Trade on Deribit I’ll start right off by saying if you’re not an experienced trader with a firm understanding of how financial derivatives work, then Deribit won’t be for you. But, if you’re a seasoned investor looking to trade cryptocurrency futures and options, Deribit is well worth considering. The platform offers a huge number of […]

Should You Buy Ethereum Right Now?

Ethereum is the second-largest cryptocurrency by market cap, and that ranking isn’t an accident. It’s earned. While Bitcoin has settled into its role as digital gold, Ethereum has built something categorically different: a programmable platform that underpins a sprawling ecosystem of decentralized finance, smart contracts, and tokenized assets. I hold ETH as part of my […]

The Best European Bitcoin ETFs

As someone who’s been actively involved in the crypto space for over a decade, I’ve seen countless trends come and go. But one thing that’s become increasingly clear is that Bitcoin is here to stay. For those of us in Europe looking for a more traditional, regulated, and perhaps less nerve-wracking way to gain exposure […]

Why Use a Crypto OTC Desk and Why Kraken’s Is Worth Considering

If you’ve been around crypto long enough, you’ve probably noticed that moving big chunks of Bitcoin or Ethereum on regular exchanges can feel like trying to fit an elephant through a doorway. Prices slip, order books dry up, and before you know it, you’ve paid a premium just to get the job done. Enter Over-the-Counter […]

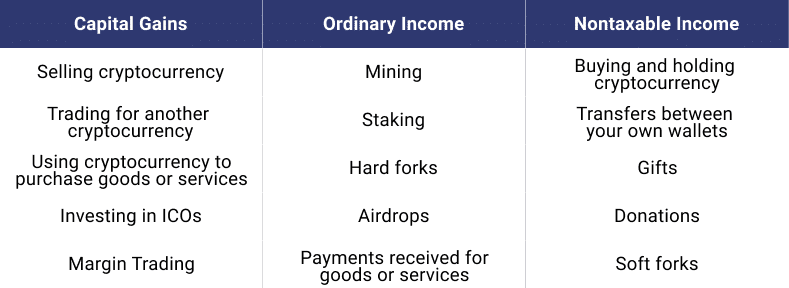

Is Trading Crypto in Portugal Tax-Free?

Portugal was once the undisputed crypto tax haven in Europe, but that changed significantly with the 2023 State Budget. If you’re considering a move to Portugal for crypto-related tax reasons, here’s what you need to know about the current rules. Last updated: March 2026. Tax laws change frequently — consult a qualified tax advisor before […]

Kubera – The All-Inclusive Net-Worth Tracker

Track your wealth with Kubera Up until recently and even to quite some extent today, the asset portfolio of many retail investors will prevalently consist of a standard range of assets. This would often include property, vehicles, company stocks and bonds, retirement accounts and insurance, term deposits and bank accounts. These portfolios are, more often […]

Nexo Review 2026

Get Started With Nexo If you hold crypto and you’re not earning anything on it, you’re leaving money on the table. Nexo is one of the platforms I’ve looked at most seriously for doing exactly that — putting idle digital assets to work while staying invested. In this review I’ll walk you through what Nexo […]

Cointelli Review – Automated Tax Reports for Crypto Transactions in the US

Automize your crypto tax report with Cointelli Over the past years, the cryptocurrency sphere has evolved into a vast and complex reality where enthusiasts and investors alike can access a multitude of financial products that come in all sorts. And if (like me) you are one of them, you will likely be actively using multiple […]

The Best Crypto Podcasts in 2026

One of the main ways that I keep updated with all the stuff that’s happening in the crypto space is through podcasts. I also run my own podcast at Mastermind.fm. Here are my favorites, categorized based on the majority of the topics they cover. The Rabbit Hole These are podcasts that are ideal for understanding […]

