2 weeks of going daily to the website to make withdrawals and I still did not manage to get it all back. This is obviously excluding all the investments that are in recovery from lenders defaulted or suspended.

This must be a one-off problem related to your bank account, since I’ve done many withdrawals over the past 5 years from Mintos and not once did I have a problem. I’ve used multiple bank accounts including TransferWise.

Quote from your post:

“If you invest in Mintos today through this link, you will also benefit from 0.5% cashback. That means that if you invest €10,000, you will get a cashback in your account of €100.”

0.5% of €10,000 is €50, not €100.

You’re right, it was 1% for a while and when it changed to 0.5% I forgot to adjust the calculation. Thanks for pointing it out.

I asked TargetCircle about the bonus and they said 1% is still in play. You might want to re-check the offer and let me know too.

The cashback for investors is 0.5% as of March 2020. I will update the post if this changes again in the future.

Hello Jean, thank you for your review.

I am newly entering into P2P platform investing, concretely i have seen only Mintos. I have a banking background and i am still not clear on some issues.

From what i explored from Mintos so far, it looks to me that except the rating of the loan originator, there is no other important information to evaluate the risk of default of any given loan in the platform. On the other hand, it is surprising to see that there is no clear correlation between loan originator risk rating and interest rate of the loan. Also as far as i have seen there is no information on how many cases the loans have defaulted when buy back option is not active or if the buy back option has been executed in the favour of the investor when the loans have had such option. As far as i remember from your post as well, you have not given such information as well, except for the portfolio defaulted due to bankruptcy of the loan originator. So can you please share what has been the number of loans that you have invested so far and has been the default rate (both buyback guaranty included/excluded).

when i look at the loan database i dont know where to start to make the selction of the loans to invest becuase there is no information regarding the default history of both loan clients and loan originators. How did you select the loans that you invested, what kind of criterias did you use?

Also, from a search from internet i encountered some information about a Latvian guy Aigars Kesenfelds, who is one of the founders of Mintos and who is also main shareholder of many loan originator companies listed in Mintos. if such thing is true to me this may be very concerning about the reliability of this platform. Do you have any information about such issue?

i would be very grateful if you could give feedback

thanks

Informative post it must have taken you a good time to write 🙂

But why are you hiding your account overview? the numbers are important to your credibility like other bloggers and reviews that promote them right?

You told us about your average interest and amount invested already in writing so to prove that it’s correct for your portfolio you should show the whole overview, Account balance, net return rate and my investments how big portion of the loans you have that is in what stage of current, late and bad debt…. Transparency is the key and these numbers don’t make sense of hiding from that perspective as long they are true. So hope you can update that for people to see how your account rly is doing than just empty words if you get what Im sayin.

Cheers

Hi Emil, thanks for your feedback. I’m of the opinion that the sharing of figures and doing monthly reports are not of benefit to the reader, and to a lesser degree also not beneficial to the blogger. I have shared my thoughts on this in a separate post. You’re most welcome to continue the discussion in the comments section of that post.

Sir this blog is really helpful glad ive found this one

Sir good day good job on this blog that youve created the basics and everything youve tackled i was eyeing on mintos for this year to begin with, question is so for novices invest & access for the beginners and auto invest is for the ones who already studied the platform right?

Hi Daniel, that’s what I would recommend, but you can also try Auto Invest directly if you want. Invest & Access also has the benefit of easy liquidity as the process for cashing out from your loans is easier. But you could also sell the loans in an auto invest portfolio.

If you’re interested in the subject and don’t mind experimenting, I would encourage you to put some money in both options.

I’ll post a separate article on my thoughts about setting up auto invest, that should be helpful.

Hi Jean,

Thanks for the detailed review of the Invest and Access feature. Being new to P2P lending as an investment I found your articles to be very helpful.

I was about to start off with Mintos (just deposited some funds and waiting for them to show in the account to be precise!) and was unsure whether to use the Invest and Access feature vs auto-invest profiles. Given that this article was originally written around six months back I’d just like to verify if you’ve experienced any additional downside to using Invest and Access and if you recommend it over profiles.

Thanks and best regards for the new year!

Hi Simon, welcome to the world of P2P lending!

I keep my articles updated and post back if something changes in a significant way, so what you read in this article is still accurate. I would say that Invest and Access is a good idea to start off with. As you read more and become more confident, you can try to set up your own Auto Invest profile and see how the two compare.

Hi Jean,

What do you think of the recent Mintos Pending Payments? I am afraid they are trying to ‘mask’ loan defaults….What do you think? Also especially of the recent LuteCredit and Monego Issues….

