The crypto lending landscape looks nothing like it did in 2023. Nexo left the US market entirely in 2022, paid a $45 million settlement, and then came back in February 2026 through a partnership with Bakkt. YouHodler, meanwhile, has been quietly building out its feature set and pushing into EU regulatory compliance under MiCA.

So which platform actually deserves your crypto in 2026? I’ve been tracking both for years, and the answer isn’t as simple as it used to be.

Quick Comparison: YouHodler vs Nexo in 2026

| Feature | YouHodler | Nexo |

|---|---|---|

| Top Stablecoin Yield | Up to 18% (USDT, USDC) | Up to 12% (fixed-term, Platinum) |

| BTC Yield | Up to 9% | Up to 5% |

| ETH Yield | Up to 9% | Up to 5.5% |

| Payout Frequency | Weekly | Daily |

| Max Loan-to-Value | 90% | 50% |

| Loan APR | Higher (trade-off for higher LTV) | From 2.9% |

| Supported Cryptos | 50+ | 100+ |

| Crypto Card | No | Yes (Europe only, Mastercard) |

| Native Token Required? | No | Yes (NEXO token for best rates) |

| US Availability | No | Yes (relaunched Feb 2026) |

| Regulation | Swiss & EU (Italy, MiCA) | Multi-jurisdictional (US, EU, AU, HK) |

| Insurance | $150M (Ledger Vault) | $150M+ (multi-custodian) |

| AUM | Not disclosed | $11B+ |

What is YouHodler?

YouHodler is an EU and Swiss-based crypto financial services platform headquartered in Lausanne, Switzerland, with operations in Italy. The platform’s bread and butter is crypto-backed lending and yield accounts, but it has expanded significantly over the past few years.

YouHodler is registered as a Virtual Asset Service Provider (VASP) in Italy under MiCA-aligned regulation, and operates under Swiss regulatory frameworks. The company is also a member of the Crypto Valley Association and the Blockchain Association of the Financial Commission.

Today, YouHodler supports over 50 cryptocurrencies and offers crypto-backed loans, yield accounts, crypto conversions, and its proprietary Multi HODL leveraged trading tool.

Read my full YouHodler review for a deeper look at the platform.

What is Nexo?

Nexo has been through quite the journey. Founded in 2018 (though the team’s fintech experience goes back further), Nexo quickly became one of the largest crypto lending platforms globally. Then came the regulatory clash.

In December 2022, Nexo exited the US market entirely after disputes with the SEC and CFPB over its Earn product. In January 2023, the company agreed to a $45 million settlement without admitting wrongdoing.

Fast forward to February 2026: Nexo is back in the US, this time through a partnership with Bakkt (the NYSE-backed digital asset platform). The new US offering includes yield programs, an integrated exchange, crypto-backed credit lines, and fiat on/off-ramps — all structured through US-licensed partners.

Today, Nexo operates in 150+ jurisdictions with $11 billion+ in assets under management, holds licenses including a California Financing Law License, New York BitLicense, ASIC registration in Australia, and a Hong Kong TCSP licence.

Read my full Nexo review for a deeper look at the platform.

Yield Accounts: Where Your Crypto Earns

This is where YouHodler has a clear edge on paper.

YouHodler yield rates (2026):

- Stablecoins (USDT, USDC, DAI, TUSD): Up to 18% p.a.

- EURC: Up to 20% p.a.

- Bitcoin (BTC): Up to 9% p.a.

- Ethereum (ETH): Up to 9% p.a.

- Solana (SOL): Up to 13% p.a.

- Other altcoins (DOT, LTC, etc.): Up to 15% p.a.

Payouts are weekly with compounding interest. No minimum deposit required, and — here’s the big one — you don’t need to hold any native token to access the highest rates.

Nexo yield rates (2026):

- Stablecoins (USDC): Up to 8% (flexible) / up to 12% (fixed-term, Platinum tier)

- Bitcoin (BTC): Up to 5% p.a.

- Ethereum (ETH): Up to 5.5% p.a.

- Solana (SOL): Up to 7% p.a.

- Polkadot (DOT): Up to 13% p.a.

Nexo compounds daily (nice), but the catch is their loyalty tier system. To get the best rates, you need to hold NEXO tokens worth at least 10% of your portfolio (Platinum tier). Without that, you’re stuck with Base tier rates, which are significantly lower.

Also worth noting for European users: due to MiCA regulations, Nexo has restricted stablecoin services in the EEA. As of March 2025, USDT, DAI, USDP, TUSD, and PAXG are no longer available for new fixed terms in the EEA region. USDC remains available.