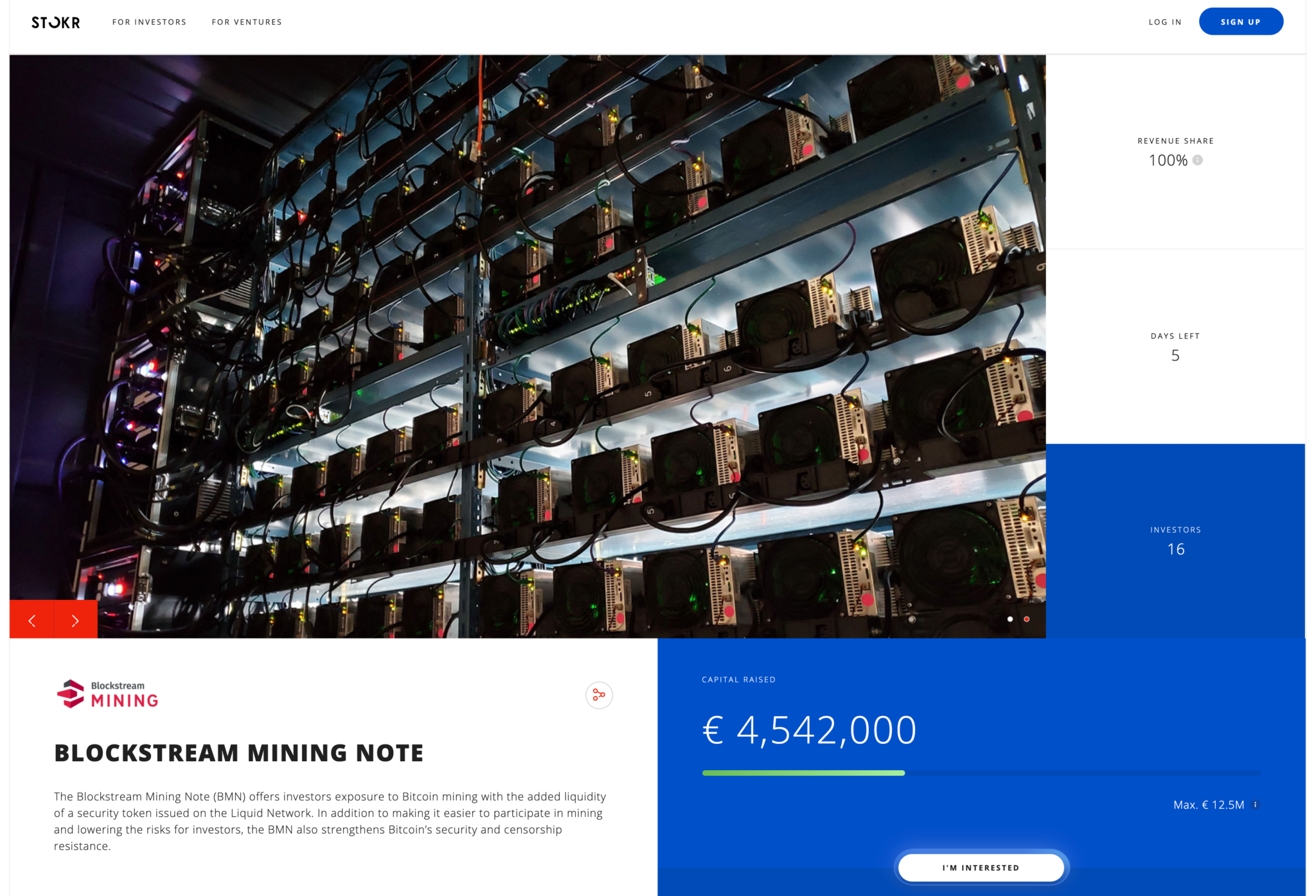

How to Invest in Bitcoin Mining

Bitcoin mining is a great way to approach investing in Bitcoin from a different angle. There are several ways that you can get involved with Bitcoin mining for profit. In this post, I’ll take a look at how you can get exposure to Bitcoin mining in various ways, and some considerations to keep in mind. […]

Best Platforms for Dollar Cost Averaging in Crypto

Let’s start off the article by making sure everyone is on the same page. It’s time to define this mysterious term and explain what DCA means. DCA (or Dollar Cost Averaging) is a technique that’s used to average your buying price or is used as the “Martingale technique”, which you use when a position is […]