Thanks

At this point Mintos is the platform I trust most, so I don’t have any suspicions of malpractice from their side. However we need to keep in mind that they are only aggregators of loans.

In order to protect ourselves from negative outcomes such as defaults it’s on us to diversify properly across multiple loan originators and types of loans as well as avoid those loan originators that are a bit shaky or operate in markets that are highly unstable.

I think it’s also healthy to be conscious of the fact that over the long term most investors will get hit by some defaults, but the profits would have more than covered those small losses, hence in the grand scheme of things it’s not that big of a deal.

Thanks Jean. Up till now actually, I never read about loan defaults on Mintos (with buyback of course). Hopefully, they keep it up 🙂

in the meantime, all the best mate 🙂

There have been loan originator defaults before on Mintos, and I mention it on this blog too. The most famous one so far is EuroCent. I was in fact affected by that default as I had money invested in Eurocent loans.

However, the profit during the year had more than covered the money lost in the default.

All the best 🙂

Pity about Eurocent :(…and they had buyback guarantee too if am not mistaken right?

Yes, buyback is useless if the loan originator itself goes bust.

Hello Jean,

I am new to investing. Currently I don’t have capital to invest, but I got new job with better income which left me with around 200-300 euros left, I would like to start investing this money rather than just let them sit in basic bank account. Do you think that Mintos is good option when I will invest on monthly base ?

Thank you for your opinion and feedback !

BR

Adam H.

Hi Adam,

I’m not a financial advisor and even if I were, it wouldn’t be responsible to give you a yes or no answer without knowing your full situation and goals, however I can tell you that I personally invest in such a way on P2P platforms like Mintos with great returns so far.

The good thing about P2P loans is that your money is still very liquid, and you could also use something like Mintos’ Invest & Access system for an easy start.

Stocks are also pretty liquid, but quite volatile and you need to really know what you’re doing if you’re going to be picking stocks. Since you’re a new investor I wouldn’t recommend that unless you are investing in a stock index.

Real estate crowdfunding websites are another option, but your money would be tied up for longer terms when compared to P2P loans, so that’s something to keep in mind.

I’ve written about all these different options for investing on this blog, so you can read about them in more depth. Happy to answer further questions.

Hi Jean, I got a question. Apart from the sad example of the Eurocent, have you had any defaults on the loans in your portfolio (those with or without buyback guarantee)?

If so, what would you say is the % of ‘bad’ loans vs all loans?

I’ve only had one loan originator go bust so far, and that is Eurocent. I’m not sure about the percentage, but it would be minuscule. I lost around €600 from the Eurocent default but I’ve earned several thousands so it’s been a positive experience overall by far.

Thanks for your answer Jean.

It seems to me that Mintos is one of the best investment deals out there (if your portfolio is diversified correctly). The risk is minimal, and the reward is decent.

I live in Russia, and I do expect Ruble to weaken vs its European counterparts in mid-/long-term, so earning % in European currencies can add some nice % ito gains in terms of RUB.

I agree Ilya. Given that you live in Russia and have first-hand knowledge of the situation there, you can also add the currency play into the mix for even bigger gains.

I stick to USD, EUR and GBP when investing as those are the currencies I use on a daily basis.

I’m trying to reconcile the average interest listed on the website of 11.89% https://www.mintos.com/en/statistics/, with the figures also on the website:

Repayments on principal € 3 371 495 180

Interest earned by investors € 68 318 003

I have no info on average length of loans, but a quick division gives 68/3371 ~2%.

Does it mean that the average loan on the platform has a 2-month length? How do the 2% reconcile with 11.89% on an annual basis?

Jean,

I have decided to calculate my own Net Annual Return and not rely on the one stated by Mintos.

I started this exercise on 14/09/2019.

My portfolio is very straightforward. I am only using “Invest and Access”. On 14/09 I stopped all deposits into my Mintos account. I have then developed a small Excel that takes the amount as at 14/09, takes the latest account value, and based on the number of days that have passes, annualises the Net Annual Return.

The formula is:

((Current Account Value – Account Value as at 14/09) / number of days passed) * 365

The result I get is constantly between 1.5% to 2% less than Mintos’ NAR.

I have waited for at least one month of data to start drawing the first conclusions … maybe it’s too early. But I believe the difference is too large.

Also, my investment target is set much higher than my current account value, meaning that all interest I get back are being immediately re-invested.

Do you have any experience on this i.e. the discrepency between the Mintos’ stated NAR and actual money returned in the portfolio? Am I making some wrong calculations in the formula?

