A carry trade or “carry trading’ is a unique trading strategy where one takes a loan at a low-interest rate and then takes that loan to invest in an asset that provides a significantly higher rate of return. It’s a strategy that has been used in traditional markets for many years between various fiat currencies but lately, many cryptocurrency enthusiasts are using this same strategy with a twist. It’s time to introduce yourself to the crypto carry trade.

A carry trade or “carry trading’ is a unique trading strategy where one takes a loan at a low-interest rate and then takes that loan to invest in an asset that provides a significantly higher rate of return. It’s a strategy that has been used in traditional markets for many years between various fiat currencies but lately, many cryptocurrency enthusiasts are using this same strategy with a twist. It’s time to introduce yourself to the crypto carry trade.

The crypto carry trade: A product of low-interest rates at banks

Before we start diving into the specific of the crypto carry trade, let’s first examine how this strategy made such an efficient transition from traditional markets to digital ones. The culprit here is our beloved central banks.

Central banks all over the world are lowering interest rates in an effort to incentivize investors to buy more assets, stop them from “passively holding” fiat in banks, and in turn, stimulate the economy. Whether this is an effective economic strategy is up for debate and could be the topic of a whole new article. However, the point here is that with low-interest rates (and in some cases, even negative interest rates in Europe), traders started getting creative with how to let these low rates work in their favor.

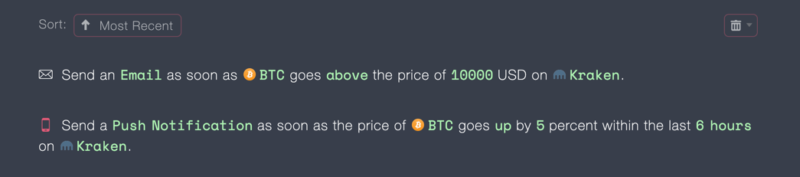

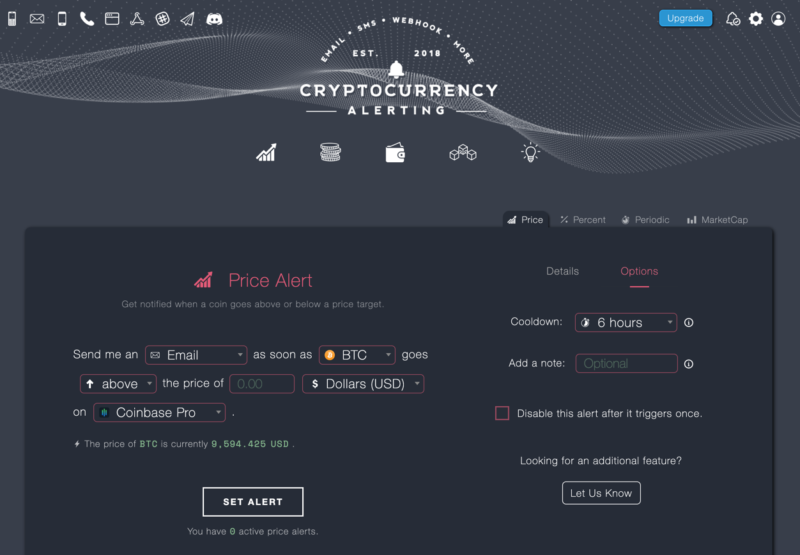

Crypto assets can go through weeks of flat price action, and then suddenly go into a frenzy in a few hours. It is not practical for investors who are not professional traders to keep on top of the crypto markets themselves, also because the market is open 24/7.

Crypto assets can go through weeks of flat price action, and then suddenly go into a frenzy in a few hours. It is not practical for investors who are not professional traders to keep on top of the crypto markets themselves, also because the market is open 24/7.

Irrespective of what your long-term investment goals are – if you plan to

Irrespective of what your long-term investment goals are – if you plan to