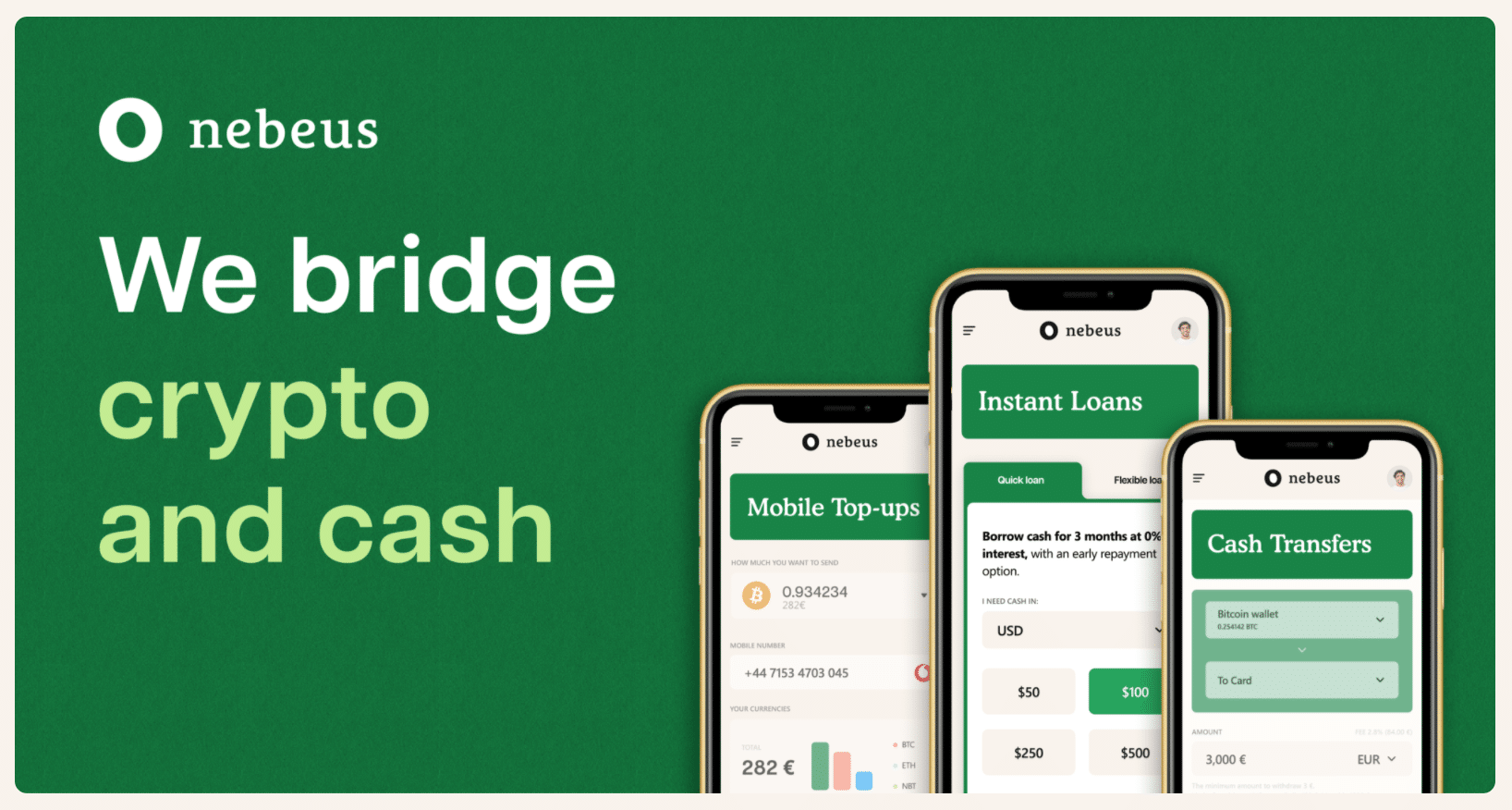

Nebeus Review 2026 – A Crypto-backed Loans Platform

Start earning on your crypto What is Nebeus? Nebeus is a regulated crypto-finance platform founded in 2014 by Sergey Romanovskiy. Based in Barcelona and operating across Europe and the UK, it bridges traditional finance and crypto through a single account — letting you borrow against your crypto, earn yield by renting it out, exchange between […]

- 1

- 2

- 3

- …

- 5

- Next Page »