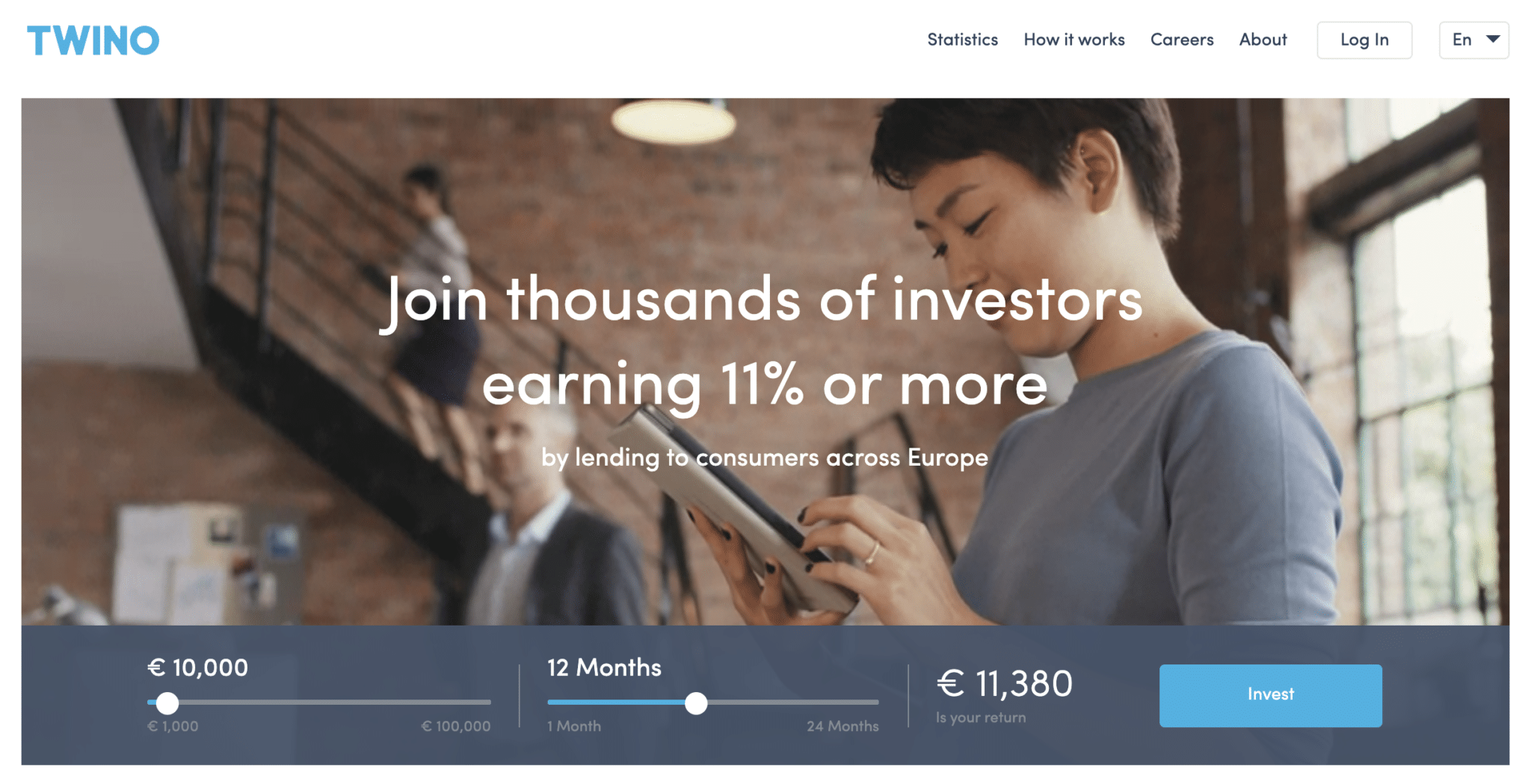

Twino was one of the first P2P lending platforms I invested in. It launched in Latvia in 2009 (the web platform went live in 2015), and for years it was a reliable part of my portfolio. I earned a steady 9%+ with zero defaults. But a lot has changed since then. The Russia-Ukraine war froze […]

Teaching Kids How to Code

In today’s fast-paced, technology-driven world, it’s no secret that coding has become an essential skill for everyone, including children. The ability to code can open up a world of opportunities, from creating apps and websites to developing software and even designing robots. In this article, I’ll share my journey on teaching my kids how to […]

What Snow Chains Do You Need for the Pyrenees in Spain and Andorra?

Every winter I travel to Andorra or Spanish ski resorts, and an essential part of my travel gear are snow chains or snow socks. Here’s my research and recommendations on the subject. When it comes to safety and security, I always go for the best even if it means spending a bit more money. For […]

Should Freelancers Set Up a Company in Estonia?

Estonia has become one of the most popular places for European freelancers to set up a company. The combination of a genuinely digital-first government, EU legitimacy, and a deferred corporate tax system makes it stand out from almost every other jurisdiction. In this article I want to look at why tens of thousands of freelancers […]

My Hardware Setup

With the new M2 processors introduced by Apple and their amazing performance, I’ve decided to switch around my hardware setup to be best suited to my lifestyle. Here’s what I have selected after doing my research. Macbook Pro 16″ M2 This will be my main machine and will be used at home and at my […]

Best Books for Kids

Reading to children from a young age is one of the best ways to develop their language skills, imagination, and love of books. I’ve spent an inordinate amount of time reading to my kids, as it was an integral part of their evening (and sometimes morning) routines. I am a big believer in the power […]

Learning to Play the Piano

I’ve always been hugely into music and dreamed of playing instruments as a young kid. However, for some reason or another, I never went for any classes in a serious way when I was young. I did learn basic guitar which I enjoyed, but never practiced enough to do anything with it. The piano is […]

Best Toys for Kids – What My Children Love Playing With

When choosing toys for your kids, it’s important to consider their interests, abilities, and developmental stage. Look for toys that are age-appropriate, safe, and durable. Avoid toys with small parts that could be choking hazards for younger children, and be sure to read the labels and instructions to ensure that the toy is suitable for […]

My Philosophy on Health and Longevity

Physical health is the foundation everything else rests on. You need it to practice sports, play with your kids, and move through life without pain. Without it, all the other forms of wealth — financial, social, mental — are harder to build and harder to enjoy. Most people understand this in theory but fail to […]

On Family Inheritances, Parent-Child, and Sibling Money Matters

Here are some notes on family inheritances. This can be a heavy subject for many families, and now that I am both a child and a parent, it makes sense to think about the topic and try to plan early. We start off with the fact that parents owe nothing to their children financially. Most […]

My Favorite Books, Blogs & Essays

Note: This list is just a small taste of books that have played an important part in my life. I’ve read hundreds of books and it has proven to be impossible to keep a definite updated list of favorite books. Here’s the one biggest catalyst for most of my successes in life: being a voracious […]

A Collection of Thoughts and Life Lessons

These are some of my thoughts and lessons that I’ve learned over the years and want to share here. At some point, I might dig deeper into some of these topics and split this up into several articles. In the meantime, enjoy and do let me know if you have any thoughts of your own […]

- « Previous Page

- 1

- …

- 10

- 11

- 12

- 13

- 14

- …

- 36

- Next Page »