TL;DR: For most European investors, a simple two-fund portfolio of a global developed markets ETF + an emerging markets ETF, purchased through a low-cost broker like DEGIRO or Scalable Capital, is the most reliable way to build long-term wealth. Keep fees under 0.20%, invest consistently, and don’t try to time the market. Read my ETF […]

My Favorite Online Shops in Spain

In Spain, a variety of online shopping websites offer fantastic deals on clothing, accessories, and more. If you’re looking to save money on new items, check out our comprehensive list of recommended websites that cater to the Spanish market: Zalando A leading European online fashion retailer, Zalando offers a wide range of clothing, shoes, and […]

My Guide to Personal Productivity Hacks and Apps

For the past twenty years, I’ve been on a journey towards improving my productivity. I’m an ideas guy and it’s very hard for me to stay focused on one thing for long. Adding to that I have a very strong drive to achieve and build things. Mix those two together and you get an explosive […]

Bondora Review 2026 – Go & Grow Returns, Risks, and My Assessment

Bondora is one of the oldest peer-to-peer lending platforms, and I joined early on in my P2P lending journey, around 2016. While this platform has been criticized by investors in the past, my portfolio has been chugging along quite well over the years, and my only complaint would be about the graphics and UI of […]

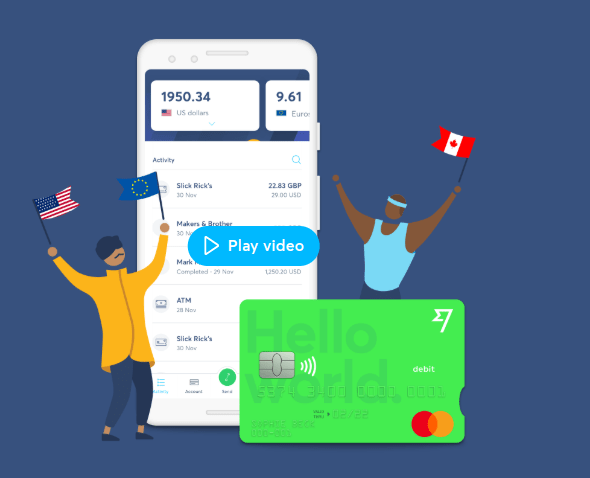

Wise Account Review 2026

I’ve had a Wise account for years, and it sits in my financial setup for one specific reason: nobody else does international money transfers as cleanly or as cheaply. I use Revolut as my primary everyday account and N26 as my European banking backbone — if you’re still deciding between those two, my N26 vs […]

Are You a Multipotentialite?

Over the course of the past couple of years, I’ve learned to identify myself as a multipotentialite. I’ve known since my childhood that I was different from most people in that I had an insanely varied and ever-changing range of interests, but I never knew how to explain why. Reading recent books like Refuse to […]

Revolut Review 2026 – An Essential Digital Banking Solution

Revolut is fast becoming one of the most popular challenger banking apps around. Learn what it has to offer and why over 10 million people have chosen Revolut for their banking needs.

Why I Write & How it Helps Me

I frequently get asked why I blog so regularly, especially in the age of Instagram, Twitter, Snapchat and all the other social media platforms that are all about short form and quickly digested content. In this post, I’ll explain why publishing my thoughts is by far the most rewarding activity for me online. A Lifelong […]

How to Migrate Emails from One Account to Another

Email migration sounds like it should be simple. Copy the emails, paste them somewhere else, done. In practice, it’s one of those tasks that can go sideways in several different ways depending on what you’re moving, where you’re moving it, and how many accounts are involved. I manage email across multiple company accounts and have […]

Beginner’s Guide To Website Flipping: How To Start Investing In Digital Assets

I’ve been involved in the web industry for around twenty years, and one thing that’s always fascinated me is the possibility of buying and selling websites. I’ve touched on this in my guide to investing as well. While this has perhaps been the domain of technical people 10+ years ago, in the last few years […]