The bottom line on yield: YouHodler offers higher headline rates and doesn’t force you to buy a native token. Nexo’s daily compounding is a small advantage, but it doesn’t close the rate gap.

One important caveat: very high yield rates in crypto should always raise questions about where that yield comes from. Neither platform is a bank, and neither offers deposit insurance in the traditional sense. Only put in what you can afford to lose.

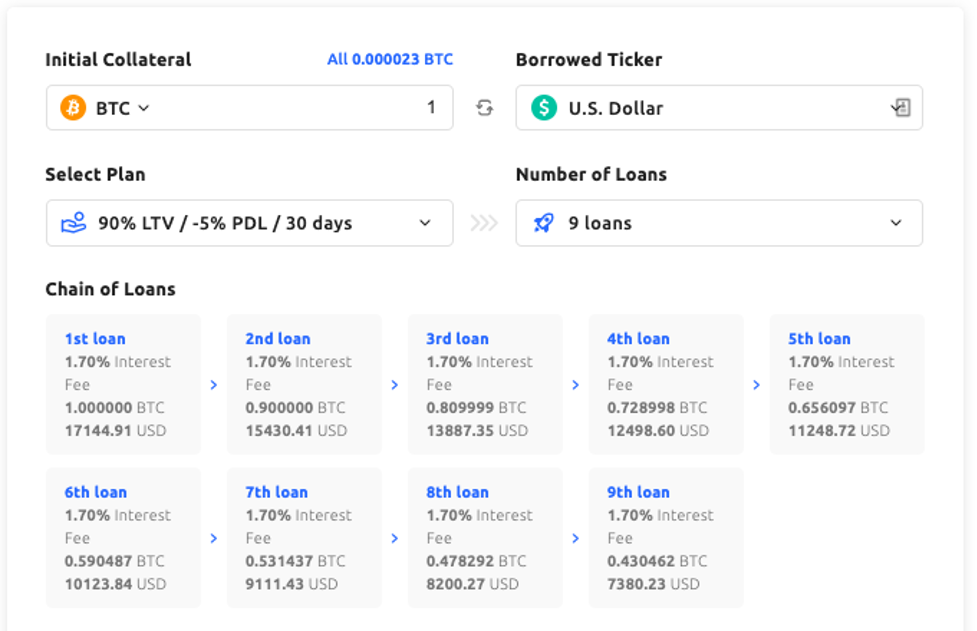

Crypto-Backed Loans

Both platforms let you borrow against your crypto without selling it. The key difference? How much they’ll lend you.

YouHodler:

- Loan-to-Value (LTV) ratio: Up to 90%

- Loan currencies: USD, EUR, CHF, GBP, BTC, stablecoins

- No credit checks

- Low minimum loan amounts

- Instant withdrawals to bank cards

- Loan management tools: Increase LTV, Close Now, Take Profit, Adjust PDL

Nexo:

- Loan-to-Value (LTV) ratio: Up to 50%

- Starting APR: 2.9% (Platinum tier)

- Loan limits: Up to $2 million

- No credit checks, no minimum repayments

- Flexible repayment terms

- More collateral options (100+ cryptos)

YouHodler’s 90% LTV is still the highest on the market. If you have $10,000 in BTC, YouHodler will lend you up to $9,000. Nexo caps it at $5,000. That’s a meaningful difference if you need maximum liquidity.

But Nexo counters with much lower borrowing costs. Starting at 2.9% APR (Platinum tier), Nexo’s loan rates are among the cheapest in crypto lending. YouHodler charges higher interest on loans — it’s the trade-off for that aggressive LTV ratio.

Short version: Need maximum cash from your collateral? YouHodler. Planning to borrow a larger amount over a longer period and want the lowest cost? Nexo.

