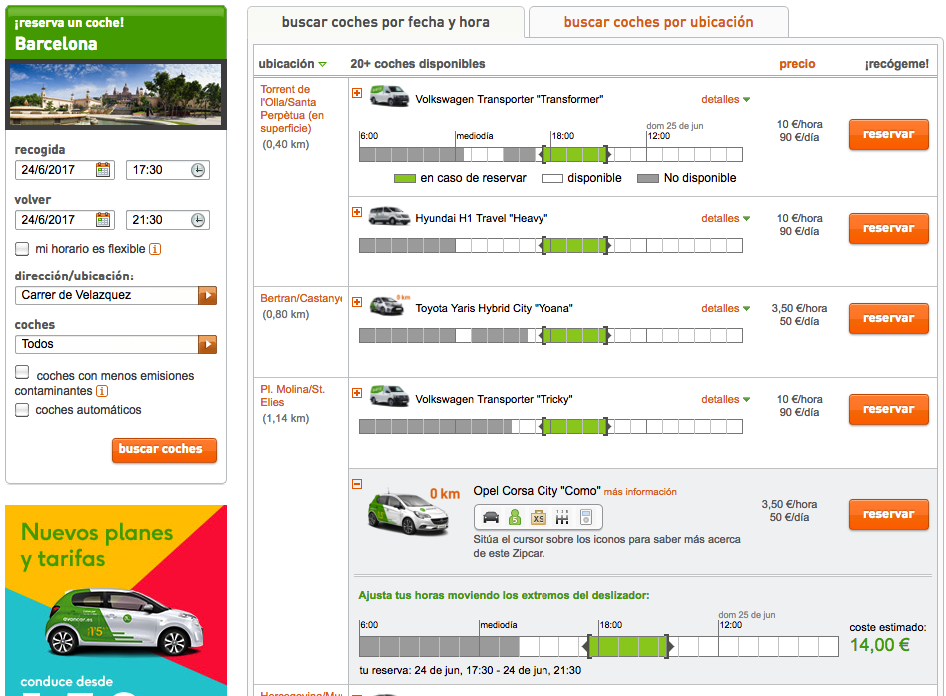

If you are staying in Barcelona for a few months, or have moved there permanently (great decision!), you probably know that transportation options abound. You have the metro, bicycles, buses and of course, you can always opt to walk around. However, Barcelona is also the city with the biggest density of scooters in Europe. You’ll […]

How to Find a Coworking Space in Barcelona

Coworking spaces are a great way to get to know people and get work done, especially if you don’t have a home office and need a place where you can focus and immerse yourself in your project. I’ve already written about the elements that make up the ideal coworking space, so armed with that knowledge, […]

Division of Matrimonial Assets in Spain

If you’re a foreign national living in Spain and you’re married, you should be well informed about the economic systems of marriage that exist in Spain and how they apply to you. The basics – Two types of Spanish systems of marriage In Spain, there are two standard economic types or systems of marriage: ‘separación de […]

How to Secure a Synology DiskStation – A Complete Security Guide

The Synology DiskStation is a great tool for backing up your files and acting as a central media storage device. Since it will host so much important data — family photos, documents, backups of all your devices — securing it properly is critical. Out of the box, a Synology NAS is reasonably secure, but there […]

Best Health Insurance Options in Spain for Expats

If you are an expat in Spain and you’re looking for private health insurance, there are three major players worth seriously considering: Sanitas, AXA, and Adeslas. Each offers unique strengths depending on your priorities—be it global flexibility, national coverage, or doctor freedom. Let’s take a look at all three so you can make an informed […]

When and How to Use Two Factor Authentication

Two-factor authentication or 2FA is a way of making your logins more secure, by not only requiring a username and password when signing in, but also a special extra code that can either be received as an SMS or else generated by an app or device. Most of you will already have used 2FA, perhaps […]

The Best Discount and Deals Websites in Spain

If you’re living in Spain you are spoilt for choice when it comes to deals and discounts websites. We have a wealth of choice for getting great prices on travel, house decor, experiences, clothes and much more. Let’s have a look at my favorite websites. Privalia Privalia is an online fashion outlet, with daily flash […]

Buying Food in Spain – Supermarkets vs Local Markets and Specialized Stores

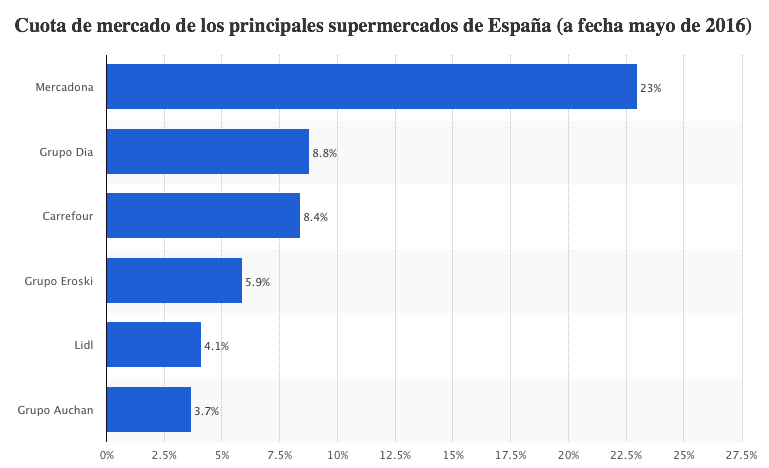

In Spain, you have many options for buying food, but as you can imagine, there are significant differences between the options. Let’s have a look at these sources. First up, you have the traditional supermarkets. The Spanish market is dominated by a few big supermarket chains: Mercadona Dia Carrefour The closest version to an organic […]