Chris, you are correct about one month being too early. For some of the worse loans, you need to wait around 90 days until buy-back to kick in and interest for it to be paid as it affects your calculations.

Mintos also includes accrued interest in the calculations, but investors don’t see that piece of data and in such a way there is a difference between their calculation and yours.

Mintos uses XIRR and Nominal Excel functions for calculations.

Hope that helps.

I think that a super important point that you cited in your article is that Mintos in profitable. Not many platforms managed to do so.

This increases considerably the safety of the p2p lending platform compared to smaller ones that hide (don’t display) the fact that they aren’t.

Yes I definitely agree that it is a very important aspect of investing with Mintos Teo, thanks for commenting.

Hi Jean

Just wondering, have you tried withdrawing any of your funds?

Yes I had, no problems whatsoever, they arrive within the usual 1-3 days in the bank account.

Hello Jean, many thanks for sharing your deep knowledge of Mintos. I started investing literally today and I have a few questions: 1) What is the difference between Invest & Access and Auto-invest? To me, it seems like in both cases the investment is automatically handled by the platform, with the only difference that in Auto-invest you have more options for customising. 2) What about interest? How often is it paid and is it reinvested by default by the platform? Thank you!

Welcome to the club! If you haven’t read it already, I’d suggest you take a look at my review of Mintos Invest & Access.

You can think of it as a typical bank savings account but with much higher interest. There is a strong focus on liquidity so you should be able to withdraw your money from it at any point.

I would suggest that you use Auto-Invest for more long-term investments, although you could also sell those loans on the secondary market should you need to do so. It’s an extra step of manually selecting the loans and putting them up for sale, a step which you wouldn’t need to do with Invest & Access as in that case you would just request a withdrawal and the system will take care of the sales automatically.

Since Mintos already have plans in place to issue debit cards for their clients later this year, I believe that Invest & Access is their preliminary step to doing so.

To recap, the biggest differences are:

Does that clear up your doubts?

yep, thanks! I missed your first review, it’s clear now

I have been watching developments in Europe since 2013 with huge interest. From what I’ve seen, Euro seems to be an unstable currency. Political developments may eventually lead to the breakup of EU and euro and individual nations to return to their national currencies. Because of this, I am interested to be invested in P2P lending in UK (regardless of Brexit) and CH.

There are plenty of articles on the web mentioning how difficult it is for non-UK residents to invest in UK P2P platform. But the same can’t be said of P2P lending in Switzerland.

Perhaps as a European, you can offer me some insights on this. Why Swiss P2P platforms are not that interested in foreign money, why bloggers outside Switzerland don’t even bother writing about Swiss P2P platforms…

PS: too bad no p2p platforms outside Switzerland (including Mintos) offers CHF loans…

I’ve taken a look at the Swiss P2P platforms, and to be honest they don’t look quite as developed as pan-European platforms like Mintos. I don’t buy into the doom and gloom scenarios for the Euro as a currency and much less the potential breakup of the EU and the reinstatement of national currencies. I believe the world is becoming more globalized and the nation-state becoming less powerful of a concept.

Due to the above, I don’t have much interest in investing in the CHF platforms, although I agree that it would be an interesting hedging strategy.

As to why they might not be that interested in foreign money, I don’t know enough about them to comment on it. Potential problems might be the KYC and AML requirements implemented in European states and a lack of size to be able to support multiple countries (support in different languages is one problem).

The reason why bloggers outside of Switzerland don’t bother writing about the Swiss platforms is easier. The platforms are not so well-known, they might not offer attractive rewards to bloggers, they might not be available in English thus it’s hard to learn about them, the rates of return are lower than on EU platforms.

Jean,

I believe Mintos or other platforms could have expanded to Switzerland, but (to my best knowledge) none of them did.

Oh well, what do I know as an outsider…

Yes, I guess it’s due to regulations and a small market.

I am investing on Mintos too (40.000+ EUR) but I have no idea how can people reach the net return above 12% as a AVERAGE return. I was never able to reach this number so I don’t have a clue how this can be AVERAGE for so many investors as Mintos have.

I have tried many strategies but i found none working. So again: How this Mintos proclamation can be true as AVERAGE net return?

It seems to me not possible because regardless how many loan originators you use you will always have too many loans not paid in time. For me is this number around 20-30%+/- two years already.

Furthermore, how this 12% average can be real number after Eurocent defaulted?

Hi Conor,

Returns depend on how you set your auto-invest up. Right now, it’s certainly possible to get 12% returns as the interest rates are high at the moment. So if investors are talking about their returns over the past few months with specific auto-invest settings, then it makes sense for them to be seeing those average returns. In my opinion, anything above 10% is good for these platforms, and I don’t really chase the very high-interest loans as I don’t want to assume the extra risk.