Unique Features

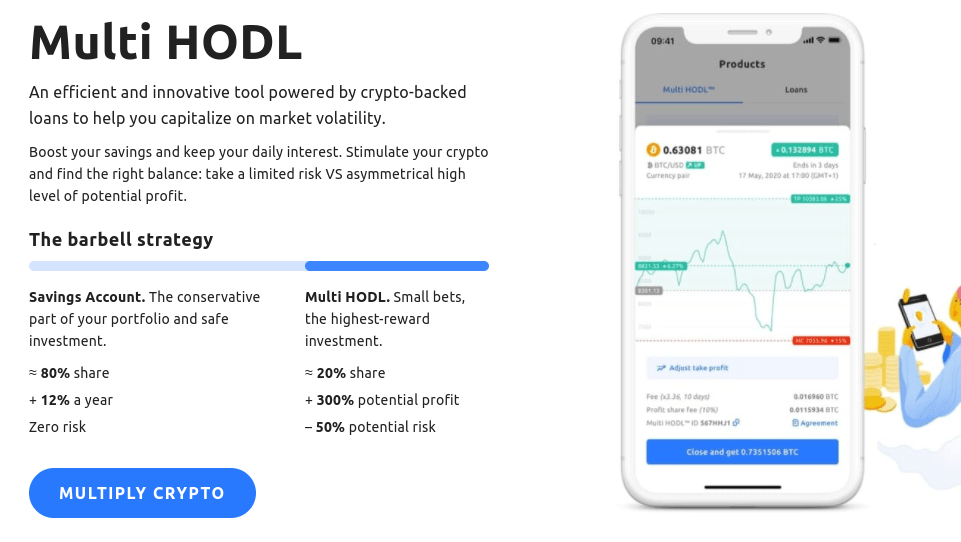

YouHodler’s Multi HODL

Multi HODL remains YouHodler’s most distinctive feature. It’s essentially a leveraged trading tool powered by the crypto-lending engine, letting you take positions in both bull and bear markets with up to 10x leverage. You can earn interest on your Multi HODL balance if the funds come from a savings account.

It’s not for everyone — leverage amplifies losses too — but for active traders who understand the risks, it’s a creative product I haven’t seen replicated elsewhere.

YouHodler also offers Turbocharge (read my Turbo Loans guide) and universal crypto conversion between crypto, fiat, and stablecoins.

Nexo Card

Nexo’s crypto debit card is the standout feature YouHodler can’t match. It’s a dual-mode Mastercard available to European users (EEA, UK, Switzerland) that lets you either spend your crypto directly or borrow against it at point of sale.

Key card details:

- Up to 2% crypto cashback

- No monthly, annual, or inactivity fees

- Accepted at 100+ million merchants globally

- Up to 2,000 EUR in free ATM withdrawals per month

- Virtual card available with $50 minimum balance; physical card requires $5,000+ balance and Gold tier

If you’re a European crypto holder who wants to spend without selling, this is a genuine advantage.

NEXO Token

The NEXO utility token pays dividends and unlocks better rates through the loyalty program. Whether this is a pro or con depends on your perspective — some see it as an incentive, others see it as a requirement that adds exposure to a platform-specific asset.

Safety and Security

YouHodler:

- $150 million pooled crime insurance via Ledger Vault

- 3-factor authentication

- PCI Security Standards for card operations

- Cryptocurrency Security Standard (CCSS) compliant

- Regular external security audits

- Fiat funds held at European and Swiss bank accounts

- Regulated in Switzerland and EU (Italy, MiCA-aligned)

Nexo:

- $150M+ insurance across multiple custodians

- SOC 2 Type 2 certified

- 2FA with biometric options

- Multi-custodian approach (BitGo, Ledger Vault, others)

- $11B+ in assets under management

- Licensed in multiple jurisdictions (US, EU, Australia, Hong Kong)

Nexo has a clear edge here in 2026. The combination of multi-jurisdictional licensing, SOC 2 Type 2 certification, and $11B+ AUM gives it stronger institutional credibility. The US relaunch through Bakkt’s compliant infrastructure also signals a more mature regulatory posture.

That said, YouHodler’s Swiss base and MiCA compliance aren’t nothing. Both platforms are significantly more transparent and regulated than the crypto lending platforms that collapsed in 2022.

The standard warning applies to both: these are not banks. Your crypto deposits are not covered by FDIC or equivalent insurance. Use a hardware wallet for long-term storage and only keep on these platforms what you’re actively lending or earning with.

Availability

YouHodler: Available in 100+ countries, but not available in the USA, Canada, China, or several other restricted jurisdictions.

Nexo: Available in 150+ jurisdictions, including the US (as of February 2026). The Nexo Card, however, is limited to European residents (EEA, UK, Switzerland).

This is a significant differentiator. If you’re a US-based investor, Nexo is the only option of the two. European investors have access to both.

YouHodler vs Nexo: The Verdict for 2026

The competitive landscape between these two has shifted meaningfully since 2023.

