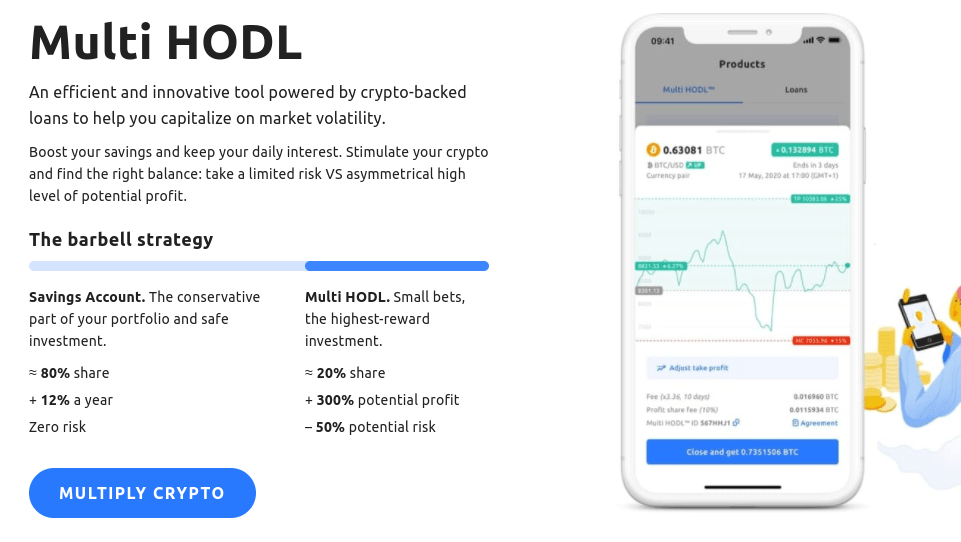

If you hold crypto and you’re not doing anything with it, you’re leaving money on the table. YouHodler is the platform I use to earn yield on idle holdings, borrow against crypto without selling, and occasionally take leveraged positions on the market. I first covered YouHodler back in 2020. A lot has changed since then […]

Spotlight Review – Easily Add Instagram Feeds to Your Site

This week was a very special one for us at RebelCode. It marks the launch of our latest plugin: Spotlight – a simple and effective way to add your Instagram feeds to your WordPress site.

What Are Good Operating Margins for WordPress Businesses?

WordPress businesses sit in a strange spot. The underlying platform is free and open source, but the businesses built on top of it — plugins, themes, hosting, SaaS products, managed services — can be extraordinarily profitable. The challenge is knowing what “good” actually looks like. Having run WordPress businesses for over a decade across plugins, […]

How to Start a Blog with WordPress

Starting a blog is a fun and rewarding experience. However, on the other hand, it can also be portrayed as being as daunting as it is interesting. Often, people are very interested in starting their own blog but struggle to get to grips with how to go about starting one from scratch. The purpose of […]

Swaper Review 2026 – A Top P2P Lending Platform

In this review, I’ll be taking a look at Swaper, one of my favorite P2P lending platforms in both function and design. Swaper is one of the latest entries into the P2P lending space in Europe, having started operations in May 2019. They have found success pretty quickly though, amassing more than 4000 active investors, […]

The Best Bitcoin and Crypto Interest Accounts in 2026

Earn interest on crypto Did you know that you could earn interest on Bitcoin, Ethereum and other crypto-assets that you own? Bitcoin has been criticized by certain people in the past for being an asset that does not yield any dividends, but this argument no longer holds any water. Important context: The crypto lending sector […]

Differences Between the US and Europe for Credit Scores, Credit Card Rewards etc

For many years I struggled to understand the lingo used in movies and books that came from the US with regard to money and finance. Here are a few terms that you are most likely to encounter that have no real parallel here in Europe. If you need me to explain anything else just leave […]

Coinbase Review 2026 – The Best Crypto Exchange for Beginners

Open a Coinbase Account Coinbase is the most regulated crypto exchange in the world and the go-to platform for investors who put compliance and safety above all else. Founded in 2012, it became the first major crypto company to list on NASDAQ (ticker: COIN) — a level of public accountability no other major exchange comes […]

eToro Review 2026 – Is It the Best Social Trading Platform?

Note: This review only applies to non-US residents. eToro is a Jack of all Trades in the online investment space, with the broker offering a full range of asset types that can be purchased at the click of a button. Now a publicly traded company on the Nasdaq (it went public in May 2025 at […]

Can Digital Nomads Legally Pay No Taxes?

I spent a good part of my twenties traveling around the world during what was the start of the digital nomad movement. A recurring theme I kept hearing was the possibility of optimizing taxes by being a digital nomad. Just walk into any co-working space in South-East Asia, and a 20-year-old from the EU or […]

How to Remove DRM from Amazon Books

Every Kindle book you buy comes locked with Digital Rights Management (DRM). That means you can only read it through Amazon’s own apps and devices. You can’t convert it to EPUB, you can’t open it in Calibre, and if Amazon ever decides to pull a title or shut down your account, those books are gone. […]

Is it Stupid to Travel While Renting Long-Term?

I spent the latter half of my twenties traveling the world, and now that I’m in my mid-thirties, a topic that comes up with my wife and friends is whether it makes financial sense to still do any long-term traveling while also renting an apartment at our home base. In our twenties, we could fit […]

- « Previous Page

- 1

- …

- 19

- 20

- 21

- 22

- 23

- …

- 36

- Next Page »