It is also true that many loans are not paid in time, it’s just part of the way consumer loans work. The average delayed loan rate you mentioned seems normal to me.

With regard to Eurocent, I know several investors who did not have any loans from that loan originator in their portfolio, so they were luckier than me and it didn’t affect their returns at all.

What?

I am not talking about “investors chat” I am talking what Mintos is saying about average return on main web page (but today’s is changed already) – what is primary marketing info for new users and what you are proclaiming be true in your own article.

I quote you: “…The average net annual return for investors is 12.06% as of June 2019, with more than 150,000 investors…”

Is not need to explain the basics to me.

I am just saying that it is hard to believe that among 150.000 investors is 12.0+% the real average number.

As of 25th July 2019 I am seeing a 12.22% average net annual return advertised on the Mintos website, with 162,168 investors from 69 countries.

I believe all those statistics are true.

The net annual return they quote might actually be two slightly different things. First, it could be the average return across all the loans listed on Mintos over the past 365 days. Secondly, it could be the actual returns obtained by investors on Mintos over the past 365 days. Whichever the case, the two statistics shouldn’t differ too much. Since I obtained a rate of return slightly less than 12% and am quite conservative with my auto-invest settings, I don’t have any reason to doubt Mintos’ claims about the average return being 12%.

Conor

I have around 10.000€ in Mintos and my NAR is 12.8%

So yes, it is very possible to have averages of 12% or more

Maybe you have many long term loans that pay less than 12 or 11%

Maybe you withdraw some of the profits (by not having interest compounding it can also affect your NAR)

How would it not be a real number 12%? If you have a low risk aversion, you can easily have a portfolio where each company has max 10% of the portfolio and make above 15%. I’m honestly more surprised at why he only makes 11.

Well, Eurocent, Aforti and so on…

https://blog.mintos.com/automatic-repayments-and-buybacks-of-aforti-finance-loans-suspended-on-mintos/

Yes, I don’t expect Eurocent will be the last, and I wouldn’t be surprised if Aforti will be the second loan originator to go bankrupt. This is how the game is played, and ultimately it’s about having bigger profits than the losses.

Hi, did you have to provide some info on your incomes to Mintos? I heard over 50 k euro and over 100 k euro they ask some proves on invested funds – like salary, info on your bank account transfer etc. ? When I reached 50 k they just asked some questions without asking for documents but they mentioned that if I reach 100 k they will ask for some documented proofs.

They might be doing that on a case-by-case basis, but so far they haven’t asked me for anything.

If you have your house in order and they ask for documents it should be a minor inconvenience and nothing more than that, so I’m not worried about it at all.

I have recently started investing in Mintos, and for the time being, my feedback is a very positive one.

Until now, I am using exclusively Invest&Access, which seems to be very good for keeping liquidity.

I am still in the process of getting to know the platform. Right now, I am observing how the ‘My Investments’ apportionment moves from one week to the next (in terms of investments and how many of them are late). From what I understood, this affects the liquidity of my overall investment since you cannot liquidate investments which are late.

Glad you’re liking Mintos Chris! Invest&Access is a great way to dip your toes and get to know how the platform works. In fact, as you are probably aware, I recently published a review of Mintos Invest&Access on this blog.

Once you’re confident with how things are going, you can set up an auto-invest system to take things to the next level. I will be publishing a guide on how to set up auto-invest on Mintos soon.

Thanks for the article. I wasn’t so sure about it at first as it sounded too good to be true! I will surely give it a try Jean!

You’re welcome Roderick! Be sure to check out my full review of Mintos too.

how do you keep track of the different investments in different platforms? a simple excel file comes to mind, but maybe there is an app for this that makes it easier.

I use an excel file and find it convenient enough. On the last day of every month I login to every platform to see how things stand, note the investment value and make any necessary adjustments to auto-invest profiles, make withdrawals and deposits, and even invest in new projects. That way I only spend one day every month on these platforms, which I feel give me a good return with regards to time spent VS money earned.

Recently started out on mintos with invest and access. So far so good. I like the high liquidity part. Until now i have been investing in property crowdfunding, but over the next few months i will probably be expanding my mintos holding.

Glad you are liking Mintos Invest & Access Chris. I’m looking forward to Mintos’ transition into a bank alternative in the coming months, and this is the first step towards that stage.

Property crowdfunding is also a good investment and quite different from P2P lending, but both have a place in an alternative investment portfolio.