The Best European P2P Lending Platforms in 2026

I’ve been investing in P2P lending since 2016. Over that time I’ve put real money into more than a dozen platforms, watched several fail, and seen others grow into properly regulated businesses that now manage hundreds of millions in investor assets. The market looks very different in 2026 than it did when I started. Four […]

Spain – The Best Quality of Life in Europe

One of my close friends sent me an email recently to tell me that he was considering moving to Spain from the UK following the UK’s Brexit vote and how things are developing over there. He is already an ex-pat, having moved away from Malta with his family a few years ago. Moving is no […]

Guide to Buying and Driving a Car in Spain

Buying a car in Spain as an expat is more involved than in many other countries. You have to navigate the used car market, understand local depreciation patterns, negotiate with dealers in Spanish, sort out insurance, and figure out what to do if you get into an accident. This guide covers all of it in […]

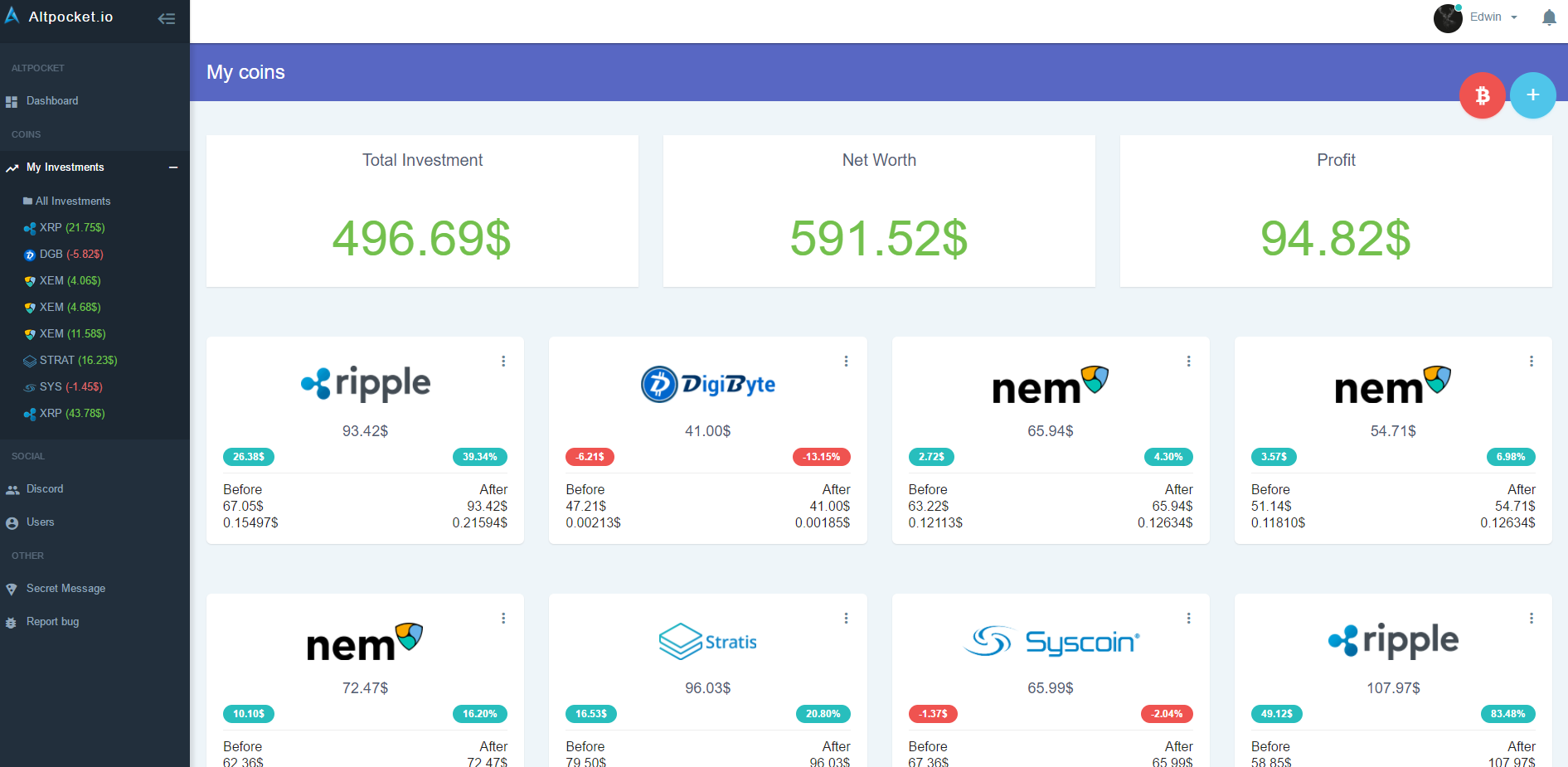

What is the Best Cryptocurrency Portfolio Tracker?

Buy cryptos With thousands of crypto tradeable assets available, it is hard to keep track of your crypto portfolio these days. Even if you’re just buying and selling one or two different coins, you can quickly lose track of things, especially if you’re using several crypto exchanges or trading apps like Coinbase, Binance etc. Not […]

- « Previous Page

- 1

- …

- 20

- 21

- 22

- 23

- 24

- …

- 27

- Next Page »