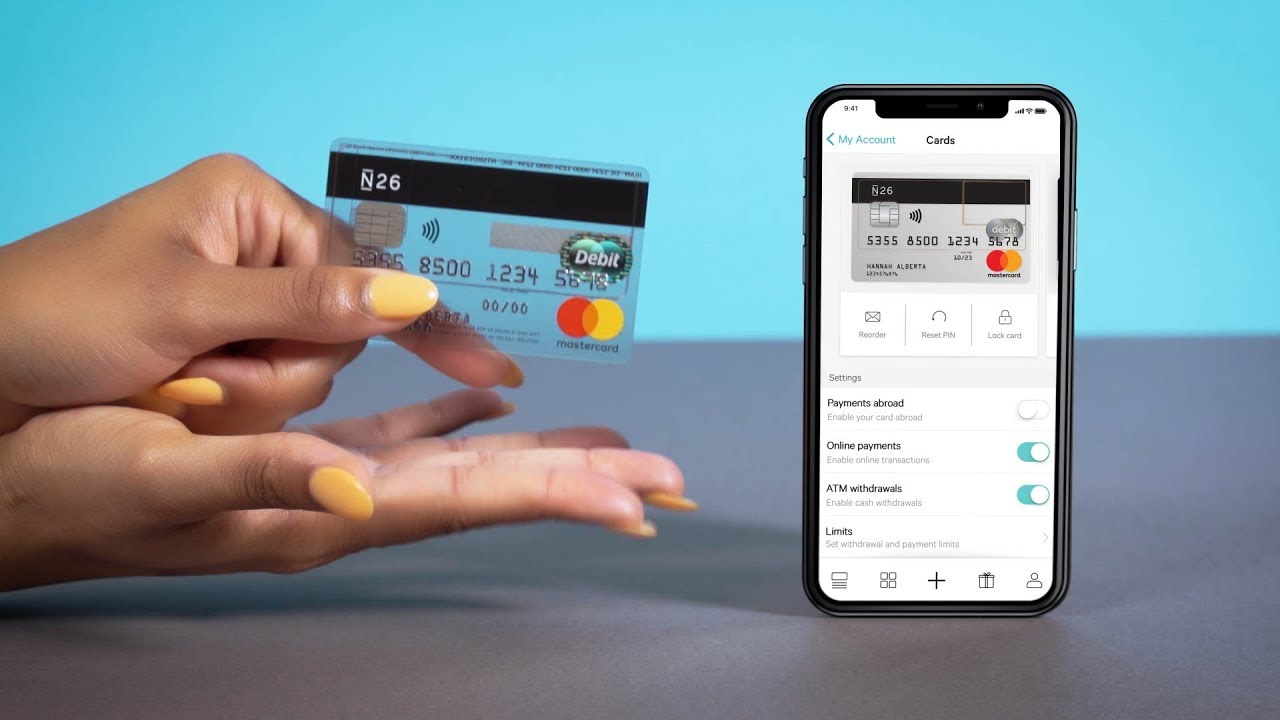

N26 Review: Mobile Banking at the Click of a Button

I’ve had an N26 account for several years. It sits alongside Revolut in my financial setup — not as a replacement, but as a complement. If you’re considering N26, that context matters: I’m not going to tell you it’s the only account you’ll ever need. But I am going to tell you why it earns […]

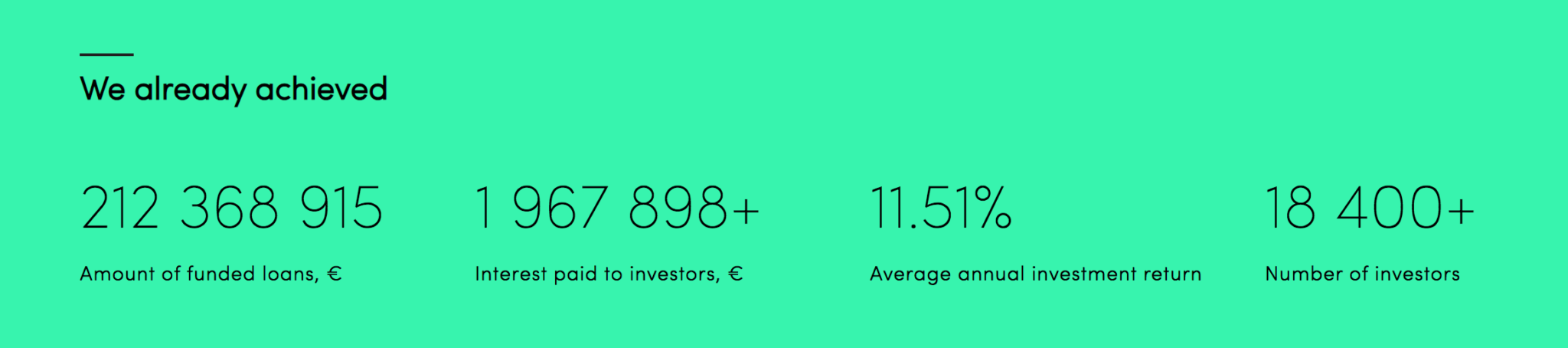

PeerBerry Review 2026 – Returns, Risks, and My Honest Assessment

Launched in 2017, PeerBerry has been gaining quite a lot of popularity among peer-to-peer platforms recently. As with many crowdlending platforms, PeerBerry originated in the Baltics – specifically Riga, Latvia. As of 2026, PeerBerry has grown to become one of the largest P2P lending platforms in Europe, with over 110,000 registered investors and more than […]

- « Previous Page

- 1

- …

- 20

- 21

- 22

- 23

- 24

- …

- 35

- Next Page »