Choose YouHodler if you:

- Want the highest yield rates without buying a native token

- Need a high LTV ratio on crypto-backed loans (up to 90%)

- Want access to leveraged trading tools like Multi HODL

- Are based in Europe or another non-US region

- Prefer simplicity — no loyalty tier hoops to jump through

Choose Nexo if you:

- Are based in the US (YouHodler isn’t an option)

- Want a crypto debit card (Europe)

- Need a large, longer-term loan at the lowest possible rate

- Value a platform with the widest regulatory coverage and largest AUM

- Don’t mind holding NEXO tokens to unlock the best rates

For European users who don’t need a card and just want the best rates, YouHodler remains the stronger choice. The yield gap is substantial, the 90% LTV is unmatched, and you don’t have to buy a platform token to get the full experience.

But Nexo’s comeback story is impressive. The US relaunch, multi-jurisdictional licensing, and $11B+ in AUM make it a more institutional-grade platform than it was three years ago. If you value regulatory breadth and are comfortable with the loyalty tier system, Nexo is a solid choice.

My advice? Don’t put all your eggs in one basket. Using both platforms for different purposes — one for yield, one for borrowing or card spending — is a perfectly valid strategy, as long as you understand the risks involved with any centralized crypto platform.

For other ways to put your crypto to work, check out my roundup of the best crypto interest accounts.

Frequently Asked Questions

Is YouHodler or Nexo safer?

Both platforms use Ledger Vault custody with $150M+ in insurance coverage, but Nexo has an edge in 2026. With SOC 2 Type 2 certification, licensing in multiple jurisdictions (US, EU, Australia, Hong Kong), and $11B+ in assets under management, Nexo has stronger institutional credibility. That said, neither platform is a bank, and your deposits are not covered by government insurance. Only use funds you can afford to lose.

Can US residents use YouHodler or Nexo?

US residents can use Nexo, which relaunched in the US in February 2026 through a partnership with Bakkt. YouHodler is not available in the US and has no announced plans to enter the market. If you’re US-based, Nexo is your only option between the two.

Do I need to buy NEXO tokens to use the platform?

You don’t need NEXO tokens to use the platform, but you’ll need them for the best rates. Nexo’s loyalty program has four tiers (Base, Silver, Gold, Platinum), and you unlock higher yields and lower borrowing rates by holding NEXO tokens worth 1%, 5%, or 10% of your portfolio respectively. YouHodler has no such requirement — everyone gets the same rates.

Which platform has better crypto-backed loans?

It depends on what you prioritize. YouHodler offers up to 90% loan-to-value (the highest on the market), meaning you can borrow more against your collateral. Nexo offers lower interest rates starting at 2.9% APR but caps LTV at 50%. For short-term, high-liquidity needs, YouHodler wins. For larger, longer-term loans at lower cost, Nexo is better.

What happened to Nexo in the US?

Nexo exited the US market in December 2022 after failing to reach agreement with the SEC and CFPB over its Earn interest product. In January 2023, the company paid a $45 million settlement without admitting wrongdoing. In February 2026, Nexo returned to the US through a compliant framework built on Bakkt’s infrastructure, which holds US money transmitter licenses and a New York BitLicense.

Are the high yields on these platforms sustainable?

High yield rates in crypto lending should always be approached with caution. The yields come from lending activities, margin trading fees, and the spread between borrowing and lending rates. When crypto markets are volatile, these yields can change quickly. Both platforms have survived the 2022 crypto winter (unlike Celsius, BlockFi, and Voyager), which is a meaningful data point, but past performance doesn’t guarantee future safety. Diversify across platforms and keep most of your crypto in self-custody.

Related

Nexo’s Card is a myth. I’am a long time Nexo user, there is no way one can get the Nexo Card.

Hoi,

Allereerst bedankt voor je informatieve artikel. !!!

Het gaat wel hard in de crypto spaar-/leenwereld. Onlangs heeft nexo haar spaartarieven drastisch verlaagd en ook is onbeperkte gratis opname niet meer mogelijk. Kennelijk normaliseert dee wereld nu ook. En dat is m.i. prima.

Ik mis overigens wel een groot voordeel van Nexo boven YouHodler in je artikel. Bij Nexo kunt je fiat sparen en bij YH niet. Tenminste dat begrijp ik hieruit.

Fiat sparen kan bij Nexo tegen redelijke percentages ( nu 6%, was 10% voor platinum-deelnemers. Onlang flinl verlaagd dus, maar nog altijd veel meer dan bij de ING etc..

De exchange van nexo ( is betrekkelijk nieuw) en rekent ca. 2% . Een stuk minder dan bij exchanges zoals zoals Bitcoinmeester (5%!)

Ik ga nu beslist ook even kijken bij YH.

Groet, Jacques

het

I’d love to read your comment if you could redo this in English.